Passive Income Investing in Australia: What Actually Works

1 hr ago

The leveraged ETF category has grown to $164.1 billion in assets under management across 572 US-listed funds as of early May 2026, yet the most common mistake among traders is sizing these instruments as if the dollar allocation tells the whole story. Most educational content explains why leveraged ETFs decay. This guide assumes the reader already knows that and answers the harder question: if TQQQ, SQQQ, SOXL, UPRO, or SPXU are going to appear in a live portfolio, what does responsible execution actually look like?

What follows is a concrete position-sizing methodology anchored to underlying index moves, a decision framework for inverse ETFs as hedges, a working model for pair trades, and a clear-eyed view of what happens when margin enters the picture. Each section builds on the one before it, moving from foundational sizing logic through tactical use cases to the highest-risk configuration available to a retail trader.

A $10,000 position in a 3x leveraged ETF does not carry the same risk as a $10,000 position in the non-levered index. It carries three times the sensitivity to every move in the underlying. The correct way to size a leveraged ETF position is relative to the anticipated move in the underlying index, not the notional dollars committed to the fund.

This is also the structural feature that makes these instruments useful. A smaller allocation in a 3x fund can represent the same index exposure as a much larger allocation in a non-levered equivalent, freeing capital for other positions. The capital efficiency is real, but only if the sizing reflects the amplified risk.

Here is the three-step process:

| Risk Budget (1% of Portfolio) | Non-Levered ETF Allocation (5% Stop) | 3x Fund Allocation (15% Fund Move) | 3x Fund with Buffer (20% Fund Move) |

|---|---|---|---|

| $500 | $10,000 | $3,333 | $2,500 |

| $1,000 | $20,000 | $6,667 | $5,000 |

| $2,000 | $40,000 | $13,333 | $10,000 |

The practitioner heuristic for TQQQ and similar 3x products simplifies this further: if normal risk per trade is 1% of portfolio in a non-levered ETF, cut notional to roughly one-third for the 3x fund, preserving the same dollar risk.

The theoretical 15% fund move from a 5% index move is a floor, not a ceiling. Two forces push actual losses higher.

Overnight gaps can move the underlying index beyond the stop level before the market opens, and the fund reprices off that gap at the full leverage multiple. Tracking error, the small daily divergence between the fund’s return and exactly 3x the index return, accumulates over multi-day holds. Sizing as if the fund could lose 20% rather than 15% on that same 5% underlying move cuts the allocation further to $5,000 on a $1,000 risk budget, building in protection against both sources of excess loss.

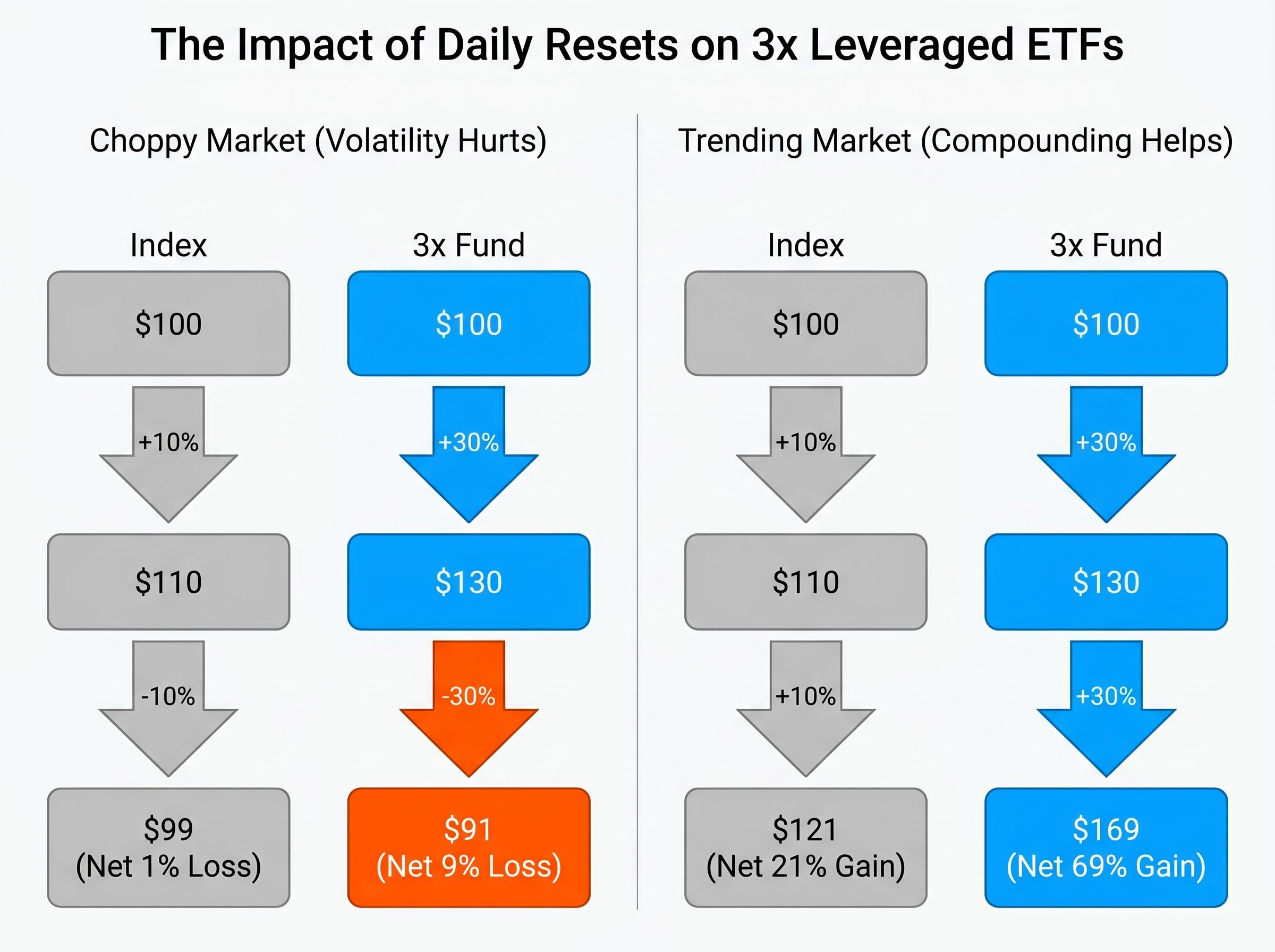

The daily reset is the mechanism that makes leveraged ETFs behave differently from a static leveraged position. Each trading session, the fund recalculates its exposure from a new baseline. On a single calm day, this barely matters. Over a sequence of alternating up and down days, it compounds against the holder even when the index finishes flat.

Consider an index that starts at $100, rises 10% to $110, then falls 10% to $99, a net 1% loss. A 3x fund tracking the same sequence moves from $100 to $130 on day one, then falls 30% of $130 on day two to land at $91, a 9% loss. The leverage multiple promised 3x the index loss (3%), but the actual result was three times worse.

The arithmetic reverses when the underlying trends in one direction. If the same index rises 10% on two consecutive days, it moves from $100 to $121, a 21% gain. The 3x fund compounds from $100 to $130 to $169, a 69% gain, exceeding three times the index return. Compounding works for the holder in sustained trends and against them in choppy conditions.

Research by Guedj, Li, and McCann (2010) examined rebalancing frequencies from December 2008 to December 2009 and found that daily-reset portfolios finished lowest while no-rebalancing portfolios finished highest, quantifying the cost of the reset mechanism over an extended volatile period.

The leveraged ETF reset period is the single variable that most sharply separates modestly leveraged products (25-50% additional exposure with no daily recalculation) from the 2x and 3x daily-reset funds discussed in this guide, and conflating the two categories is a structurally different error from simply misjudging position size.

Environments where compounding helps:

Environments where compounding hurts:

The practical holding-period rule: intraday to a few days for tactical traders. Anything beyond that requires active monitoring and position resizing.

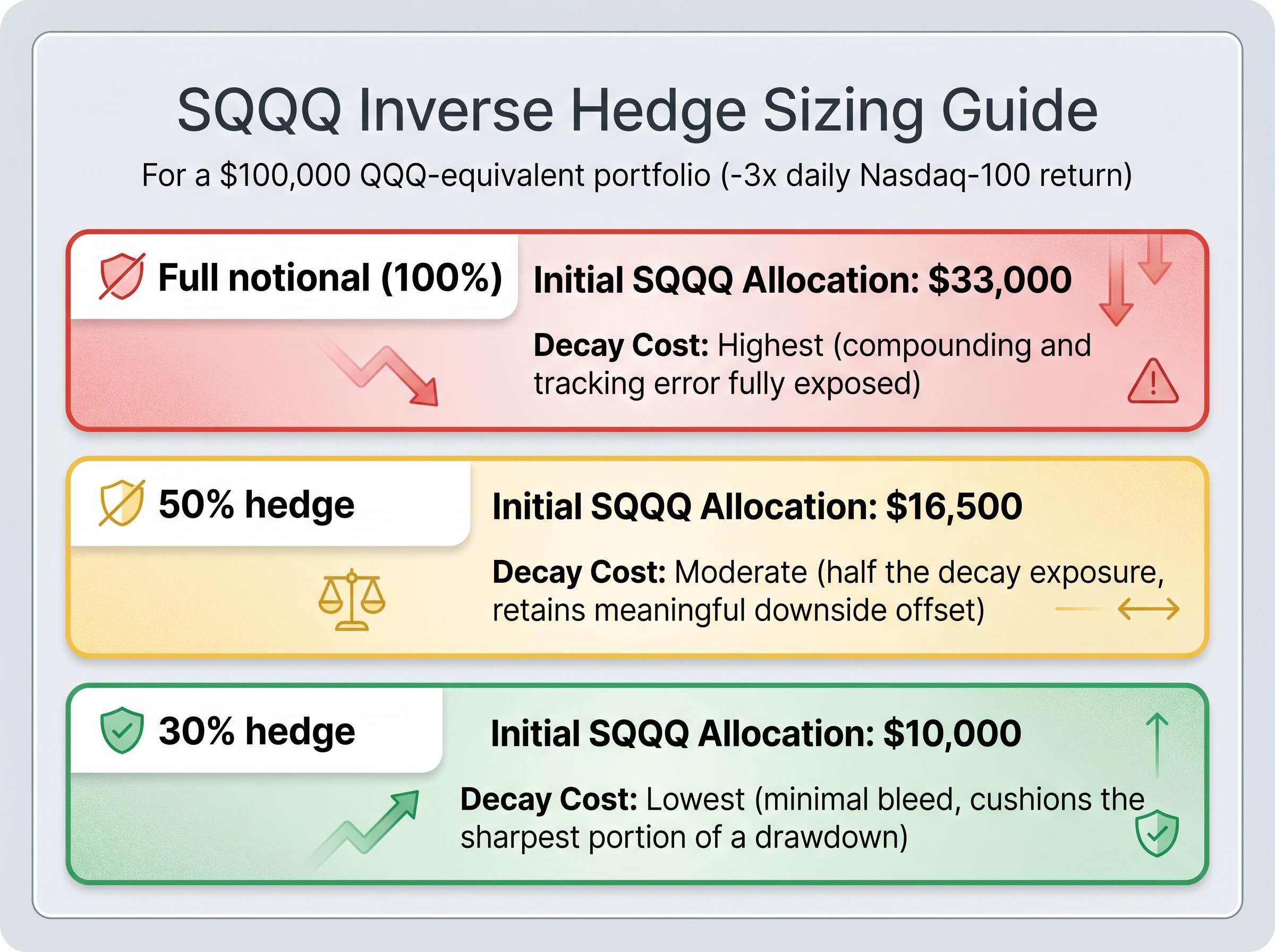

The legitimate use case for an inverse leveraged ETF is narrow and specific: temporarily offsetting downside risk around a known catalyst without selling core long positions and triggering tax consequences. An FOMC announcement, a concentrated tech portfolio heading into major earnings, or a geopolitical spike affecting growth stocks can all justify a short-term inverse overlay.

Sizing that overlay requires three steps:

Practitioner consensus points to hedging only 30-50% of tech exposure rather than the full notional. Partial protection with minimal decay cost tends to outperform full protection that bleeds daily.

| Hedge Coverage | Initial SQQQ Allocation | Approximate Two-Day Decay Cost |

|---|---|---|

| Full notional (100%) | $33,000 | Highest: compounding and tracking error fully exposed |

| 50% hedge | $16,500 | Moderate: half the decay exposure, retains meaningful downside offset |

| 30% hedge | $10,000 | Lowest: minimal bleed, cushions the sharpest portion of a drawdown |

The liability condition is straightforward. When an inverse position becomes open-ended, held for weeks without a defined exit trigger, daily resets and path dependency accumulate losses even if the anticipated sell-off eventually materialises. The hedge becomes a second source of erosion in a portfolio that may already be under pressure.

Short-side exposure costs extend well beyond the decay that inverse ETFs accumulate through daily resets; in direct short positions, borrow fees can exceed 15% annualised on heavily shorted names, and a 2025 CFA Institute study found retail short sellers lost an average of 18% annually even when their directional thesis proved correct.

A pair trade with leveraged ETFs expresses a relative-value view rather than a directional bet. The structure combines a long leveraged position in one sector or index with an offsetting short or inverse position in a related but distinct asset. The profit comes from the spread between the two, not from the market moving in a single direction.

The most actively discussed structure in 2025-2026 practitioner commentary involves SOXL (3x long semiconductors). A trader might go long SOXL against a short position in a non-levered semiconductor ETF such as SOXX or SMH, or against short SOXS (-3x semis), to express a view on volatility or convexity rather than purely betting on semiconductor direction. The AI and semiconductor bull market has made this a frequently referenced setup around earnings cycles and chip-sector catalysts.

SOXL is typically described as providing “option-like” exposure, with position sizes capped at 1-3% of portfolio and used around specific catalysts.

Three conditions that make a leveraged ETF pair trade appropriate:

Three conditions that indicate the structure is being misused:

A traditional pair trade in non-levered ETFs carries one layer of market risk per side. The same structure with leveraged ETFs carries three times the sensitivity per side, requiring position sizes at roughly one-third of the non-levered equivalent to maintain comparable dollar risk per point move.

The correlated-collapse scenario is the primary failure mode. In a broad market sell-off, the long leveraged leg can fall sharply while the short or inverse leg fails to offset it fully, particularly if the sell-off compresses the spread between the two assets rather than widening it. Losses accumulate on both sides simultaneously.

Pair trades with leveraged ETFs require daily review. The compounding effects on each leg diverge over time, shifting the effective ratio of the trade even when the underlying spread is stable. Set-and-forget management is incompatible with this structure.

A 3x leveraged ETF bought on 2x margin gives you 6x exposure to the underlying index. A 5% adverse index move is a 30% loss on that position.

That arithmetic is the entire argument. A 3x fund multiplied by 2x margin creates an effective 6x exposure to the underlying index movement. This is not a moderate increase in risk; it is an exponential multiplication that can produce portfolio-level damage from a single bad session.

Some brokerages prohibit leveraged or inverse ETF purchases in margin accounts outright. Others allow it with higher maintenance margin requirements and additional risk disclosures.

FINRA Regulatory Notice 22-08 establishes heightened supervision requirements for broker-dealer recommendations of complex products, explicitly covering leveraged and inverse ETFs, and mandates that firms assess customer understanding and provide additional disclosures before facilitating trades in these instruments.

FINRA Regulatory Notice 22-08 (March 2022) remains the operative regulatory framework. It requires firms to adopt heightened supervision for recommendations of complex products including leveraged ETFs, assess customer understanding, provide additional disclosures, and potentially restrict access for certain customers. SEC Rule 18f-4 (adopted 2020, actively enforced through 2025-2026) constrains how much leverage ETFs can embed at the fund level, with enforcement activity in 2025-2026 including a pause on high-leverage fund filings and a March 2026 warning to issuers regarding 3x and 5x product proposals.

Before combining margin with leveraged ETFs, three questions need clear answers:

Every tactic in this guide collapses into a single discipline: run a checklist before placing the trade, not after the position is already live.

Pre-trade checklist:

Market-environment green lights for leveraged ETF positions:

If the holding period may extend to weeks rather than days, cut the position size by half again on top of the one-third notional adjustment already made for the leverage factor. For example, if a trader would normally use $150,000 of SPY for a swing trade, the equivalent UPRO position starts at $50,000 (one-third notional) and drops to $25,000 if the trade might run beyond a few sessions.

Even with correct sizing on individual trades, aggregate exposure matters. Experienced practitioners cap total leveraged ETF exposure, all tickers combined, at 5-10% of total portfolio, with mainstream guidance closer to the lower end of that range.

Running leveraged ETFs in a clearly ring-fenced sleeve, separate from core long-term holdings, makes risk attribution cleaner. It prevents tactical positions from distorting overall portfolio metrics and creates a hard boundary that is visible at a glance. The $164.1 billion in US leveraged and inverse ETF assets across 572 funds as of early May 2026 confirms these instruments are mainstream enough to warrant systematic treatment rather than ad hoc use.

The core-and-satellite framework, typically structured as 75% broad index ETFs and 25% higher-conviction positions, provides a useful organisational model for the kind of ring-fenced trading sleeve described here, where leveraged ETF exposure sits clearly separate from long-term holdings and is bounded by a hard percentage cap.

Leveraged ETFs are not inherently irresponsible instruments. They require a fundamentally different risk-management approach from conventional index funds, one built around underlying-index exposure rather than dollar allocation.

The hierarchy of risk runs from a single-leg leveraged position through inverse hedges and pair trades to the margin-plus-leverage combination, each step representing an increase in complexity and potential loss speed. Getting the sizing right on the simplest configuration is the prerequisite for attempting anything more complex.

The $164.1 billion in this category and ongoing SEC enforcement activity on new high-leverage product launches (3x and 5x proposals flagged in March 2026) signal that these instruments will continue evolving. Staying current on brokerage requirements and regulatory guidance is part of using them responsibly.

Investors exploring adjacent structures after mastering position sizing for 3x daily-reset funds will find our deep-dive into leveraged covered call ETFs, which examines how a 1.25x equity overlay combined with a call-writing strategy produces a portfolio delta of approximately 0.92 alongside yields exceeding 13%, a meaningfully different risk profile from the instruments covered in this guide.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A leveraged ETF strategy uses funds that deliver a multiple of daily index returns, such as 3x, requiring position sizing based on underlying index exposure rather than dollar allocation, since a $10,000 position in a 3x fund carries three times the sensitivity of the same dollar amount in a non-levered fund.

Set your dollar risk budget, estimate the worst-case move in the underlying index, then divide by the leverage-adjusted fund move; for example, a 5% index move becomes roughly 15% at the fund level in a 3x product, so a $1,000 risk budget on a $100,000 portfolio implies an allocation of approximately $6,667.

SQQQ delivers -3x the daily Nasdaq-100 return, so roughly $33,000 of SQQQ approximates a -1x offset on $100,000 of QQQ-equivalent exposure for small moves over a single session, though practitioner consensus recommends hedging only 30-50% of tech exposure to limit daily decay costs.

Purchasing a 3x leveraged ETF on 2x margin creates an effective 6x exposure to the underlying index, meaning a 5% adverse index move produces a 30% loss on that position, an exponential risk multiplication that can cause portfolio-level damage in a single session.

Each trading day, a leveraged ETF recalculates its exposure from a new baseline, which causes compounding to work in the holder's favour during sustained directional trends but erodes value during choppy, alternating up-and-down sessions, even when the underlying index finishes flat over the period.