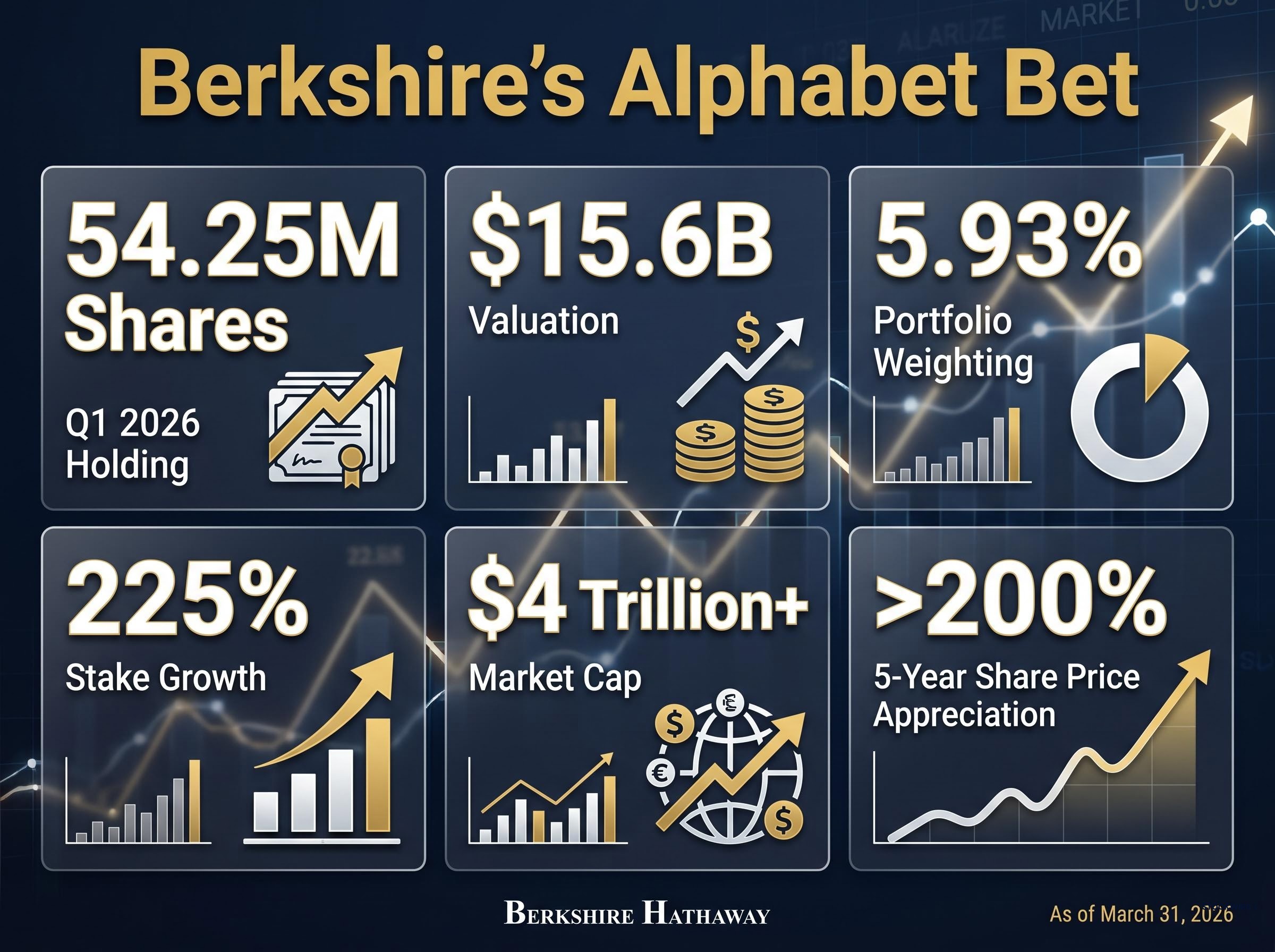

When one of the most closely watched investment portfolios in the world nearly triples a position in a single company at a $4 trillion-plus market capitalisation, the instinct is to ask what just happened. The better question is what it teaches. Berkshire Hathaway’s Alphabet stake, which grew approximately 225% to roughly 54.25 million shares valued at approximately $15.6 billion as of Q1 2026 13F filings, is not primarily a story about one stock pick. It is a public demonstration of economic moat investing applied at scale in a market that many investors find difficult to navigate. This article uses Berkshire’s Alphabet position as a concrete, real-world lens for identifying moat-protected businesses. By the end, readers will have a working checklist grounded in Warren Buffett’s documented principles, not abstract theory, that they can apply to their own portfolios.

What Berkshire’s Alphabet bet actually tells us

The numbers are worth sitting with before moving past them.

Berkshire’s Alphabet position: approximately 54.25 million GOOGL shares, valued at roughly $15.6 billion, representing a 225% stake increase across the reported update period.

That scale of commitment to a single name, at a moment when Alphabet’s market cap already exceeded $4 trillion and its share price had appreciated more than 200% over the preceding five years, is not a casual addition. It is a conviction bet backed by a specific analytical framework.

The confirmed position details:

- Q1 2026 holding: approximately 54.25 million GOOGL shares

- Valuation: approximately $15.6 billion

- Portfolio weighting: approximately 5.93% of Berkshire’s disclosed portfolio

- Alphabet market cap at time of purchase: exceeding $4 trillion

- Stake growth: approximately 225% across the reported update period

It is worth noting that sources conflict on the precise quarter Berkshire first established its Alphabet position; some reporting points to Q1 2025, while independent research suggests the stake was initiated in Q3 2025 at approximately 17.8 million shares. The cumulative position reflected in the Q1 2026 filing, however, is confirmed across multiple sources.

The natural reader instinct here is to treat this as a buy signal: Berkshire bought it, so should I? That instinct misses the more durable takeaway. Greg Abel, Berkshire’s new chief executive, has been characterised as more receptive to technology investments than Buffett historically was, though direct reporting on his specific influence remains thin. What is visible, and what the 13F filing makes available to any individual investor, is the analytical framework that a company must pass before earning this level of capital allocation. The rest of this article unpacks that framework.

Greg Abel’s capital allocation approach since assuming the CEO role at the start of 2026 has been characterised by a wider technology aperture than Buffett’s, with the Alphabet stake representing one of the clearest early signals that the post-Buffett era will not simply mirror the investment patterns of the previous three decades.

When big ASX news breaks, our subscribers know first

Understanding the economic moat: the concept behind the investment decision

The term “economic moat” is one that many investors have encountered but fewer could define precisely enough to apply. At its core, an economic moat is a structural competitive advantage that allows a business to defend its profitability and market position over time. It is not a hot product, a single quarter of strong earnings, or a favourable news cycle. It is a durable barrier that makes it difficult for competitors to replicate the company’s economics.

Morningstar formalised Buffett’s original concept into five sources of competitive advantage, covering intangible assets, switching costs, network effects, cost advantage, and efficient scale, with companies that exhibit multiple reinforcing sources considered materially more durable than those relying on a single driver.

Buffett has articulated this preference repeatedly in public statements: a high-quality business purchased at a reasonable price is preferable to a mediocre business purchased at a discount.

Buffett’s documented principle: A high-quality business at a reasonable price is preferable to a mediocre business at a discounted price.

The distinction sounds obvious in isolation. In practice, it cuts against one of the most common screening habits among retail investors: sorting by valuation multiples and gravitating toward whatever appears cheapest. Moat analysis asks a different first question. Not “is it cheap?” but “is it durable?”

When the sector does not save you

Spirit Airlines offers a sharp illustration of what the absence of a moat looks like in practice. Spirit operated in the same aviation industry as larger, better-capitalised carriers. When fuel costs rose, the airline lacked the pricing power, brand loyalty, or cost structure to absorb the pressure. It collapsed, not because the airline industry was doomed, but because Spirit had no structural protection within it.

A moat-protected operator in a similarly pressured industry can raise prices, retain customers, or absorb input-cost increases through scale advantages. The protection is company-specific, not sector-wide. A technology company with no moat is more dangerous to own than a consumer staples company with a deep one; sector labels do not confer durability.

The four moat signals Alphabet passes

The value of moat analysis lies in its repeatability. The four signals below are not conclusions about Alphabet; they are diagnostic questions that any investor can apply to any company. Alphabet simply makes the process visible because the answers are publicly available.

| Moat Signal | Diagnostic Question | How Alphabet Answers It | Why It Matters to Investors |

|---|---|---|---|

| Brand dominance | Does the brand remove price as the primary competitive variable? | Identified as the world’s most valuable brand in recent rankings | Brand strength supports premium pricing and customer retention across cycles |

| Pricing power | Can the company raise prices without losing customers? | Advertising pricing reflects demand-driven auction economics with limited substitution risk | Pricing power is the most testable moat signal using public data |

| Durable cash generation | Does the business generate consistent free cash flow across market conditions? | Alphabet’s cash generation has persisted through multiple market cycles | Consistent cash flow funds reinvestment and signals structural advantage |

| Technology talent and infrastructure | Does the company possess capabilities competitors cannot easily replicate? | Described as possessing one of the strongest technology development teams in the US; Apple AI partnership deepens platform embeddedness | Talent moats compound over time as institutional knowledge accumulates |

Brand and pricing power

Alphabet’s identification as the world’s most valuable brand, according to brand valuation rankings, is more than a headline. In Buffett’s framework, brand strength matters because it differentiates a company from competitors in a way that removes price as the sole variable customers consider. When advertisers choose Google’s search platform, they are not comparison-shopping on cost alone; they are buying access to an audience and intent-matching infrastructure that no alternative replicates at equivalent scale.

The pricing power test asks a direct question: can the company raise prices without losing customers to competitors? In Alphabet’s case, the advertising auction model means pricing is demand-driven. As long as advertiser demand persists, which it has across multiple cycles, the economics hold.

AI infrastructure and talent

Google possesses what is described as one of the strongest technology development teams in the United States. That assessment was tested publicly when ChatGPT launched and Alphabet initially appeared to be on the back foot in artificial intelligence. The perception gap was real; for a period, competitors appeared to have leapfrogged Google’s AI capabilities.

What followed was a reassertion. Alphabet’s partnership with Apple to provide foundation AI models embedded Google’s infrastructure more deeply into mainstream consumer platforms, not as a peripheral feature but as a foundational layer. This is a moat that was tested and held, which is more informative than a moat that was never challenged.

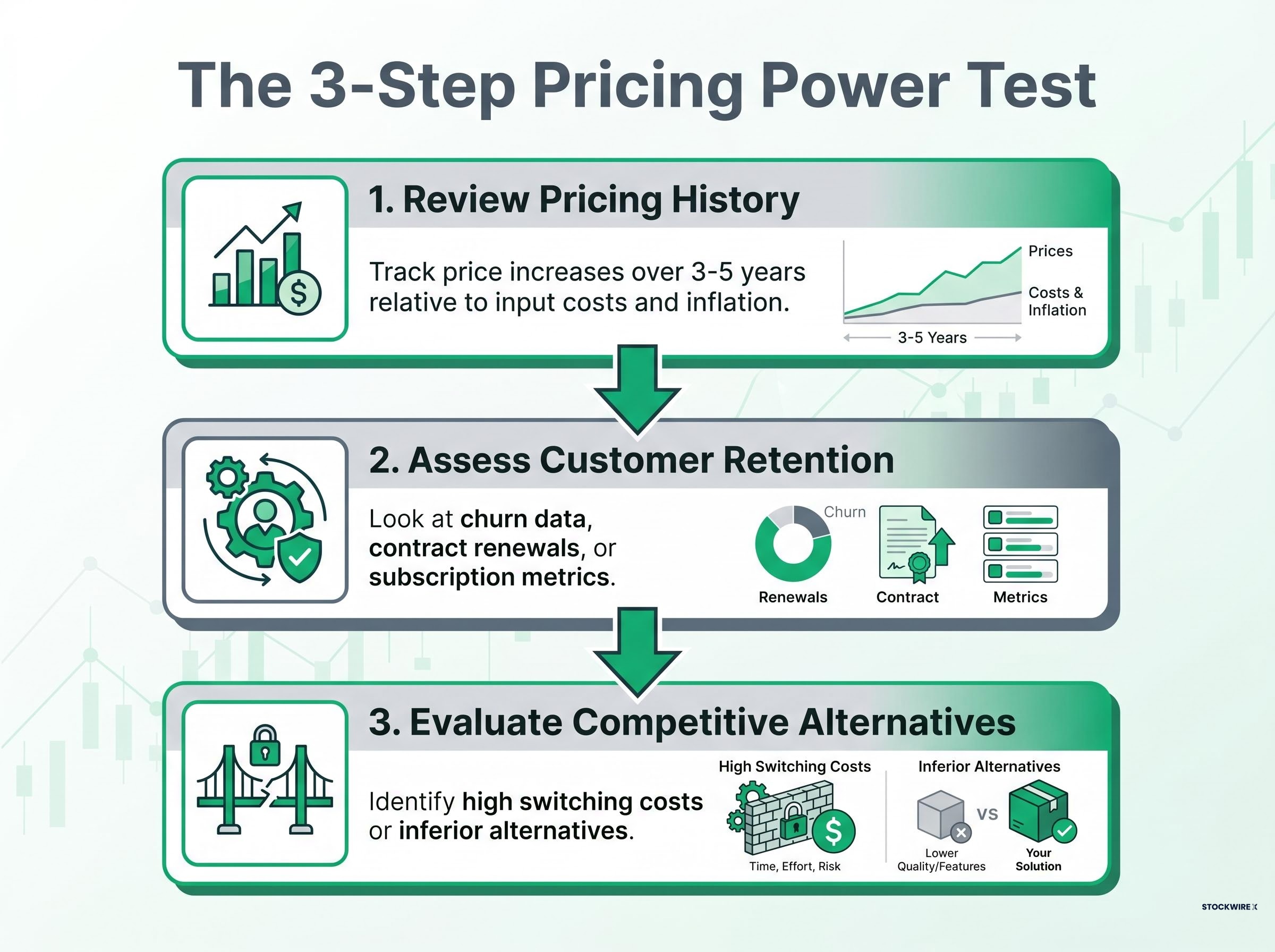

The pricing power test: the single most useful moat diagnostic

If one signal had to do the work of all four, pricing power would be the one. It is the most operationally testable moat characteristic available to individual investors because it can be assessed through publicly available information without institutional research access.

Buffett’s litmus test: Can the business raise prices without losing customers to competitors?

The elegance of this test is its binary clarity. A company either demonstrates sustained pricing power or it does not. Consistent cash generation over time is a downstream signal that pricing power has held; if a business maintains strong free cash flow across varying economic conditions, the pricing structure is holding.

For any company under evaluation, a three-step approach makes this test practical:

- Review pricing history. Examine whether the company has raised prices over the past three to five years and track the trajectory of those increases relative to input costs and inflation.

- Assess customer retention. Look at publicly available churn data, contract renewal rates, or subscription metrics. If prices rose and customers stayed, the signal is positive.

- Evaluate competitive alternatives. Identify what a customer would switch to if prices increased further. If the alternatives are meaningfully inferior or the switching costs are high, the moat is likely real.

No institutional research subscription is required for any of these steps. Earnings call transcripts, annual reports, and competitor filings provide the raw material. This makes pricing power the most accessible entry point into moat analysis for individual investors building their own research process.

A transferable moat checklist for your own stock research

The Alphabet case study has illustrated how four moat signals apply to one specific company. The step that converts this from observation into methodology is generalisation: a checklist that works regardless of which company appears on the screen.

The following seven-point framework is derived directly from the principles and signals covered in this article, each phrased as a diagnostic question:

- Does the company possess a brand or market position that removes price as the primary competitive variable?

- Can the company raise prices without losing customers to competitors?

- Does the business generate consistent free cash flow across varying market conditions?

- Does the company hold capabilities, whether in talent, infrastructure, or intellectual property, that competitors cannot easily replicate?

- Is the company’s competitive advantage structural (built into the business model) rather than cyclical (dependent on favourable market conditions)?

- Has the moat been tested by competitive pressure, a new entrant, or a market downturn, and did it hold?

- Is the current price reasonable relative to the quality and durability of the moat, rather than simply cheap relative to peers?

The relationship between moat quality and valuation is where many applications of the framework break down; Morningstar’s own approach treats them as independent variables, assessing competitive durability first and then asking separately whether the current price is justified, because a wide moat at an unjustifiable price is not a margin of safety.

Moat-protected companies tend to decline less and rebound more quickly during market downturns. That characteristic makes this framework particularly valuable during periods of volatility or apparent overvaluation, precisely when the temptation to abandon quality for discount is strongest.

Individual investors hold a structural advantage that is easy to overlook. Unlike Berkshire, which must deploy billions and is locked out of smaller opportunities by its own scale, retail investors can add capital continuously and access small-cap opportunities that institutional portfolios cannot touch. The checklist above is, paradoxically, more actionable for a retail investor than for the institution whose investment inspired it.

A few behavioural principles complement the analytical framework:

- Panic selling during downturns has been shown repeatedly by research to cost investors more than it returns over time

- Market-timing strategies, moving to cash and attempting to re-enter at lower prices, historically underperform consistent long-term investing through volatility

- Compounding returns accrue to the investor who applies consistent criteria across market cycles, not to the investor who applies the best criteria once

The moat framework matters most when markets make it hardest to use

Berkshire’s Alphabet investment required a specific form of discipline that is easy to admire and difficult to replicate. Buying a company whose share price had already appreciated more than 200% over five years, at a market capitalisation exceeding $4 trillion, is not what a price-focused investor would do. A price-focused investor would have screened Alphabet out long before the position was established.

What made the investment possible was conviction in the moat framework. The framework’s criteria, brand dominance, pricing power, cash generation, and infrastructure depth, were all met. The price was reasonable relative to the quality of the underlying business. That was enough.

The lesson extends beyond any single position. Research has shown consistently that panic selling and market-timing strategies cost investors more than they return over time. The moat framework’s value is not purely analytical; it is psychological. It provides a consistent set of criteria that anchor decision-making when market conditions create the most pressure to abandon process.

Dalbar’s Quantitative Analysis of Investor Behavior tracks the annual gap between market returns and the returns average equity investors actually capture, and its findings consistently show that behavioral errors, particularly panic selling and ill-timed market exits, account for a substantial portion of that underperformance.

Berkshire’s Alphabet position is now too large, and the entry point too far in the past, for individual investors to replicate directly. The checklist that the investment illustrates, however, is not. It can be opened alongside a brokerage screen tomorrow morning and applied to any company, at any market capitalisation, in any sector. The framework is the transferable asset. Consistent application across market cycles, especially the uncomfortable ones, is what separates knowing from doing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.