How to Value ASX REITs Using a Five-Test Framework

3 hrs ago

Most ASX biotechs share a predictable financial profile: no revenue, accelerating cash burn, and a survival strategy built on regular equity raises. Immuron (ASX: IMC; NASDAQ: IMRN) is structured differently in almost every respect. With a record AUD$7.3 million in FY25 sales, two FDA-cleared clinical assets targeting combined US peak sales of approximately US$500 million, and management guiding to improving profitability in FY26, the company represents a configuration that is genuinely rare among ASX biotech stocks. Understanding why requires examining all four pillars of the business model together: the commercial foundation, the clinical pipeline, the partnering strategy, and the path to breakeven. What follows is an explanation of each, and why their convergence in a single ASX-listed company creates a risk-return profile that is structurally different from the sector majority.

The standard ASX biotech operates on a well-worn loop. A company holds pre-clinical or early clinical assets, generates no revenue, and funds its operations through dilutive equity raises that erode shareholder value with each successive round. There is typically no near-term path to commercial sales, and survival depends on capital markets remaining open and receptive.

Probability-weighted valuation is the standard framework applied to development-stage biotechs, where each clinical milestone triggers a revision to the market’s assumed probability of eventual approval, and the magnitude of that revision, not reported earnings, drives the share price; this is precisely the framework that Immuron’s commercial revenue layer partially decouples from, because a funded, growing product line provides a valuation anchor that exists independently of clinical outcomes.

Immuron’s oral polyclonal antibody platform breaks that pattern. The same technology that underpins its clinical pipeline also powers two marketed products, Travelan (IMM-124E) and ProIBS, launched in Australia for irritable bowel syndrome in October 2025, generating revenue that does two things simultaneously: it validates the underlying platform in real-world commercial use, and it partially funds operations, reducing capital dependency.

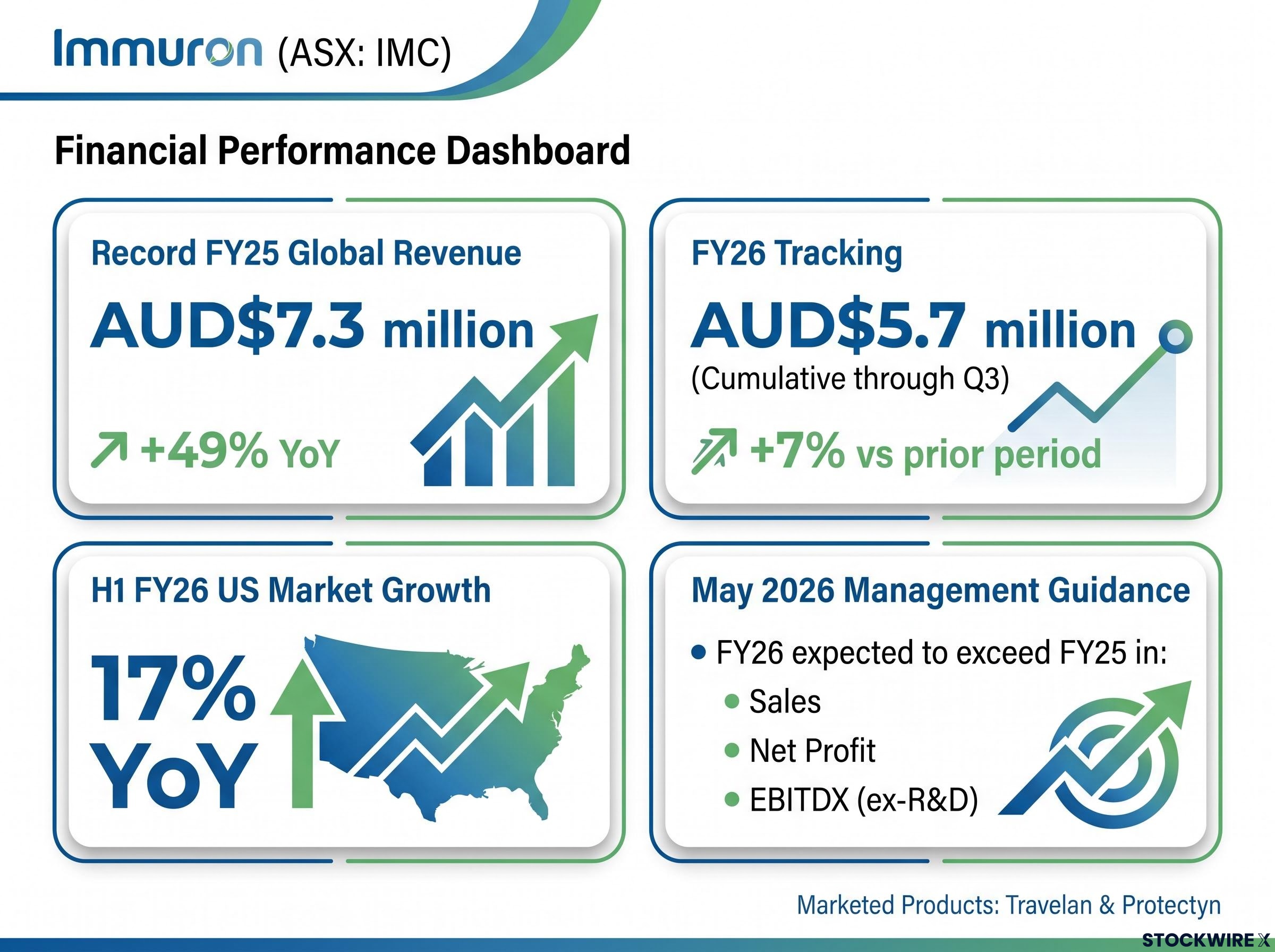

Record commercial sales: AUD$7.3 million in FY25 global revenue, up 49% year-on-year.

The trajectory has continued into FY26. Cumulative sales through Q3 FY26 reached AUD$5.7 million, up 7% on the prior corresponding period, with H1 FY26 US market growth of 17% year-on-year.

The contrast with the sector norm is direct:

For a company at Immuron’s stage, the most informative financial lens is not total profitability. It is whether the commercial operations can sustain themselves independently of the clinical investment layer. That is precisely what EBITDX (ex-R&D) measures.

EBITDX (ex-R&D) stands for earnings before interest, tax, depreciation, and foreign exchange movements, with R&D expenses, the R&D Tax Incentive, and R&D grants excluded from the calculation. Stripping out the R&D layer isolates the performance of the commercial business on its own terms.

Management guidance (May 2026): FY26 full-year sales, net profit, and EBITDX (ex-R&D) are each expected to exceed FY25 figures.

That guidance, anchored against FY25 record sales of AUD$7.3 million and FY26 already tracking above that pace, carries a specific implication. The commercial side of the business is trending toward a point where it covers its own costs without relying on capital raises.

This breakeven measure does not mean total company profitability. R&D spending will still appear on the income statement. What it means is that the commercial operations, the sales, distribution, and overhead costs of running the marketed product lines, are self-sustaining.

That is a meaningful structural shift. If, on top of commercial self-sufficiency, partnering proceeds arrive (covered below), the R&D investment layer could be funded through deal economics rather than equity issuance. Total profitability becomes achievable without serial capital raises, a scenario most ASX biotechs cannot credibly outline.

Polyclonal antibodies are mixtures of antibodies that target multiple parts of a pathogen at once, rather than locking onto a single specific target the way monoclonal antibodies do. That breadth of coverage can be advantageous when the objective is to neutralise a pathogen across several mechanisms of action simultaneously.

What distinguishes Immuron’s platform is oral delivery. The antibodies are formulated to be taken by mouth rather than injected, which is clinically relevant for gastrointestinal indications where the therapeutic target sits in the gut. For conditions like traveller’s diarrhoea or C. difficile infection, delivering antibodies directly to the site of disease through an oral route aligns the delivery mechanism with the biology of the target.

The platform has received multiple Investigational New Drug (IND) approvals from the US Food and Drug Administration (FDA), a regulatory milestone that carries weight beyond paperwork.

For Immuron, multiple IND clearances across its platform’s programmes represent repeated regulatory validation of both the company’s scientific approach and its manufacturing capability.

The FDA regulatory environment facing ASX biotechs with US market strategies has become materially more complex in 2025-2026, with staffing reductions exceeding 1,300 employees creating unpredictable approval backlogs particularly for novel therapeutic platforms, a structural headwind that makes the credibility signalled by Immuron’s existing multiple IND clearances more valuable, not less, as the agency’s review capacity tightens.

IMM-124E targets traveller’s diarrhoea, a condition that affects tens of millions of international travellers annually. The asset has progressed to a stage where it qualifies for an end-of-Phase 2 meeting with the FDA, a regulatory milestone that establishes the pathway for late-stage development. US peak sales for IMM-124E are estimated at approximately US$100 million.

IMM-529 targets clostridioides difficile infection (CDI), a serious and often recurrent gastrointestinal infection that imposes high morbidity and healthcare costs, particularly in hospital and aged-care settings. CDI’s clinical severity and recurrence profile make it a significant unmet medical need. IMM-529 has received FDA IND clearance to proceed into Phase 2 clinical trials. Its US peak sales potential is estimated at approximately US$400 million, positioning it as the larger value driver in the portfolio.

CDC CDI surveillance data documents the ongoing burden of clostridioides difficile across both community and healthcare settings in the United States, with hospital-onset and community-associated cases tracked separately to reflect the distinct patient populations and recurrence patterns that make CDI a persistent unmet medical need.

| Asset | Indication | Clinical stage | US peak sales estimate |

|---|---|---|---|

| IMM-124E | Traveller’s diarrhoea | Eligible for end-of-Phase 2 FDA meeting | ~US$100 million |

| IMM-529 | Clostridioides difficile infection | FDA IND clearance for Phase 2 | ~US$400 million |

Combined US peak sales opportunity: approximately US$500 million across both assets, built on the same validated commercial platform.

Two FDA-cleared assets on a single platform, each targeting a distinct gastrointestinal indication with a defined US market, create a pipeline with layered value. IMM-124E offers nearer-term clinical progression; IMM-529 offers the larger commercial prize. Together, they provide the commercial context for the partnering strategy that follows.

The standard ASX biotech funding loop works like this: raise equity, spend on trials, dilute shareholders, raise again. Each cycle erodes long-term shareholder value, and the process depends entirely on capital markets remaining receptive. For companies with large-scale Phase 2 and Phase 3 programmes ahead, the cumulative dilution can be substantial.

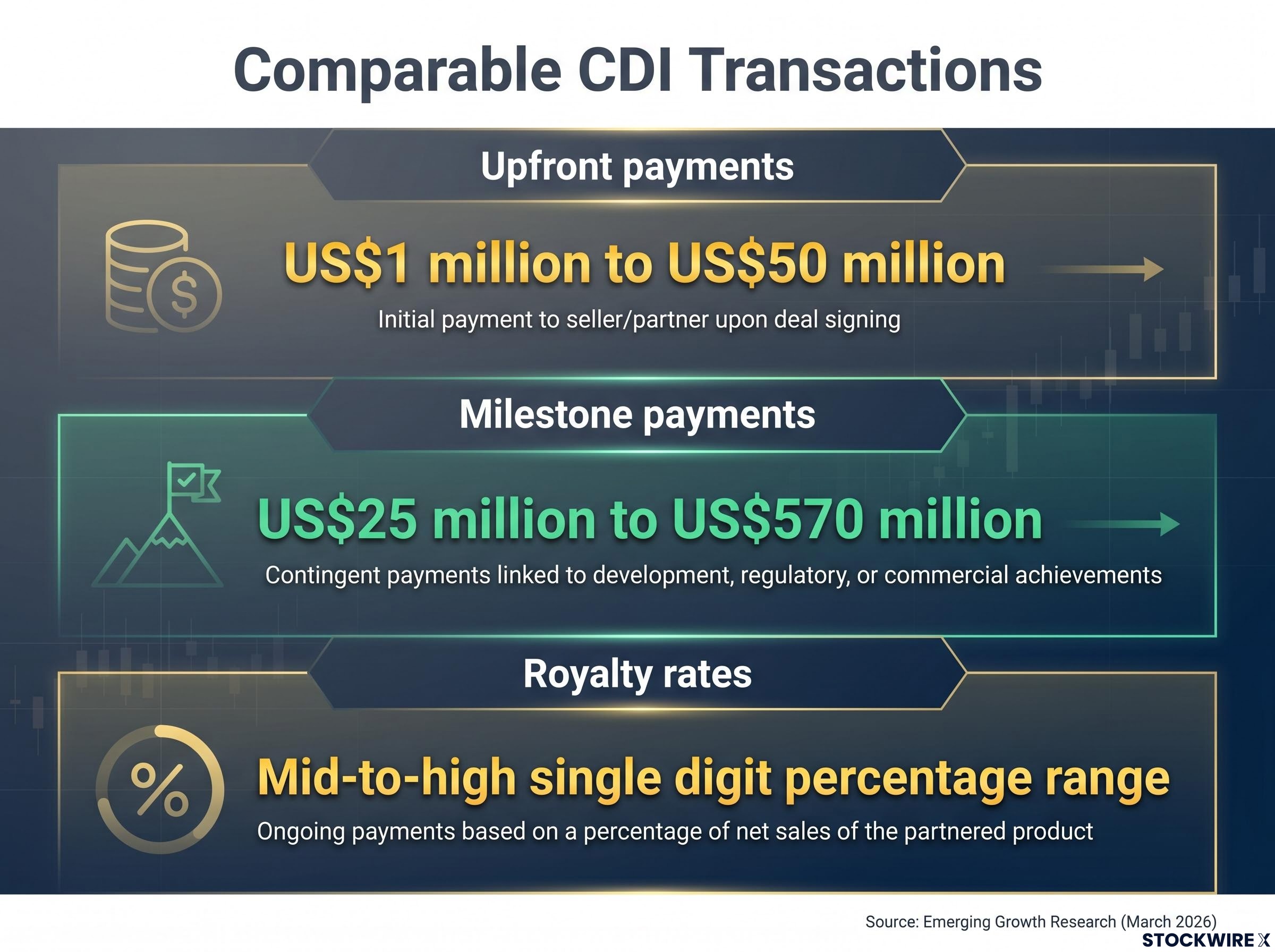

Immuron’s partnering model is a deliberate structural alternative. Under this approach, a larger pharmaceutical or biotech partner funds the trial and commercial infrastructure in exchange for regional or global rights to the asset. Immuron monetises its intellectual property through three channels: upfront payments, development and regulatory milestone payments, and ongoing royalties on commercial sales.

According to Emerging Growth Research’s analysis of comparable CDI partnering transactions (March 2026), deal structures in the space have followed these ranges:

| Deal component | Range from comparable transactions |

|---|---|

| Upfront payments | US$1 million to US$50 million |

| Milestone payments | US$25 million to US$570 million |

| Royalty rates | Mid-to-high single digit percentage range |

At realistic deal terms within those ranges, an IMM-529 partnership could be financially transformational relative to Immuron’s current market capitalisation. The partnering approach changes the company’s financial profile in three specific ways:

The IMM-529 partnering strategy has been a consistent management priority through early 2026, with the A$10.0 million cash position providing approximately 22.5 months of runway and giving Immuron negotiating leverage in licensing discussions without the near-term capital raise pressure that typically constrains smaller ASX biotech companies.

Individually, none of Immuron’s four distinguishing features are unique in global biotech. Revenue-generating biotechs exist. FDA-cleared pipelines exist. Partnering strategies exist. Breakeven trajectories exist. What is uncommon, particularly on the ASX, is their convergence in a single company at this scale and stage.

The ASX biotech sector is dominated by pre-revenue, cash-consuming development companies. A company that combines growing commercial sales, multiple FDA-cleared pipeline assets, a partnering-led development model, and a credible operating breakeven trajectory presents a risk-return profile that does not fit the sector’s default template.

ASX biotech binary risk is a structural feature of development-stage companies that Immuron’s model partially mitigates: while pre-revenue biotechs are entirely dependent on clinical readouts to validate their investment case, a company with growing commercial sales and a self-sustaining product line has a financial floor that does not disappear if a single trial misses its endpoint.

The combination of commercial revenue, an FDA-cleared pipeline, partnering-led development, and a breakeven trajectory creates a risk profile that is structurally different from the sector majority. That does not remove clinical, regulatory, or commercial execution risk. It does mean the framework for evaluating those risks is different from the one investors typically apply to ASX development biotechs.

Readers seeking further detail on Immuron’s investment case may consult the Emerging Growth Research analyst report (March 2026), available via the Immuron investor relations page at investors.immuron.com.au/analyst-reports.

The forward-looking catalysts that will shape the next phase of the investment case are:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including management guidance and peak sales estimates, are subject to change based on market developments, clinical outcomes, and company performance. Past performance does not guarantee future results.

EBITDX ex-R&D measures earnings before interest, tax, depreciation, and foreign exchange movements, with all R&D costs stripped out, so investors can assess whether a biotech's commercial operations are self-sustaining independently of its clinical spending. For Immuron, management has guided that this metric will improve in FY26, signalling the marketed product business is trending toward covering its own costs without relying on equity raises.

Immuron's pipeline includes IMM-124E, targeting traveller's diarrhoea with an estimated US peak sales opportunity of approximately US$100 million, and IMM-529, targeting clostridioides difficile infection with an estimated US peak sales opportunity of approximately US$400 million, for a combined US peak sales estimate of around US$500 million.

Rather than funding late-stage trials through repeated equity raises, Immuron is pursuing licensing deals where a larger pharmaceutical partner covers trial costs in exchange for regional or global rights, with Immuron receiving upfront payments, milestone payments, and royalties. Comparable CDI partnering transactions have involved upfront payments of US$1 million to US$50 million and milestones of US$25 million to US$570 million, according to Emerging Growth Research.

An Investigational New Drug clearance from the FDA is the formal regulatory permission required before a company can begin human clinical trials in the United States, and it is only granted after the agency reviews preclinical safety data, manufacturing quality, and the proposed trial design. Multiple IND clearances across a platform, as Immuron has received, signal repeated regulatory acceptance of both the underlying science and the company's manufacturing capability.

Because Immuron generates recurring commercial sales from Travelan and its recently launched ProIBS product, it has a financial floor that does not disappear if a single clinical trial misses its endpoint, unlike pre-revenue biotechs whose entire investment case depends on clinical readouts. FY25 commercial revenue reached a record AUD$7.3 million, up 49% year-on-year, with FY26 cumulative sales through Q3 tracking 7% above the prior corresponding period.