ASIC has identified revenue recognition, asset impairment, and financial instrument measurement as its judgment-intensive focus areas for financial reporting scrutiny in FY2026-27. These three accounting domains share a common trait: each relies heavily on preparer assumptions, making them the areas of financial statements most susceptible to optimistic estimates and management bias. The regulator’s annual surveillance programme shapes how auditors select files, how preparers defend their estimates, and how investors should weigh the disclosures they encounter in annual reports. For listed companies and sophisticated investors reading financial statements, understanding ASIC’s financial reporting priorities is functionally equivalent to understanding where reporting risk concentrates. What follows decodes the FY2026-27 programme, explains the mechanics of audit surveillance, maps the enforcement actions already underway, and draws out the practical implications for investors interpreting disclosures and for preparers managing regulatory exposure.

The three accounting areas drawing ASIC’s sharpest scrutiny

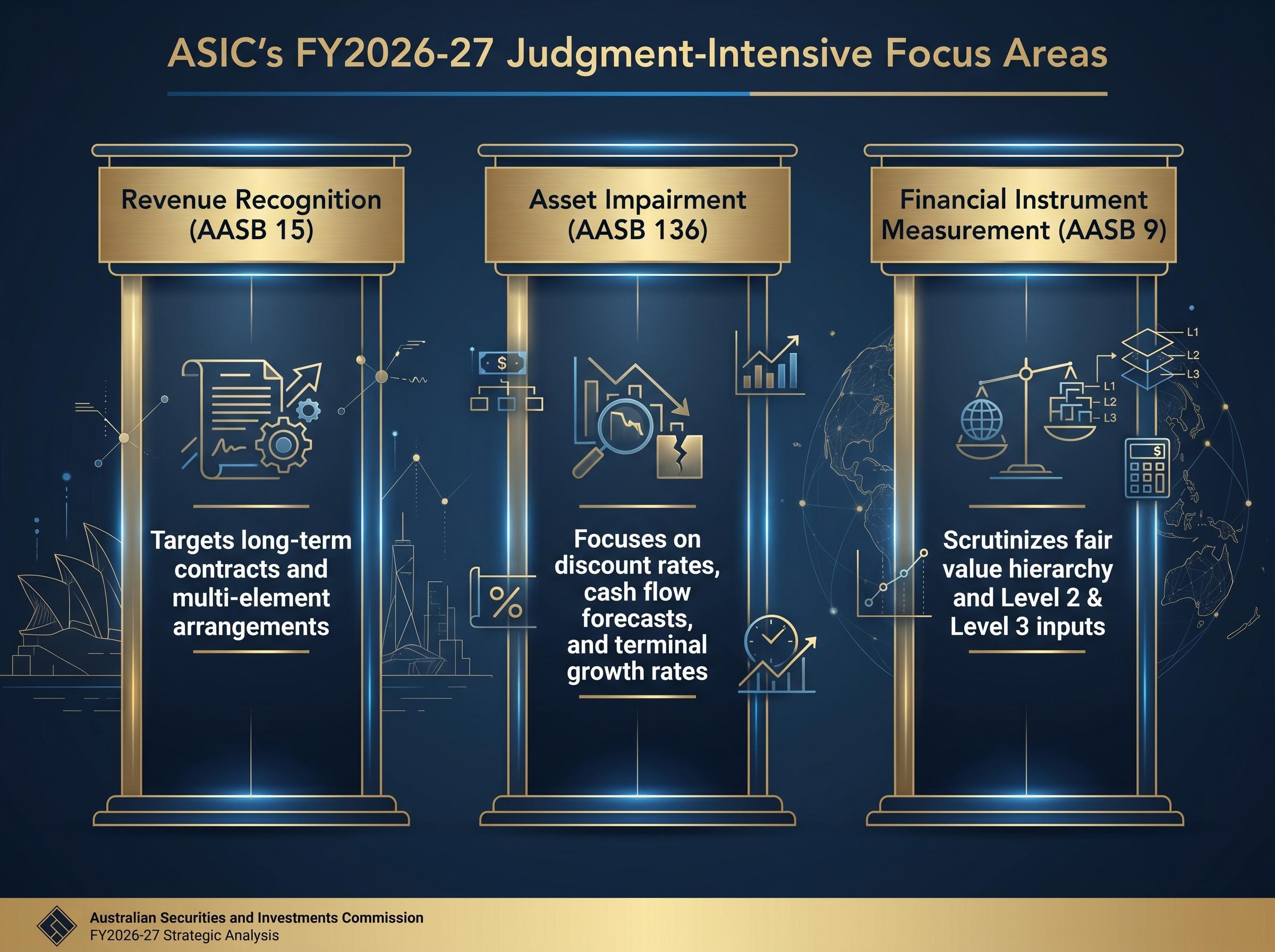

The selection of revenue recognition, asset impairment, and financial instrument measurement as ASIC’s core scrutiny areas for FY2026-27 reflects a deliberate regulatory judgment. All three sit at the intersection of accounting complexity and preparer discretion, the point where management assumptions, rather than observable data, determine reported outcomes.

ASIC Commissioner Kate O’Rourke has attributed these three areas as the FY2026-27 focus, building on findings documented in ASIC Report 819 (31 October 2025), which addressed FY2024-25 reporting and audit quality across listed and unlisted companies, registrable superannuation entities, and managed investment schemes.

Each area carries its own specific risk logic:

- Revenue recognition scrutiny targets the timing and amount of recognised revenue, particularly in long-term contracts or multi-element arrangements where management assumptions about performance obligations drive reported outcomes.

- Asset impairment scrutiny focuses on the assumptions underlying recoverable amount calculations, including discount rates, cash flow forecasts, and terminal growth rates, where small changes in inputs produce large changes in carrying values.

- Financial instrument measurement scrutiny covers fair value hierarchy classifications and the reasonableness of Level 2 and Level 3 inputs, where instruments are valued using models rather than quoted market prices.

The common thread is that each area requires preparers to exercise judgment that cannot be mechanically verified. ASIC’s programme tests whether those judgments are reasonable, evidenced, and consistently applied, or whether they serve to obscure deteriorating fundamentals behind optimistic assumptions.

When big ASX news breaks, our subscribers know first

Why judgment-intensive accounting is where reporting risk concentrates

Not all accounting standards carry the same level of reporting risk. Some are mechanical: a rule produces a fixed outcome, and preparer discretion is minimal. Others are judgment-intensive, requiring forward-looking estimates that depend on assumptions about the future, assumptions that cannot be verified against observable market prices at the time they are made.

The three standards underpinning ASIC’s current focus illustrate this distinction:

- AASB 15 (Revenue from Contracts with Customers) requires preparers to identify performance obligations, allocate transaction prices, and determine when revenue is recognised over time or at a point in time; each step involves estimates about contract completion and variable consideration.

- AASB 136 (Impairment of Assets) requires preparers to estimate the recoverable amount of assets using discounted cash flow models, where the choice of discount rate, forecast period, and terminal growth rate can shift the outcome by tens of millions of dollars.

- AASB 9 (Financial Instruments) requires fair value measurement where Level 2 and Level 3 inputs rely on unobservable or partially observable data, making the resulting valuations difficult for external readers to independently verify.

ASIC’s surveillance programme exists precisely to test whether the assumptions disclosed under these standards are reasonable, supported by evidence, and applied consistently across reporting periods. The regulator’s stated programme objective is promoting high-quality, consistent, and comparable financial information to underpin informed investor decision-making and market integrity.

SSRN research on managerial opportunism in asset impairment provides empirical evidence that preparers systematically delay recognition of impairment losses and apply upwardly biased discount rate and cash flow assumptions, the precise behaviours ASIC’s surveillance programme is designed to detect and deter.

Decommissioning provisions: a targeted review within the broader programme

ASIC has also flagged a dedicated review of entities carrying decommissioning and site-restoration cost provisions. The assessment will be conducted against illustrative example D of AASB 137 (Provisions, Contingent Liabilities and Contingent Assets), making this a compliance test against specific guidance rather than a general quality review.

This is particularly relevant to resources sector entities carrying significant rehabilitation liabilities, where the gap between provision estimates and actual future costs has historically attracted regulatory attention.

How the audit surveillance programme reinforces financial reporting quality

ASIC’s audit surveillance programme operates as more than a periodic review exercise. It functions as an accountability system with defined selection criteria, escalation pathways, and, beginning in FY2026-27, a public remediation-tracking mechanism.

The regulator plans to review 25 audit files in FY2026-27, with selection drawn from three streams:

- Material corrections or suspected misstatements identified through ASIC’s financial reporting surveillance or external referrals.

- Intelligence indicating audit quality risks, including independence concerns flagged through ASIC’s monitoring or market intelligence.

- Random sampling to maintain baseline coverage across the audit population.

| Selection Stream | What It Targets |

|---|---|

| Material corrections / suspected misstatements | Entities where financial reporting errors or potential misstatements have been identified through ASIC surveillance or referrals |

| Quality intelligence / independence concerns | Audit engagements where ASIC has received information suggesting audit quality or auditor independence risks |

| Random sampling | Audit files selected randomly to maintain baseline quality coverage across the broader population |

| Remediation tracking (new in FY2026-27) | Audit firms’ actual implementation of remedial measures committed following prior-cycle findings, publicly reported for the first time |

FY2026-27 marks the first cycle in which ASIC will track and publicly report on audit firms’ actual implementation of remedial measures committed following prior findings. This adds an accountability dimension absent from previous cycles. ASIC is also engaging separately with the six largest audit firms regarding firm-wide responses to Report 817 (7 October 2025) findings on auditor independence and conflicts of interest.

Managed investment schemes have been added to the audit file review scope for FY2026-27, expanding coverage beyond the existing population of listed and unlisted companies and registrable superannuation entities.

Enforcement against non-lodgers signals market integrity expectations

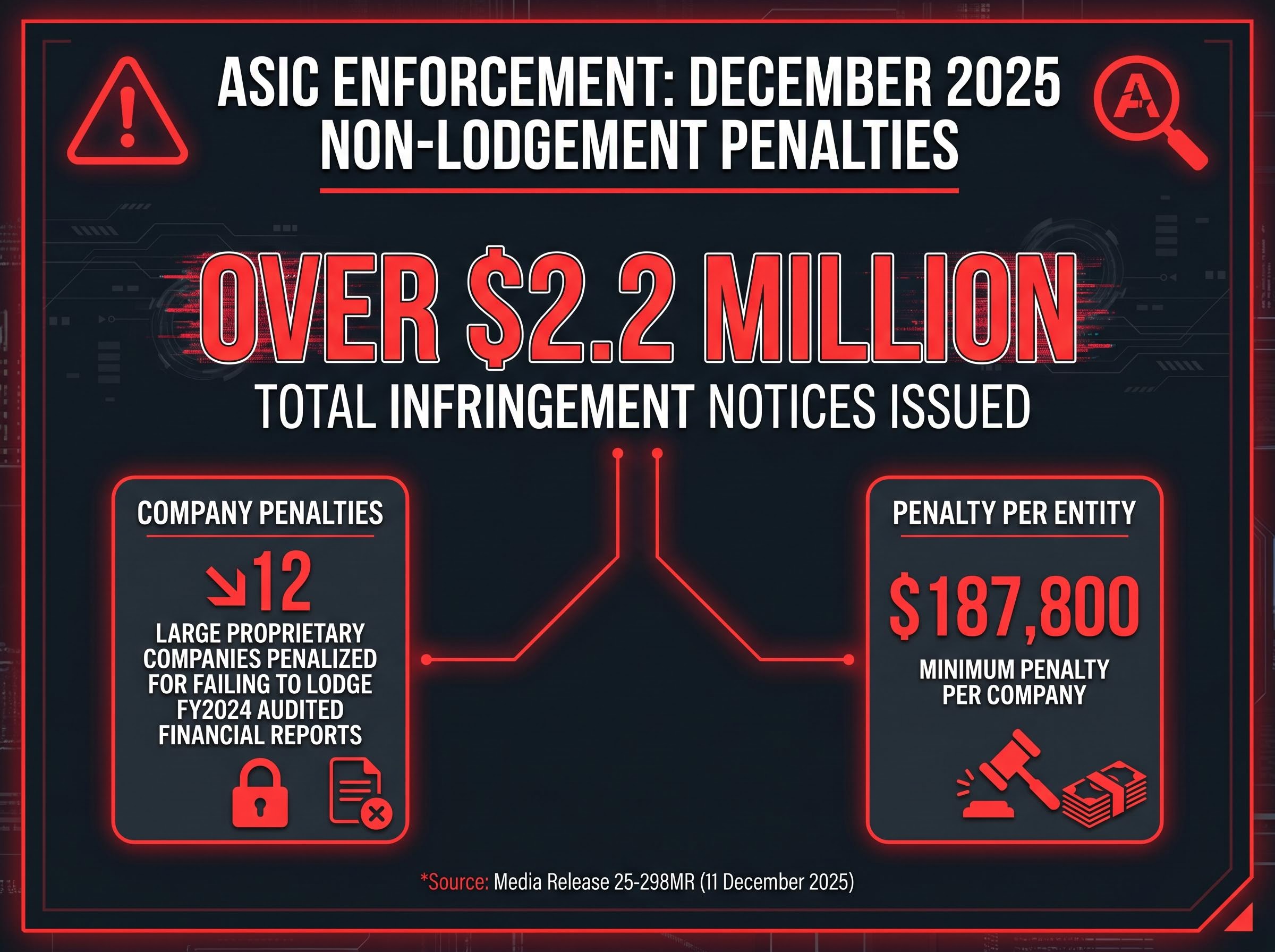

In December 2025, ASIC issued infringement notices totalling over $2.2 million to 12 large proprietary companies for alleged failure to lodge FY2024 audited financial reports.

All 12 companies paid their respective notices, with a minimum penalty of $187,800 per company under Corporations Act lodgement obligations. The fact that all notices were paid without contested proceedings indicates the penalties were sufficient to compel compliance at the first stage of enforcement.

The enforcement action, detailed in Media Release 25-298MR (11 December 2025), sits within a broader policy framework:

- Media Release 25-273MR (November 2025) classified financial reporting misconduct, including non-lodgement, as an active 2026 enforcement priority.

- ASIC’s Key Issues Outlook 2026 (January 2026) reinforced non-lodgement and poor-quality reporting as ongoing surveillance targets for large proprietary companies.

The pattern is instructive. ASIC is not treating non-lodgement as a technical compliance gap to be remedied through guidance alone. The escalation from published priorities to financial penalties within a single quarter signals a regulatory posture that treats disclosure compliance as a non-negotiable baseline for market participation.

Sustainability reporting oversight adds a new compliance dimension for FY2026-27

Australia’s mandatory sustainability reporting regime requires Group 1 entities to report for periods beginning on or after 1 January 2025, making FY2026-27 the first full operational cycle for the largest reporting entities. This is genuinely new regulatory territory, not an extension of existing financial reporting obligations but a parallel compliance framework with its own standards, assurance requirements, and regulatory oversight.

ASIC has taken an active administrative posture in preparation. Support measures implemented to date include:

- Publication of FAQs addressing stakeholder queries on reporting obligations

- Issuance of relief provisions for specific compliance challenges

- Revised guidance in response to practical implementation questions

- A publicly maintained relief register, with individual relief decisions being progressively added

ASIC has indicated that preliminary observations on lodged sustainability reports will be released shortly, targeted at assisting entities with 30 June reporting dates preparing to submit sustainability reports for the first time. The regulator has also engaged with major audit firms on assurance approaches to sustainability reports.

The practical complexity of mandatory sustainability reporting becomes visible at the entity level: Santos carries a Scope 3 footprint representing more than 75% of its total emissions with no binding net-zero commitment, a disclosure gap that will face limited assurance requirements as Australia’s climate reporting regime moves into year two.

Reform consultation does not reduce current compliance obligations

The Australian Government’s Budget announcement flagged a proposed consultation on reforms to reduce sustainability reporting burden while preserving core requirements. However, this consultation does not suspend or modify current lodgement obligations for Group 1 entities.

ASIC has explicitly stated it will continue administering the mandatory climate reporting framework regardless of forthcoming reforms. Preparers cannot treat reform uncertainty as a reason to defer compliance work; the current obligations remain in full effect.

The next major ASX story will hit our subscribers first

What the 2026-27 priorities mean for investors reading financial reports

ASIC’s surveillance priorities function as a map of where financial statement risk is most likely to be obscured by optimistic assumptions. Investors who align their financial report reading with these priorities are stress-testing disclosures against the same criteria the regulator applies, a materially more rigorous approach than accepting management assumptions at face value.

The practical application is straightforward. When reading annual reports, investors should direct attention to the notes most exposed to preparer judgment:

- Check revenue recognition policies for timing assumptions, particularly in entities with long-term contracts or multi-element arrangements where revenue is recognised over time.

- Examine impairment note discount rates and cash flow projections; compare these against the entity’s cost of capital and sector benchmarks to assess reasonableness.

- Assess fair value hierarchy disclosures for Level 3 inputs, which rely on unobservable data and are the most difficult to independently verify.

- Review decommissioning provision methodology for resources-exposed holdings, particularly against AASB 137 guidance.

Investors can apply a practical cross-check to the revenue recognition concerns ASIC has flagged: net income that consistently exceeds operating cash flow across multiple quarters is one of the most reliable early signals of aggressive revenue recognition, a divergence that is visible in the cash flow statement but invisible in headline earnings numbers.

Questions investors should ask when reading the key focus areas

For revenue recognition: Does the entity disclose the specific performance obligations driving revenue timing? Have recognition policies changed from the prior period, and if so, what is the quantified impact?

For asset impairment: What discount rate has been applied in the recoverable amount calculation, and how does it compare to the entity’s weighted average cost of capital? Are cash flow projections consistent with the entity’s published guidance?

For financial instruments: What proportion of the portfolio is classified at Level 3 in the fair value hierarchy? Does the entity disclose the sensitivity of Level 3 valuations to changes in key inputs?

Report 819 (31 October 2025) provides prior-cycle findings that investors can use to contextualise the quality of current reporting across reviewed entities.

Australia’s reporting integrity framework is tightening, not stabilising

The FY2026-27 priorities are not a static checklist. They represent another step in a multi-year directional tightening of Australia’s financial reporting oversight: expanding surveillance scope (managed investment schemes added), increasing accountability mechanisms (public remediation tracking introduced for the first time), escalating enforcement (infringement notices totalling over $2.2 million in a single action), and adding entirely new regulatory layers (mandatory sustainability reporting).

ASIC’s engagement with the six largest audit firms on Report 817 independence findings signals that firm-level culture and governance are now within the regulator’s sightlines, not just the quality of individual audit files. Reports 816, 817, and 819 establish the prior-cycle baseline, and the Key Issues Outlook 2026 (January 2026) confirms this trajectory extends forward.

ASIC’s financial reporting programme sits within a broader regulatory architecture in which continuous disclosure obligations have also been tightened, with the Federal Court’s April 2026 ruling against Electro Optic Systems establishing that the disclosure obligation attaches at the point of internal awareness, not at the point of formal board sign-off.

ASIC’s stated programme objective is to foster reliable financial disclosure that underpins market integrity and informed investor decision-making.

Both preparers and investors should treat the annual surveillance priorities not as a compliance checklist to satisfy minimally but as a leading indicator of where financial statement quality is most likely to deteriorate and where regulatory intervention is most probable. The direction of travel is clear: more scrutiny, broader scope, and stronger enforcement consequences for those who fall short.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding ASIC’s planned activities are based on published regulatory documents and are subject to change.