Stock-Bond Correlation Hits 30-Year Extreme, Rattling 60/40 Investors

3 hrs ago

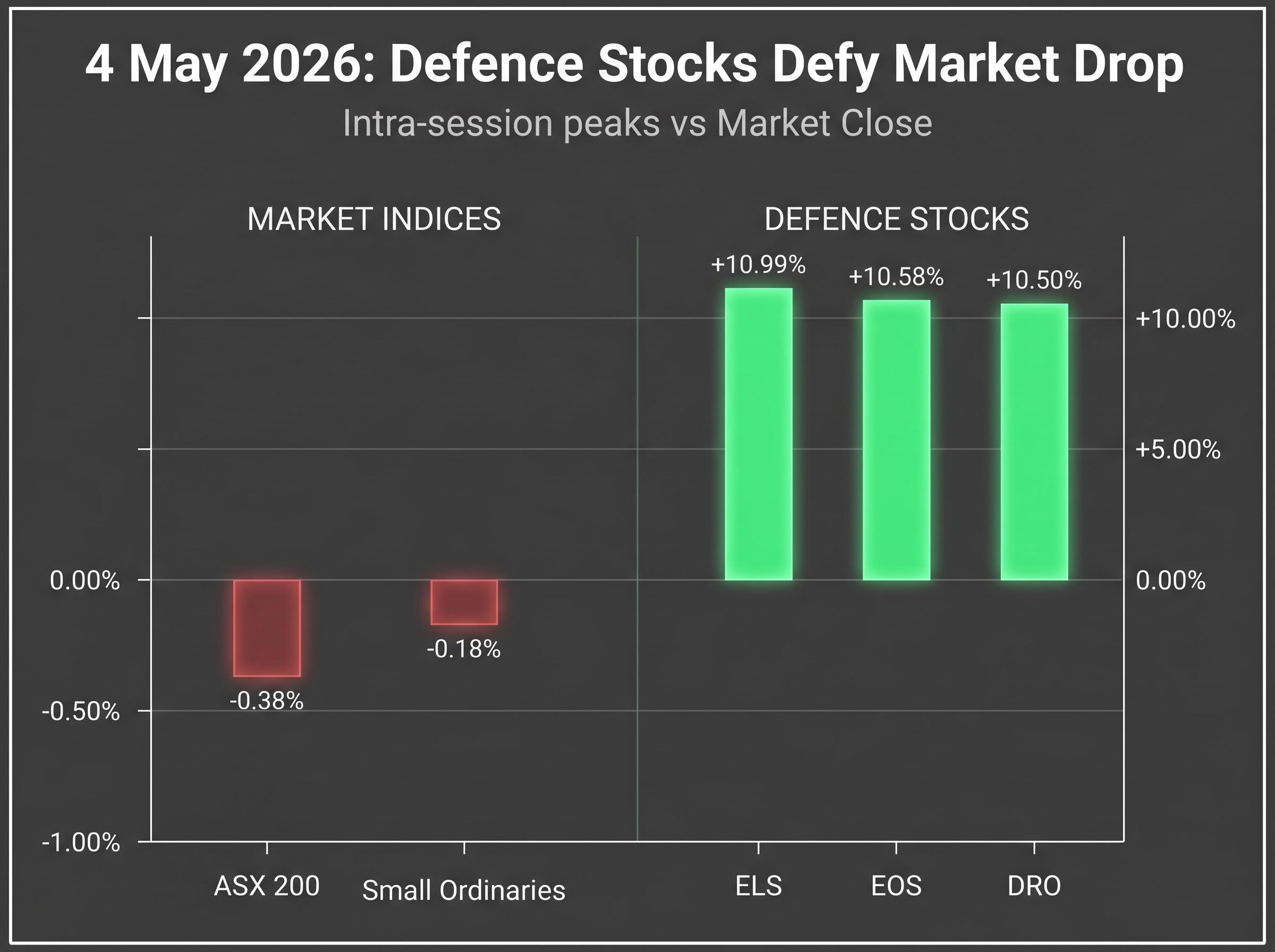

The ASX 200 fell 32.7 points on 4 May 2026, shedding 0.38% to close at 8,697.1. Consumer Staples dropped 2.58%. Most sectors finished in the red. Yet three ASX defence stocks posted gains that, on any other session, would have dominated the market wrap. The catalyst: a signal from US President Trump that American forces would escort neutral tankers through the Strait of Hormuz, an announcement that landed on a defence sector already running hot on counter-drone contracts, AUKUS spending expectations, and a 12-month rally that had already repriced several names by hundreds of percent.

What follows is an examination of which stocks moved and by how much, why the Hormuz announcement connects to these specific companies, and how investors can distinguish a sentiment spike from a durable re-rating in a sector where geopolitical headlines arrive faster than contract confirmations.

The Small Ordinaries Index fell 0.18% on 4 May 2026. This was not a session where small caps rallied broadly and defence names rode the tide. The moves in Electro Optic Systems (EOS), DroneShield (DRO), and Elsight (ELS) were structurally distinct from the market’s direction.

The divergence in magnitude across the three names tells its own story.

| Stock | Intra-session move | Session peak | Approximate weekly gain |

|---|---|---|---|

| EOS | +6.0% to $9.89 | +10.58% to $9.93 | ~40% |

| DRO | +4.6% to $3.75 | +10.50% to $4.00 | ~24% |

| ELS | +2.4% | +10.99% to $5.25 | ~50% |

Trump’s stated intention to provide military escort for neutral tankers navigating the Strait of Hormuz connected directly to the operational capabilities these three companies sell. Counter-drone systems, drone detection platforms, and drone communications technology are precisely the categories a naval escort operation in contested waters would require.

The broader market was pricing in risk. These names were pricing in demand.

The rally makes more sense once the product categories are grounded in what a Strait of Hormuz military operation would actually look like on the water.

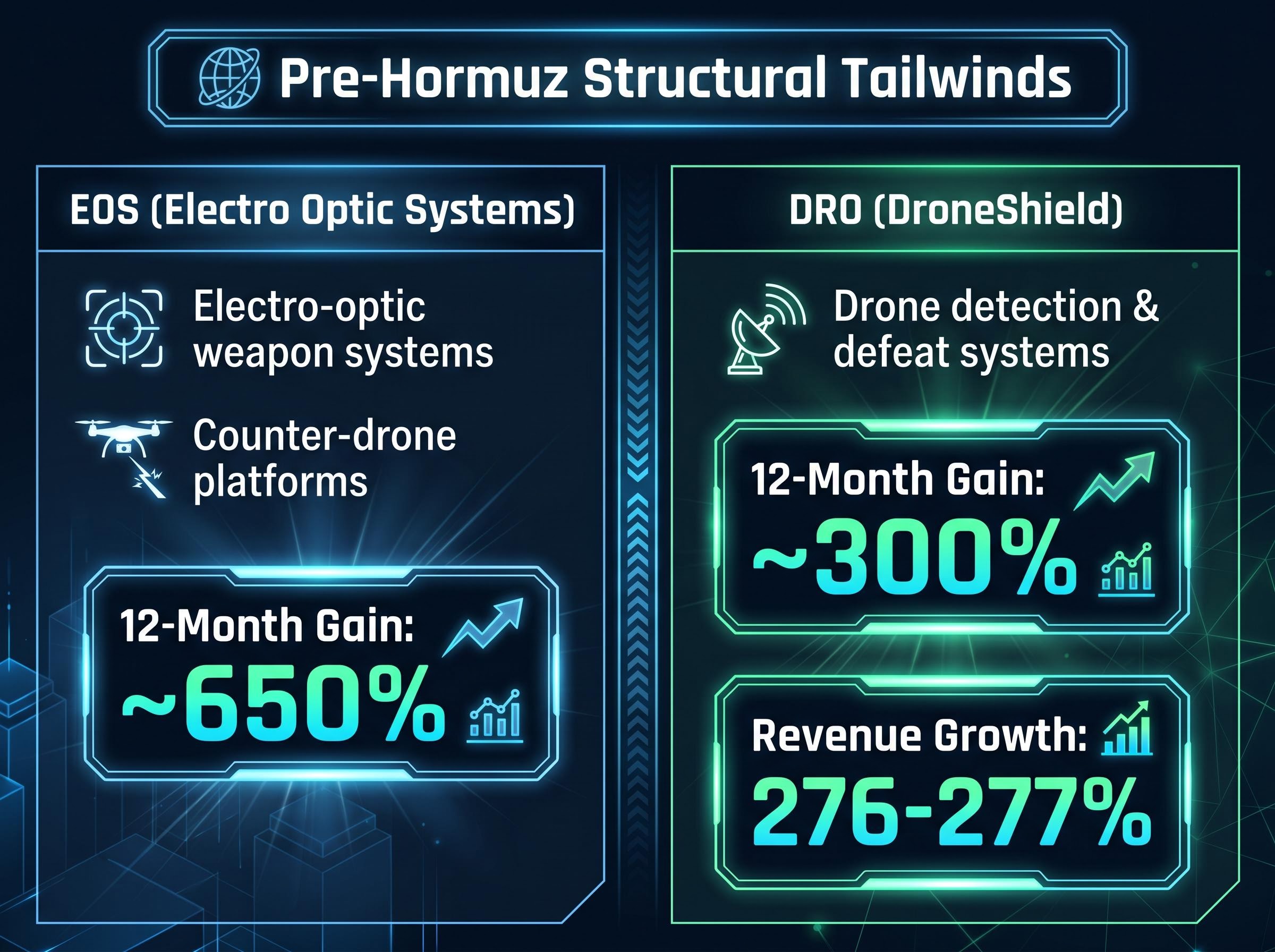

Bell Potter has designated 2026 the “year of the drone,” citing a global spending inflection in drone detect-and-defeat systems.

That characterisation explains why Trump’s announcement landed on fertile ground. Analyst consensus on DRO sits at an average price target of $4.90, approximately 15% above the 4 May peak, suggesting the broker community had already been pricing in accelerating demand before the Hormuz catalyst arrived.

A geopolitical announcement does not create revenue. It reprices the probability and timing of future revenue. Understanding this transmission mechanism is what separates reactive trading from informed positioning.

The process operates in three stages:

Small and mid-cap defence names are disproportionately sensitive to this cycle. A single contract can represent a material percentage of annual revenue at their scale, unlike large defence primes where individual awards are marginal to the total.

The AUKUS partnership provides a multi-decade structural demand floor beneath this event-driven cycle, giving Australian defence firms a baseline that extends well beyond any single geopolitical headline.

The 4 May session did not create the defence rally. It accelerated one already underway.

EOS had gained approximately 650% over the prior 12 months, reaching an all-time high before the session began. That appreciation was driven by confirmed counter-drone system orders linked to active conflict zones. DRO had risen approximately 300% over the same period, underpinned by 276-277% revenue growth in its most recent results. These are not speculative positions sustained by sentiment alone; they are companies whose revenue trajectories had already shifted.

The AUKUS partnership commits Australia to a multi-decade shipbuilding, counter-drone, and broader defence capability ramp that provides structural demand visibility regardless of which specific conflict drives headlines in any given quarter. Austal (ASB), another ASX-listed name, carries direct exposure to the AUKUS shipbuilding programme and has been flagged as a strategic position amid Middle East escalation.

Beyond AUKUS, European defence budgets have been elevated across multiple nations in 2026, and Indo-Pacific force posture planning continues to expand counter-drone procurement timelines. The tailwind is global, not dependent on a single theatre or a single announcement.

Bell Potter’s characterisation of a 2026 spending inflection in drone detect-and-defeat systems reflects this broader policy convergence. The structural layer was already in place. Trump’s Hormuz signal added momentum, not foundation.

The analytical case is sound. The risk case is equally specific.

In November 2025, DRO CEO Oleg Vornik’s share sales caused a notable price decline, a reminder that insider actions can diverge from the narrative retail investors are trading on.

The analyst average price target for DRO sits at $4.90, roughly 15% above the 4 May peak. Even the bullish case suggests limited near-term upside from current levels. EOS was already at all-time highs before the session, raising the entry-point risk for new positions.

The structural tailwind is durable. The event-driven premium layered on top of it may not be.

The two-layer structure of this sector, structural fundamentals beneath event-driven sentiment, requires a two-part evaluation process. After any geopolitical catalyst, two questions clarify whether the move is investable or merely tradeable:

The AUKUS spending ramp, the global drone warfare procurement wave, and ongoing Middle East escalation suggest the structural tailwind is likely to generate further event catalysts. This framework will be tested repeatedly.

The 4 May rally in EOS, DRO, and ELS was both event-driven and structurally grounded. Neither characterisation alone captures the full picture. The Hormuz announcement added velocity to a sector that had already repriced on confirmed contracts, revenue inflections, and a multi-decade policy commitment through AUKUS.

The evaluation framework, distinguishing the fundamental layer from the sentiment premium, is the tool that makes future geopolitical catalysts in this sector legible rather than reactive. With AUKUS commitments, global counter-drone procurement expansion, and Middle East escalation all pointing in the same direction, investors who understand the two-layer structure are better positioned than those chasing individual headlines.

Readers seeking deeper context may find value in related analysis covering AUKUS-linked ASX stocks and the broader global defence spending cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding defence spending and procurement timelines are subject to change based on geopolitical developments and government policy decisions.

ASX defence stocks are shares in Australian companies supplying military technology such as counter-drone systems, drone detection platforms, and communications infrastructure. In 2026 they have risen sharply due to AUKUS spending commitments, global counter-drone procurement growth, and geopolitical catalysts like the US Hormuz escort announcement.

US President Trump signalled that American forces would escort neutral tankers through the Strait of Hormuz, a contested maritime corridor where counter-drone and drone communications technology would be operationally required. This repriced the demand outlook for all three companies at a time when the broader ASX 200 fell 0.38%.

Geopolitical escalation signals increased operational tempo to defence procurement offices globally, compressing approval timelines and reducing contract cancellation risk. Markets respond by raising the probability-weighted value of a company's pipeline, lifting share prices even before new contracts are formally signed.

The broker consensus average price target for DroneShield sits at approximately $4.90, which is roughly 15% above the 4 May 2026 intra-session peak of $4.00, suggesting limited near-term upside from elevated post-catalyst levels according to analyst estimates cited in the article.

Key risks include expectation overextension where share prices price in contract wins before they are confirmed, insider selling signals as seen when DroneShield CEO Oleg Vornik sold shares in November 2025, and catalyst confirmation uncertainty where the full scope of an announcement may be amplified beyond confirmed operational commitments.