DHHF vs GHHF: What Gearing Actually Does to Your Returns

2 hrs ago

A single ETF listed on the ASX in October 2024 now channels investor capital into the armaments programmes, surveillance technology firms, and defence contractors supplying NATO and its allies, charging 0.55% per year to do it. Global defence spending is accelerating at a pace not seen in decades. European rearmament, Indo-Pacific security concerns, and Australia’s own AUKUS commitments are each pulling budgets higher. Australian retail investors looking to position around this structural shift now have a direct vehicle: ARMR, the Betashares Global Defence ETF. But the fund bundles together complex sector dynamics, ethical questions, and thematic valuation risks that are easy to underestimate from the headline alone. This explainer walks through exactly what ARMR holds and how it works, what drives and threatens its underlying theme, and how it fits (or does not fit) alongside the other ways an ASX investor can access defence exposure.

ARMR tracks the VettaFi Global Defence Leaders Index, a rules-based benchmark that selects companies deriving more than 50% of their revenue from the development and manufacturing of military and defence equipment or defence technology. Because the index is rules-based rather than actively managed, the fund behaves more like a specialised sector index fund than a stock-picking vehicle. The companies that enter and exit are determined by revenue tests and eligibility criteria, not by a portfolio manager’s discretion.

Australia now has more than 2.69 million investors holding ASX-listed ETFs, a cohort that grew by 411,000 in 2025 alone as funds under management reached $330.6 billion, reflecting how thoroughly the structure has moved from niche product to mainstream portfolio tool.

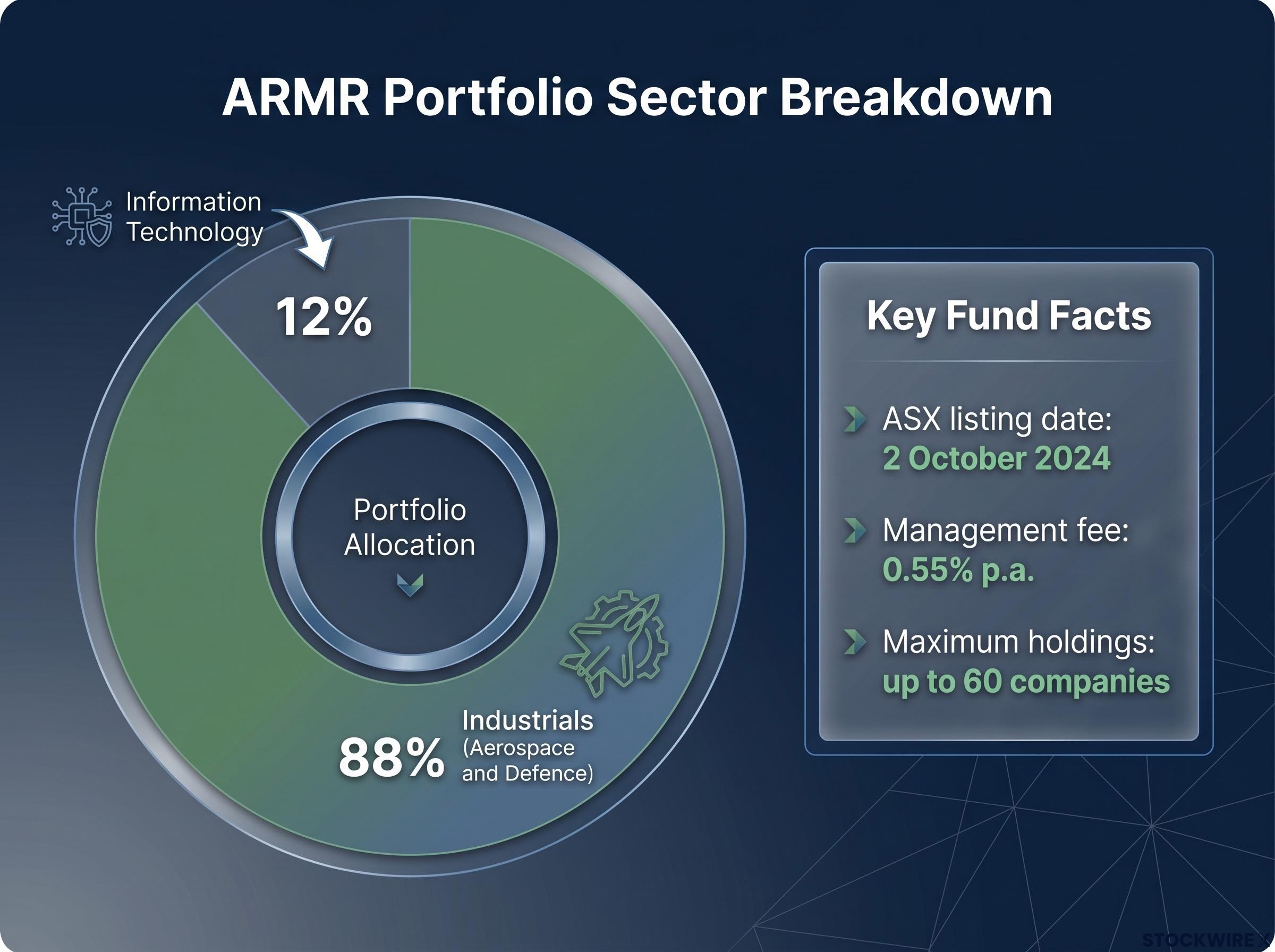

Key product facts at a glance:

Eligible companies must be headquartered in NATO member countries or major NATO allies, a grouping that explicitly includes Australia, Japan and South Korea. This geographic filter is a deliberate design choice, not a side effect. It shapes the geopolitical character of the portfolio, anchoring it to Western-aligned defence supply chains and excluding manufacturers in non-allied nations regardless of their size or revenue.

The named holdings make the abstract defence theme tangible. Among the largest positions are six companies spanning three continents and multiple sub-segments of the industry.

| Company | Headquarters Country | Primary Defence Activity |

|---|---|---|

| Palantir Technologies | United States | Data analytics and intelligence software |

| Rheinmetall AG | Germany | Armoured vehicles and munitions |

| Safran SA | France | Aircraft systems and propulsion |

| Lockheed Martin | United States | Advanced weapons, aircraft and space systems |

| BAE Systems | United Kingdom | Naval vessels, electronic warfare and land systems |

| General Dynamics | United States | Combat vehicles, submarines and IT services |

The sector breakdown reinforces how broad the modern defence industry has become. It is no longer confined to tanks and jets.

Geographic exposure sits primarily with US and European companies. Third-party data occasionally showing a high Australian allocation is unreliable given the index’s explicitly global mandate. Investors expecting domestic defence exposure should note that ARMR is dominated by the large Northern Hemisphere primes and technology firms, which behave very differently to Australian small-cap defence names.

Defence revenues flow from government procurement budgets, not consumer wallets. This single fact shapes the entire investment thesis behind ARMR.

Why this matters: Government-budget-driven revenues insulate defence earnings from typical business cycles. Consumer confidence can fall, retail sales can contract, and defence contract payments continue. The trade-off is that these earnings carry political sensitivity instead of consumer sensitivity, a different risk profile rather than a lower one.

Four structural forces underpin the current spending environment:

The distinction between structurally elevated and cyclically elevated matters for investors assessing ARMR’s staying power. The spending commitments outlined above are tied to multi-year policy decisions and alliance obligations, not to short-term sentiment.

SIPRI world military expenditure data for 2025 confirms that European and Asia-Pacific defence budgets are expanding at rates not recorded in decades, lending independent empirical weight to the structural spending narrative that underpins ARMR’s investment thesis.

Each of the structural tailwinds described above has a corresponding risk operating on a different timeline. Honest assessment of ARMR requires examining both sides.

Defence sector valuations had already re-rated substantially before ARMR listed, with ITA and XAR trading at forward price-to-earnings multiples roughly 10-20% above their five-year averages by mid-2026, and Goldman Sachs, BofA, and Barclays all flagging overcrowding in April and May of that year; historical analogues from 1991, 2002, and 2003 show reversals of 10-30% once budget realities replaced conflict headlines.

A note on ethics: Investors with ESG screens, values-based mandates, or personal ethical objections to weapons manufacturing should assess their position before allocating. This is the one risk category that cannot be managed through diversification, position sizing, or timing.

Understanding these risks is not a reason to avoid ARMR automatically. Sizing the position appropriately requires knowing which risks are quantifiable and which are structural features of how the defence theme operates.

The Australian domestic defence universe is small relative to the global industry. Focusing only on ASX-listed names omits the large US and European contractors that generate the majority of global defence revenue. Stock picking in this space also requires ongoing monitoring of contract pipelines, export permissions, programme risk, and government relationships, work that is demanding for most retail investors.

The domestic universe of ASX defence names is small but demonstrably reactive, with EOS, DroneShield, and Elsight posting intra-session gains of up to 11% on a single geopolitical announcement in May 2026, a pattern that illustrates how quickly individual-stock positions in this sector can swing on sentiment rather than contract fundamentals.

ARMR addresses several of these limitations through a single trade. The fund provides global breadth across up to 60 companies, removes the need to research individual names, and diversifies away the idiosyncratic risk that a contract loss, cost overrun, or governance event can impose on a single stock.

| Factor | ARMR ETF | Individual ASX Defence Stocks |

|---|---|---|

| Geographic breadth | Global (NATO members and allies) | Australia only |

| Diversification | Up to 60 holdings across sub-sectors | Typically 1-2 positions |

| Required investor effort | Index-managed; minimal monitoring | Active research on contracts, governance, programmes |

| Cost structure | 0.55% p.a. management fee (verify against PDS) | Brokerage only; no ongoing management fee |

Three limitations come with the ETF approach, and all are knowable upfront rather than surprises. First, investors cannot exclude specific companies within the portfolio; the index rules determine holdings, not personal preference. Second, single-stock outperformance from a well-chosen name is surrendered in favour of diversified sector exposure. Third, the 0.55% p.a. management fee is an ongoing cost that compounds over time.

These are costs that suit some investors and not others. For those who want genuine defence sector exposure without becoming sector specialists, the ETF resolves several practical problems. For those with strong conviction in a specific company and the expertise to monitor it, direct ownership may serve them better.

Before ARMR belongs in any portfolio, five practical checks are worth completing:

ASIC Regulatory Guide 282 on Exchange Traded Products sets out the obligations ETF issuers must meet around product disclosure, target market determinations, and AFS licensing, forming the regulatory framework within which ARMR and similar products operate in Australia.

Investors with short time horizons, low risk tolerance, or active ethical screens may reasonably choose not to hold ARMR even if they acknowledge the financial case. No thematic ETF is appropriate for every investor, and that judgement is not a reflection of whether the thesis is sound.

ARMR is a satellite holding, not a core position. In practical terms, this means a small allocation alongside broad-based Australian and global equity ETFs, sized so that underperformance in the defence theme does not damage overall portfolio outcomes. Many investors would keep a single thematic exposure to a small percentage of total equities, treating it as an expression of a long-term view on sustained government defence budgets rather than a tactical trade.

Investors exploring the structural reasons why thematic allocations often underperform their reported returns will find our deep-dive into thematic ETF investor timing risk, which examines how the ARK Innovation ETF’s +233% reported return translated into an estimated -35% experience for actual investors due to poorly timed inflows near peak valuations, a dynamic directly applicable to any single-theme product entering after a strong run.

ARMR is a precise, rules-based instrument tied to a specific geopolitical and fiscal thesis. It is not a generic industrials fund or a broad equity product. The investment case remains intact as long as government defence budgets stay elevated, NATO and Indo-Pacific spending commitments continue, and technology modernisation sustains demand across the industry’s sub-sectors.

The case weakens if budget consolidation overtakes rearmament, if diplomatic de-escalation reduces procurement urgency, or if valuations compress after the re-rating that preceded the fund’s listing. These are not predictions; they are the conditions that determine whether the thesis holds.

Reading the Product Disclosure Statement and, where appropriate, consulting a licensed financial adviser are the concrete next steps before any allocation. The ETF exists to make a specific thematic exposure accessible. Whether that exposure belongs in a given portfolio is a personal question, not a product question.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ARMR is an ASX-listed ETF that tracks the VettaFi Global Defence Leaders Index, selecting companies that derive more than 50% of their revenue from military and defence equipment or defence technology, with holdings capped at up to 60 companies headquartered in NATO member countries or major NATO allies.

ARMR holds up to 60 defence and defence-technology companies, with roughly 88% of portfolio weight in aerospace and defence industrials and approximately 12% in information technology firms such as Palantir Technologies; named large positions include Rheinmetall, Lockheed Martin, BAE Systems, Safran, and General Dynamics.

ARMR charges a management fee of 0.55% per annum, though investors should verify the current fee against the issuer's latest Product Disclosure Statement before allocating.

The key risks include political and budget reversals that could reduce government defence spending, thematic valuation risk given defence stocks had already re-rated before ARMR listed, single-theme concentration across all 60 holdings, and ethical considerations for investors with ESG or values-based screens.

ARMR provides global breadth across up to 60 NATO-aligned companies for a 0.55% annual fee, removing the need for active research on individual contracts and governance; individual ASX defence stocks offer Australia-only exposure with no management fee but require ongoing monitoring and carry higher idiosyncratic risk from contract losses or programme setbacks.