A warehouse company purchased at roughly 3% of its liquidation value, held through a 90% currency collapse, returned approximately 90 times the original capital in dollar terms. The lira was not the obstacle. It was the distraction.

Turkey’s equity market has spent years generating some of the most extreme valuation anomalies visible in any liquid public market. Chronic currency instability, hyper-speculative local investor behaviour, and sustained foreign investor withdrawal combined to produce conditions most observers dismissed as uninvestable. A small number of fundamentals-oriented investors reached the opposite conclusion, and the returns they generated suggest their analytical framework deserves closer examination than Turkey’s macro headlines typically receive.

What follows is a dissection of the structural conditions that created those anomalies, the selection framework that separated genuine opportunity from value traps, and the specific mechanics of how one position compounded through currency collapse rather than despite it. The goal is a replicable analytical lens for identifying currency-insulated equity opportunities in distressed macro environments.

Why Turkey’s equity market became an anomaly factory

Turkish public company shareholders turn over the entire shareholder float approximately every 17 days. Roughly 4% of shares change hands daily. To put that figure in context, it implies a market where virtually every participant is oriented toward same-day or same-week profits rather than long-run ownership of businesses.

When an entire investor base is structured around that kind of activity, the price of a listed business reflects daily sentiment rather than underlying asset value. The consequences are visible in direct comparisons: comparable businesses in Turkey and India, beverage bottlers, airport operators, infrastructure owners, traded at a fraction of Indian multiples. The businesses were not inferior. The investor base demanded something entirely different from them.

Several structural characteristics reinforced this dynamic:

- Float turnover: Full shareholder base turnover approximately every 17 days, among the highest of any liquid public equity market

- Regulatory price caps: Daily price movement capped at 10%, creating artificial liquidity constraints during stress

- Speculative orientation: Local retail dominance with an overwhelming bias toward short-term momentum trading

- Foreign investor withdrawal: Institutional capital exited on macro grounds, removing the natural buyer base for fundamentally cheap assets

“The stock market is a device for transferring money from the active to the patient.”

That observation, attributed to Warren Buffett and referenced frequently by value investors operating in frontier markets, is not a platitude in Turkey. It is a precise description of the mechanism that kept asset-backed businesses trading at fractions of their worth for years.

The mechanism of retail sentiment diverging from fundamentals is not unique to frontier markets; it appears repeatedly in developed markets, where algorithmic momentum strategies maintain prevailing trends until physical supply disruptions force a quantitative recalibration, a dynamic that can sustain mispricings far longer than most investors expect.

When big ASX news breaks, our subscribers know first

The replication framework: what this approach requires from an investor

The opportunity Turkey presented was not random. It followed a structure that can be identified in advance, provided the investor applies the correct filter. Four conditions must be present simultaneously, and the difficulty of satisfying all four is precisely why the opportunity persisted.

| Criteria | Qualifies for Framework | Does Not Qualify |

|---|---|---|

| Market behaviour | Documented hyper-speculative turnover creating valuation disconnects | Efficient or institutionally dominated market with consensus-driven pricing |

| Revenue base | Foreign-currency revenues or hard-asset backing independently verifiable | Lira-denominated earnings with no inflation or FX hedge |

| Valuation anchor | Asset values assessable in dollar or euro terms, independent of local currency | Book value or earnings denominated in depreciating local currency |

| Holding capacity | Multi-year horizon with no requirement for short-term catalyst | Quarterly performance pressure or redemption-driven fund structure |

The selection filter against value traps is where most investors fail. A Turkish bank trading at a price-to-earnings ratio of 0.1 looks extraordinarily cheap on a spreadsheet. But bank assets are lira-denominated. The apparent cheapness may be illusory if the currency continues to depreciate and the asset base erodes in real terms. Lira-denominated earnings or book value do not qualify as a hard anchor under this framework.

Portfolio concentration risk compounds in distressed-currency environments because institutional mandates that restrict non-US or non-domestic exposure structurally exclude the markets where the most severe valuation anomalies appear; the same home bias that leaves most portfolios overweight a single AI capex cycle simultaneously guarantees that frontier and emerging market mispricings remain uncorrected for years.

Turkey’s broader investability continues to evolve. Foreign direct investment equity inflows reached $6.7 billion in 2024, up from $5.9 billion in 2023, according to the U.S. Department of State’s 2025 Investment Climate Statement. Inflation remained elevated at 32.37% as of April 2026. The macro challenge persists, which is precisely why the behavioural conditions that generate mispricing persist alongside it.

Turkey’s broader investability continues to evolve, with the U.S. Department of State 2025 Investment Climate Statement recording foreign direct investment equity inflows of $6.7 billion in 2024, up from $5.9 billion in 2023, against a backdrop of inflation remaining elevated at 32.37% as of April 2026.

The structural source of edge in these markets is the discipline of rejection: passing on thousands of apparently cheap opportunities and acting only on the handful where the asset backing is independently verifiable and the discount is severe.

Separating currency-insulated businesses from the rest

The lira moved from approximately 5 per dollar at the time of initial investment to approximately 45 per dollar seven years later. That is a roughly 90% nominal decline. Annual averages trace the progression: 32.83 in 2024, 39.49 in 2025, and approximately 45.89 as of late May 2026.

For most businesses listed on Borsa Istanbul, that depreciation is devastating. Revenue earned in lira buys less in real terms each year. Cost structures inflate. Margins compress. The macro story that caused foreign institutions to withdraw was, for these businesses, entirely correct.

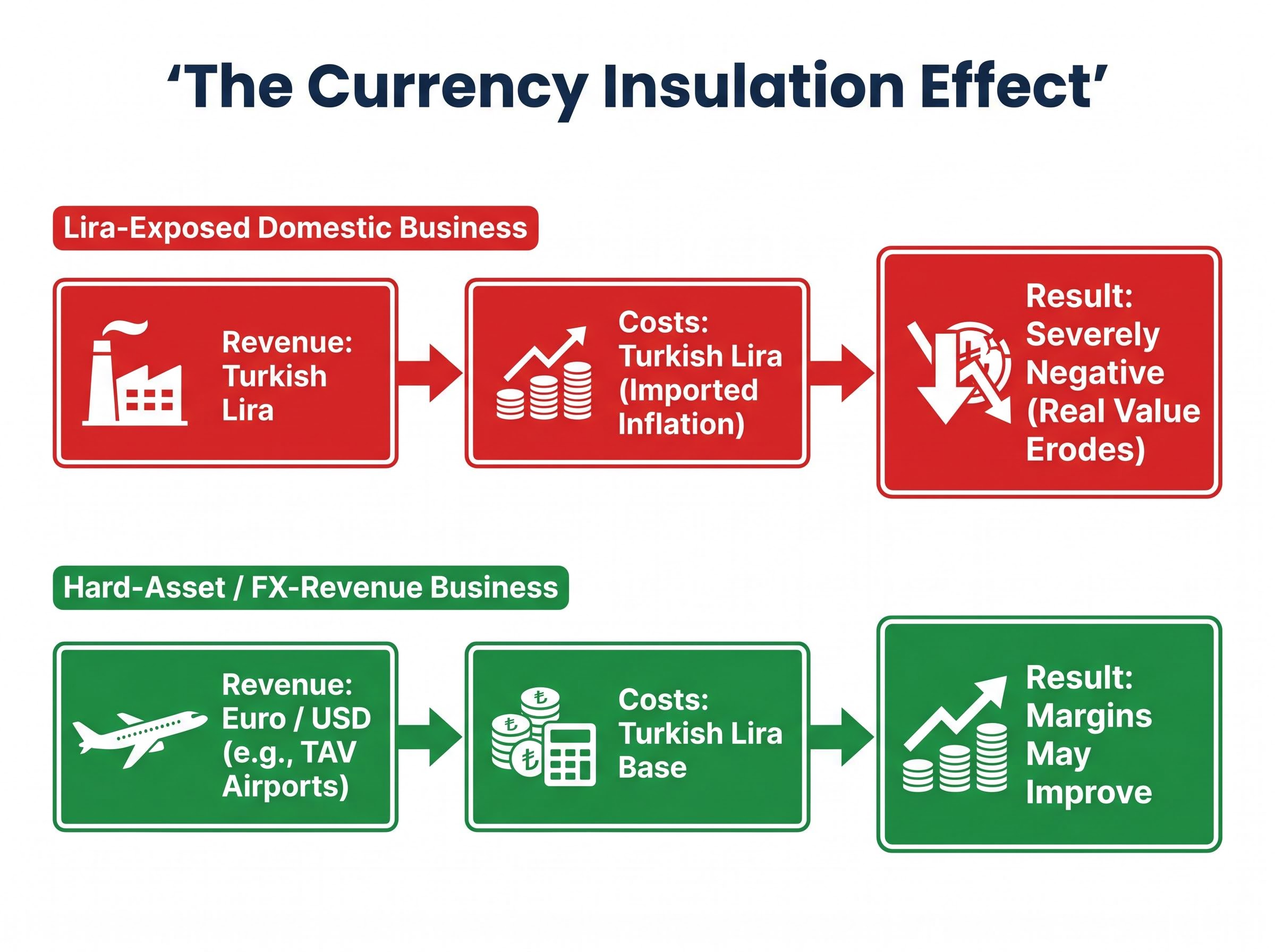

But the lira’s collapse is largely irrelevant for a specific subset of businesses: those backed by hard assets whose values track inflation or foreign currency benchmarks, or those earning revenue in euros or dollars while paying costs in lira. TAV Airports illustrates the structure clearly. Euro-denominated revenues from international passenger traffic paired with a lira cost base meant the currency’s decline actually improved margins rather than eroding them.

| Business Type | Revenue Currency | Cost Currency | FX Impact Assessment |

|---|---|---|---|

| Lira-exposed domestic business | Turkish lira | Turkish lira (with imported input inflation) | Severely negative; real value erodes with currency |

| Hard-asset or FX-revenue business | Euro / USD or inflation-linked hard assets | Turkish lira | Neutral to positive; lira depreciation may improve margins |

The investor’s problem was never the lira. It was the selection criteria applied before the lira became relevant. Get the asset-backing question right, and the currency takes care of itself.

How to value a business when the currency is on fire

In a market where inflation distorts earnings multiples and the local currency undermines book value, most conventional valuation tools produce noise rather than signal. Liquidation value analysis offers a way through.

Liquidation value, in this context, refers to the estimated proceeds from selling all underlying assets (real estate, warehouses, infrastructure) at distressed but real-world prices, net of liabilities, denominated in the currency of the assets themselves rather than the listed equity.

The logic for using liquidation value as the primary anchor in a hyper-speculative, currency-collapsing environment is straightforward. Earnings multiples are distorted by inflation. Book value can be lira-denominated and therefore depreciating in real terms. But hard asset values in real estate and infrastructure tend to track inflation or foreign currency benchmarks. They provide a floor that is denominated in something harder than the local currency.

Infrastructure asset valuation requires a separate analytical lens from earnings-based approaches precisely because regulated and contracted revenue streams create a hard floor beneath the equity that conventional multiples fail to capture, a structural parallel to the liquidation value anchor described here.

The calculation follows a clear sequence:

- Identify hard assets: Catalogue the company’s physical assets (real estate, warehouses, land, infrastructure) that have value independent of the local currency

- Estimate asset-level value in dollar or euro terms: Use comparable transaction data, replacement cost, or independent appraisals to establish what those assets would fetch in a hard currency

- Net liabilities: Subtract all debt and obligations to arrive at a net asset figure

- Compare to market capitalisation: Express the listed equity’s market cap as a percentage of the net liquidation value to identify the discount

Applying the framework to Reysas Logistics

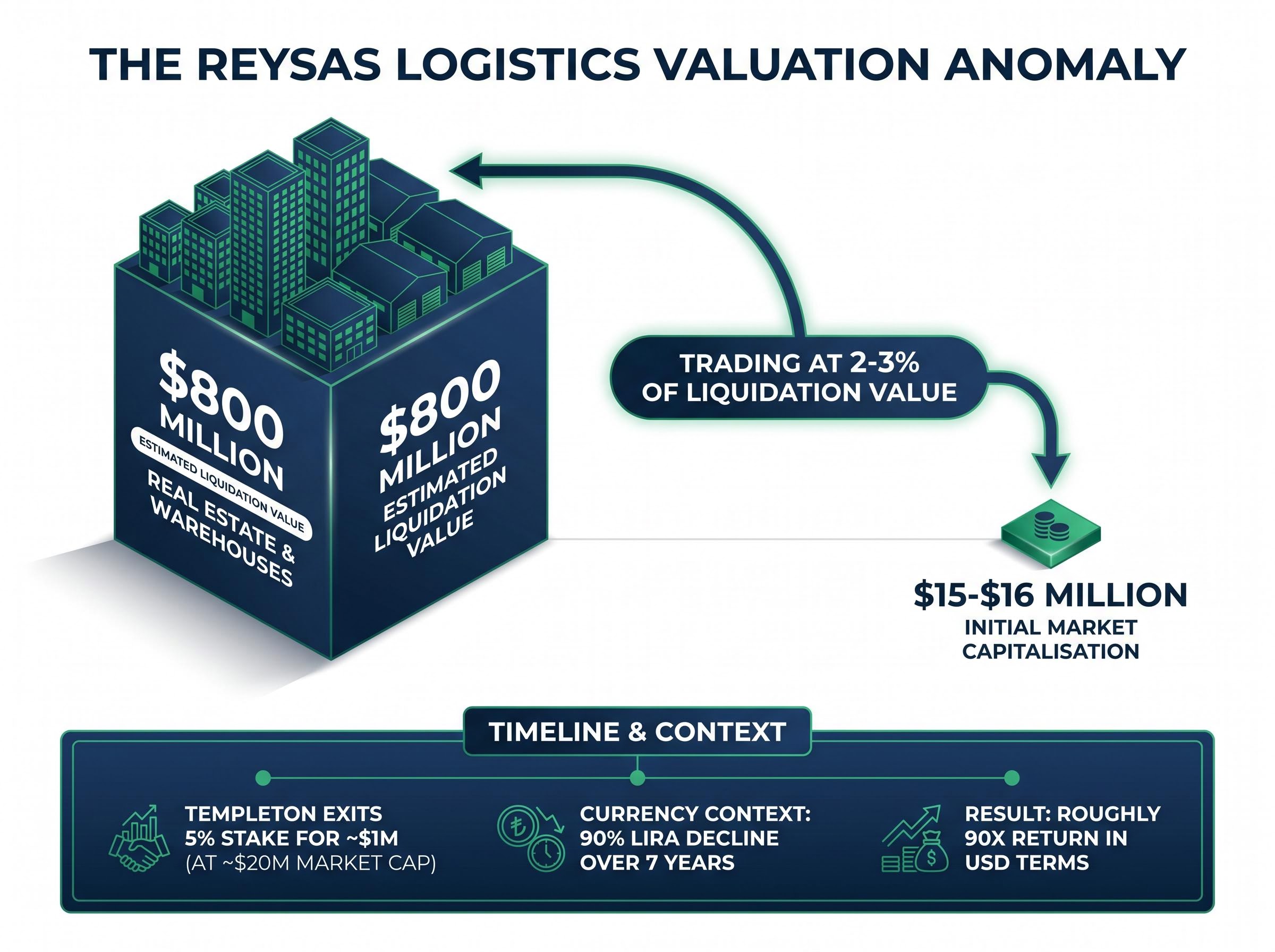

Reysas Logistics (RYSAS), a Turkish warehouse and logistics operator, illustrates the framework at its most extreme.

At the point of initial investment, the company’s market capitalisation stood at approximately $15-$16 million. The estimated liquidation value of its underlying real estate and warehouse assets was approximately $800 million. That implied the equity was trading at roughly 2-3% of the value that a buyer of the physical assets would need to pay.

The entry opportunity was sharpened by institutional selling. Templeton, the global fund manager, sold a 5% stake for approximately $1 million when the total market cap was roughly $20 million. The sale reflected institutional indifference to fundamentals in a market dominated by currency anxiety rather than asset-level analysis.

The liquidation value estimate was not a prediction that the company would be liquidated. It was a floor: the price below which the equity could not rationally trade indefinitely, because a buyer of the entire company could realise multiples of the purchase price simply by selling the assets.

How hard-asset backing translates into dollar-denominated returns

The return sequence is straightforward to state. Entry at approximately $15-$16 million market capitalisation. Current return approaching approximately 90 times the original capital, denominated in USD, despite the lira losing roughly 90% of its value over the holding period.

The mechanism is equally clear. Hard assets, warehouses, real estate, logistics infrastructure, appreciate in real terms or track foreign currency benchmarks. The lira decline was largely offset by asset value appreciation in those terms. The extreme initial discount (buying at 2-3% of liquidation value) provided a margin of safety large enough to absorb any residual currency erosion and still deliver extraordinary compounding.

The conditions required to hold

The return arithmetic is clean. The conditions required to earn it were not. The investor held through circumstances that would cause most institutional capital to exit:

- No analyst coverage: Zero institutional research coverage for most of the holding period

- Institutional selling at the wrong time: Templeton exited a 5% stake for approximately $1 million, removing the most sophisticated capital from the register

- Seven-year holding horizon: No observable catalyst for most of the period; the thesis was structural, not event-driven

- Daily sentiment volatility: In a market turning over its float every 17 days, the share price reflected noise rather than value on any given week

- Regulatory price caps creating illiquidity: The 10% daily movement cap meant that in periods of stress, sellers could not exit and buyers could not enter at scale

The market’s hyperactivity was the feature, not the bug. It kept other long-term buyers away throughout the compounding period, preserving the discount for anyone willing to sit still while the float churned around them.

Why temperament, not prediction, determines long-run investment outcomes

The 90x return was not a product of macroeconomic forecasting. The investor did not predict the lira’s trajectory, Turkey’s political conditions, or the Central Bank of the Republic of Türkiye’s (CBRT) rate decisions (the policy rate was raised to 46% in April 2025 and subsequently cut to 37% by January 2026). The return was a product of structural analysis applied once and held without interference.

The 17-day float turnover is not merely a behavioural curiosity. It is the mechanism that kept the price disconnected from value for long enough to generate the return. The same hyperactivity that creates the mispricing prevents its correction, because the capital required to close the gap (patient, long-duration, fundamentals-oriented) is precisely the capital that the market’s conditions repel. For context, Berkshire Hathaway shareholders might take a decade to fully turn over the register. The structural gap in holding periods is the structural gap in returns.

Research suggests fewer than 1% of active stock pickers demonstrate genuine skill. The wealth transfer runs consistently from hyperactive to patient participants. Distressed-currency markets with liquid public equities and hard-asset businesses will continue to produce these situations, because the conditions that create them, speculation, currency instability, foreign investor withdrawal, are self-reinforcing and unlikely to be arbitraged away quickly.

The 90x return is not a lesson about Turkey. It is a lesson about what happens when structural analysis meets structural patience in any market that rewards neither.

Analytical framework first, macro narrative never

The investor did not predict the lira’s path, Turkey’s political trajectory, or the macro outcome. The return came from a single structural insight, that hard-asset-backed businesses in hyper-speculative markets can trade at fractions of their worth, applied with discipline across a seven-year horizon.

The transferable action is direct: identify liquid public markets with documented speculative behaviour, screen for businesses with hard-asset or foreign-currency revenue backing, and apply liquidation-value analysis as the primary valuation anchor rather than earnings multiples or book value. The conditions that produced this opportunity, currency instability, speculative local markets, institutional withdrawal on macro grounds, are present in multiple frontier and emerging markets simultaneously. The bottleneck is analytical framework and holding discipline, not information.

Geopolitical fragmentation accelerates the conditions this framework targets: as industrial policy diverges across regional blocs, capital controls tighten, and institutional investors withdraw from politically complex markets on macro grounds, the repricing gap between fundamental asset value and listed equity widens in precisely the jurisdictions most global allocators are reducing exposure to.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.