What UK Traders Lose When Their CFD Account Goes Offshore

13 hrs ago

Most Australian investors think they are diversified. They own a handful of ASX stocks, maybe an index fund, and the portfolio spans banks, miners, a supermarket or two. It feels broad. It is not. The ASX is one of the most concentrated major indices in the developed world, with financials and materials commanding a disproportionate share of total index weight.

That concentration matters more than most investors realise. The ASX represents roughly 2% of global equity market capitalisation. An Australia-only portfolio leaves the other 98% of the world’s investable companies off the table, including entire sectors like semiconductors, cloud computing, global pharma, and artificial intelligence infrastructure that barely register on the local index.

This guide walks through a specific three-ETF structure designed to solve that problem. You will get the rationale behind each fund selection, how the 40/30/30 allocation weights work together, the practical steps to implement the portfolio on the ASX today, and how to adjust the framework for your own risk tolerance and time horizon.

Start with a number: the ASX accounts for approximately 2% of global equity market capitalisation. That means defaulting to Australian equities, even through a well-constructed local index fund, means you are choosing to ignore 98% of the world’s investable market.

That choice has consequences. The ASX is structurally overweight to financials and materials relative to a global developed market benchmark. Those two sectors carry a disproportionate share of the index, which means a locally focused portfolio rises and falls with bank earnings, commodity cycles, and a narrow set of domestic large-caps.

Compare that with the sectors the ASX barely touches:

You can own twenty different ASX stocks and still have almost no exposure to these areas. That is not diversification in any meaningful global sense. It is familiarity masquerading as breadth.

The practical cost is real. If the next decade’s equity returns are driven by AI infrastructure buildout, global healthcare innovation, or digital platform expansion, an ASX-only portfolio misses most of the upside. Home bias feels like safety because you recognise the names. But recognition is not protection.

The home bias return gap between the ASX and global benchmarks is not a theoretical concern: over the decade to June 2025, the ASX delivered 11.1% annualised versus 15.5% for the S&P 500, and Morningstar data confirms that franking credits alone do not close the difference for growth-oriented investors.

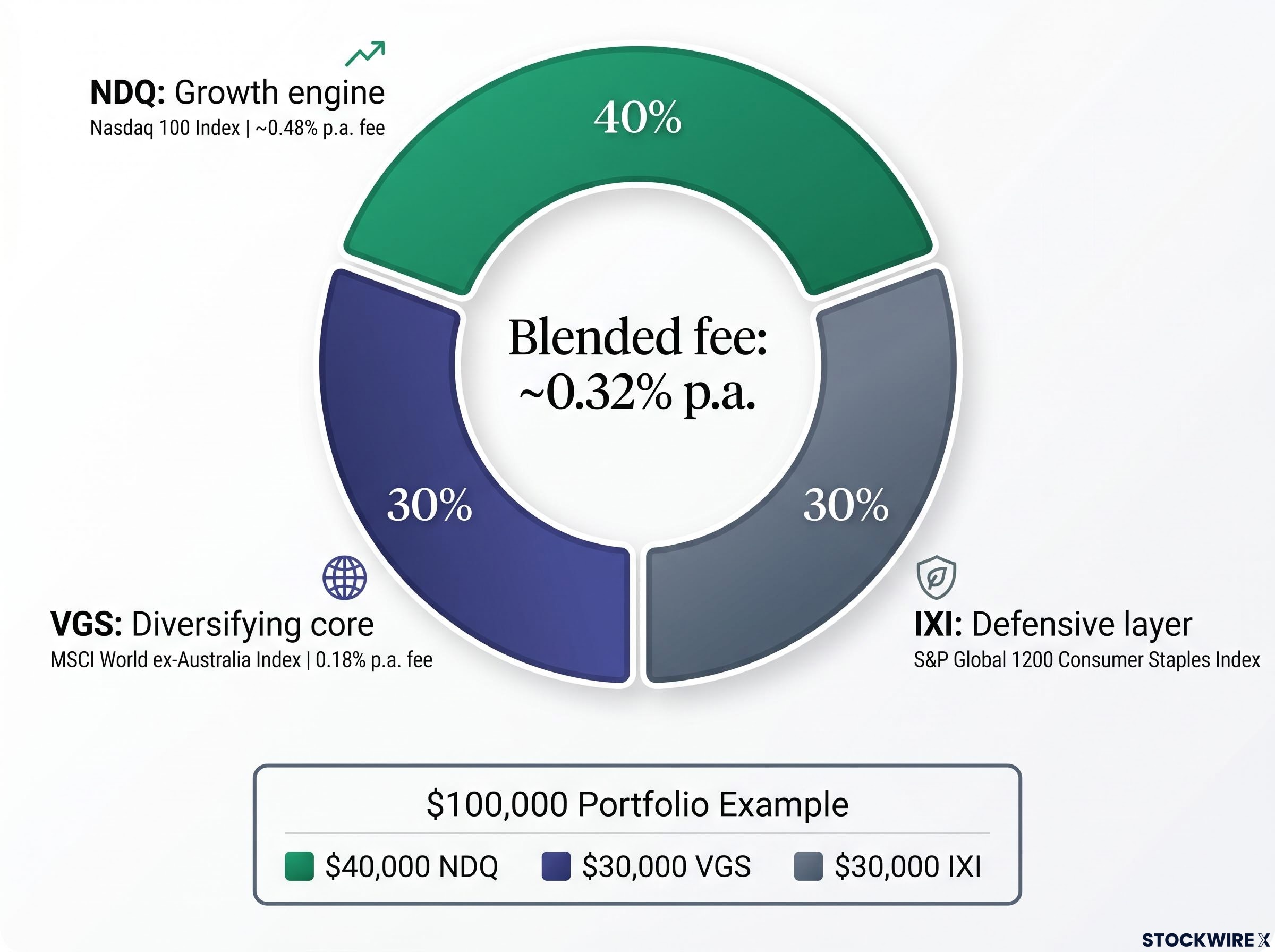

The portfolio allocates 40% to NDQ, 30% to VGS, and 30% to IXI. Each weight reflects a specific role, and the three funds were chosen because of how they complement each other, not because any single one is the “best” ETF on the ASX.

For a $100,000 portfolio, that translates to $40,000 in NDQ, $30,000 in VGS, and $30,000 in IXI.

| ETF Code | Role | Index Tracked | Management Fee (indicative) |

|---|---|---|---|

| NDQ | Growth engine | Nasdaq 100 Index | ~0.48% p.a. |

| VGS | Diversifying core | MSCI World ex-Australia Index | 0.18% p.a. |

| IXI | Defensive layer | S&P Global 1200 Consumer Staples Sector Capped Index | Verify via current PDS |

Fees are indicative and should be verified against each fund’s current Product Disclosure Statement (PDS) before investing.

ASIC’s regulatory guide on exchange traded products outlines the disclosure obligations ETF issuers must meet, which is why each fund’s Product Disclosure Statement contains the standardised fee, risk, and benchmark information you need to verify before committing capital.

NDQ tracks the Nasdaq 100 Index. Its role in the portfolio is to provide concentrated exposure to large US non-financial companies, dominated by technology, communication services, and consumer platforms.

The trade-off is volatility. NDQ carries more short-term price swings than a broad global index fund, and is especially sensitive to shifts in interest rate expectations and technology sector sentiment.

VGS tracks the MSCI World ex-Australia Index. It holds thousands of companies across developed markets outside Australia, including the United States, Europe, Japan, Canada, and a range of other significant economies.

At 30%, VGS ensures the portfolio is not solely reliant on one country, one sector, or one growth narrative.

IXI tracks the S&P Global 1200 Consumer Staples Sector Capped Index. Consumer staples covers the products households reach for consistently: think packaged food, beverages, personal care goods, and cleaning supplies.

The trade-off here is slower growth. Consumer staples companies typically do not deliver the same upside as technology or innovation-led businesses. You are trading some return potential for a smoother ride.

The allocation weightings are not arbitrary. The 40% tilt to NDQ reflects a deliberate growth bias. The 30% to VGS reflects a commitment to geographic breadth. The 30% to IXI reflects a willingness to trade some upside for reduced drawdown severity. Understanding why each weight exists is what allows you to adjust them confidently for your own circumstances.

Understanding each fund individually is one thing. Understanding what happens when conditions get difficult is where the portfolio’s design earns its value.

The three funds create internal balancing mechanisms:

Honesty matters here. All three are equity funds. In a broad global selloff, all three will fall. IXI’s defensiveness is relative, not absolute. It historically drops less than growth-oriented funds in risk-off episodes, but it still drops.

Knowing this in advance is the point. When your next correction arrives and IXI also declines, you will understand that the decline is smaller than it would have been without the defensive layer, rather than panicking because “even the safe one is down.”

Currency exposure note: All three ETFs are unhedged, meaning AUD movements affect your returns in both directions. A weaker Australian dollar helps your returns (your foreign holdings are worth more in AUD terms). A stronger Australian dollar hurts. This is an ongoing feature of the portfolio, not a one-off risk.

You understand the logic. Here is what you would actually do.

Rebalancing trigger: If NDQ drifts above 45% or below 35% of your portfolio, rebalance. Same logic applies if VGS or IXI drifts more than 5 percentage points from their 30% target. This keeps the portfolio’s risk profile intact without generating excessive trading costs.

The rebalancing rule is not just a portfolio mechanics exercise. It is a behavioural discipline. Without it, you naturally end up overweight in whichever asset has recently performed best, which is exactly the mechanism behind most retail investor underperformance. A simple rule prevents you from accidentally doubling down at the peak.

The 40/30/30 allocation is a starting point, not a fixed rule. You can adjust it, but each adjustment comes with a trade-off.

A currency-hedged global ETF could substitute for VGS if you are concerned about AUD movements, though hedging changes the fund’s risk and return profile and is worth researching separately.

The choice between hedged versus unhedged ETFs is not purely theoretical: over the year to May 2026, HNDQ returned 40.2% while unhedged NDQ returned 27.2%, a 13 percentage point gap produced entirely by AUD/USD appreciation rather than any difference in the underlying Nasdaq 100 holdings.

Every adjustment is a trade-off, not a free upgrade. Increasing NDQ raises growth potential and increases drawdown severity. Adding Australian equities opens up franking credits but risks drifting back toward exactly the concentration problem you are trying to solve.

A high-equity, growth-tilted portfolio suits a multi-decade investment horizon. If you are within five years of needing the money, a pure equity allocation carries more short-term risk than most investors are comfortable with.

At that point, introducing bonds or cash into the mix would be prudent. That moves beyond the scope of this three-ETF framework and is worth discussing with a licensed financial adviser.

The portfolio’s structural advantages are genuine:

The limitations are equally real:

Each fund’s PDS should be read in full before investing. This framework gives you a clear starting structure and the logic behind it, but your personal situation may warrant a different allocation or additional asset classes.

For investors wanting to audit whether their VGS and NDQ holdings create unintended concentration in individual mega-cap names, our full explainer on ETF overlap walks through exactly how to identify shared positions across both funds using free tools in a single afternoon.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

If you want a portfolio reviewed against your specific circumstances, a licensed financial adviser is the logical next step.

—

The 40/30/30 ASX ETF portfolio is a three-fund structure allocating 40% to NDQ (Nasdaq 100 growth exposure), 30% to VGS (broad developed-market diversification), and 30% to IXI (global consumer staples as a defensive layer), designed to give Australian investors access to the 98% of global equity markets the ASX does not cover.

Financials and materials dominate the ASX by index weight, and the entire exchange represents only about 2% of global equity market capitalisation, meaning a locally focused portfolio has almost no exposure to semiconductors, cloud computing, global pharmaceuticals, or AI infrastructure.

Check allocations once or twice per year and act if any ETF has drifted more than 5 percentage points from its target weight; where possible, use new cash contributions to top up underweight positions rather than selling existing holdings, since selling crystallises capital gains while topping up does not.

Unhedged ETFs move with AUD exchange rate fluctuations, so a weaker Australian dollar boosts your returns while a stronger dollar reduces them; over the year to May 2026, the hedged HNDQ returned 40.2% versus 27.2% for unhedged NDQ, with the entire 13 percentage point gap produced by AUD appreciation rather than any difference in underlying holdings.

IXI tracks global consumer staples companies whose earnings are driven by non-discretionary household spending, so the fund historically declines less than growth-oriented equity funds during risk-off episodes, providing a partial offset when technology stocks sell off sharply.