Immuron Explained: the ASX Biotech Built on Revenue, Not Raises

5 hrs ago

Most Singapore-based retail investors who attempt their first leveraged ETF trade encounter an unexpected barrier: a mandatory eligibility review that no one mentioned when they opened their brokerage account. The barrier has a name. Leveraged and inverse exchange-traded funds fall under the Monetary Authority of Singapore’s (MAS) Specified Investment Products (SIP) classification, a regulatory designation that activates a set of eligibility conditions before any trade can be placed. The classification applies not only to products listed on the Singapore Exchange (SGX) but also to overseas leveraged ETFs, including US-listed 3x sector funds, when accessed through MAS-licensed brokers.

This guide explains what the SIP classification means for retail investors trading leveraged ETFs in Singapore, which eligibility pathway applies (and why it differs from the process many investors initially expect), what brokers assess during the Customer Account Review (CAR), and how the SGX Academy module functions as an alternative route for those who do not meet standard criteria.

The MAS operates a two-tier classification system for investment products available to retail investors. On one side sit Excluded Investment Products (EIPs): ordinary shares, plain-vanilla ETFs, and bonds whose terms are generally understandable without specialised knowledge. On the other sit Specified Investment Products (SIPs): instruments that feature derivatives, embedded structural complexity, or payoff profiles materially different from their underlying reference.

The distinction between EIPs and SIPs reflects a genuine structural difference in what investors are buying: plain-vanilla ETFs hold baskets of securities directly and require no derivative overlay to deliver their stated exposure, whereas leveraged products layer in swaps and futures that alter the payoff profile in ways that are not immediately obvious from the fund name alone.

Leveraged and inverse ETFs land in the SIP category for three specific structural reasons:

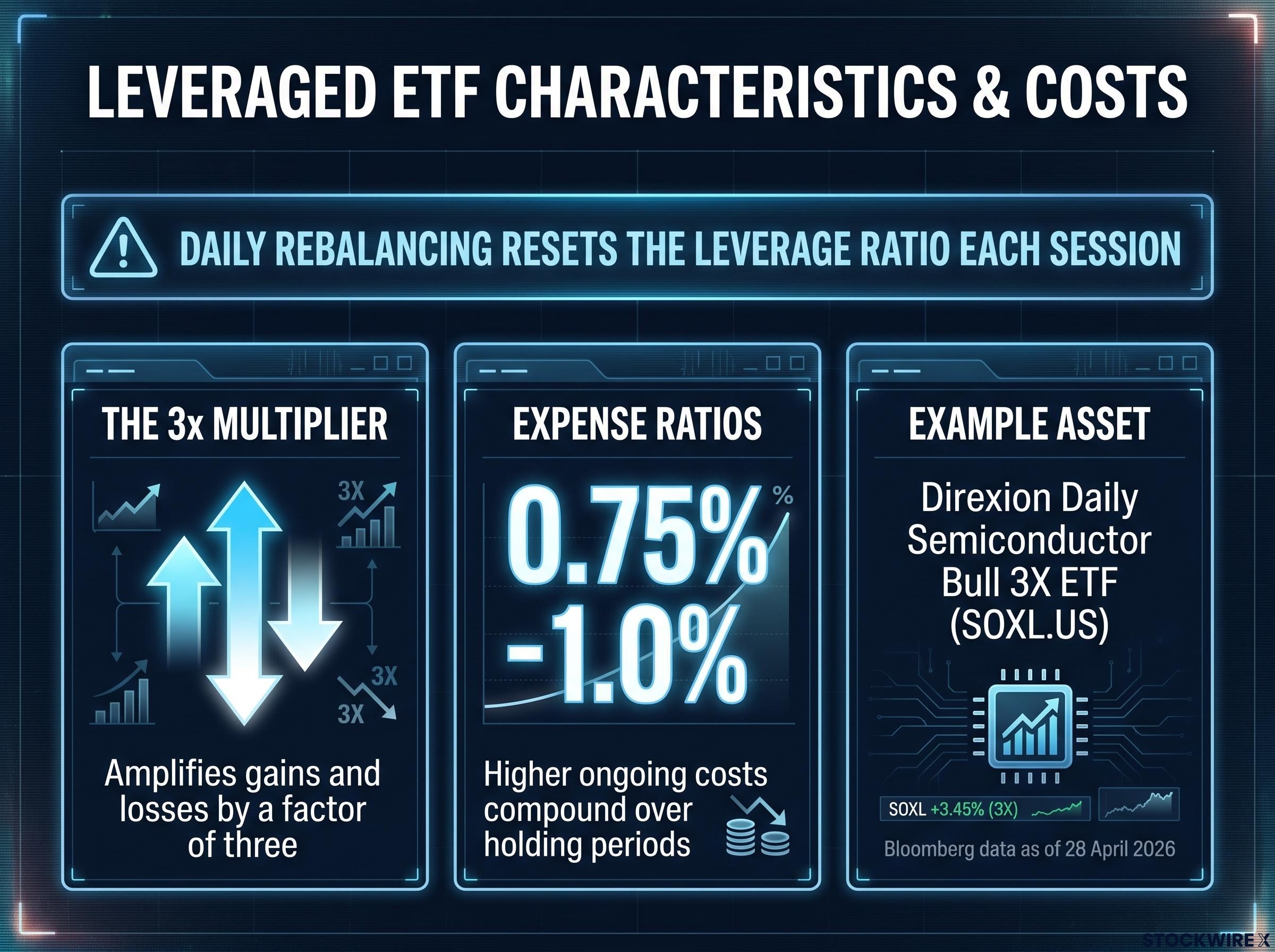

Daily rebalancing is the mechanism that makes a 3x leveraged ETF behave so differently from a 3x margin loan: each evening the fund resets its derivative positions to restore the target leverage ratio, and this compounding of percentage moves over consecutive sessions produces outcomes that can diverge materially from any simple multiple of the index’s cumulative return.

The SIP classification, which remains in effect as of 19 June 2026, triggers enhanced distribution safeguards rather than an outright ban. Retail investors can still trade these products, but they must first satisfy eligibility conditions designed to confirm baseline product understanding.

| Category | Examples | Typical structural features | Retail access conditions |

|---|---|---|---|

| EIP (Excluded Investment Product) | Ordinary shares, plain-vanilla ETFs, standard bonds | Straightforward terms; no embedded derivatives | Standard brokerage account; no additional assessment |

| SIP (Specified Investment Product) | Leveraged ETFs, inverse ETFs, structured warrants | Derivatives use, daily rebalancing, amplified or inverse payoff | Customer Account Review (listed SIPs) or Customer Knowledge Assessment (unlisted SIPs) required |

Two acronyms circulate through Singapore broker documentation and investor forums, and confusing them wastes preparation time. The distinction is straightforward once made explicit, but broker onboarding materials do not always draw the line clearly.

The Customer Account Review applies to listed SIPs, which include leveraged and inverse ETFs traded on exchanges. Because these products are listed instruments, the CAR is the operative gateway. It is conducted at the account level, before any trade is placed, and determines whether an investor is authorised to access the listed SIP product category through that broker.

The Customer Knowledge Assessment (CKA) applies to unlisted SIPs, a separate product category that includes structured notes sold over the counter and other OTC instruments. Investors who search for “CKA leveraged ETFs” are being misdirected; the CKA governs a different class of products entirely.

The key distinction: CAR applies to listed SIPs (including leveraged and inverse ETFs). CKA applies to unlisted SIPs (such as structured notes and OTC products). For leveraged ETF trading, only the CAR is relevant.

The CAR is not a single standardised national examination. It is an eligibility assessment that brokers conduct using a combination of self-declared background information and, in many cases, a short questionnaire on SIP features and risks. Three dimensions are assessed:

The most commonly cited trading history threshold is a minimum of six transactions in similar products within the preceding three years, though exact criteria vary by broker. Some broker implementations also require periodic renewal of the assessment, commonly every three years.

Scope note: CAR requirements apply when trading through MAS-licensed brokers regardless of whether the product is SGX-listed or an overseas-listed leveraged ETF. An investor accessing a US-listed 3x fund through a Singapore-based, MAS-licensed broker must still satisfy the CAR or the alternative SGX Academy pathway before placing any trade.

Investors who satisfy the education, experience, or trading history thresholds are authorised to trade listed SIPs through that broker. The process is typically completed once and remains valid for a set period.

Investors who do not meet the standard CAR criteria are not permanently barred. An alternative qualification pathway exists through the SGX Academy, detailed in the following section.

SGX Academy, the investor education arm of Singapore Exchange, offers an Online Education Programme for Listed SIPs. This self-paced module serves as the alternative qualification route for investors whose educational background, work experience, or trading history does not meet the standard CAR thresholds.

The programme covers three areas: how leveraged and inverse ETFs are structured, their risk characteristics, and the use cases for which they are appropriate. A short assessment follows the module content, and investors must pass it to receive a completion record.

The practical steps are sequential:

Portability: The SGX Academy completion record can be used with multiple MAS-licensed brokers, not just the one through which the investor initially intends to trade.

The programme is generally available at no charge, though investors should confirm the current status directly with SGX Academy. As of 19 June 2026, the programme remains available and recognised by MAS-licensed brokers as a valid alternative pathway.

The SIP regime took effect on 1 January 2012 as part of a broader set of post-Global Financial Crisis reforms by MAS. The framework responded to two documented problems:

The MAS announcement on SIP retail investor requirements, published in July 2011, confirmed that the CAR and CKA frameworks would take effect on 1 January 2012, with the explicit purpose of ensuring intermediaries assess investment knowledge before selling complex products to retail customers.

The framework’s stated purpose is to promote informed decision-making and ensure a baseline level of product knowledge before trading. It is not designed to restrict access permanently or to prevent losses outright. No investor is barred from trading leveraged ETFs indefinitely; the two-route structure (demonstrated experience through the standard CAR criteria, or demonstrated education through the SGX Academy programme) reflects the MAS view that either pathway achieves the same baseline understanding objective.

That design logic also explains why the framework covers overseas leveraged ETFs accessed through Singapore brokers. The eligibility requirement attaches to the intermediary relationship, not the listing venue.

The qualification process is designed to build the knowledge this section delivers. Investors who have satisfied the CAR or completed the SGX Academy programme are authorised to trade, but authorisation and preparedness are not the same thing.

Leverage operates symmetrically. A 3x leveraged ETF amplifies gains by a factor of three on a given day, but it amplifies losses by the same factor. Position sizing and risk management tools such as stop-loss orders become operationally important rather than optional.

Position sizing in leveraged ETF trading is not merely a risk preference; it is a mechanical consequence of the leverage ratio itself, since a 3x fund requires roughly one-third the notional allocation of an equivalent unlevered position to achieve the same index exposure, with an additional buffer needed to absorb overnight gaps and tracking error that can push realised losses above the theoretical multiple.

The compounding principle: Returns over periods longer than a single day can diverge substantially from a simple multiple of the underlying index’s return. Daily rebalancing resets the leverage ratio each session, and this compounding effect means that a 3x leveraged ETF held for a month will not necessarily deliver three times the index’s monthly return. These instruments are designed for short-term, tactical use.

The Direxion Daily Semiconductor Bull 3X ETF (SOXL.US), which provides three-times leveraged exposure to semiconductor sector performance (referenced using Bloomberg data as of 28 April 2026), illustrates the practical reality: an investor holding such a product for weeks rather than days may experience returns that look nothing like three times the index movement over the same period.

Four product-specific variables warrant evaluation before selecting a leveraged ETF:

| Variable | High-liquidity product | Sector-specific product | Reader implication |

|---|---|---|---|

| Liquidity and trading depth | Deep order book; tight spreads during market hours | Thinner trading volumes; wider intraday variation | Easier entry and exit with less slippage in high-liquidity products |

| Bid-ask spreads | Typically narrow (a few cents) | Can widen significantly in volatile sessions | Wider spreads increase the cost of short-term round-trip trades |

| Expense ratios | Higher than standard ETFs; typically 0.75%-1.0% | Often comparable or slightly higher | Higher ongoing costs compound over holding periods |

| Tracking performance | Generally close to target multiple on a daily basis | May show greater deviation from target multiple | Assess whether the product delivers its stated multiple reliably on a daily basis |

The two primary practical use cases for these instruments are capitalising on short-term directional moves at a sector or index level, and establishing short-equivalent exposure through inverse ETFs without directly shorting individual securities. Neither use case is suited to a buy-and-hold strategy.

The pathway from classification to authorised trading access follows a clear sequence:

These rules apply whether trading SGX-listed leveraged products or overseas-listed instruments such as US 3x sector funds, provided the trade is placed through an MAS-licensed broker.

Qualified access enables two tactical applications:

Investors who have worked through the qualification process should approach these instruments as a deliberate tactical layer rather than a portfolio core. Defined time horizons, appropriate position sizing, and active monitoring align with the product design. The qualification process exists because these instruments reward preparation and penalise assumptions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and leveraged product returns are subject to daily compounding effects that may produce outcomes materially different from expectations over multi-day holding periods.

The Specified Investment Products classification is a regulatory designation by the Monetary Authority of Singapore that applies to instruments with structural complexity, including leveraged and inverse ETFs, requiring retail investors to satisfy eligibility conditions before trading them through any MAS-licensed broker.

The Customer Account Review (CAR) applies to listed SIPs such as leveraged and inverse ETFs, while the Customer Knowledge Assessment (CKA) applies to unlisted SIPs such as structured notes and OTC products; investors seeking to trade leveraged ETFs only need to complete the CAR, not the CKA.

Investors who do not meet the standard CAR thresholds for education, work experience, or trading history can complete the SGX Academy Online Education Programme for Listed SIPs, pass its short assessment, and submit the completion record to their MAS-licensed broker as an alternative qualification pathway.

Yes, the CAR requirement attaches to the intermediary relationship rather than the listing venue, so any investor accessing a US-listed leveraged ETF through a MAS-licensed Singapore broker must still satisfy the CAR or the SGX Academy alternative pathway before placing a trade.

Leveraged ETFs use daily rebalancing to reset their leverage ratio at the close of each session, meaning compounding of percentage moves over multiple days can cause the fund's cumulative return to diverge materially from a simple multiple of the underlying index's return, making these instruments suited only for short-term tactical use.