How Wesfarmers Buys, Builds, and Exits to Create Value

4 hrs ago

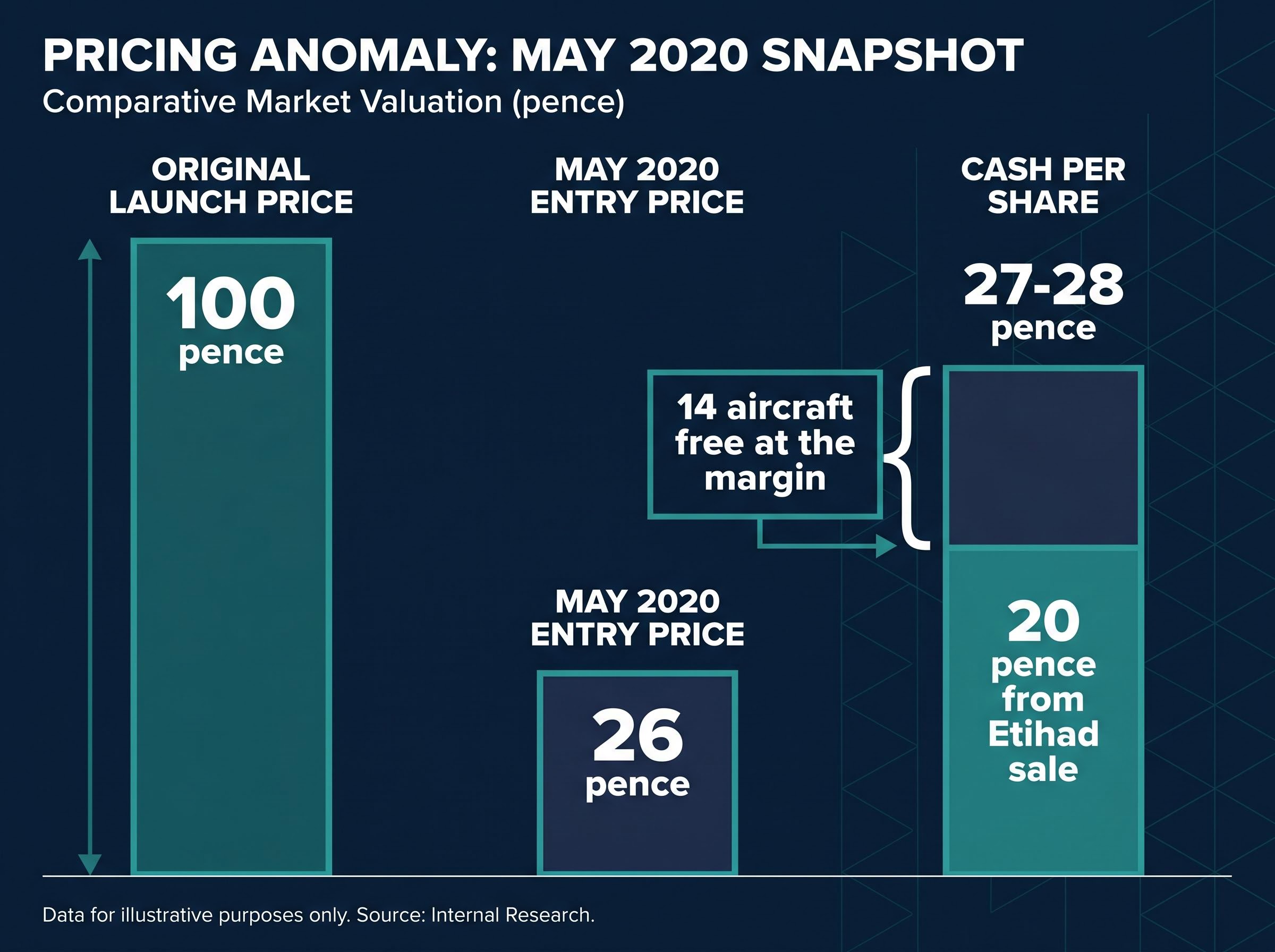

In May 2020, a fund manager bought shares in a COVID-crashed aircraft leasing company at approximately 26 pence per share. The company held roughly 27-28 pence in cash per share on its balance sheet. The aircraft were, at the margin, free.

This is the story of Amedeo Air Four Plus (AA4+), a UK-listed aircraft leasing fund whose pre-pandemic sale of two Airbus A380s to Etihad Airways left it holding more cash than its entire market capitalisation during the pandemic selloff. The position was held for approximately six years before a Qatari bank takeover closed at 73 pence per share, delivering a return of roughly 181% on price alone, before income and capital returns.

What follows uses the AA4+ case to unpack the core mechanics of deep value investing: how to identify setups where the downside is near zero, why structural sellers create mispricings that informed buyers can exploit, and how asset valuation works when standard methods fail. Each concept is anchored to a specific moment or number from the trade, so the framework is concrete rather than theoretical.

The arithmetic was striking. In February 2020, weeks before the pandemic shut down global aviation, AA4+ completed the sale of two A380 aircraft to Etihad Airways. The proceeds, combined with accumulated cash, left approximately $130 million on the balance sheet as the world locked down.

At the May 2020 entry price of roughly 26 pence per share, the cash per share stood at approximately 27-28 pence, comprising roughly 20 pence from the Etihad sale proceeds plus accumulated cash. The fund had originally launched at 100 pence per share. Now it traded at a quarter of that price, and the cash alone exceeded the market capitalisation.

The balance sheet arithmetic at the centre of the AA4+ thesis, comparing cash per share to the entry price, is a transferable skill that applies to any listed company, and investors who have not worked through the mechanics of reading a balance sheet systematically may find it useful to build that foundation before applying it to complex situations like aircraft leasing funds.

The implication was calculable, not speculative. Buying at 26 pence meant acquiring fourteen aircraft for less than nothing at the margin. The investment thesis required no view on aviation recovery, no opinion on airline survival, and no forecast for aircraft valuations. The cash cushion did the work.

Three conditions created the setup:

The core arithmetic: approximately 26 pence entry price versus approximately 27-28 pence cash per share. At that price, the buyer was paying less than cash value. Fourteen aircraft came free at the margin.

The position was sized at approximately 3-4% of fund assets, below the standard 5% position size, reflecting the perceived complexity of the holding. That sizing decision itself tells a story about how deep value positions are calibrated: the asymmetry was clear, but the path to realisation was not.

AA4+ existed because of a specific post-crisis need. After the 2008 global financial crisis, UK-listed aircraft leasing funds were designed as bond-like income vehicles for institutional portfolios. Each aircraft was financed with approximately 75% debt and 25% equity, and 12-year leases (roughly half an aircraft’s useful lifespan) provided a regular distribution to shareholders.

At launch, AA4+ offered an expected return of approximately 8-9% coupon equivalent, with principal returned to investors at wind-down. The dominant shareholders were UK institutional holders: multi-asset, endowment-style funds that owned the vehicle for its income characteristics, not for the underlying aircraft values.

This ownership structure became the trigger for the mispricing. When the pandemic forced a dividend suspension, the instrument no longer served its purpose in these portfolios. The income-oriented holders were not selling because they had identified something wrong with the aircraft or the leases. They were selling because a vehicle designed to deliver quarterly income had stopped delivering quarterly income. Their motivation was structural, not informational.

That distinction is the foundation of the deep value framework. When the seller’s reason for selling has nothing to do with the asset’s intrinsic value, the price signal they are sending is noise.

Income-oriented institutions were not applying fundamental valuation metrics to the aircraft portfolio when they sold; they were responding to the removal of a portfolio function, and that distinction separates informational selling from structural selling in any market.

| Dimension | Income investor view | Asset-value investor view |

|---|---|---|

| What they care about | Quarterly dividend yield and regularity of payment | Net asset value per share relative to market price |

| What triggered their sell decision | Dividend suspension removed the instrument’s portfolio function | Price falling below cash per share created asymmetric upside |

| What they were ignoring | Balance sheet cash, aircraft fleet value, lease contracts | Short-term income disruption and sentiment-driven selling |

Identifying the cash floor was straightforward. The harder analytical work was establishing a credible value for the aircraft themselves, because the two aircraft types in the fleet presented entirely different valuation problems.

The Boeing 777s in the portfolio could be valued using standard appraiser data. The type has a deep secondary market, active trading, and comprehensive coverage from multiple appraisal houses. A fund manager could source a valuation with a phone call.

The A380 was a different proposition entirely. Only approximately 200 A380s were ever built. Over 100 of those were operated by a single airline, Emirates. Thai Airways permanently retired its six A380s in 2020, with no plans for reactivation, illustrating the bifurcated nature of the secondary market. For Emirates-compatible airframes, demand existed. For everything else, it was limited.

The A380 secondary market was effectively two markets: airframes that suited Emirates’ configuration and operational requirements, which retained value, and retired frames from carriers like Thai Airways, which faced challenging disposition outcomes. Valuation required understanding which side of that divide each aircraft sat on.

This meant that valuing the A380s in AA4+’s portfolio required a separate analytical judgment about Emirates’ fleet strategy rather than simply consulting market data. Emirates confirmed plans to retain the A380 in service to at least 2040-2041, supported by an ongoing cabin retrofit programme, but the valuation still could not rely on a functioning marketplace.

The solution was to build a floor from the bottom up, using contractual minimums and conservative scrap estimates. The approach followed four steps:

This floor analysis was conservative by design, consistent with lender-friendly rather than owner-friendly appraiser assumptions. Most investors treat complex asset valuation as a reason to pass on an opportunity. In this case, breaking the asset into its contractual minimum and its scrap components established a credible floor, which is exactly the skill set that deep value situations demand.

By early 2021, the arithmetic case for AA4+ was visible to anyone who read the balance sheet. Vaccine rollout was underway. Broader aviation stocks were recovering. Yet AA4+ shares remained around 25-26 pence through the first half of 2021.

The price did not stay depressed because the market disagreed with the thesis. It stayed depressed because the market microstructure worked against price discovery.

Three specific factors extended the mispricing beyond the initial pandemic shock:

By 2021, approximately two-thirds of the share price was estimated to be covered by cash. The mispricing was widening even as the fundamental picture improved.

The clearing event came in July 2021, when a large block trade removed a major institutional seller from the share register. After that single transaction, the prolonged selling cycle ended and the price began to stabilise.

During the holding period, quarterly dividends of 2 pence per share were paid. Three additional capital returns via share redemptions also occurred, with approximately $100 million of the Etihad sale proceeds returned to shareholders by the end of 2021 (roughly $30 million retained). Identifying a mispricing and being able to exploit it at scale are two different problems; understanding the microstructure of how and when a mispricing clears is part of the analytical work.

The AA4+ position was not purely passive. The governance dimension was a deliberate part of the return-capture strategy, designed to ensure that when the moment for a strategic decision arrived, shareholder interests would be represented at the board level.

The approach avoided public campaigns. Instead, the focus was on board-level access and the appointment of a shareholder-aligned director. The fund maintained a productive working dialogue with the board chairman, a former senior partner at a UK aviation finance law firm, which provided the basis for constructive engagement.

In late 2023, Tom Sharp of Metage Capital joined the board as a shareholder representative, positioned ahead of an anticipated strategic review. The appointment was the product of sustained engagement rather than a hostile approach.

The strategic review commenced in late 2023 and attracted multiple bids, illustrating the competitive interest in the fund’s asset base. The process culminated in a recommended offer from LAC 10 LLC, a subsidiary of Lesha Bank, at 73 pence per share in cash, announced in March 2026. The offer implied an equity value of approximately $190 million.

The scheme document was published on 1 April 2026, and shareholder meetings were held on 27 April 2026. More than 98% of votes cast were in favour at both the Court Meeting and General Meeting. Completion is expected in Q3 2026, subject to court sanction and UAE merger control clearance.

The pre-bid stated NAV was 106.9 pence per share, meaning the offer represented a discount to NAV of more than 30%. That discount reflects the illiquidity and complexity premia inherent in winding down a bespoke aircraft leasing vehicle, but the 73 pence outcome still represented a near-threefold return from the 26 pence entry.

Key milestones from entry to exit:

The board engagement shows that deep value investing in closed-end funds is not purely passive. Influencing the governance conditions that allow a strategic review to happen is part of how the thesis is realised.

The AA4+ trade worked because three structural preconditions were present simultaneously. Remove any one of them, and the return profile changes materially.

The permanent capital point deserves emphasis. The holding period was approximately six years, from May 2020 to an expected completion in mid-2026. The position was held through projected lease expiries running into the mid-2030s without needing that scenario to materialise. Few fund structures can accommodate that patience.

Warning signs that would have invalidated the thesis:

The goal of deep value investing is not to find cheap assets. It is to find situations where the downside is bounded by something observable and the seller’s motivation is unrelated to the asset’s intrinsic value. The AA4+ case illustrates all three conditions operating together.

Readers wanting to see the same three structural preconditions applied in a radically different context will find our deep-dive into liquidation value investing in distorted markets, which traces how a Turkish logistics company purchased at roughly 2-3% of liquidation value delivered approximately 90 times the original capital in dollar terms despite the lira losing 90% of its value, with worked analysis of how hard-asset floors and structural seller dynamics operated in a hyper-inflationary environment.

The full arc of the investment started with an entry that required near-zero optimism about aviation. At approximately 26 pence in May 2020, the cash on the balance sheet covered the purchase price. The aircraft fleet was free at the margin. No bullish view on recovery was necessary.

What followed was six years of structural patience: holding through the income-investor exodus, engaging constructively with the board, waiting for the register to clear, and supporting the governance conditions that enabled a competitive strategic review. The exit came at 73 pence per share, with Lesha Bank acquiring the fund at an implied equity value of approximately $190 million.

Compounding over long horizons requires both the structural capacity to hold through sentiment-driven volatility and the behavioural discipline not to exit a thesis before the catalysts that realise it have had time to materialise, two conditions that the AA4+ holding period of approximately six years illustrates concretely.

The total return on price alone was approximately 181%, from 26 pence to 73 pence, before accounting for quarterly dividends and three capital return redemptions during the holding period.

The trade required no bullish view on aviation, no forecast of aircraft values, and no opinion on airline recovery. It required the arithmetic discipline to notice that cash per share exceeded the purchase price, and the structural patience to hold until the thesis was realised.

The edge was not a superior view on aircraft or airlines. It was the willingness to do the balance-sheet arithmetic when others were selling without doing it, and to hold a permanent-capital vehicle through the full duration of a thesis that took six years to play out. In deep value investing, patience and structural analysis are the durable advantages: not predicting recovery, but identifying situations where recovery is not required to win.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Deep value investing is a strategy that targets assets trading significantly below their intrinsic or liquidation value, typically because sellers are exiting for structural rather than informational reasons. The goal is to find situations where the downside is bounded by something observable, such as cash on a balance sheet, and where the seller's motivation has nothing to do with the asset's underlying worth.

When a stock trades below its cash per share, the market is effectively valuing the company's other assets at less than zero, meaning a buyer acquires those assets for free at the margin. In the Amedeo Air Four Plus case, shares were purchased at approximately 26 pence while cash per share stood at roughly 27-28 pence, making the entire fleet of fourteen aircraft free at the entry price.

A structural seller is one who exits a position for reasons unrelated to the asset's intrinsic value, such as an income-focused institution selling after a dividend suspension. Because their decision is driven by portfolio function rather than fundamental analysis, the price signal they generate is noise rather than information, creating mispricings that informed buyers can exploit.

When no active secondary market exists, such as for A380 aircraft during the pandemic, investors can build a floor value from the bottom up using contractual minimums in lease agreements and conservative parts-out estimates. In the AA4+ case, a contractual return payment of approximately $17 million per aircraft combined with a conservative $8 million parts-out estimate established a credible floor without relying on market pricing.

Permanent capital structures, such as listed closed-end investment companies, allow investors to hold a thesis through its full duration without being forced to sell due to redemption pressure. The AA4+ position required approximately six years from entry to exit, a holding period that would have been impossible for an open-ended fund facing investor redemptions at depressed prices.