ASX Shorts Build Into Cochlear Results and A2 Milk’s 40% Rally

4 hrs ago

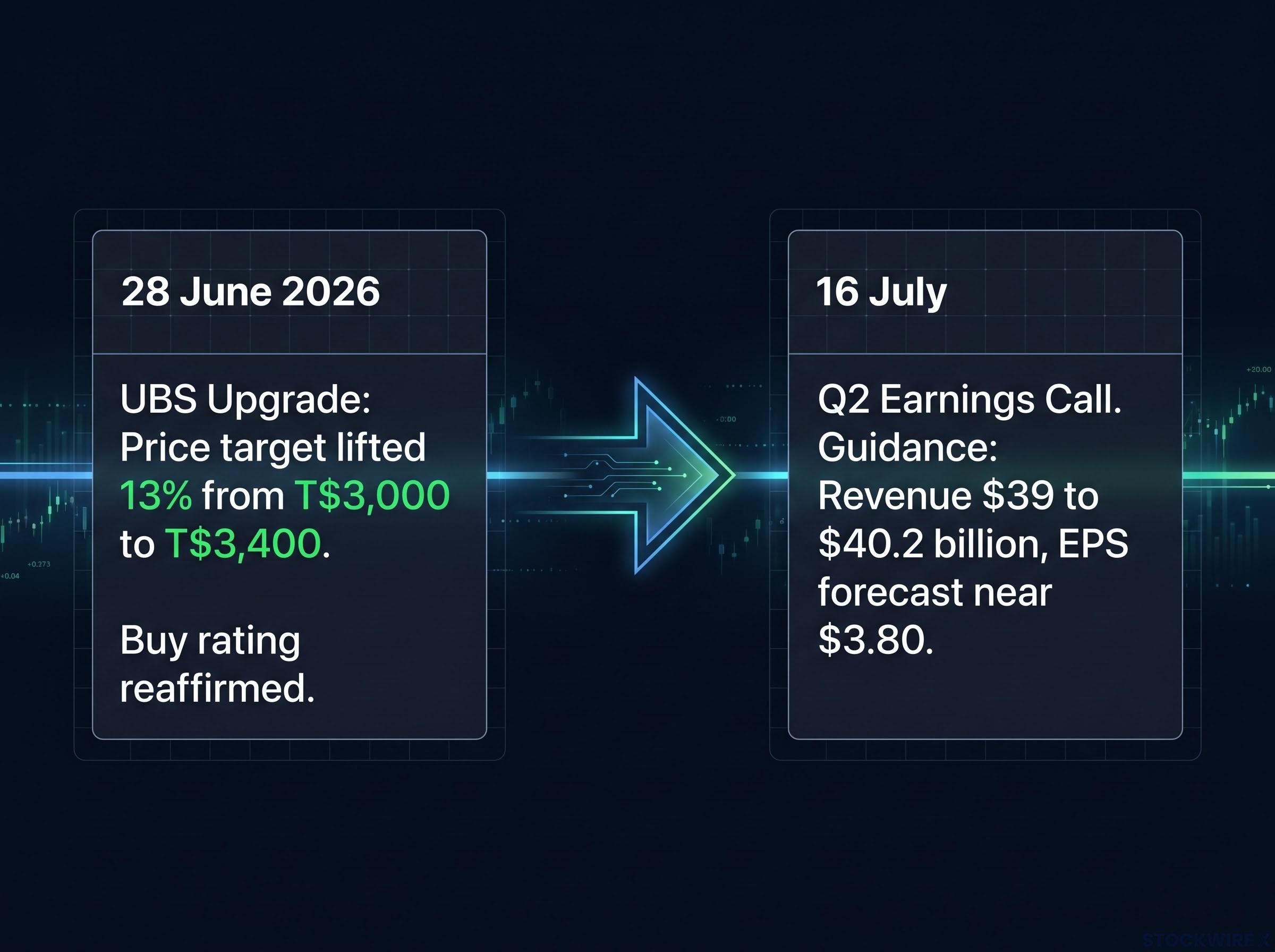

UBS raised its TSMC price target by more than 13% to T$3,400 and reaffirmed a Buy rating on 28 June 2026, and the timing is deliberate: the upgrade lands 18 days before TSMC reports Q2 2026 earnings on 16 July, framing the event as a catalyst rather than a risk.

This is not a routine valuation refresh. UBS revised its 2026 revenue growth forecast upward, reflecting a strengthened view on TSMC’s earnings path at a moment when the company sits at the centre of the AI infrastructure buildout. With consensus Q2 earnings-per-share (EPS) forecasts near $3.80 and revenue guidance already set at $39 to $40.2 billion, the bar is high and UBS is still raising its hand.

Here is what the three structural catalysts behind the upgrade, AI demand, capex expansion, and a potential 2027 price hike, actually mean for investors, and exactly what TSMC needs to confirm on 16 July for this thesis to hold.

The specifics of the upgrade matter, but so does the calendar. UBS published its revised TSMC price target on 28 June 2026, nearly three weeks before the Q2 earnings call. Pre-earnings upgrades of this kind are a specific signal: the analyst expects the event to confirm, not challenge, the thesis.

Three components define the call:

TSMC’s own Q2 guidance: Revenue of $39 to $40.2 billion, with full-year 2026 growth exceeding 30% in USD terms.

According to Investing.com forecasts, Q2 EPS is expected to land near $3.80 with quarterly revenue of approximately $40.06 billion. UBS is telling the market that these numbers are a floor, not a ceiling, and that investors who wait for the print may pay a higher price for the same conviction.

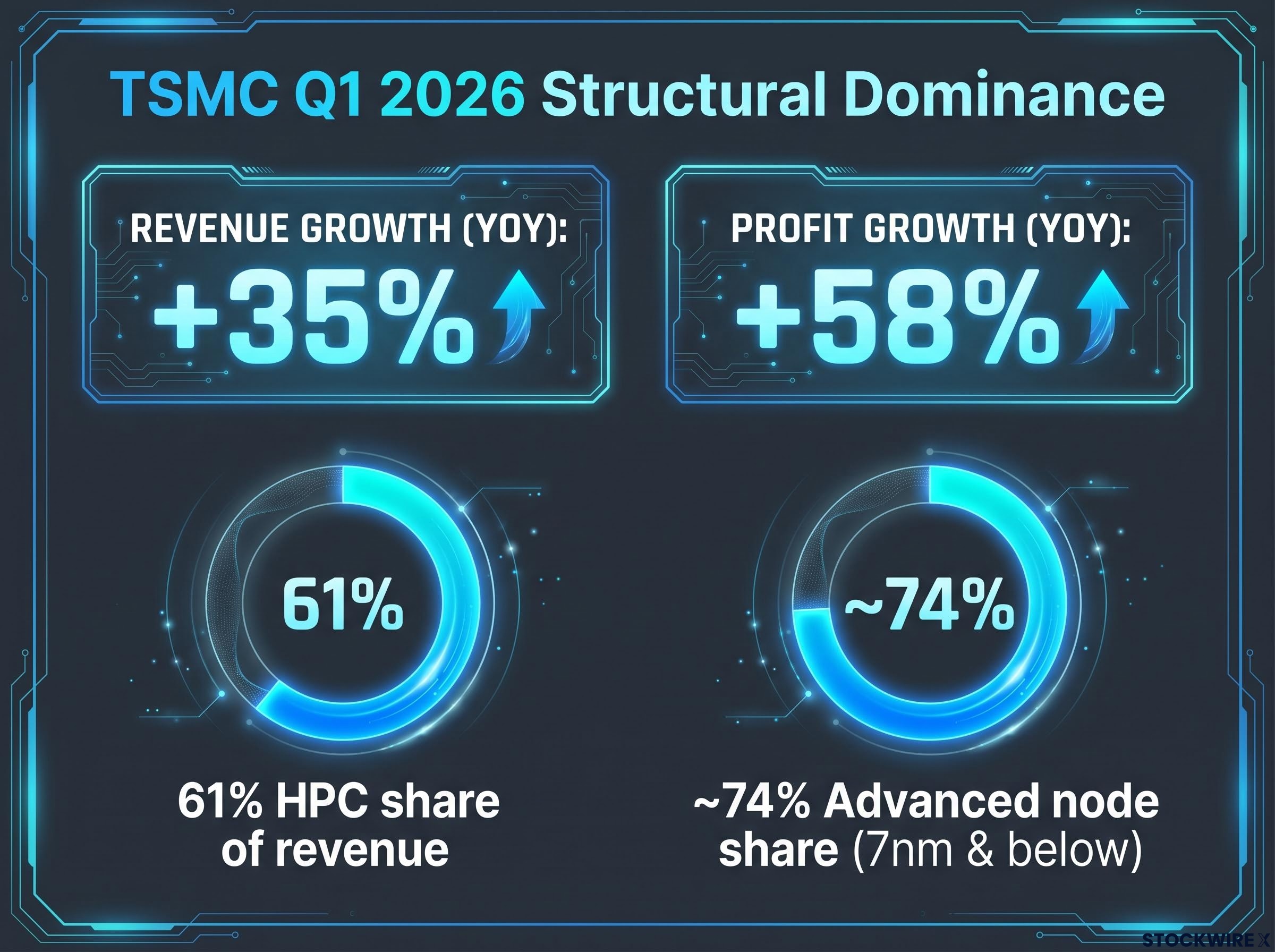

TSMC’s Q1 2026 results provide the empirical grounding for UBS’s demand thesis, and the numbers are not subtle.

| Revenue Metric | Q1 2026 Figure |

|---|---|

| Revenue growth (YoY) | +35% |

| Profit growth (YoY) | +58% |

| HPC share of revenue | 61% |

| Advanced node share of wafer revenue (7nm and below) | ~74% |

TSMC guided Q2 2026 revenue to $39 to $40.2 billion, explicitly crediting “extremely robust” AI demand for cutting-edge nodes. The high-performance computing (HPC) segment, which encompasses AI processors, now accounts for 61% of total quarterly revenue. That makes it the dominant business line, not a growth adjunct.

When HPC accounts for 61% of revenue and 74% of wafer revenue comes from nodes below 7nm, you are no longer looking at a diversified chipmaker with an AI tailwind. You are looking at an AI infrastructure company with a legacy segment attached.

TSMC’s foundry dominance is inseparable from the structural architecture of the AI chip supply chain, where Nvidia, ASML, and Broadcom each occupy distinct non-interchangeable layers that collectively explain why hyperscaler capex commitments translate so directly into TSMC order volume.

The distinction matters for risk assessment. Hyperscaler customers are making multi-year, capex-heavy cluster investments rather than ordering in short cycles. Order visibility appears unusually long, with AI and HPC stretching TSMC’s production “to maximum levels” according to industry analysts.

This supports UBS’s claim that demand has not peaked. The 16 July call is where management will either confirm or complicate that visibility picture, particularly around how far out firm orders extend into 2027.

TSMC’s 2026 capital expenditure (capex) guidance of $52 to $56 billion is not just a spending figure. It is a declaration of strategic intent. Against the approximately $40.9 billion spent in 2025, this represents an increase of roughly 37% year-over-year.

The 37% year-over-year capex increase represents one of the sharpest single-year jumps in recent TSMC history, and management expects to spend toward the upper end of the range.

The spending is geographically distributed:

According to UBS, capital expenditure is expected to keep climbing throughout the 2026 to 2028 window as TSMC builds out capacity to address customer concerns around supply constraints. For investors, the tension is real: higher capex will compress free cash flow and may pressure margins as overseas fabs ramp with lower initial utilisation and higher cost structures.

A three-year capex ramp of this scale tells you TSMC’s management has line of sight to demand that justifies spending before the revenue arrives. It also means near-term free cash flow will be under pressure, and investors need to decide whether they are comfortable with that trade-off. The geographic diversification does reduce some geopolitical risk, which can support valuation multiples even as near-term costs rise.

The hyperscaler capex cycle driving TSMC’s order book is simultaneously compressing the return on equity of the companies placing those orders, with depreciation and amortisation projected to climb from 7% of revenue in 2022 to approximately 12% by 2027, a structural asymmetry that concentrates profitability at the supplier layer rather than the buyer layer.

UBS’s most speculative but potentially most impactful call is its expectation that TSMC will implement a wafer pricing increase as early as the beginning of 2027. In a capacity-constrained environment where AI and HPC demand exceeds current manufacturing capabilities, the preconditions for pricing power are in place.

The mechanism is straightforward. Once capacity is built and fixed costs are largely sunk, incremental revenue from higher wafer prices flows disproportionately into operating income and EPS. Even a modest percentage increase in average selling prices (ASPs), the average price received per unit sold, has an outsized earnings impact.

This matters because many Street estimates currently assume relatively stable pricing. If the market begins pricing in higher 2027 ASPs, consensus earnings for 2027 and beyond could be revised upward. The share price re-rating from a confirmed price hike could be larger than the underlying earnings improvement alone.

Three conditions need to hold for the 2027 price hike to materialise:

Samsung and Intel are investing in advanced-node capacity, and any credible progress at 3nm or below would give customers like Nvidia and Apple alternative sourcing options. Customer contract structures may also constrain TSMC’s ability to renegotiate pricing on short timescales. And if AI capital spending softens in 2027 due to broader macro conditions, pricing power would weaken regardless of competitive positioning.

TSMC’s competitive moat at 3nm and below, where its wafer capacity is estimated at roughly eight times that of Samsung and Intel combined, is the structural foundation on which both the pricing power thesis and customer lock-in argument ultimately rest.

The Q2 earnings call on 16 July is not just a results print. It is a thesis validation event.

The four watchpoints below will determine whether UBS’s T$3,400 target looks conservative, realistic, or ahead of itself. Investors who enter the call with a clear evaluation framework are better positioned to act on what management actually says rather than reacting to a headline EPS number.

| Watchpoint | What to Listen For | Why It Matters to the Thesis |

|---|---|---|

| Capex guidance | Any updates to the $52-$56 billion range; commentary on 3nm and below capacity additions | Confirms whether management still sees demand sufficient to justify upper-end spending |

| AI and HPC demand visibility | How far out TSMC has firm orders; whether management reinforces multi-year structural demand | Validates UBS’s claim that AI demand has not peaked and supports revenue estimate upgrades |

| Margin and cost commentary | Overseas fab ramp costs, tariff exposure, currency headwinds; any signals around value-based pricing | Determines whether revenue growth translates into earnings growth or gets absorbed by cost pressures |

| Competitive and geopolitical risk | How management characterises threats from Samsung, Intel, and Terafab at leading-edge nodes; raw material and supply-chain dependencies | Assesses whether TSMC’s pricing power and customer lock-in face credible near-term threats |

How management answers these four questions will tell you whether the current share price reflects realistic expectations or priced-in perfection, and which direction the earnings reaction is likely to move.

The opportunity case is grounded in structural positioning:

The risk case is equally evidence-based:

The question for investors is not whether TSMC is a strong business. It is whether the current price already reflects the good news UBS is projecting. The 16 July earnings call is the event that will clarify which direction the balance of evidence is tilting.

For investors wanting a disciplined framework for managing the transition from the current capacity-constrained environment to the 2027-2029 supply wave, our dedicated guide to semiconductor cycle positioning covers the five-indicator system for capturing peak-cycle gains without holding premium multiples past their expiry date.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

UBS raised its TSMC price target to T$3,400 on 28 June 2026, up from T$3,000, representing a 13% increase, while reaffirming its Buy rating.

UBS published its upgrade 18 days before the 16 July earnings call as a deliberate signal that it expects the results to confirm rather than challenge its thesis, with Q2 revenue consensus near $40.06 billion and EPS near $3.80 treated as a floor, not a ceiling.

TSMC guided 2026 capex to $52-$56 billion, up roughly 37% from approximately $40.9 billion in 2025, covering new fabs in Arizona, Japan, and Taiwan, signalling that management has demand visibility sufficient to justify spending before the revenue materialises.

UBS expects TSMC to raise wafer average selling prices as early as 2027, which would drive outsized EPS growth because incremental revenue at that point flows largely into operating income; the thesis requires continued capacity constraints, no credible competitive narrowing from Samsung or Intel, and stable AI infrastructure spending.

The four key watchpoints are updates to the $52-$56 billion capex guidance, the extent of firm AI and HPC order visibility, margin commentary covering overseas fab ramp costs and tariff exposure, and management's characterisation of competitive threats from Samsung and Intel at leading-edge nodes.