How to Research Small Cap Stocks Before the Crowd Does

8 hrs ago

The hardest investment decision you will make is not what to buy. It is whether to hold when the market is loudly, persistently, and often convincingly telling you that you are wrong. In small-cap investing, where thin liquidity and sentiment-driven pricing can move a stock 70% against you while the underlying business remains entirely intact, that decision is not theoretical. It is the difference between capturing a multi-year return and locking in a permanent loss.

Consider the stakes. Mineral Resources fell from approximately $70 to $15 before recovering toward the $60-$70 range. HMC Capital dropped from above $10 to $2.50, below its estimated net tangible assets. These are not marginal pullbacks. They are the kind of drawdowns that force a genuine psychological reckoning, one where instinct and analysis pull in opposite directions.

This piece gives you a specific, repeatable framework for telling the difference between a thesis that has broken and one that is simply uncomfortable. You will walk away with the analytical tools to build conviction before you buy, the psychological architecture to maintain it under pressure, and a decision tree for knowing when to hold, when to add, and when to walk away.

Every time you buy a stock, you are making a statement: the market has this wrong. That disagreement is the entire basis of the position. And it will be tested, sometimes severely, before the market comes around to your view. The question is whether you have built the structure to survive the interval.

The distinction that matters most is between the market revising its sentiment and the underlying business actually changing direction. The first is noise. The second is a thesis event. The investor who cannot tell them apart will always capitulate at the worst moment, because maximum sentiment divergence and maximum opportunity tend to arrive at exactly the same time.

ASX small cap volatility is most often a product of thin order books and illiquidity rather than a genuine signal that a business has deteriorated, a distinction that professional managers at Fairlight, Spheria, and Wilson Asset Management each documented when their portfolios fell 30% or more in 2024 on no change to underlying company quality.

Pro Medicus illustrates this precisely. The model fair value sat at approximately $310 per share. The stock declined to around $120 at a point of dislocation. The directional thesis, that PME’s enterprise medical imaging contracts would continue to expand, remained intact throughout. The model did not fail. The market simply disagreed with it for a period, and that disagreement was the opportunity.

Conviction is holding because verified evidence has not changed. Stubbornness is holding because of ego or sunk-cost psychology. The difference is the quality of the work done before the position was opened.

If you define being “right” as the price matching your model on any given day, you will sell exactly when you should hold. Maximum divergence between your estimate and the market’s price is precisely when your edge, if it exists, is largest.

The ability to hold through a severe drawdown is not psychological willpower alone. It is structural preparation, done before the position is opened, that transforms a price decline from a crisis into a checklist.

The first discipline is identifying the one to three variables that actually drive a stock’s value and price. Not twenty metrics monitored equally. Not a full discounted cash flow model that gives false precision. The one to three things that, if they change, change everything.

XRF Scientific is the clearest example. The single dominant variable identified was sample processing volumes in its highest-margin division. When that variable trends upward, the directional thesis is intact, regardless of noise elsewhere. When you can name your variable that specifically, a 40% drawdown becomes a tractable question rather than an overwhelming one.

For REITs, the primary variable is often even simpler: interest rate direction. Research has shown that rate direction frequently overrides all other valuation considerations in the REIT space, making it the one variable worth monitoring above everything else.

Before you buy, write down three things: the one to three variables you are monitoring, the specific conditions that would trigger a reassessment (your kill-switches), and your directional call on the business. Keep this document short, specific, and honest.

The pre-buy thesis discipline described here, identifying key variables, setting kill-switch conditions, and assessing directional correctness, sits within a broader share selection process that covers how to evaluate business quality, read key financial metrics from ASX filings, and size positions to protect against a single bad outcome.

This is the document you return to during a drawdown. Not the stock chart. Not the broker commentary. Not the social media discourse. Your pre-written thesis is the only thing that separates a disciplined reassessment from a panic reaction.

The principles above are not abstract. Three ASX case studies demonstrate how they operate in practice, each doing a different piece of work.

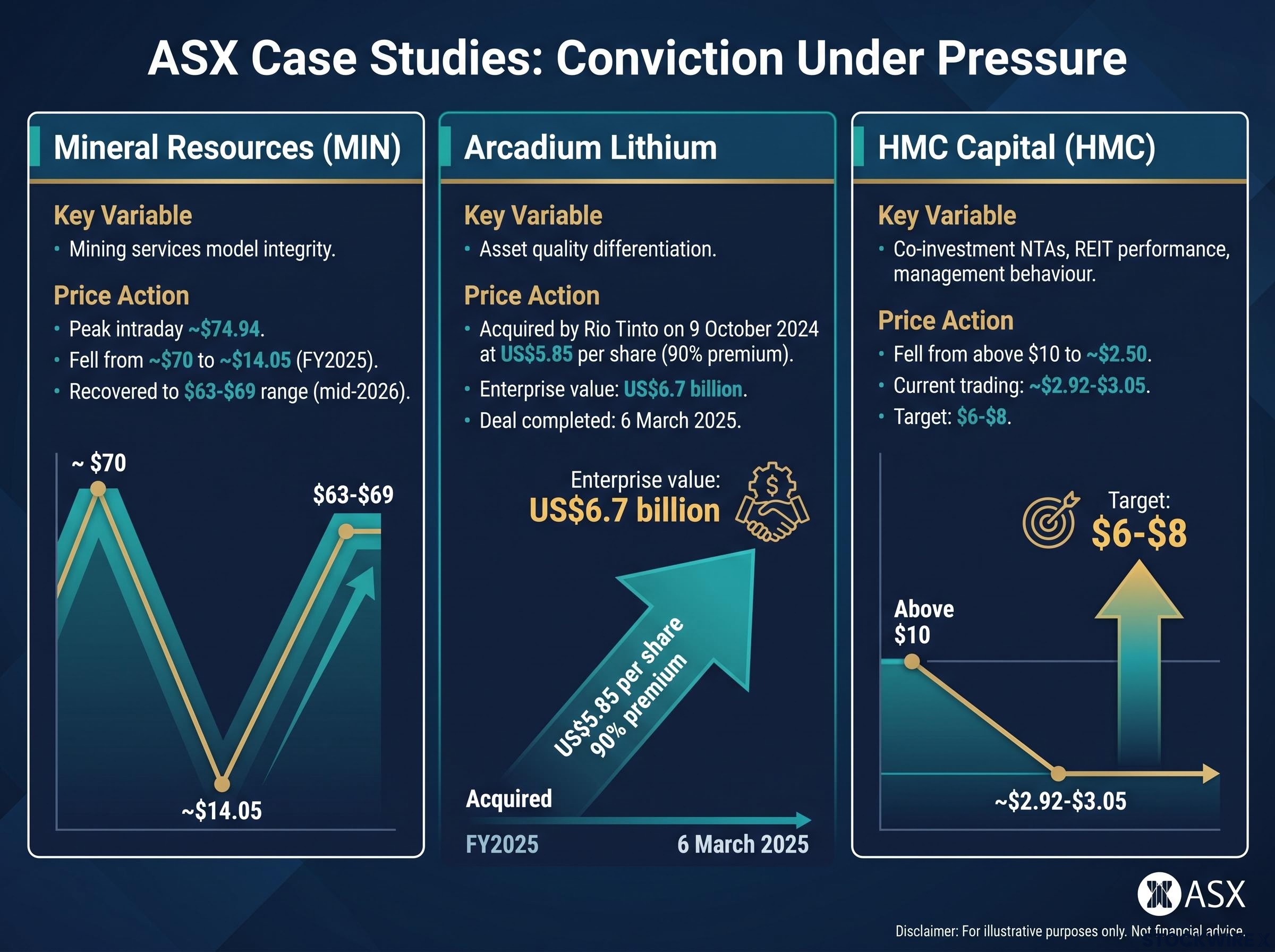

Mineral Resources declined from approximately $70 (peak intraday levels reached approximately $74.94) to a closing low of around $14.05 during FY2025, before recovering to trade in the $63-$69 range through mid-2026. The stock faced a convergence of damaging headlines: significant debt load, allegations of executive misconduct, commodity price weakness, and operational difficulties with the Onslow haulage road. At the depth of the selloff, bearish sentiment was at its most intense. For holders of the thesis, however, the operative question was not whether the headlines were damaging but whether the integrated mining services model had structurally deteriorated. It had not. Investors who anchored their assessment to that specific variable, rather than to the volume of negative coverage, retained their position and participated in the subsequent recovery.

Arcadium Lithium tested a different kind of conviction. As lithium sentiment soured, the market priced all lithium producers as an interchangeable group, making no distinction based on asset quality. The thesis held that brine-based extraction operations carried meaningful advantages over hard rock equivalents, a structural gap the market had declined to value. That view was validated decisively on 9 October 2024, when Rio Tinto announced an all-cash acquisition of Arcadium at US$5.85 per share, a 90% premium to the pre-announcement price, with an enterprise value of approximately US$6.7 billion. The deal completed on 6 March 2025. The bid effectively placed a dollar figure on the exact quality distinction the thesis had argued. The discomfort of holding a non-consensus position prior to that moment was not incidental; it was the mechanism by which the mispricing existed.

HMC Capital represents a live conviction thesis. After falling from above $10 to a low of approximately $2.50, the stock traded below the assessed value of its underlying co-investments and net tangible assets, including its holdings in listed REITs. The entry was made on that basis, with a medium-term target of $6-$8. Three monitoring questions remain active: whether the co-investment valuations and NTAs continue to hold up, whether the underlying REITs are delivering operationally, and whether management’s capital allocation behaviour remains consistent with the original thesis.

| Company | Drawdown | Thesis type | Key variable monitored | Outcome / current status |

|---|---|---|---|---|

| MIN | ~$70 to ~$14.05 | Integrated mining services + commodity optionality | Mining services model integrity | Recovery to $63-$69 range |

| Arcadium Lithium | Pre-announcement discount to quality | Brine vs. hard rock quality gap | Asset quality differentiation | Acquired by Rio Tinto at 90% premium |

| HMC | ~$10+ to ~$2.50 | Platform value below NTA | Co-investment NTAs, REIT performance, management behaviour | Live thesis; trading ~$2.92-$3.05 |

The common factor across all three is not confidence that the stock would recover. It is a pre-established framework that told the investor what evidence would change their mind, which meant they could hold without drifting into hope.

Most investors treat research as a depletable effort spent on one stock. Professionals treat it as a compounding asset, one that produces multiple expressions of the same thesis with different risk profiles.

When deep sector research surfaces an investment idea, it almost always surfaces related instruments at the same time: royalties, REITs, platform vehicles, and related operators. The question is not just “should I buy this stock?” but “which instrument best expresses this thesis at the level of risk I want?”

The Mineral Resources research illustrates this directly. Work conducted on MIN surfaced Red Hill Minerals as a party holding a royalty over the same underlying project. Where MIN’s position carried meaningful debt and balance sheet exposure, the royalty holder simply receives a share of revenue, insulated from the leverage risks that weighed on the operator. The thesis was effectively the same; the risk profile was materially different.

A royalty holder participates in a project’s revenue stream without carrying the operator’s balance sheet obligations, capturing project upside while sidestepping the leverage that amplifies drawdowns.

The HMC ecosystem offers an even richer set of options. The platform value thesis can be expressed via HMC Capital itself, via HomeCo Daily Needs REIT (HDN), via HealthCo Healthcare and Wellness REIT (HCW), or via DigiCo Infrastructure REIT (DGT), which came to market in December 2024 at an issue price of approximately $5.00 and had since fallen to trade at around $2.40, a deep discount to both its float price and book value.

When a position is underwater and creating psychological pressure, asking “is there a better instrument to express this thesis at current prices?” is a legitimate alternative to either holding the original position or exiting entirely. This question converts thesis-building from a single-stock decision into a portfolio-level skill.

The analytical work covered above is necessary but not sufficient. You also need a psychological architecture that allows you to operate the framework under pressure, because the pressure is precisely when most investors abandon their process.

“I only change my view when confronted with specific new facts that contradict my thesis, not when the number of people who disagree with me increases.”

Media coverage, analyst downgrades, and increased short interest are sentiment signals, not evidence signals. Your task during external pressure is to distinguish new facts from amplified sentiment. Only new facts that contradict a foundational assumption constitute grounds for reassessment.

Sell-decision biases including the disposition effect, recency bias, and herd behaviour cluster precisely at the moment when a drawdown is deepest and the pressure to act is strongest; research from the University of Chicago found that randomly selected exits outperformed professional managers by up to 150 basis points annually, identifying the exit decision as the primary site of portfolio value destruction.

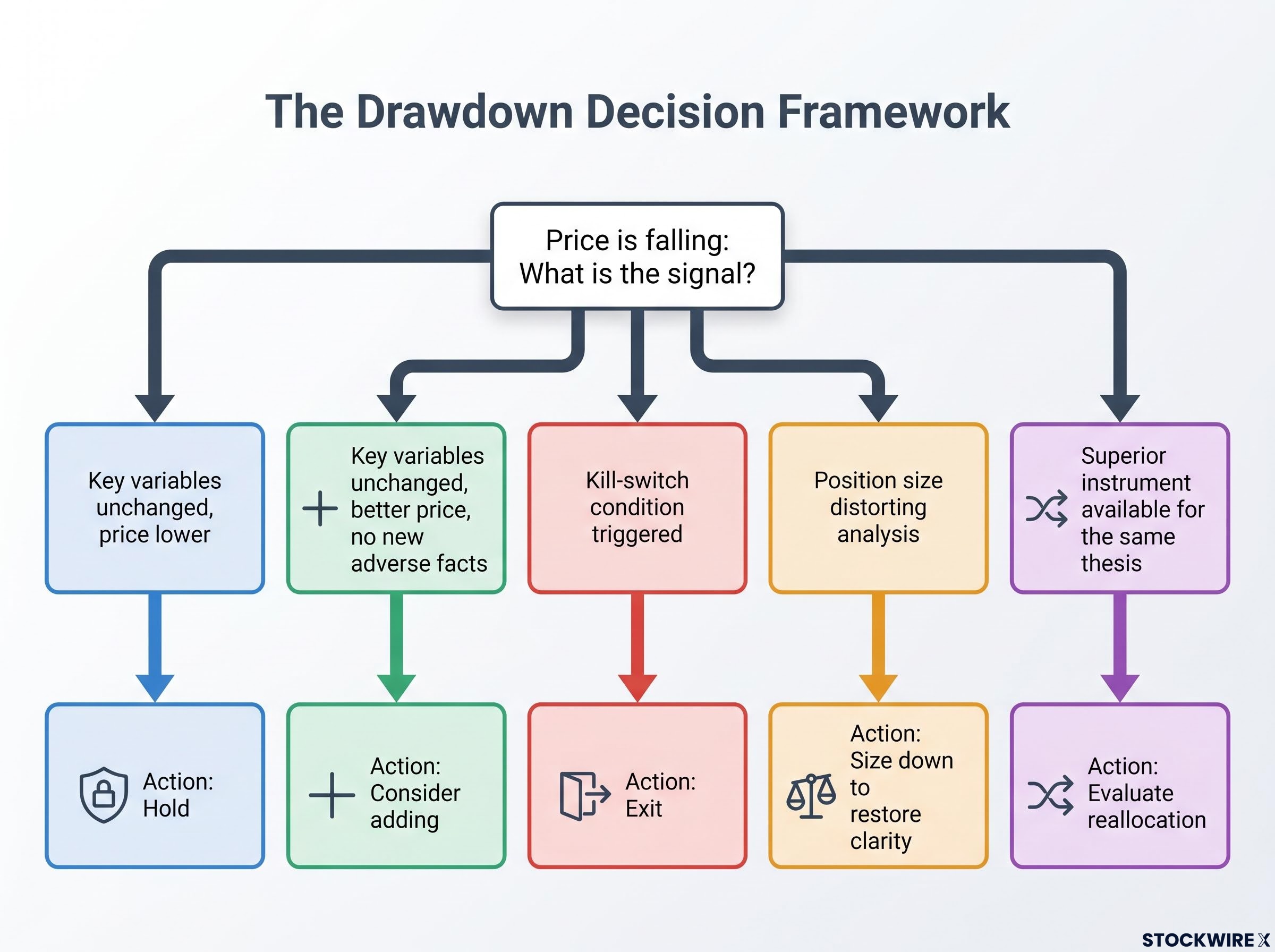

The framework above converges on a single practical question: what do you actually do when the price is falling? The answer is not “stay disciplined.” The answer is a specific decision tree.

When to hold: Your key variables are unchanged. The headline noise is sentiment, not evidence. Your directional call on the business remains intact. The price has moved against you, but nothing in your pre-written thesis has been falsified.

When to consider adding: The same thesis applies, the price is lower, no new adverse facts have emerged, and the risk-reward has improved within thesis bounds. Adding is not averaging down blindly. It is a deliberate assessment that the thesis is intact and the entry point is better.

When to exit: A foundational assumption has been clearly broken. One of your pre-identified kill-switch conditions has triggered. Or a superior, lower-risk expression of the same thesis now exists and reallocation is preferable. Or the opportunity cost of holding has materially shifted because a clearly better risk-reward exists elsewhere.

New analyst downgrades, increased short interest, and media coverage are not by themselves evidence of a broken thesis. They are sentiment amplifiers. The question is always whether they contain specific new information that contradicts a foundational assumption.

The cost of exiting too early is not abstract: a $100,000 investment held continuously in the S&P 500 for a decade grew to approximately $272,000, but missing just 10 trading days reduced the ending balance to $153,000, with seven of those 10 best days occurring within two weeks of the 10 worst, making it structurally impossible to avoid the drawdown without also missing the recovery.

| Signal type | Recommended action |

|---|---|

| Key variables unchanged, price lower | Hold |

| Key variables unchanged, better price, no new adverse facts | Consider adding |

| Kill-switch condition triggered | Exit |

| Position size distorting analysis | Size down to restore clarity |

| Superior instrument available for the same thesis | Evaluate reallocation |

The question is never “has the stock fallen enough to worry?” It is “has a specific pre-identified condition been met?” If the answer is no, your framework says hold. You now have a structure to stand behind rather than a feeling to fight.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Conviction investing rests on two interlocking disciplines, and neither works without the other. The first is the analytical work done before you buy: identifying your key variables, writing your thesis with explicit kill-switches, and mapping the instruments that express the same thesis at different risk levels. The second is the psychological architecture maintained during the drawdown: the infinite game reframe, the Man in the Arena decision rule, the low-correlation diagnostic, and the position sizing kill-switch.

Senica Financial Solutions, which has recorded approximately 20% annualised returns since inception, treats these not as instinctive responses or personal character traits but as documented, repeatable processes that are applied consistently regardless of market conditions.

Here is what that process looks like as a checklist you can apply starting today:

In any portfolio, the positions that will test your conviction most severely are probably already held. The framework in this article is not preparation for the next buy. It is applicable right now.

—

Investing with conviction means holding a position through severe price declines because your pre-identified key variables and kill-switch conditions have not been triggered, not because you feel confident or because the stock has fallen far enough. Conviction is grounded in verified evidence, not ego or sunk-cost psychology.

The distinction comes down to whether a specific, pre-identified kill-switch condition has been met. If your one to three key variables are unchanged and no foundational assumption has been falsified, the drawdown is sentiment-driven noise, not evidence that the thesis has failed.

Kill-switch conditions are the specific events or data points you name before opening a position that would prove a foundational assumption wrong. Writing them down before you buy is what separates a disciplined reassessment during a drawdown from a panic reaction driven by price movement alone.

Adding is appropriate when the same thesis applies, no new adverse facts have emerged, and the lower price improves the risk-reward within thesis bounds. Exiting is appropriate when a kill-switch condition has triggered, a foundational assumption has clearly broken, or a superior lower-risk instrument now exists to express the same thesis.

Arcadium Lithium was acquired by Rio Tinto on 9 October 2024 at US$5.85 per share, a 90% premium to the pre-announcement price, with an enterprise value of approximately US$6.7 billion, directly confirming the thesis that brine-based extraction assets were structurally superior to hard rock equivalents and had been mispriced by a market treating all lithium producers as interchangeable.