Most investors fixate on what a company earns today. The ones with the strongest long-term track records tend to obsess over a different question: whether those earnings can survive competition for the next 20 years. That question sits at the heart of economic moat investing, a framework popularised by Warren Buffett and formalised by Morningstar’s equity research team into a structured, analyst-driven rating system. In Australia, the VanEck Morningstar Wide Moat ETF (ASX: MOAT) offers the most direct way for retail investors to access this philosophy through a single ASX-listed vehicle. What follows is an explainer covering what an economic moat actually is, why some businesses have one and most do not, how Morningstar screens for them, and how MOAT’s methodology differs structurally from simply buying the S&P 500 through a standard index fund. By the end, readers will know whether this style of investing matches their philosophy and what the real trade-offs look like.

Why competitive advantages erode faster than most investors expect

In competitive markets, above-average returns on capital attract rivals. New entrants copy products, undercut pricing, and erode margins. Over time, most companies’ profitability reverts toward the industry average, often faster than shareholders anticipate.

The analytical challenge is distinguishing which businesses have structural characteristics that slow or prevent this erosion from those that merely look durable because they have had a strong run. The difference matters enormously to long-term returns, yet the two categories often look identical in a snapshot of current earnings.

Buffett framed this distinction as a moat: a durable competitive advantage protecting a business the way a medieval castle’s moat protects against attackers. The wider the moat, the longer the protection is expected to hold.

Buffett’s investment philosophy rests on exactly this discipline: identifying businesses with structural protection and waiting for the price to reflect less than intrinsic value before committing capital, a practice that produced Berkshire Hathaway’s long-run record and now sits at the centre of debates about whether Greg Abel will maintain the same rigour.

Morningstar formalised the concept into an analyst-assigned rating system with three tiers:

- No moat: no identifiable sustainable advantage

- Narrow moat: competitive advantages expected to sustain excess returns for at least 10 years

- Wide moat: advantages expected to sustain excess returns for 20 years or more

The distinction between companies that look durable and those with genuine structural protection sharpens when the question shifts from “is this business profitable?” to “what specifically prevents a well-funded competitor from replicating this business within a decade?”

- Companies that look durable: high current margins, strong recent growth, a well-known brand, a dominant market position today

- Companies with genuine structural protection: identifiable barriers to replication, pricing power that persists through downturns, cost structures competitors cannot match without decades of investment

Investors who skip this conceptual grounding tend to confuse current profitability with durable profitability, a mistake that leads to overpaying for businesses whose advantages are more fragile than they appear.

When big ASX news breaks, our subscribers know first

The five sources of a genuine economic moat

Morningstar’s equity research team identifies five distinct sources of durable competitive advantage. A company may hold one or several simultaneously; the combination generally produces a stronger and longer-lasting moat. Understanding each source gives investors a practical checklist applicable to any business.

Morningstar’s economic moat rating assigns one of three tiers to each covered company based on analyst assessment of whether competitive advantages can sustain excess returns on invested capital for a defined period, with the wide moat tier requiring a 20-year durability threshold that fewer than 20% of covered companies typically meet.

Intangible assets

Brands, patents, and regulatory licences create barriers that competitors cannot easily replicate. A pharmaceutical company holding patent protection on a blockbuster drug faces no direct competition for the duration of that patent. A consumer brand with decades of trust, such as a dominant luxury goods house, commands pricing power that new entrants cannot manufacture overnight. Regulatory licences in industries such as banking or telecommunications restrict competition by design.

Cost advantages and efficient scale

Some businesses operate at a structural cost advantage that competitors cannot match without equivalent scale or infrastructure investment. A global distributor with decades of supply chain optimisation can price below smaller rivals while maintaining margins. Efficient scale applies where the market is only large enough to support one or two profitable operators, creating a natural monopoly dynamic. Airports, regulated utilities, and toll road operators frequently benefit from this source.

Switching costs and network effects

Enterprise software providers benefit from switching costs: once a company has integrated a platform into its operations, trained its staff, and built workflows around it, the cost of moving to a competitor is substantial. This lock-in effect produces recurring revenue and high retention rates.

Network effects operate differently but with similar durability. A payments platform becomes more valuable to merchants as more consumers use it, and more valuable to consumers as more merchants accept it. Each additional user strengthens the network’s competitive position. Dominant platform businesses and payment networks are among the most frequently cited examples.

Morningstar’s wide moat designation requires analysts to assess sustainability, not just current strength. A company may exhibit network effects today, but if the network is vulnerable to disruption or regulatory intervention, the moat rating reflects that fragility.

Morningstar’s wide moat designation requires analysts to assess sustainability, not just current strength, and moat trajectory matters as much as the initial classification: an advantage that is widening produces a very different long-term return profile than one that is stable or slowly eroding under competitive or technological pressure.

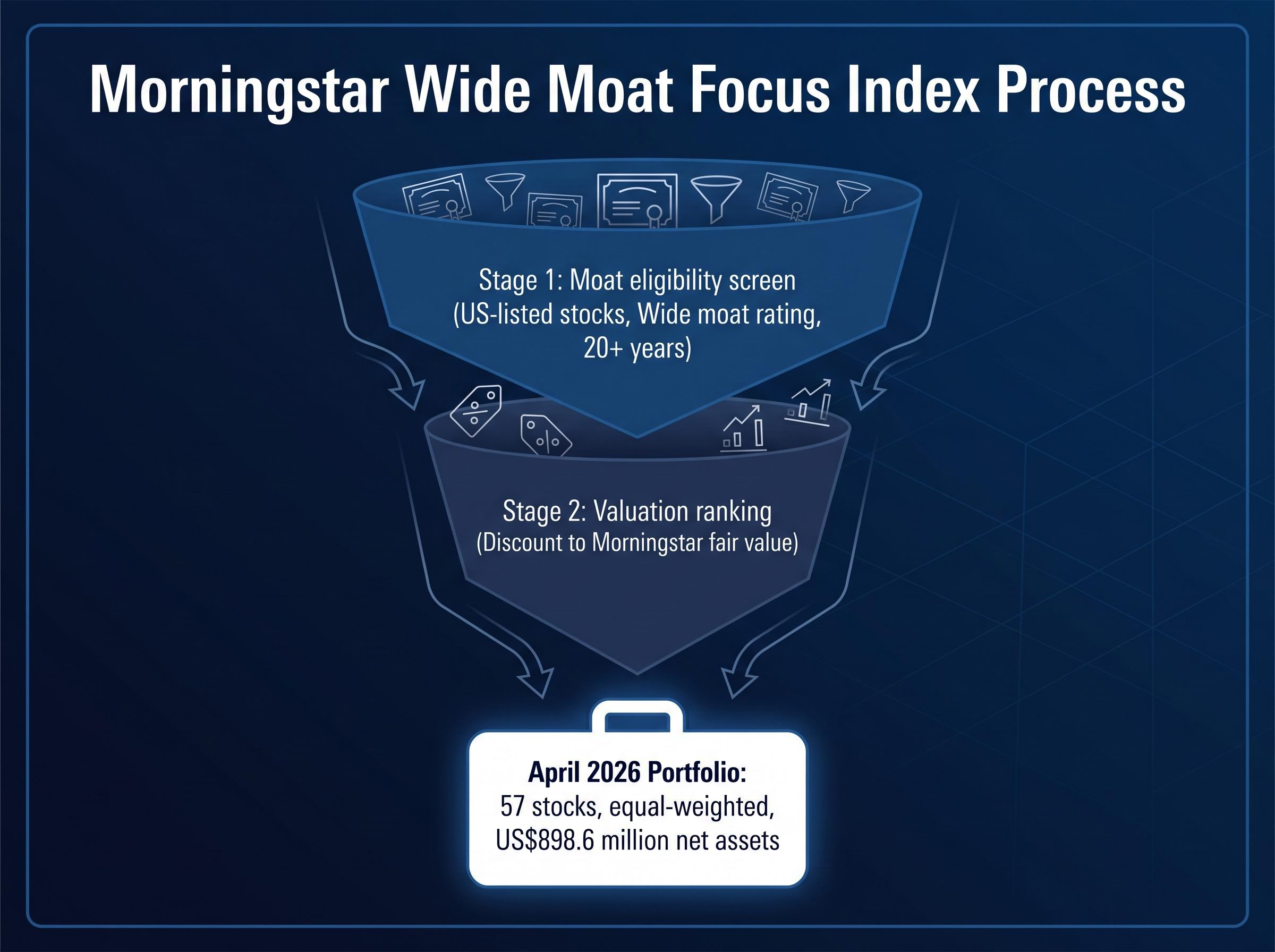

How Morningstar turns a philosophy into a stock-screening process

The Morningstar Wide Moat Focus Index, which MOAT tracks, uses a two-stage construction process that combines quality screening with valuation discipline:

- Moat eligibility screen: only US-listed stocks assigned a wide moat rating by Morningstar’s equity analysts are eligible for inclusion. This filters the universe down to companies whose competitive advantages are assessed as sustainable for 20 years or more.

- Valuation ranking: among eligible wide-moat stocks, the index ranks candidates by their discount to Morningstar’s fair value estimate and selects the most undervalued names. A wide-moat company trading at or above fair value gets excluded in favour of one offering a larger margin of safety.

A wide moat rating reflects Morningstar’s assessment that a company possesses durable competitive advantages expected to sustain excess returns on invested capital for 20 years or more.

This valuation overlay is the mechanism that distinguishes MOAT from a simple quality screen. The fund does not merely buy good businesses; it buys good businesses when they are cheap relative to Morningstar’s assessment of intrinsic value.

| Stage | Filter applied | What gets excluded |

|---|---|---|

| 1. Moat screen | Wide moat rating from Morningstar analysts | Companies with no moat or narrow moat ratings |

| 2. Valuation ranking | Largest discount to Morningstar fair value estimate | Wide-moat stocks trading at or above fair value |

The index rebalances quarterly, triggering regular additions and removals. Stocks are added when their prices fall or their fair value estimates are upgraded, increasing the discount. Stocks are removed when they rally close to or above fair value. This means the top holdings can change materially at each reconstitution.

As of the April 2026 factsheet, MOAT holds 57 stocks, is equal-weighted (meaning no single stock dominates the portfolio), and has net assets of approximately US$898.6 million. The management expense ratio sits at 0.49% per annum.

What MOAT actually owns and how that differs from a standard S&P 500 fund

The structural differences between MOAT and broad US index trackers such as IVV, VTS, or VGS are significant enough to produce materially different portfolio behaviour. The comparison matters because Australian investors will find these funds sitting side by side on their broker platform.

| Feature | MOAT | IVV / VTS / VGS |

|---|---|---|

| Index tracked | Morningstar Wide Moat Focus Index | S&P 500 / Total US Market / Global |

| Stock count | 57 | 500+ |

| Weighting method | Equal-weighted | Market-cap weighted |

| Selection criteria | Wide moat + discount to fair value | Market capitalisation |

| Mega-cap tech exposure | Lower (valuation-constrained) | Higher (cap-weighted) |

| MER | 0.49% p.a. | 0.03%-0.18% |

| Rebalancing frequency | Quarterly (active reconstitution) | Periodic (index-driven) |

Equal weighting is the structural feature with the most visible consequences. In a cap-weighted index, the largest companies by market capitalisation dominate portfolio returns. In MOAT, a mid-cap company with a strong moat carries the same weight as a mega-cap name. This is structurally impossible in a cap-weighted fund.

The valuation constraint compounds the difference. When the largest technology stocks trade above Morningstar’s fair value estimates, the methodology systematically reduces or eliminates exposure to them. The result is a portfolio that can look meaningfully different from the S&P 500 in both sector and size composition, historically tilting heavier toward healthcare and quality technology names while remaining lighter in mega-cap growth.

The three sharpest structural differences for investors comparing the two approaches:

- Concentration: 57 stocks versus 500-plus creates a fundamentally different risk and return profile

- Weighting: equal weight versus cap weight means MOAT’s returns are not dominated by a handful of mega-caps

- Selection logic: moat-plus-valuation versus pure market capitalisation means MOAT is simultaneously a quality screen and a value discipline

The honest trade-offs: when moat investing lags and why that is not always a red flag

Concentrated factor strategies, including quality and moat-based approaches, have underperformed cap-weighted indices for extended periods. The 2020-2023 stretch was a pronounced example, when a small number of mega-cap technology stocks drove the majority of S&P 500 returns.

The structural reason is straightforward. When the market’s biggest winners are also the most expensive relative to fundamental value, MOAT’s valuation screen systematically excludes or underweights them. During momentum-driven bull markets where a narrow group of stocks pulls the index higher, this creates a performance headwind that can persist for years.

The interaction between moat ratings and AI valuations has become one of the more contested areas of Morningstar’s framework in 2026, with Nvidia and Broadcom holding wide moat designations underpinned by CUDA switching costs and custom silicon lock-in, while names like Micron carry no moat rating despite significant price rallies driven by thematic AI association.

The core trade-off: a higher fee (0.49% p.a. versus 0.03%-0.18% for broad index funds), combined with a concentrated factor tilt, requires tolerance for tracking error. If outperformance does not materialise over the investor’s holding period, the fee differential compounds against them.

Three specific scenarios where MOAT is likely to lag a broad index fund:

- When a small number of mega-cap stocks drive the majority of index returns and those stocks trade above Morningstar’s fair value estimates

- When momentum and growth factors outperform value and quality factors for sustained periods

- When the quarterly rebalancing rotates into names that have further to fall before the market recognises their intrinsic value

Australian commentary has consistently positioned MOAT as a satellite or complementary holding rather than a core index fund replacement, recognising these dynamics. Investors who understand why MOAT can lag for years are far better positioned to hold it through those periods than investors who bought it expecting consistent outperformance.

Tracking error is not evidence the approach is broken. It is the expected cost of a differentiated methodology, and the patience required is part of what the strategy demands.

How Australian investors are using MOAT within a broader portfolio

The recurring consensus in Australian financial commentary frames MOAT as a satellite holding that complements, rather than replaces, a core allocation to low-cost broad index funds such as IVV, VTS, or VGS.

The logic has a geographic dimension. The ASX is heavily concentrated in financials, mining, and resources. US-focused quality-screened funds provide sector diversification that Australian equities alone cannot deliver, giving investors exposure to healthcare, technology, and consumer businesses with durable competitive advantages.

Practical considerations for Australian investors evaluating whether to add MOAT as a satellite holding:

- Conviction in the methodology: investors who believe Morningstar’s moat analysis adds genuine informational value beyond what a cap-weighted index captures have a reasonable case for inclusion

- Fee tolerance: at 0.49% per annum, MOAT costs materially more than broad index alternatives; investors need to be comfortable with that drag compounding over long time horizons

- Time horizon: MOAT is suited to investors who can hold across full style cycles, accepting multi-year periods where the fund lags the broader market

- Portfolio role: pair MOAT with low-cost index funds for diversification; it is not designed to function as a standalone core holding

The decision is not whether moat investing is “better” than index investing. It is whether the investor’s philosophy, fee tolerance, and time horizon align with a quality-and-valuation discipline that will, by design, behave differently from the broader market.

For investors ready to move from evaluating MOAT to deciding how large a satellite allocation fits their circumstances, our dedicated guide to structuring an ETF portfolio covers asset allocation frameworks, the consequences of cap-weighted domestic concentration, and the practical mechanics of combining a factor-based satellite with low-cost core index funds.

Economic moats are a lens, not a guarantee

The moat framework offers a rigorous way to think about durable competitive advantage, and MOAT provides a systematic, ETF-accessible way to act on it. No methodology eliminates market risk or guarantees outperformance.

Morningstar’s moat ratings are analyst judgements, not objective facts. The quarterly rebalancing reflects the reality that valuations shift and competitive dynamics change. A wide moat today does not mean a wide moat in perpetuity.

This approach is designed for investors who want their equity exposure to reflect a quality and valuation discipline, who understand that means accepting periods of divergence from the broader market, and who are building a portfolio intended to hold across full market cycles.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Investors considering MOAT may wish to review VanEck Australia’s product page for current holdings, factsheet data, and performance history, and to assess their own risk tolerance, time horizon, and existing portfolio composition before making any allocation decision.