Why BTK Inhibitor Resistance Opens a Door for Off-the-Shelf CAR-T

2 hrs ago

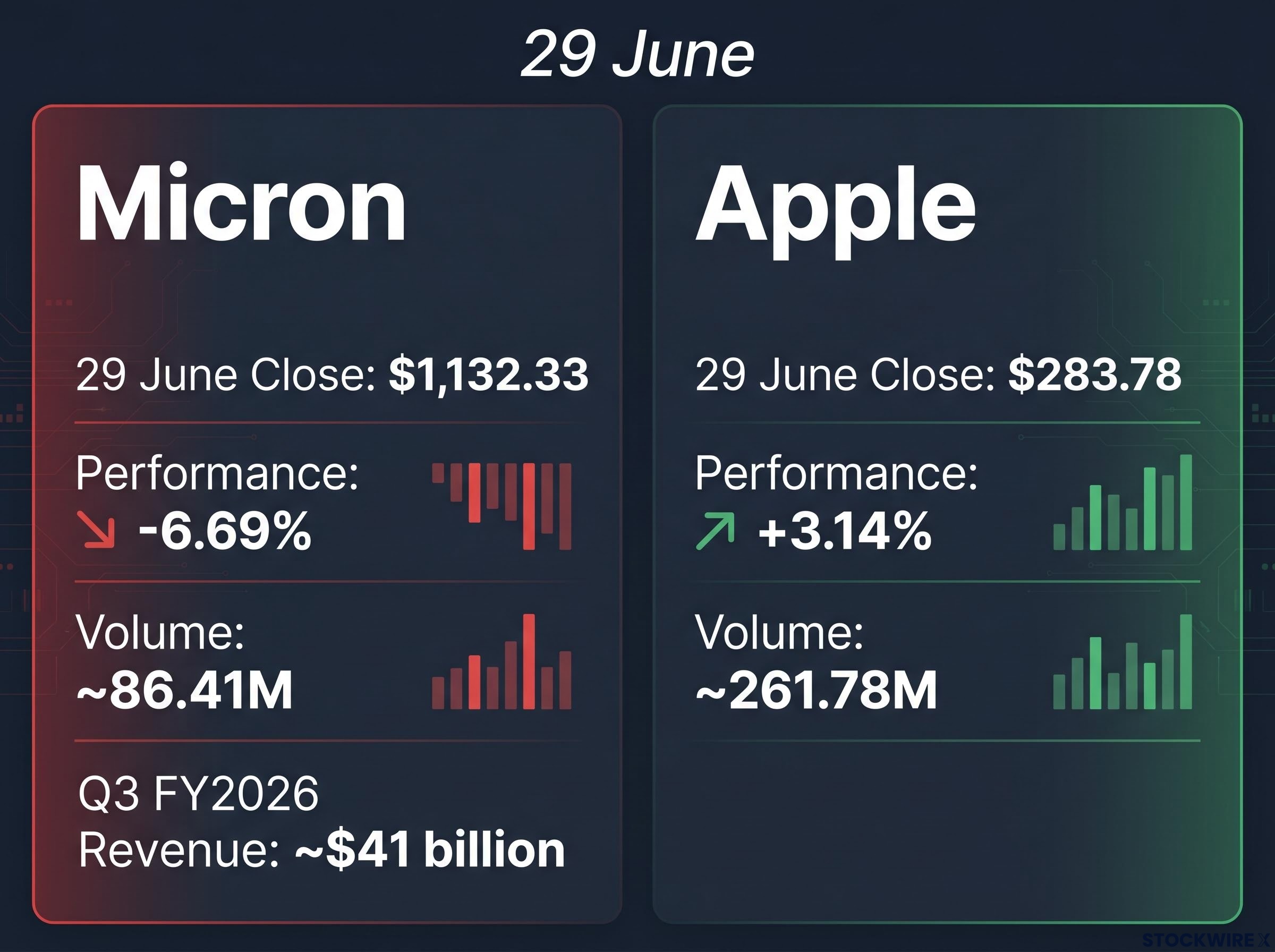

Micron’s revenue roughly quadrupled year over year. Gross margins pushed into the low-to-mid eighties. The stock fell 6.69% on 29 June.

That contradiction sits at the centre of a broader fracture running through AI-linked equities right now. Chip demand is not in question. What has cracked is investor confidence in the path from that demand to actual returns. Apple rising 3.14% on the same session Micron dropped nearly 7% is not random noise. It reflects a deliberate rotation in how markets are sorting AI-era winners, and the sorting criteria have changed.

The contrasting moves in Micron, Apple, Nvidia, and Microsoft reveal where AI infrastructure value is actually being captured, and where it is still being spent without a clear payoff. Here is the framework for reading that divergence before positioning in any of these names.

Micron’s Q3 FY2026 results were, by any conventional measure, exceptional. Revenue reached approximately $41 billion, roughly quadrupling year over year. Gross margins rose into the 81-85% range, driven by surging demand for high-end memory used in AI data centres. This was not a company reporting modest beats. This was a company posting one of the strongest quarters in semiconductor history.

Revenue roughly quadrupled year over year. Gross margins hit the low-to-mid eighties. The stock then fell more than 20% from its post-earnings highs.

The first pressure came from outside Micron entirely. Broadcom’s early June 2026 earnings, where management provided AI revenue guidance slightly below some analyst expectations, triggered a sector-wide reassessment of whether AI semiconductor spending is starting to plateau. That repricing hit every AI hardware name, but it hit Micron, trading at AI-era multiples, with particular force.

The second pressure was product-specific. Reports surfaced regarding potential adjustments to Nvidia memory configurations for some AI platforms, raising concerns about future demand for high-bandwidth memory (HBM), the specific high-margin product category driving Micron’s margin expansion.

Micron’s 16 non-cancellable HBM supply agreements, with pricing floors above any prior cycle peak, are the structural element most analysts cite when distinguishing the current memory upcycle from previous ones; those HBM supply agreements also explain why concerns about Nvidia configuration adjustments cut so sharply against a thesis built on locked-in contract visibility.

The third was technical. Micron has been heavily owned by retail traders. Some strategists argue that investors sold positions to free cash for high-profile IPOs such as SpaceX, adding mechanical selling pressure on top of fundamental doubts. By 29 June, shares closed at $1,132.33, down 6.69% on volume of approximately 86.41 million shares.

The results confirmed demand is real. The price action told a different story: the market has stopped treating strong chip demand as a sufficient reason to hold a stock trading at AI-era multiples.

The market did not simply reward Apple by default. The initial reaction to its price increases, announced around 25 June, was sharply negative. Shares fell more than 6%, their worst single day in over a year, as investors priced in the risk that higher sticker prices would compress consumer demand.

The increases were substantial:

| Product | Old Price | New Price |

|---|---|---|

| MacBook Air 512GB | $1,099 | $1,299 |

| iPad models (various) | Varied | +$100-$150 across range |

Apple cited AI-driven memory and storage cost inflation as the explicit rationale. Then the recovery came. By 29 June, shares closed at $283.78, up 3.14% on volume of approximately 261.78 million shares. Investor sentiment moved away from demand-risk concern toward a view that Apple can absorb rising component costs and transfer them to consumers without undermining its brand standing or the loyalty of its ecosystem.

Two dynamics explain why the market designated Apple a quality refuge:

Apple’s arc from its own sharp selloff to a 29 June gain tells you the market is actively sorting companies by who absorbs AI costs versus who passes them through, and is placing a premium on the latter.

The context for Micron’s individual decline is a sector-level event that preceded it. In early June 2026, around 5-6 June, the SOX (Philadelphia Semiconductor Index) recorded its steepest single-session fall in years after Broadcom’s AI revenue guidance landed short of certain analyst forecasts, prompting a broad repricing across the sector.

The scale was severe. Nvidia alone lost approximately $300-$330 billion in market capitalisation at intraday lows. Broadcom and Marvell both saw sharp double-digit declines before partially recovering. The affected names tell you this was not about one company’s results:

The SOX historical data shows the Philadelphia Semiconductor Index has experienced several sharp single-session drawdowns during the current AI investment cycle, making the early June 2026 repricing severe but not without precedent in a sector prone to sentiment-driven dislocations at elevated valuation multiples.

By 29 June, Nvidia had stabilised somewhat, closing at $192.53, down a comparatively modest 1.64% on approximately 179.30 million shares. But stabilisation is not restoration.

Nvidia’s CEO characterised the selloff as a buying opportunity, pointing to continued global AI infrastructure investment and arguing that underlying AI demand retains structural durability.

That management optimism sits in tension with the price action. The fact that even a partial recovery in Nvidia still left it down on 29 June signals that investor confidence in the AI hardware thesis has not been restored. It has only paused from active selling.

Start with what is unambiguously true. Hyperscalers are committing tens of billions of dollars to data centres and specialised chips. Chip demand, as Micron’s results demonstrate, is genuine and growing. No serious market participant disputes this.

The problem is what comes after the spending.

Each quarter in which AI-related spending grows faster than identifiable AI-driven revenue adds valuation strain to hardware and infrastructure names. That pattern, which investors are now actively testing as a thesis, has shifted the criteria for what counts as an attractive AI position.

Morningstar has quantified the capex-to-revenue lag at 18-24 months for AI infrastructure investments, a timeline that creates a structural problem for semiconductor names trading at AI-era multiples: each quarter that passes without monetisation evidence does not leave the valuation premium intact, it actively erodes the justification for holding it.

The distinction between the old trade and the new one is specific:

Evidence like Micron’s exceptional margin and revenue performance is now read not simply as good news, but as a signal that customers’ rising costs may not be sustainable without commensurate end-user revenues. The market has moved from rewarding any AI exposure to demanding proof that AI projects generate cash flows sufficient to justify today’s prices.

For anyone evaluating an AI-linked position today, the central question is no longer “does this company benefit from AI demand?” It is “can this company show that AI demand is generating cash flows that justify its current price?”

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

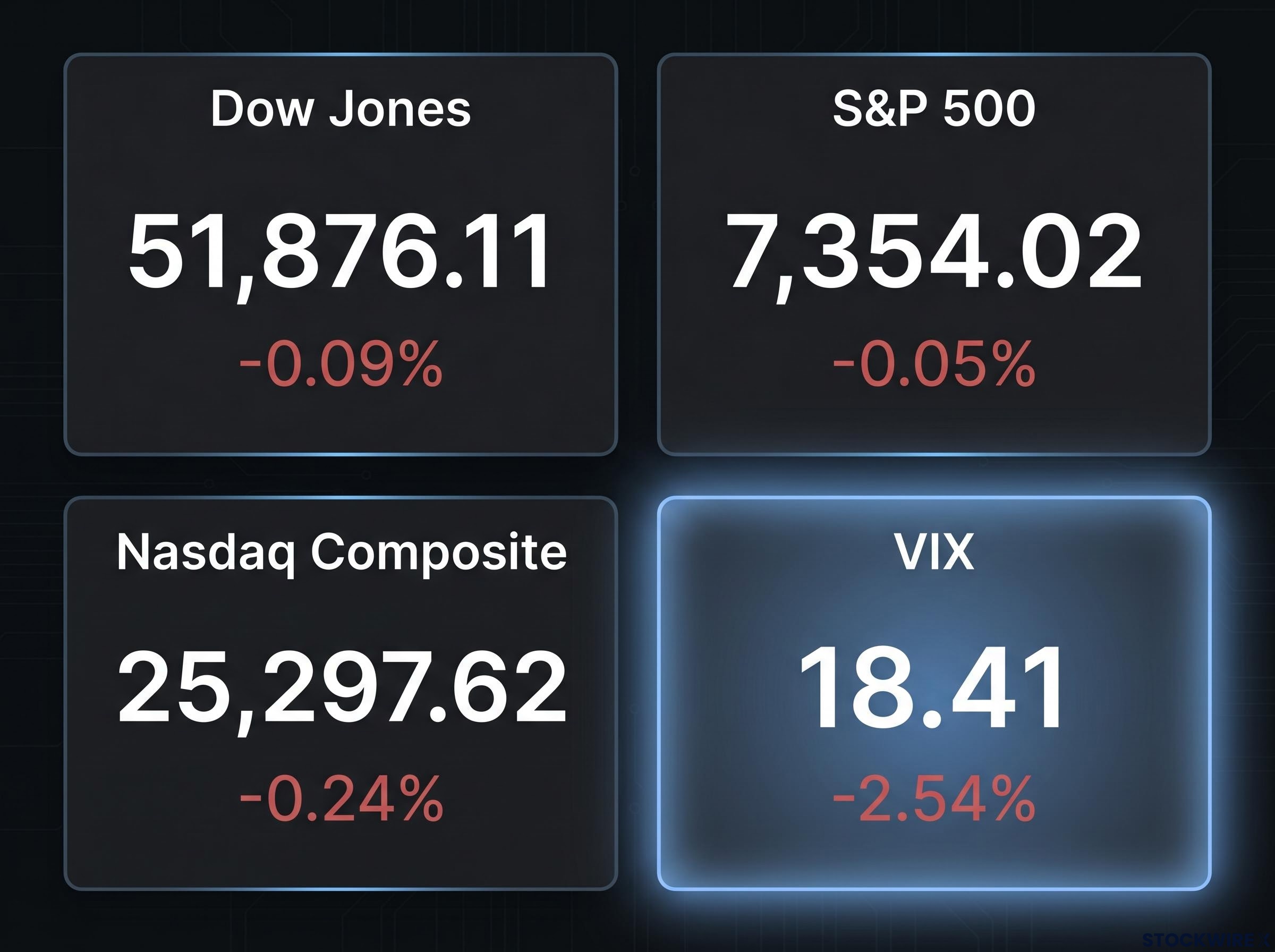

The broader market on 29 June was not panicking. That is precisely what makes the semiconductor repricing more significant, not less.

| Index | 29 June Level | Change | Signal |

|---|---|---|---|

| Dow Jones | 51,876.11 | -0.09% | Flat, no broad risk-off |

| S&P 500 | 7,354.02 | -0.05% | Near unchanged |

| Nasdaq Composite | 25,297.62 | -0.24% | Mild tech underperformance |

| VIX | 18.41 | -2.54% | Declining fear, selective repricing |

U.S. and European equity futures edged higher, partly lifted by easing Middle East tensions. Tech valuation concerns and a firming U.S. dollar kept Asian markets on the back foot.

A VIX below 20 alongside individual semiconductor stocks moving 6-7% in a single session is the market’s way of telling you this is a deliberate, considered repricing of a specific thesis. Calm markets discriminating against specific narratives produce a more durable signal than broad risk-off moves. Investors rotating within tech are making an active choice, not reacting to external shock.

The analytical work across this piece points to three distinct readings of the current environment, each flowing from the data rather than arriving as generic advice.

For investors wanting a structured framework to apply this logic to specific holdings, our deep-dive into moat-based AI stock selection examines how Morningstar’s economic moat ratings separate durable AI infrastructure winners from names whose recent gains rest on thematic association rather than structural competitive advantage.

The operating framework for this moment is no longer “AI exposure.” It is “AI earnings quality.” The divergence between Micron and Apple on 29 June is not a one-day anomaly. It is a preview of how the market is likely to sort the AI field for the next several quarters.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The AI exposure trade rewarded any company touching AI infrastructure, favouring revenue growth and order backlogs regardless of cash flow conversion. The AI earnings quality trade, which now dominates market sentiment, rewards companies that can demonstrate AI demand is generating cash flows that justify current prices, prioritising pricing power, margin protection, and identifiable recurring revenue over raw growth.

Three pressures converged: Broadcom's slightly disappointing AI guidance triggered a sector-wide reassessment of AI hardware spending, reports surfaced about potential Nvidia memory configuration adjustments that threatened demand for Micron's high-margin HBM products, and retail investor selling to fund high-profile IPOs such as SpaceX added mechanical pressure on top of fundamental doubts about whether AI-era multiples were still justified.

HBM is the specific high-margin memory product category driving Micron's gross margin expansion into the 81-85% range, and Micron has locked in 16 non-cancellable supply agreements with pricing floors above any prior cycle peak. The concern is that any adjustment to Nvidia's memory configurations for AI platforms could threaten demand for the very product underpinning Micron's margin thesis.

Around 5-6 June 2026, the SOX Philadelphia Semiconductor Index recorded its steepest single-session fall in years after Broadcom's AI revenue guidance came in slightly below analyst forecasts, prompting a broad repricing that hit Nvidia with an approximately $300-$330 billion intraday market cap loss and pushed Broadcom and Marvell into sharp double-digit declines before partial recoveries.

The central question has shifted from whether a company benefits from AI demand to whether it can show that AI demand is generating cash flows sufficient to justify its current price. Companies with demonstrated pricing power and the ability to pass AI-related costs to end customers, like Apple, are being treated as relative safe havens, while infrastructure and component plays like Micron and Nvidia face continued volatility until monetisation evidence accumulates.