Why ThaiBev’s RTD Spirits Bet Is a Tax Play, Not a Trend Chase

1 hr ago

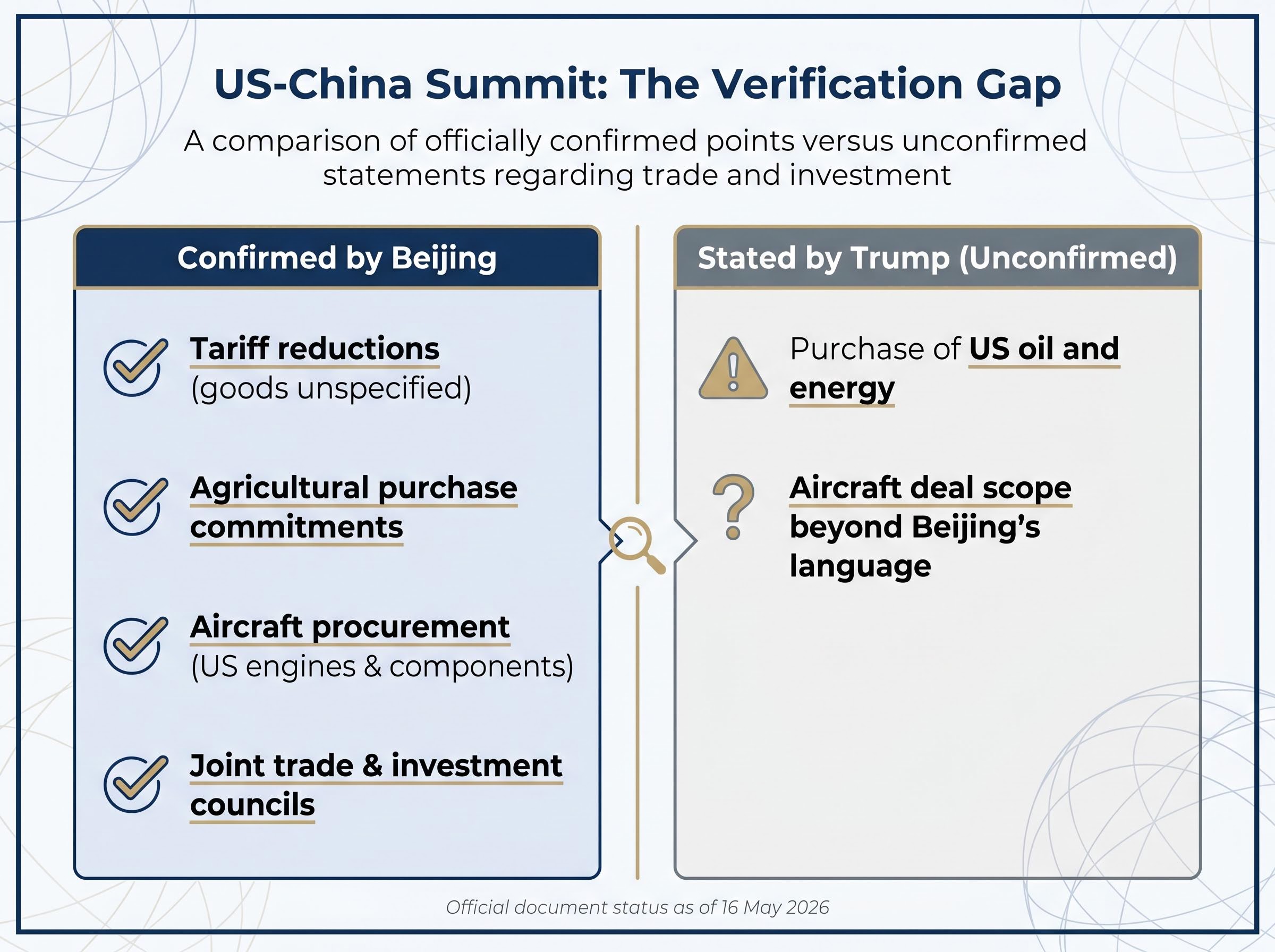

The two largest economies emerged from a Beijing summit this week with something they have not had in years: a shared statement of intent to lower trade barriers. The US-China trade deal headlines, however, obscure a significant gap between what was announced and what has actually been confirmed. The meeting between President Trump and President Xi on 14-15 May 2026 concluded with China’s Commerce Ministry confirming preliminary consensus on tariff reductions, agricultural purchases, aircraft procurement, and the creation of joint trade and investment councils. President Trump, in post-summit remarks, made additional claims, including Chinese commitments to buy US oil, that Beijing has not corroborated. For investors, the distance between verbal commitment and verified agreement matters enormously. What follows is a breakdown of every confirmed outcome, what remains unverified, and what each development means for markets and supply chains in practical terms.

The only official document available as of 16 May 2026 is China’s Commerce Ministry statement, released the same day. No joint communiqué, no formal tariff schedule, and no implementation timeline has been published by either government. The US Trade Representative’s office has issued no press release tied to the summit. The White House has released no trade fact sheet.

Beijing’s Commerce Ministry characterised the outcomes as a “preliminary consensus,” with negotiating teams from both nations working to finalise details.

That framing is deliberate. A preliminary consensus is not an agreement. It signals direction without locking in commitments.

The Beijing summit did not materialise in a vacuum. Pre-summit market positioning had already driven the Shanghai Composite to its highest close since July 2015 on 13 May, with gains priced entirely into anticipation rather than confirmed outcomes, creating the asymmetric reversal risk that now shapes how investors should read the verification gap.

| Confirmed by Beijing’s official statement | Stated by Trump / not confirmed by Beijing |

|---|---|

| Preliminary consensus on tariff reductions (goods unspecified) | Chinese commitment to purchase US oil and energy |

| Agricultural purchase commitments with reciprocal duty reductions | Scope of aircraft deal beyond Beijing’s confirmed language |

| Aircraft procurement deal including US engine and component supply | |

| Establishment of joint trade and investment councils |

The verification gap is not a minor editorial distinction. Investors who price in Trump’s characterisation without waiting for Beijing’s confirmation risk positioning for outcomes that may not materialise.

Beijing’s statement confirms a preliminary consensus on reducing tariffs across a bilateral scope. That is where the specifics end.

The commitment is directional. It confirms both sides discussed tariff relief and agreed in principle that some reduction should happen. What goods, by how much, and when remain open questions.

The agricultural pillar carries more detail than the tariff commitment, though significant gaps remain.

Trump’s separate characterisation of farm purchase volumes has not been corroborated by any Chinese government source. The oil purchase claim sits entirely outside Beijing’s confirmed language.

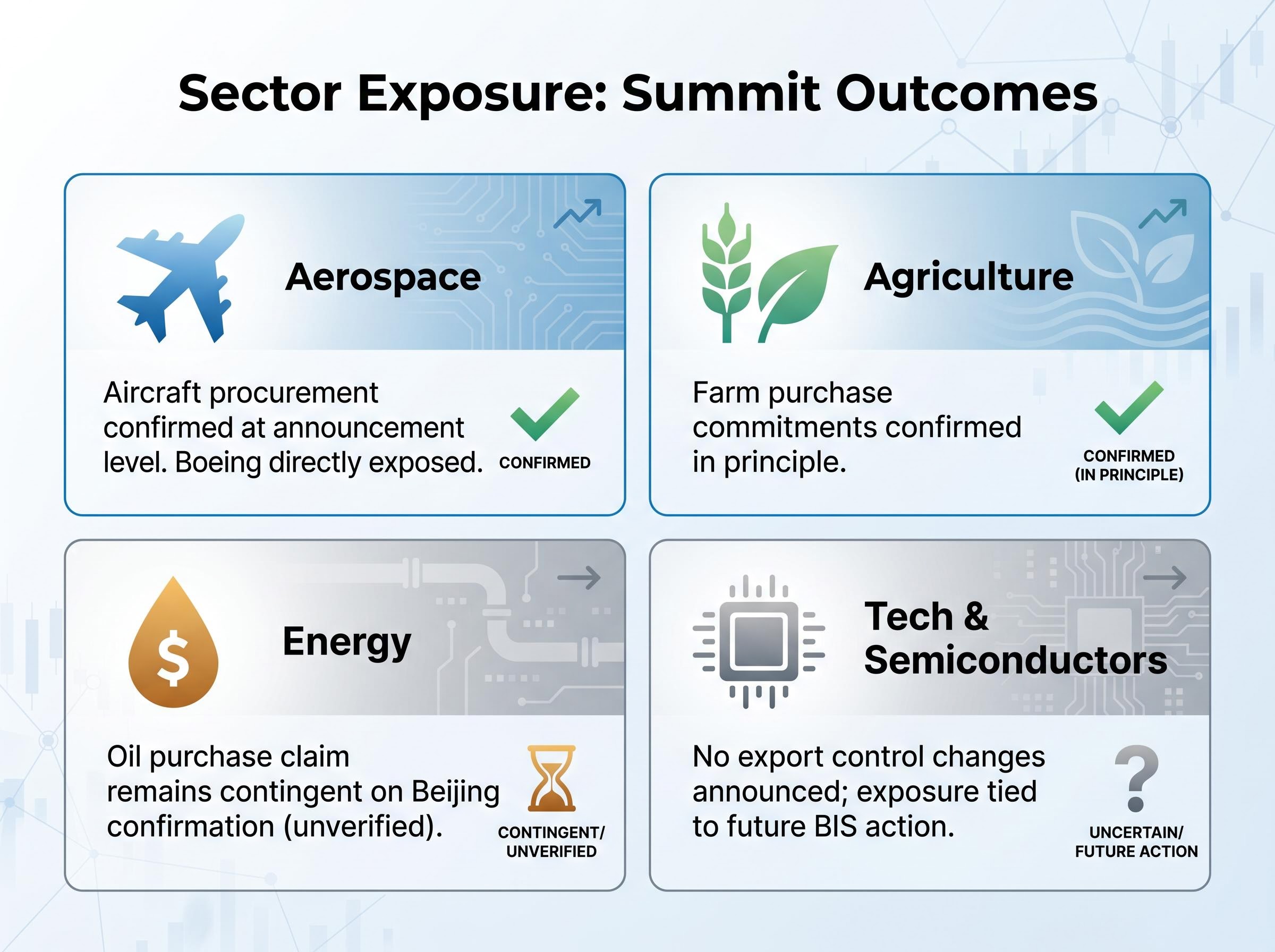

The aircraft deal is a two-way commitment: China agreed to procure US-manufactured planes, and the United States agreed to supply engines and components for those aircraft.

For aerospace investors, the confirmed language supports the thesis that China is willing to resume large-scale Boeing purchases. The precise commercial terms, however, remain unverified.

The creation of joint trade and investment councils received less market attention than the tariff and purchase commitments. It may prove the more significant outcome.

Standing bilateral councils are designed to create permanent channels for ongoing negotiation, replacing the pattern of intermittent summits followed by long silences. If properly constituted, they would represent the first durable institutional mechanism for managing US-China trade friction since the relationship deteriorated sharply through 2025.

The 2019-2020 Phase One deal offers a direct comparison: it included large purchase commitments without an enforcement or dialogue infrastructure. China fell substantially short of its purchase targets, and neither side had a standing mechanism to address the gap.

That history is why the council announcement matters. Purchase commitments without institutional follow-through have already failed once.

PIIE analysis of Phase One purchase shortfalls found that China purchased only 58 percent of the US exports it had committed to under that agreement, a concrete figure that illustrates precisely the implementation risk now attached to the Beijing summit’s agricultural and energy purchase language.

The specific details that remain unknown:

Until these are confirmed, the councils exist as a concept rather than an institution.

The two economies are deeply intertwined by trade flows, supply chains, and capital markets, yet politically adversarial on technology, security, and regional influence. That tension means trade announcements frequently serve domestic political purposes as much as they reflect implementable agreements.

The 2025 backdrop matters. Reporting from multiple outlets describes the period as one of intense trade conflict, with tariff escalations, retaliatory measures, and a sharp deterioration in bilateral relations. The Beijing summit represents a de-escalation signal, a willingness by both sides to return to the table. That signal is real even without a formal deal attached to it.

Several structural friction points survived the summit unchanged:

AI chip export controls illustrate precisely why the summit’s silence on semiconductor policy matters: the BIS approved H200 sales to approximately ten Chinese firms during the summit period, but Beijing’s independent customs block has prevented any commercial shipments from completing, meaning the controlling barrier now sits in Beijing rather than Washington regardless of diplomatic optics.

None of these friction points had a resolution pathway announced at the summit. For investors with exposure to semiconductor names or Taiwan-sensitive supply chains, the status quo on these issues is unchanged.

The summit produced directional signals. Converting them into investable convictions requires watching for specific follow-through documents and regulatory actions.

Key sources to monitor for confirmation of summit outcomes:

The four sectors carrying the most direct exposure, ranked by the specificity of what has been confirmed:

Separating probability distributions across summit agenda items matters enormously here: analysts at Fidelity International flagged before the summit concluded that trade purchase commitments, AI security outcomes, and energy positioning each carry fundamentally different likelihoods of materialising, and that pricing them as a single undifferentiated optimism trade is a positioning error.

Beijing’s Commerce Ministry stated that negotiating teams will work to finalise and implement outcomes “as quickly as possible,” but provided no specific timeline. Investors should treat current announcements as directional signals rather than confirmed policy.

The Beijing summit marks a genuine de-escalation between the world’s two largest economies after a period of severe trade conflict. That signal carries weight. Preliminary consensus on tariffs, sectoral purchase commitments, and institutional council creation are meaningful steps if followed through with formal agreements and implementation schedules.

The operative word remains “if.” No tariff lines have been published. No purchase volumes have been confirmed. No council has met. In US-China trade, the gap between announcement and implementation has historically been wide, and the Phase One experience is a direct reminder. The summit’s lasting significance will be determined not by what was said in Beijing this week, but by what appears in official documents over the coming weeks and months.

For investors tracking the energy sector exposure identified above, our deep-dive into the Iran oil price cascade examines the structural supply mechanics behind the unverified oil purchase claim, including why Brent has already exceeded pre-conflict analyst consensus targets, how tanker loadings have collapsed 50% week on week, and what a June-July inventory shortfall means for commodity and consumer-facing equity positioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

China's Commerce Ministry confirmed a preliminary consensus on tariff reductions, agricultural purchase commitments with reciprocal duty reductions, an aircraft procurement deal including US engine and component supply, and the creation of joint trade and investment councils. No formal tariff schedule, joint communique, or implementation timeline has been published by either government.

A preliminary consensus signals that both sides have agreed in principle on a direction, but it is not a binding agreement and does not lock in specific commitments. For investors, this distinction matters because outcomes priced into markets may not materialise if formal agreements and implementation schedules are never published.

Trump stated that China committed to purchasing US oil and energy, and made additional claims about the scope of the aircraft deal that went beyond Beijing's official language. Beijing's Commerce Ministry statement does not mention energy purchases at all, meaning those claims remain unverified.

Under the 2019-2020 Phase One deal, China purchased only 58 percent of the US exports it committed to, and neither side had a standing mechanism to address the shortfall. This history is a direct reminder that purchase commitments without institutional follow-through carry significant implementation risk.

Aerospace is most directly exposed, with Boeing reliant on Chinese aircraft orders; agriculture is positioned for upside if product lists and volumes are confirmed; energy remains contingent on Beijing verifying the oil purchase claim; and technology and semiconductors are unaffected for now, as no changes to AI chip export controls were announced.