How to Use Dividend Yield as a Valuation Signal on the ASX

3 mins ago

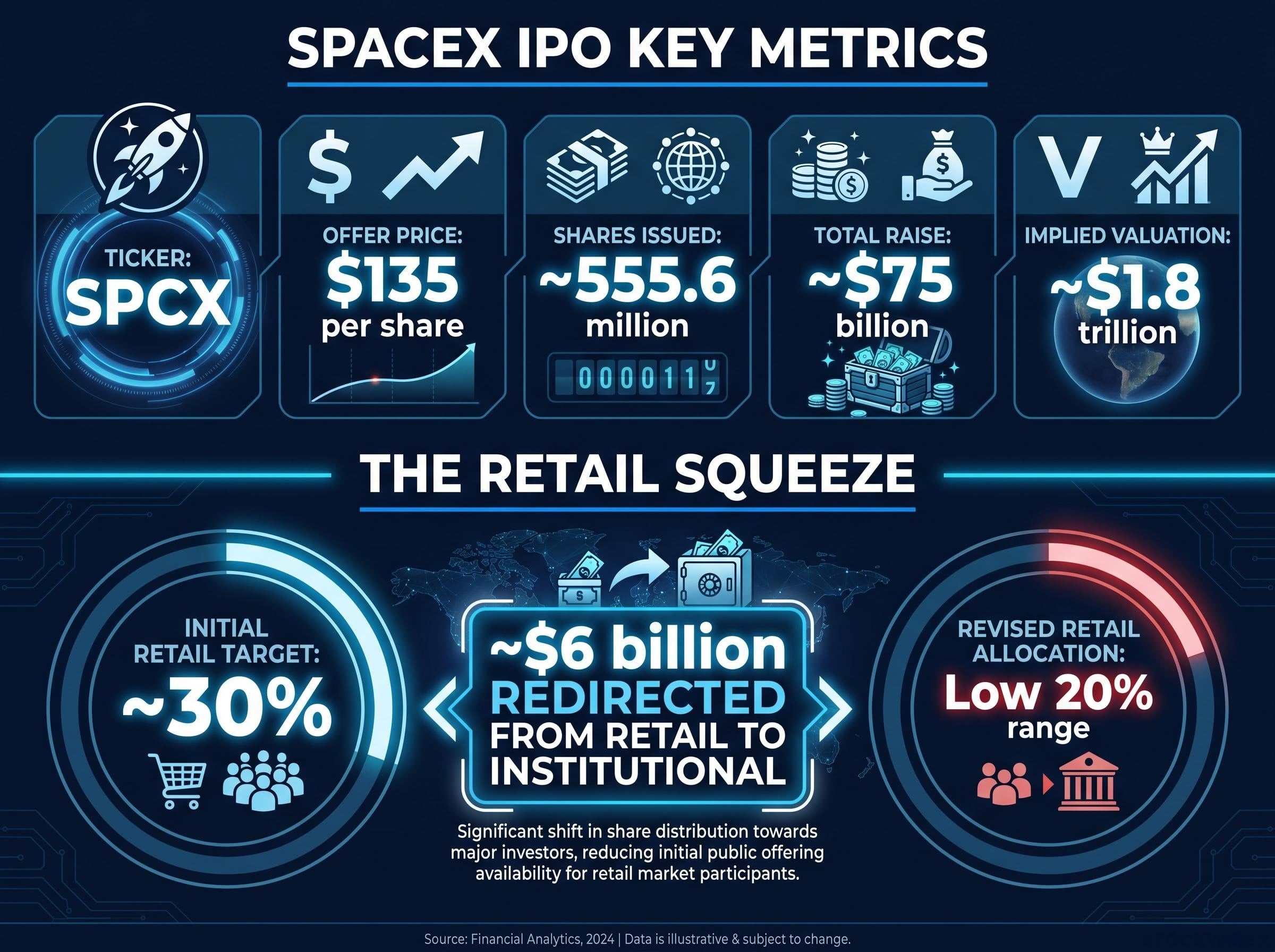

SpaceX priced its IPO at $135 per share on 11 June 2026, targeting a roughly 30% retail allocation out of a $75 billion raise. By pricing day, that figure had been revised down to the low 20% range. Billions of dollars in shares shifted from individual investors to institutional buyers, and most retail investors never saw it happen.

The SpaceX listing (ticker: SPCX) is the largest IPO raise on record and one of the most anticipated public offerings in years. It also crystallises a dynamic that plays out in nearly every major U.S. IPO: retail investors arrive with expectations shaped by headline demand figures, and leave with smaller allocations than anticipated, if they receive any shares at all. What follows unpacks why that happens, using SpaceX as a concrete case study. Readers will understand how the IPO allocation process works from bookbuilding through brokerage distribution, why institutional demand structurally crowds out retail participation, and what practical options exist for individual investors navigating high-demand listings.

The numbers were staggering. SpaceX issued approximately 555.6 million shares at $135 each, raising roughly $75 billion and implying a valuation of approximately $1.8 trillion. The offering was listed on both the Nasdaq Global Select Market and Nasdaq Texas under the ticker SPCX, with trading debuting on 12 June 2026. A nine-bank underwriting syndicate, led by Goldman Sachs, Morgan Stanley, Bank of America, and JPMorgan, and including Barclays, Deutsche Bank, RBC, UBS, and Wells Fargo, managed the process.

Early expectations placed the retail investor allocation at approximately 30% of the total raise. That starting point was already generous by historical standards; the typical U.S. IPO runs roughly 90/10 in favour of institutions. By the time pricing was finalised, the retail share had been revised to the low 20% range, according to CNBC, citing an anonymous source.

“The difference between a 30% and a 22% retail allocation on a $75 billion raise is approximately $6 billion in shares redirected from individual investors to institutional buyers at the IPO price.”

That $6 billion did not vanish. It moved to institutional investors at the offering price, while the retail investors who lost those shares were left to buy on the open market at whatever price the stock cleared on day one.

The structural bias exposed in the SpaceX deal is not unique to a single listing; IPO mechanics for retail investors have consistently favoured insiders across the full history of the U.S. public markets, with the bookbuild process, lockup structure, and secondary market dynamics each compounding the disadvantage before a retail buyer places a single order.

| Detail | SpaceX IPO |

|---|---|

| Pricing date | ~11 June 2026 |

| Ticker | SPCX |

| Listing venues | Nasdaq Global Select Market; Nasdaq Texas |

| Offer price | $135 per share |

| Total raise | ~$75 billion |

| Implied valuation | ~$1.8 trillion |

| Initial retail allocation target | ~30% |

| Revised retail allocation | Low 20% range |

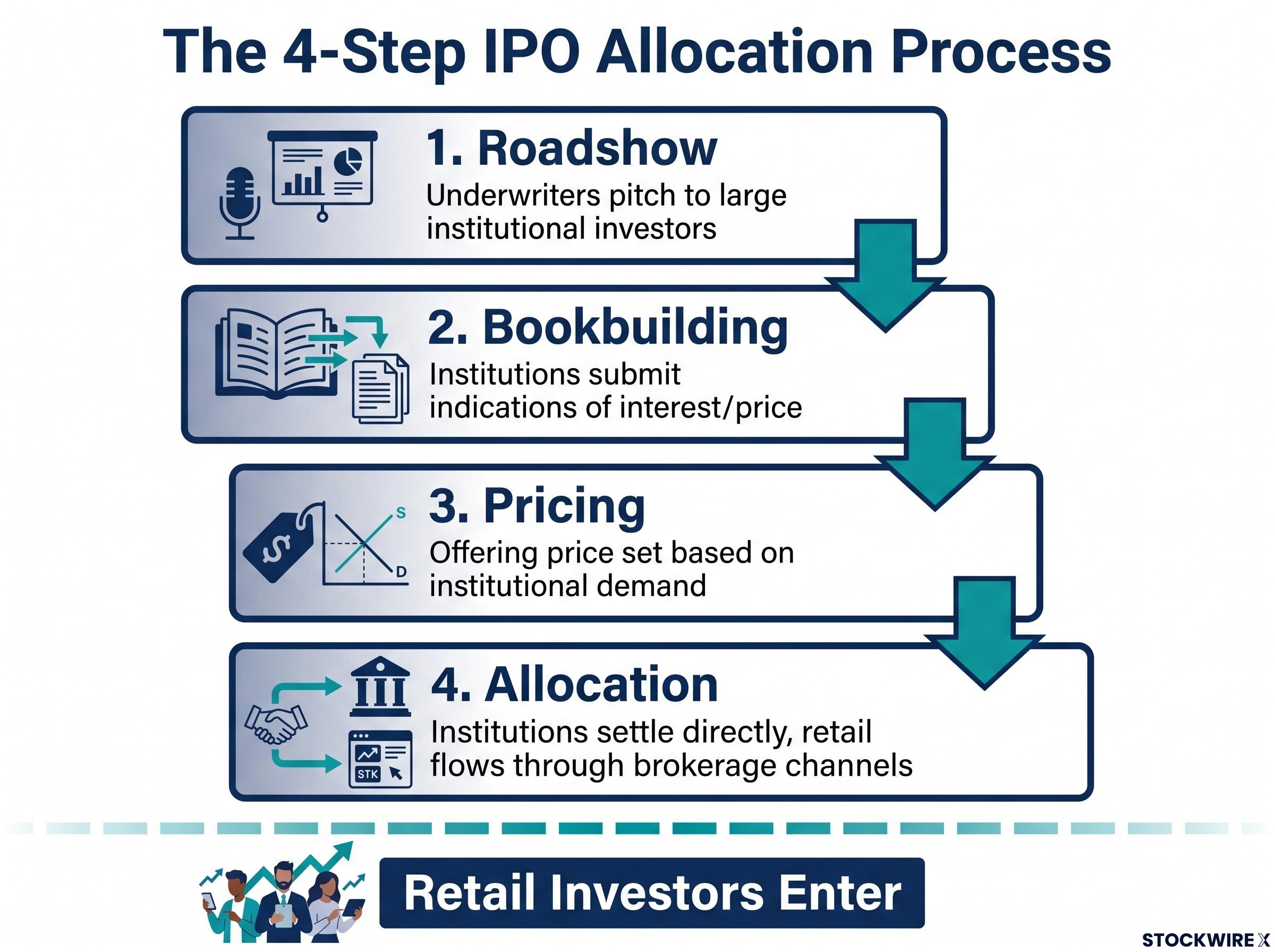

Most retail investors encounter an IPO only through a notification on their brokerage app. The entire upstream process, the one that determines how many shares they will be offered and at what price, is already complete by that point.

The sequence unfolds in four steps:

The SpaceX syndicate of nine banks managed this process for a $75 billion deal. The scale of the institutional infrastructure involved, hundreds of fund meetings, thousands of price-conditional bids aggregated across a global investor base, illustrates why the system centres on institutional capital. Retail demand, arriving later and without differentiated pricing signals, enters a process that has already been shaped by the institutional book.

The indicative retail/institutional split established early in a deal is not a contractual commitment. According to Fidelity, the retail percentage can be higher or lower on a deal-by-deal basis. The SEC, per Investor.gov, does not regulate how shares are allocated between institutions and individuals. That regulatory point matters: the compression is not a breach of rules. It is the process functioning as designed.

The retail squeeze in SpaceX was not adversarial. It was the logical outcome of three structural mechanisms that activate whenever institutional demand is high.

“The SEC does not regulate the business decision of how shares are allocated between institutions and individuals.” (Investor.gov)

The Investor.gov IPO allocation guidance confirms that the SEC does not regulate the business decision of how shares are distributed between institutions and individuals, leaving underwriters and the issuing company with full discretion over how the book is filled and who receives shares at the offering price.

The initial 30% retail target in SpaceX was already well above the historical U.S. baseline of approximately 90/10 institutional/retail. Even the revised low-20% figure remained generous by industry norms. The compression was not a malfunction; it was the system calibrating to the strength of institutional appetite.

Even after the syndicate sets a retail percentage, individual investors face a second bottleneck. Each brokerage firm receives a syndicate allocation, which may itself be small. The brokerage then distributes that slice among its eligible retail clients using its own internal criteria, and those criteria differ meaningfully by platform.

Robinhood’s IPO Access programme operates a random lottery: each eligible request has equal probability of receiving all, some, or none of the shares requested. Other brokers use pro-rata scaling, distributing shares proportionally across requests. Others prioritise by client assets and revenue. There is no standardised, industry-wide retail allocation method. The rules change by platform and by deal.

Some brokers warn explicitly that their syndicate allotment may be very small, limiting what they can offer individual clients regardless of demand. The practical result is that two investors requesting the same number of shares on different platforms can receive completely different outcomes.

Before any general retail allocation takes place, a portion of many IPO offerings is carved out through directed share programmes (DSPs), which are shares set aside for employees, customers, or associates of the company. This slice is removed before either institutional or general retail receives anything, further reducing what remains for ordinary retail investors.

| Channel | Allocation method | Relationship priority |

|---|---|---|

| Mass-market broker | Lottery or pro-rata; small syndicate slice | None |

| Private bank / wealth management | Direct syndicate relationship; client priority | High (revenue-ranked) |

| Directed share programme | Reserved pre-allocation | Limited to employees/customers/associates |

Private bank and wealth management clients occupy a structurally different position. Rather than competing in a mass-market broker pool, they access IPO shares through their institution’s direct relationship with the underwriting syndicate, bypassing the general retail queue entirely.

Investors who receive an IPO allocation pay the offering price. In the SpaceX case, that was $135 per share. Investors who miss the allocation and want shares must buy on the open market once trading begins on 12 June 2026, paying whatever the market clears.

The two experiences diverge sharply:

“Strong institutional oversubscription signals institutional appetite at the offering price. It does not guarantee that open-market prices will remain elevated after day one.”

The valuation premium baked into marquee listings like SpaceX is a separate risk layer from allocation mechanics: prediction markets at the time of filing implied a debut market cap above $2 trillion, well above the $1.5-1.75 trillion analyst consensus, a gap that means sentiment alone could account for a substantial portion of the day-one open price retail buyers would pay.

Initial trading days for high-profile IPOs can be highly volatile. Some heavily oversubscribed IPOs have declined sharply in early trading despite strong institutional demand. Open-market buyers bear the full weight of that volatility.

Lockup periods, which typically run 90-180 days post-IPO according to **E\*TRADE** guidance, also shape the aftermarket picture. When lockup periods expire, a significant volume of shares held by insiders and early investors becomes eligible for sale, creating a defined supply event. For retail investors who missed the IPO, lockup expirations can represent a potential secondary entry point at prices that may be more stable than day-one peaks.

The historical 90/10 institutional/retail baseline means most retail investors have always been open-market buyers for major IPOs. This is the norm, not the exception.

Understanding the system’s mechanics does not eliminate the structural disadvantage, but it does create specific, actionable choices. Several levers are genuinely within an individual investor’s control.

Long-term IPO underperformance compounds the day-one entry price risk for open-market buyers: newly listed companies have underperformed comparably sized established peers by an average of 3.3% per year over their first five years, a structural drag that turns a seemingly moderate annual shortfall into a materially worse outcome relative to simply buying index exposure instead.

The standard underwritten bookbuild is not the only path to a public listing. Two alternatives meaningfully alter the retail access dynamic.

Direct listings, used by Spotify and Slack, involve no bookbuilding and no preferential allocation. All investors, retail and institutional, trade from day one on an open order book. The trade-off is the absence of underwriter price stabilisation, meaning greater volatility at the open.

Dutch auction IPOs, such as Google’s 2004 offering, allow retail investors to submit competitive bids and receive shares at the market-clearing price, reducing the informational advantage that institutions hold during bookbuilding.

Neither format has displaced the standard underwritten bookbuild as the dominant U.S. IPO mechanism, but both represent meaningful departures from the allocation dynamics described throughout this article.

The retail compression in SpaceX was not a malfunction. It was the disclosed, legal outcome of a system built around institutional capital, operating exactly as its participants, regulators, and disclosed policies describe. The SEC does not regulate allocation decisions. Underwriters prioritise the clients that anchor their books. Brokerages distribute their small syndicate slices using methods that vary by platform and by deal.

Understanding this does not eliminate the disadvantage. It does eliminate the false expectations that cause the most costly retail mistakes: overpaying on day one because demand felt like a guarantee, or assuming misconduct where disclosed market structure is the actual explanation. Investors who understand IPO mechanics can make better decisions about when to pursue allocation, when to wait for the secondary market, and how to read the structural signals correctly.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The IPO allocation process is the sequence by which shares in a newly listed company are distributed to investors, starting with a roadshow and bookbuilding phase open only to large institutions, then a pricing decision made the night before trading, and finally a distribution of shares that flows to retail investors only through brokerage syndicate allotments after institutional buyers have already been served.

Retail investors receive smaller IPO allocations because underwriters prioritise institutional clients who submit price-conditional bids during bookbuilding, generate more revenue, and can absorb large blocks of shares; when institutional demand is strong enough to oversubscribe a deal many times over, underwriters have full discretion to reduce the retail portion, as happened with SpaceX where the retail allocation was revised down from roughly 30% to the low 20% range.

SpaceX priced its IPO at $135 per share on 11 June 2026, raising roughly $75 billion, and the revision of the retail allocation from approximately 30% to the low 20% range redirected an estimated $6 billion in shares from individual investors to institutional buyers at the offering price, leaving retail investors who missed out to purchase on the open market at whatever price the stock cleared on day one.

Not all retail brokers receive syndicate allocations for IPOs; platforms like Robinhood use a random lottery through their IPO Access programme, while other brokers use pro-rata scaling or client asset rankings, meaning platform choice materially affects an investor's odds of receiving shares at the offering price.

Retail investors who miss an IPO allocation can monitor lockup expiration dates, typically 90-180 days after the listing, as a potential secondary entry point when insider share sales may create more stable or lower prices than the often volatile day-one open market.