Why Governance and Communication Drive Post-IPO Value

8 hrs ago

Most Australian investors receive franked dividend statements at least once a year. A significant share do not realise they may be entitled to a cash refund from the Australian Taxation Office (ATO), even if they owe no tax at all. Australia’s dividend imputation system is one of the most shareholder-friendly tax frameworks in the world, yet it remains widely misunderstood. With the ATO now automatically refunding franking credits to eligible recipients aged over 60 from the 2024-25 tax year onward, understanding the system has become more valuable, and more accessible, than ever.

This guide explains exactly how franking credits work, how they are calculated, who benefits and by how much, and what investors need to do to claim what they are owed. By the end, readers will understand their dividend statements, know whether they are entitled to a refund, and recognise the compliance rules that protect their eligibility.

Australian companies pay corporate tax on their profits before distributing what remains as dividends. Without the imputation system, those same profits would be taxed a second time in the shareholder’s hands, once at the company level and again at the individual’s marginal rate. That double-taxation problem is what franking credits exist to correct.

The mechanism is straightforward. When a company pays corporate tax at 30% (or 25% for eligible small business entities), it generates a credit that attaches to the dividend paid from those after-tax profits. That credit, known as a franking credit or imputation credit (the terms are interchangeable), passes through to the shareholder. It represents tax already paid and functions as a direct offset against the shareholder’s personal tax liability.

Franking credits represent tax already paid at the company level, passed through to the shareholder as a credit against their personal tax liability. They exist to ensure company profits are not taxed twice.

The result is that the shareholder effectively pays only the difference between the corporate tax rate and their own marginal rate. For investors whose marginal rate sits at or below the corporate rate, the credit may eliminate the tax liability entirely, or produce a cash refund.

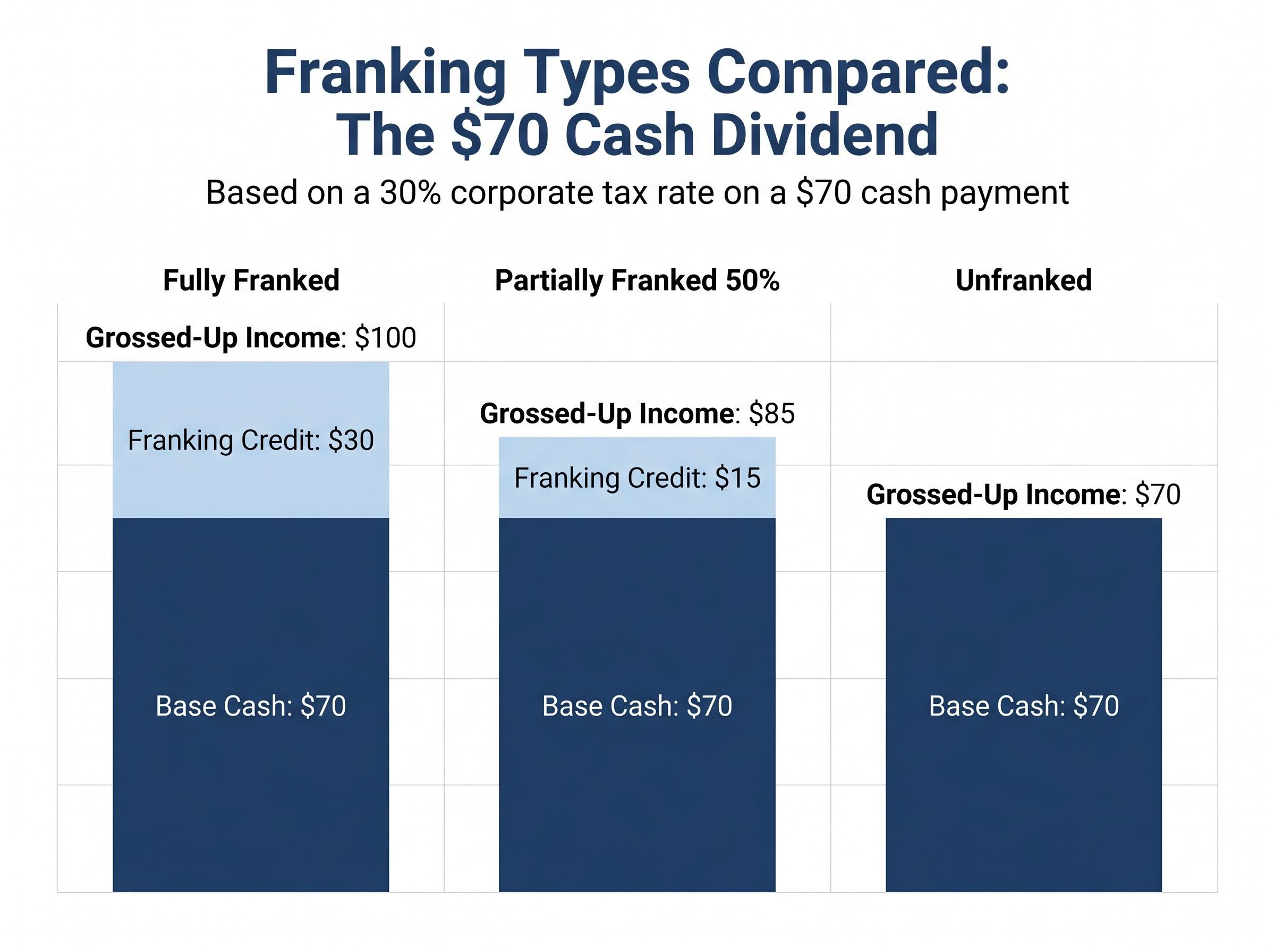

Not every dividend carries the same franking benefit. The distinction between fully franked, partially franked, and unfranked dividends determines how much of the company’s tax payment flows through to the investor, and that difference can materially alter after-tax returns.

A fully franked dividend carries a credit equivalent to the full corporate tax rate on the entire dividend amount. For every $70 received in cash from a company taxed at 30%, a $30 franking credit is attached. The shareholder’s assessable income is grossed up to $100, with the $30 credit available to offset the tax calculated on that amount.

An unfranked dividend carries no credit at all. This typically occurs because the underlying profits were earned or taxed offshore. The full cash amount is taxed at the shareholder’s marginal rate with no offset.

The formula for calculating the credit on any franked dividend is:

Franking Credit = (Dividend Amount / (1 – Company Tax Rate)) x Company Tax Rate

Using a $70 cash dividend at the 30% rate: ($70 / 0.70) x 0.30 = $30. For a company taxed at 25%, the same formula produces: ($70 / 0.75) x 0.25 = $23.33. The rate used always matches the rate applicable to the paying company.

A partially franked dividend sits between the two extremes. If a dividend is 50% franked at 30% on a $70 payment, only half the dividend attracts the credit, producing a $15 franking credit rather than the full $30.

| Franking Type | Cash Dividend | Franking Credit | Grossed-Up Income | Effective Value (Zero-Tax Investor) |

|---|---|---|---|---|

| Fully franked (30%) | $70 | $30 | $100 | $100 |

| Partially franked (50% at 30%) | $70 | $15 | $85 | $85 |

| Unfranked | $70 | $0 | $70 | $70 |

The practical implication is that a lower-yielding fully franked stock can outperform a higher-yielding unfranked one on an after-tax basis. Investors comparing dividend income should assess the franking level before drawing conclusions about which holding delivers the better return.

Franking levels interact directly with income stock valuation: a grossed-up dividend yield adjusted for the refundable credit will produce a materially higher present value than the face cash yield, which means dividend discount models applied to ASX stocks without a franking adjustment systematically understate the income proposition for domestic investors.

The system works in two steps, and both must be understood to see why cash refunds are possible.

That third step is where many investors leave money on the table. The refund mechanism means that franking credits are not simply a tax reduction; they can produce a direct cash payment from the ATO to investors whose tax liability falls below the credit amount.

From the 2024-25 tax year onward, the ATO automatically refunds franking credits to eligible Australian residents aged over 60 who do not need to lodge a full tax return or whose sole reason for lodging is to claim the refund. No application is required for those who qualify.

For individuals who do lodge a return, franking credits are reported at Item 11 (dividends), and any excess credits are refunded automatically through the assessment process. Those not required to lodge who do not qualify for the automatic refund can use ATO Form NAT 4105 to claim.

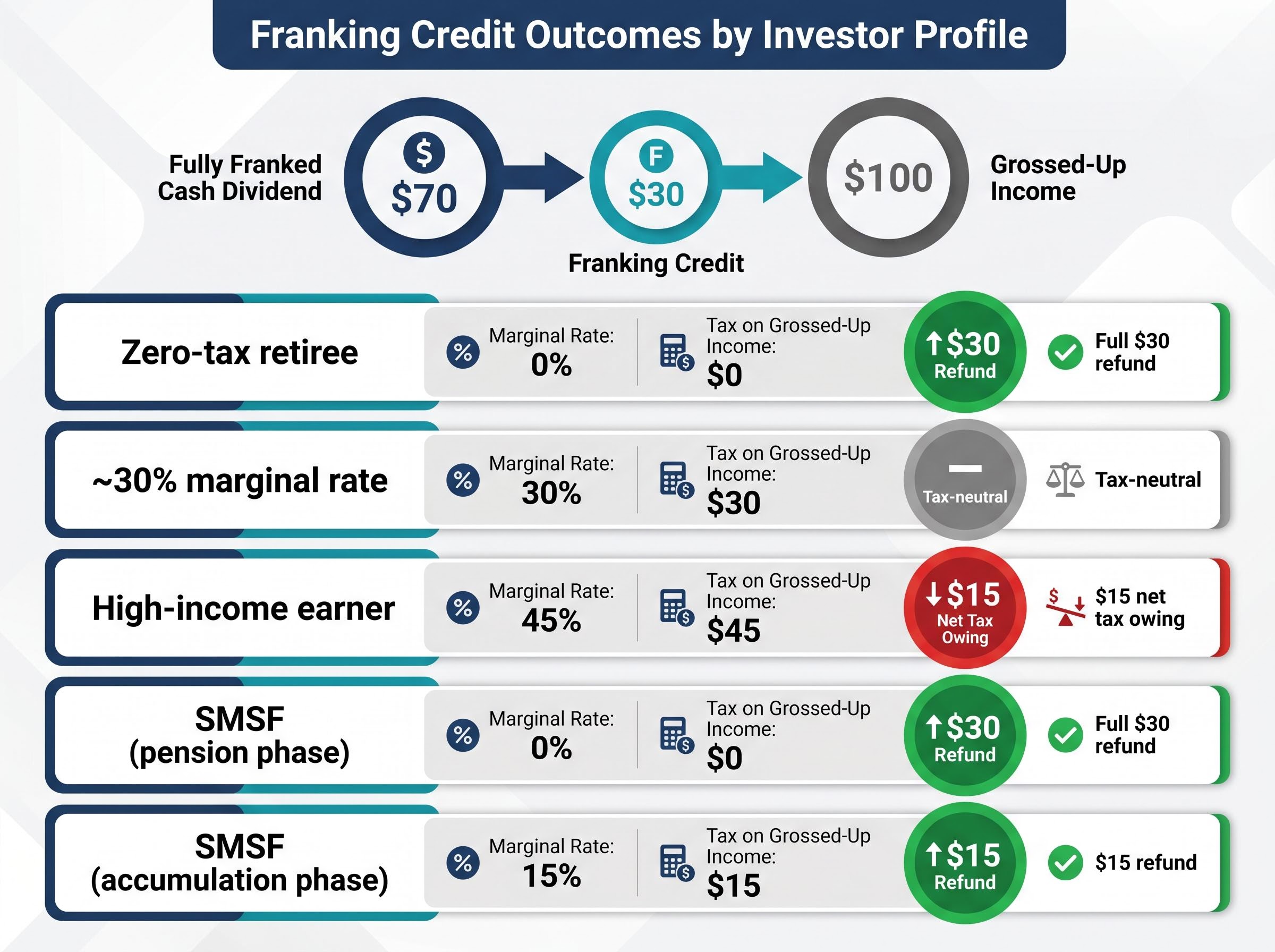

The dollar value of a franking credit depends entirely on the investor’s tax position. The following examples, all based on a $70 fully franked dividend at the 30% corporate tax rate, show how the same dividend produces different outcomes across four profiles.

A zero-tax retiree (total income below the effective threshold of approximately $21,884, which includes the base $18,200 tax-free threshold plus the Low Income Tax Offset of up to $700) owes no tax on the $100 grossed-up income. The full $30 credit is refunded as cash. Effective return: $100 on a $70 dividend. At scale, $1,000 in fully franked dividends with $429 in associated credits yields a full $429 ATO cash refund.

An investor on a marginal rate of approximately 30% owes $30 in tax on the $100 grossed-up income. The $30 credit offsets the liability exactly. No refund, no additional tax. The outcome is tax-neutral.

A high-income investor at the 45% marginal rate owes $45 on the grossed-up $100. The $30 credit partially offsets the liability, leaving a residual $15 in tax owing. The credit still reduces the tax bill, but does not eliminate it.

| Investor Type | Marginal Rate | Cash Dividend | Franking Credit | Tax on Grossed-Up Income |

|---|---|---|---|---|

| Zero-tax retiree | 0% | $70 | $30 | $0 (full $30 refund) |

| ~30% marginal rate | 30% | $70 | $30 | $30 (tax-neutral) |

| High-income earner | 45% | $70 | $30 | $45 ($15 net tax owing) |

| SMSF (pension phase) | 0% | $70 | $30 | $0 (full $30 refund) |

Self-managed superannuation funds in pension phase pay a 0% tax rate, making every dollar of franking credits fully refundable. The credits function as a direct cash supplement to the fund’s income.

SMSFs in accumulation phase pay tax at 15%. Credits offset that liability first, and any surplus is refunded. On a $100 grossed-up dividend, the fund owes $15 in tax; the $30 credit covers it entirely and produces a $15 refund.

One compliance point separates SMSFs from individual investors. The $5,000 small-shareholder exemption from the 45-day holding rule does not apply to SMSFs. Every parcel must comply with the holding period, regardless of the credit amount involved.

Franking credit allocation gaps in super funds represent a structural cost that never appears in any fee disclosure document, meaning an SMSF trustee who receives full refundable credits may be capturing significantly more after-tax value than a member of a large pooled fund invested in the same underlying ASX equities.

Shares must be held genuinely “at risk” for at least 45 consecutive days around the ex-dividend date (90 days for preference shares) for franking credits to be claimable. The days of purchase and sale are excluded from the count, meaning the margin between compliance and forfeiture can be narrow.

Individual taxpayers whose total annual franking credits remain below $5,000 are exempt from this rule entirely. That threshold is equivalent to approximately $11,667 in fully franked dividends at the 30% rate, or approximately $15,000 at the 25% rate. Most investors holding diversified ASX portfolios will fall comfortably below it.

The conditions that can disqualify a franking credit claim include:

Investors in companies that raise capital to fund franked distributions face new ATO scrutiny under PCG 2025/3, issued in September 2025. The guidance introduces a risk assessment framework and increases the “substantial part” threshold to 20%, relevant for investors in companies undertaking such arrangements.

The ATO guidance on PCG 2025/3 classifies capital-raising arrangements designed to fund franked distributions as a Category C reportable tax position, signalling that the regulator treats these structures as carrying a high level of compliance risk for the companies that use them.

There is no two-year holding requirement for franking credits. The 45-day rule is the only holding period condition. The two-year misconception likely conflates franking credit rules with the capital gains tax discount, which itself requires 12 months, not two years.

Non-residents of Australia generally cannot claim franking credit refunds. Eligibility requires full-year Australian tax residency.

One further detail catches investors off-guard: the franking rate on a 2024-25 dividend is based on the company’s 2023-24 base rate entity status, not its current-year classification. A company that recently changed size category may frank at a rate that differs from what investors expect.

Understanding the system is the first step. Acting on it is where the financial benefit materialises.

Verify the franking level of dividends before purchasing shares. Franking levels can change year to year based on a company’s tax position and the proportion of its profits subject to Australian corporate tax. ASX dividend announcements, company tax statements, and resources such as Morningstar’s upcoming dividends page provide current information. ASX companies noted for consistent fully franked dividend histories include Washington H. Soul Pattinson (SOL), Fortescue (FMG), Ridley Corporation (RIC), and United Overseas Australia (UOS), though investors should verify current status before acting.

Franking level changes between periods are more common than investors expect: ANZ’s recent move from 70% to 75% franking on its H1 FY26 interim dividend lifted the grossed-up value from approximately 107 cents to 109.68 cents per share, a meaningful shift in after-tax income that would not be visible to investors comparing only the face cash dividend.

For a zero-tax retiree, a 5% fully franked dividend yield on a stock with 30% franking translates to approximately 7.1% pre-tax equivalent gross yield when the refundable credit is included. That effective uplift occurs without taking on any additional market risk.

The action checklist for any franking-aware investor:

SMSF trustees face the most stringent record-keeping obligation. Each share parcel must be tracked separately for 45-day compliance, with no exemption threshold available.

The imputation system is a structural advantage available to Australian resident investors that international shareholders in the same companies cannot access. It rewards domestic ownership of Australian equities with a tax credit that, for the right investor profile, converts into cash.

The steps are straightforward. Understand the franking level of every dividend received. Know where the investor’s own tax position falls relative to the corporate tax rate. Comply with the 45-day rule where it applies. Claim what is owed, whether through a tax return, the ATO’s automatic refund process for eligible over-60s, or Form NAT 4105.

For a zero-tax investor, a fully franked dividend effectively delivers $100 of value for every $70 in cash received. An unfranked dividend of the same amount delivers exactly $70. The franking credit accounts for the entire difference.

The ATO’s automatic refund process from 2024-25 onward means the system is becoming easier to access. It remains most valuable, however, for investors who understand it well enough to confirm their eligibility, maintain their compliance, and build their portfolios with the after-tax return in full view.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Franking credits, also called imputation credits, represent corporate tax already paid by an Australian company on its profits before paying dividends. They attach to dividends and allow shareholders to offset that pre-paid tax against their own personal tax liability, with any excess refunded as cash by the ATO.

Use the formula: Franking Credit equals (Dividend Amount divided by (1 minus Company Tax Rate)) multiplied by Company Tax Rate. For example, a $70 cash dividend from a company taxed at 30% produces a $30 franking credit, giving you $100 in grossed-up assessable income.

Yes. If your franking credits exceed your total tax liability, the ATO refunds the difference as cash. From the 2024-25 tax year onward, eligible Australian residents aged over 60 receive this refund automatically without needing to lodge a full tax return.

The 45-day rule requires that shares be held genuinely at risk for at least 45 consecutive days around the ex-dividend date (90 days for preference shares), excluding the days of purchase and sale, for franking credits to be claimable. Individual investors whose total annual franking credits remain below $5,000 are exempt from this rule.

SMSFs in pension phase pay 0% tax, making all franking credits fully refundable as cash. SMSFs in accumulation phase pay 15% tax, so credits first offset that liability and any surplus is refunded. Unlike individual investors, SMSFs have no $5,000 small-shareholder exemption from the 45-day holding rule.