In April 2020, crude oil futures briefly traded at negative values. Sellers were effectively paying buyers to take oil off their hands. The price of a physical commodity with obvious real-world demand had disconnected entirely from its fundamental worth.

That episode was extreme, but the underlying dynamic is not rare. Stock prices routinely diverge from the value of the businesses they represent, sometimes for months or years at a stretch. Understanding why this happens is not an academic exercise; it is the foundation of every investment approach that aims to buy something for less than it is worth.

This article explains the structural and behavioural forces that produce persistent gaps between price and value, illustrates those forces with documented real-world cases, and outlines what an investor actually needs, analytically and psychologically, to profit from the divergence rather than be hurt by it.

What the efficient market hypothesis gets right (and where it quietly breaks down)

The efficient market hypothesis deserves to be taken seriously before it is qualified. At the index level, prices absorb information quickly enough that most active managers cannot consistently outperform after fees. This is not a contested claim; it is the documented experience of decades of practitioner data. The average stock-picker, after costs, trails the index.

Where the hypothesis loses its grip is at the level of individual securities. Benjamin Graham framed the distinction precisely: in the short term, markets function as voting mechanisms, reflecting sentiment and crowd psychology. Over longer periods, they operate as weighing mechanisms, converging toward fundamental value. The gap between the vote and the weight is where mispricing lives.

The strength of the efficiency claim varies by market segment:

- Index level: Prices aggregate information quickly. Consistent outperformance after fees is difficult for most participants.

- Large-cap single stocks: Efficiency is high but imperfect. Earnings surprises, forced selling, and sentiment shifts can produce temporary dislocations.

- Small-cap and neglected single stocks: Efficiency degrades meaningfully. Fewer analysts, lower passive coverage, and thinner liquidity allow prices to diverge from value for extended periods.

The argument that follows is not that markets are broken. It is that they are selectively and predictably inefficient in ways that create exploitable patterns for investors with the right tools and temperament.

When big ASX news breaks, our subscribers know first

The structural forces that prevent prices from reflecting value

Mispricing is not a random accident. It is the predictable output of structural features baked into how modern markets operate. Three forces are most responsible:

- Passive investing dominance: Index funds and ETFs now follow benchmarks rather than analyse businesses, reducing the volume of fundamental analysis applied to individual securities.

- Institutional constraints: Sector restrictions, mandate limits, and forced selling during fund redemptions can suppress prices for reasons entirely unrelated to underlying business value.

- Speculative retail participation: Meme-stock and crypto-adjacent behaviour introduces sentiment-driven flows that can overwhelm fundamental price discovery in the short run.

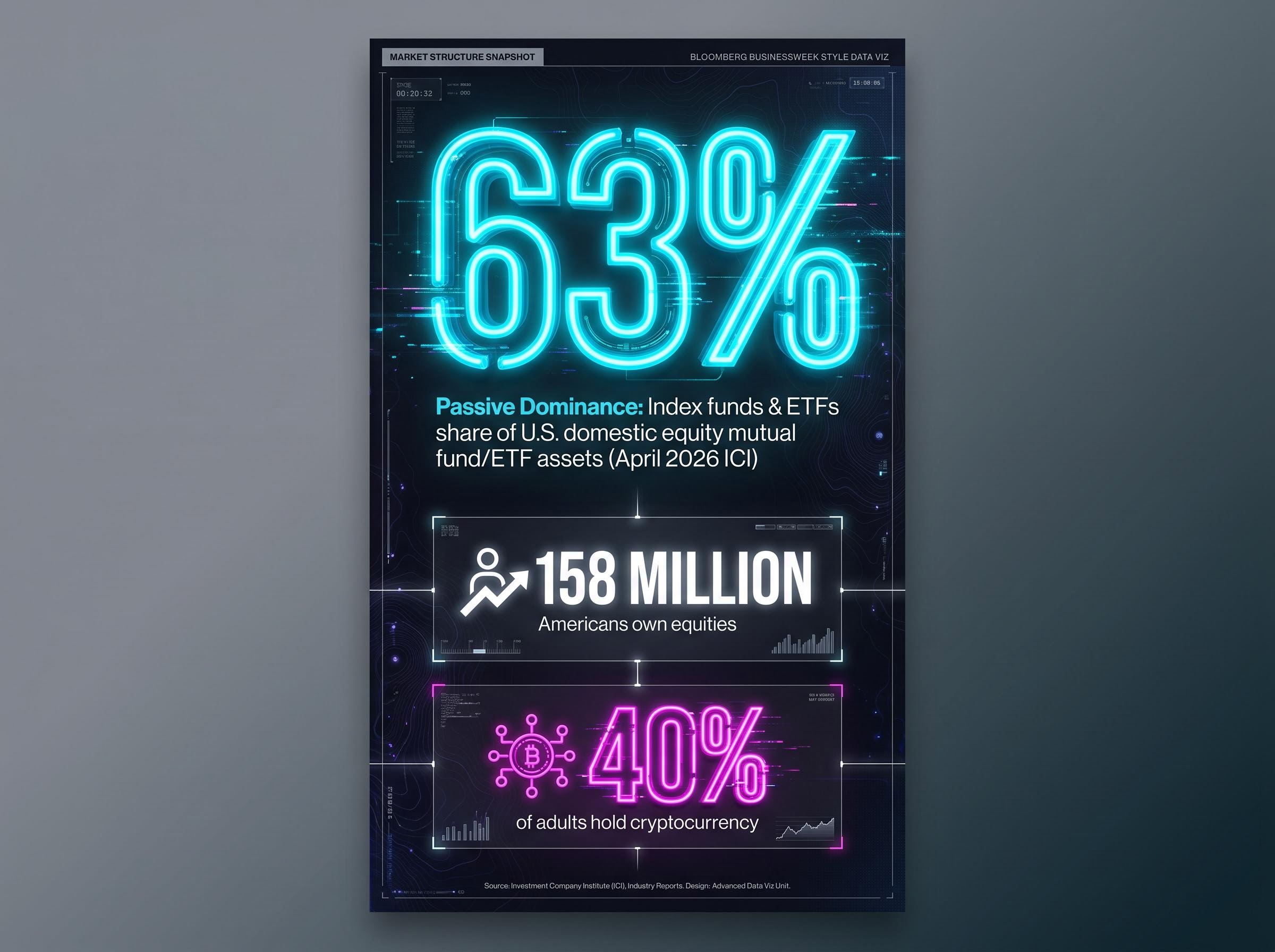

Index funds and ETFs account for approximately 63% of U.S. domestic equity mutual fund and ETF assets, according to the Investment Company Institute’s April 2026 release. The majority of capital flowing into markets is not performing fundamental analysis on individual companies.

The scale of retail participation compounds the effect. Approximately 158 million Americans own equities, with an estimated 40% of adults also holding cryptocurrency, activity characterised in industry research as speculative rather than investment-driven.

The inference is straightforward. When most market participants are either tracking an index or speculating on momentum, the pricing signal for any individual stock degrades. This is not a temporary condition. It is a structural feature of the current market environment.

For investors who grasp this dynamic, market inefficiency is not a flaw waiting to be corrected. It is a recurring condition produced by the architecture of modern capital markets, and it is most pronounced in the smaller, less liquid, or less-followed names where passive flows represent a larger share of total trading volume relative to fundamental-analysis-driven activity.

Why behavioural biases make mispricings persistent, not fleeting

A common assumption is that mispricings are corrected quickly by rational arbitrage. The evidence suggests otherwise. Human psychology does not merely fail to correct mispricings; it actively sustains and deepens them before any correction arrives.

Benjamin Graham observed that an investor’s primary adversary is typically their own behaviour rather than any external market force.

Loss aversion is the mechanism on the downside. When prices fall, the pain of loss triggers selling at precisely the moment when the gap between price and value is widest. Rather than correcting the undervaluation, this behaviour deepens it. Fear of missing out operates in reverse on the upside, drawing capital into already-extended positions and stretching overvaluation further before the reversion comes.

Loss aversion, the tendency to feel losses roughly twice as intensely as equivalent gains, produces a measurable return shortfall that Morningstar’s ‘Mind the Gap’ research consistently estimates at 1-2 percentage points per year, because investors sell near market lows and re-enter after prices have already recovered.

The 1999 Berkshire Hathaway episode illustrates the dynamic precisely. Berkshire declined approximately 23% while the S&P 500 gained roughly 18% including dividends. A Barron’s article questioned whether Warren Buffett’s approach remained relevant. The business value of Berkshire’s holdings had not declined. The market price had. Investors who sold during that period acted on behavioural pressure, not analytical insight.

Seth Klarman’s principle applies here: strong analytical conviction must coexist with genuine openness to revision when new information emerges. The distinction matters. Conviction without openness produces stubbornness. Openness without conviction produces capitulation at exactly the wrong moment.

Uncertainty about future outcomes is penalised heavily by markets, even when the range of plausible outcomes is acceptable to long-term investors. This penalty creates a structural window in which prices undershoot value, and behavioural forces keep them there longer than rational models predict. Patience, then, is not merely a virtue. It is a structural requirement for anyone seeking to profit from the gap.

What mispricing actually looks like: three documented cases

Theory becomes actionable when attached to specific examples. The following three cases span different asset classes and time periods, but the pattern is consistent: price moved far more dramatically than any plausible change in underlying value.

| Asset | Price at mispricing | Reference/recovery price | Mechanism |

|---|---|---|---|

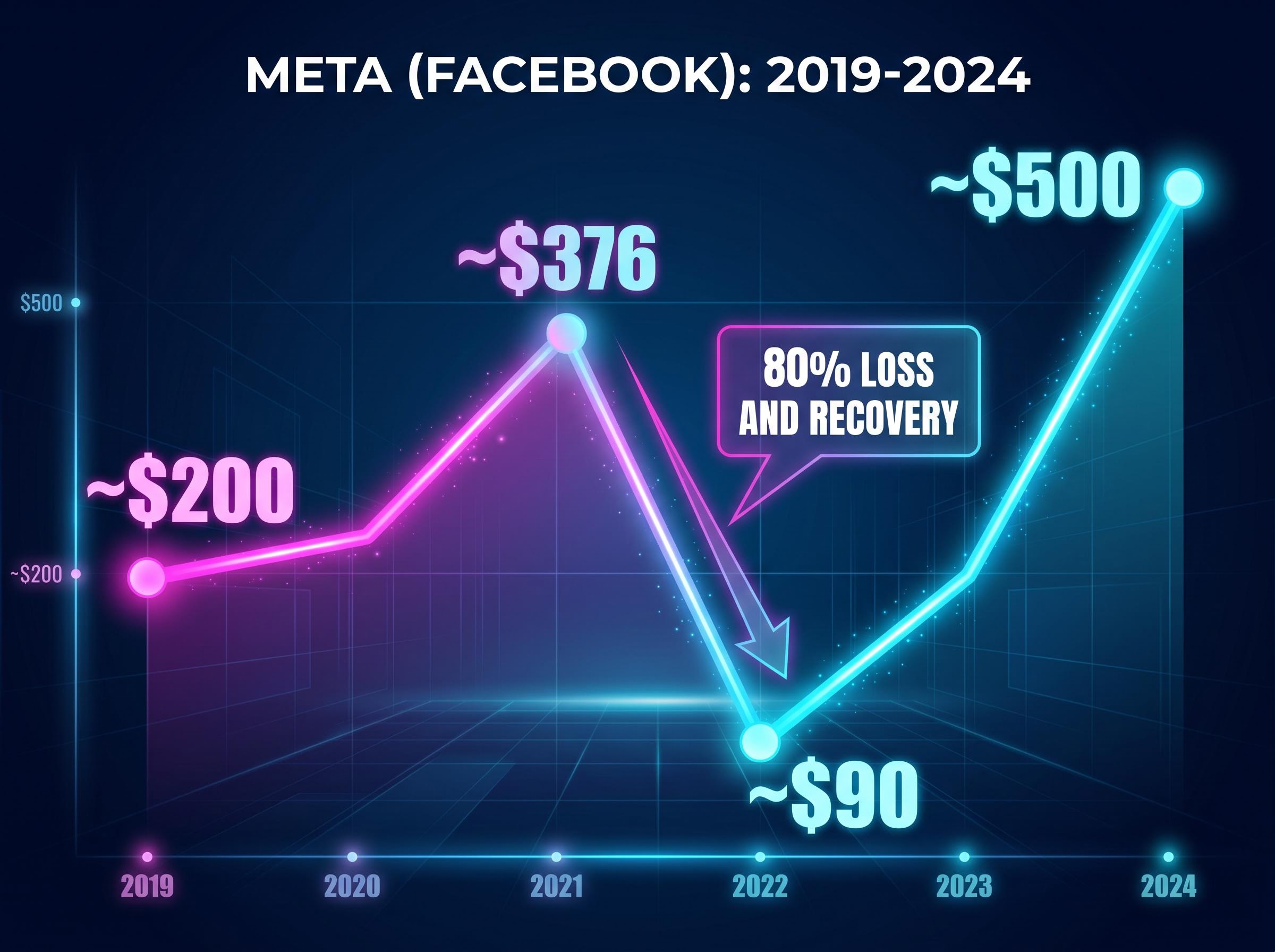

| Meta (Facebook) | ~$90 | ~$500 | Sentiment-driven sell-off; business fundamentals remained intact |

| Activision Blizzard | ~$50 (public market) | ~$95 (Microsoft acquisition) | Public market persistently underpriced relative to strategic acquirer value |

| Crude oil futures | Briefly negative (April 2020) | Sharp recovery within ~1 year | Forced selling and storage constraints disconnected price from fundamental value |

Meta shares moved from approximately $200, peaked near $376, collapsed to roughly $90, then recovered to approximately $500 over a period spanning roughly 2019-2024. The underlying advertising business did not lose and regain 80% of its value during that window. The price did.

Activision Blizzard traded near $50 in public markets before Microsoft acquired the company at approximately $95 per share. The gap between those two figures was not an information problem; it reflected the public market’s persistent inability to price the business at what a strategic buyer would rationally pay.

Crude oil futures briefly going negative in April 2020 remains the most extreme case. A commodity with undeniable real-world demand reached a price that implied it had negative worth, not because the oil was worthless but because storage constraints and forced contract liquidation overwhelmed fundamental pricing for a brief window.

The strategic acquirer’s valuation perspective

The Activision case introduces a useful analytical concept. The price a strategic acquirer would pay for a whole business serves as an independent reference point for assessing whether a public-market price makes sense. This benchmark is particularly useful for smaller companies that are realistic acquisition candidates, where the gap between public-market sentiment and private-transaction value tends to be largest. When a stock trades at a significant discount to what an informed buyer would pay for the entire enterprise, the mispricing signal strengthens.

The investor toolkit for exploiting market inefficiency

Knowing that mispricing exists is not the same as being able to profit from it. The gap between diagnosis and exploitation is primarily a problem of analytical capability and psychological architecture, not information access.

The requirements are sequential, not interchangeable:

- Analytical foundation. The ability to assess what a business is worth independent of its current market price. This means evaluating a company through a business lens (cash flows, competitive position, asset value) rather than a price-chart lens. Walter Schloss demonstrated over decades that disciplined fundamental analysis applied consistently can produce strong long-term results independent of short-term noise. The skill is learnable, but it demands sustained effort.

- Psychological architecture. The willingness to appear wrong for extended periods, act against consensus, and hold a position while the market moves against it before the correction arrives. Value investing requires the willingness to appear incorrect while the market catches up to fundamental reality. This is not a personality trait; it is a practised capacity that most investors never develop.

Value investing metrics such as price-to-earnings ratio, price-to-book ratio, free cash flow yield, and debt-to-equity ratio provide the analytical scaffolding for assessing what a business is worth independent of its current market price, and the hardest practical challenge they pose is distinguishing a structurally declining business from a temporarily mispriced one, the distinction that separates value traps from genuine opportunities.

The clearest contemporary evidence of exploitable mispricing appears in deal arbitrage and post-earnings dislocations, cases where prices move sharply on news or sentiment before reverting toward fundamental value. These categories offer the most observable proof that markets are not uniformly efficient, and they are accessible to investors who have built both layers of the toolkit.

The honest self-assessment question is not “Do I believe markets are inefficient?” Most investors already do. The question is: “Do I have the analytical tools and behavioural discipline that this approach actually demands?” That distinction separates conviction from capability.

Patience as the edge that structural forces cannot erode

The structural argument from earlier in this article points to a conclusion that extends well beyond any single trade. Passive investing reduces fundamental analysis on individual stocks. Retail speculation introduces noise. Behavioural biases sustain mispricings longer than rational models predict. Together, these forces guarantee a recurring supply of mispriced securities.

The patient investor’s edge is not information. Markets aggregate information quickly at the index level. The edge is time horizon and emotional architecture: the capacity to assess what a business is worth, buy when the price diverges from that value, and wait for convergence without capitulating to the pressure of apparent underperformance.

With approximately 63% of U.S. domestic equity mutual fund and ETF assets tracking indices rather than performing fundamental security analysis, the structural supply of mispricing is not shrinking. If anything, it is deepening in the segments of the market where passive flows dominate relative to fundamental-analysis-driven activity.

Investment Company Institute data on active and index investing shows domestic equity index funds accounting for 63.2% of total assets as of March 2026, confirming that the structural shift away from fundamental security analysis is not a marginal phenomenon but the defining feature of how U.S. equity capital is currently deployed.

Warren Buffett’s sustained adherence to value principles through the 1999 underperformance episode and over subsequent decades remains the best-documented long-run illustration of the compounding effect of this approach. The market declared him obsolete. The weighing mechanism, over time, disagreed.

Market inefficiency is not a market failure waiting to be corrected. It is a structural and psychological condition that patient, analytically grounded investors can exploit repeatedly over time.

For readers wanting to extend this framework to the other side of the mispricing problem, our deep-dive into price versus value examines the Nifty Fifty collapse of 1968-1973, where investors in world-class companies lost approximately 90% of portfolio value by paying 80-90 times forward earnings, and applies Howard Marks’ second-level thinking framework to identify where the same valuation structure is repeating in today’s AI-driven market.

The market will keep being wrong. The question is whether you can wait.

Price and value diverge not randomly but for structural and behavioural reasons that are unlikely to disappear. The forces producing mispricing, passive dominance, speculative retail flow, and behavioural biases, are all present and active in U.S. markets today. Meta, Activision Blizzard, and crude oil futures each demonstrated, in different ways and at different scales, that the gap between what something costs and what it is worth can be enormous.

The practical starting point is a single question: how do you currently distinguish between a falling price that signals a deteriorating business and a falling price that signals a market mispricing of a sound one? That distinction is where the analytical and behavioural work begins.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.