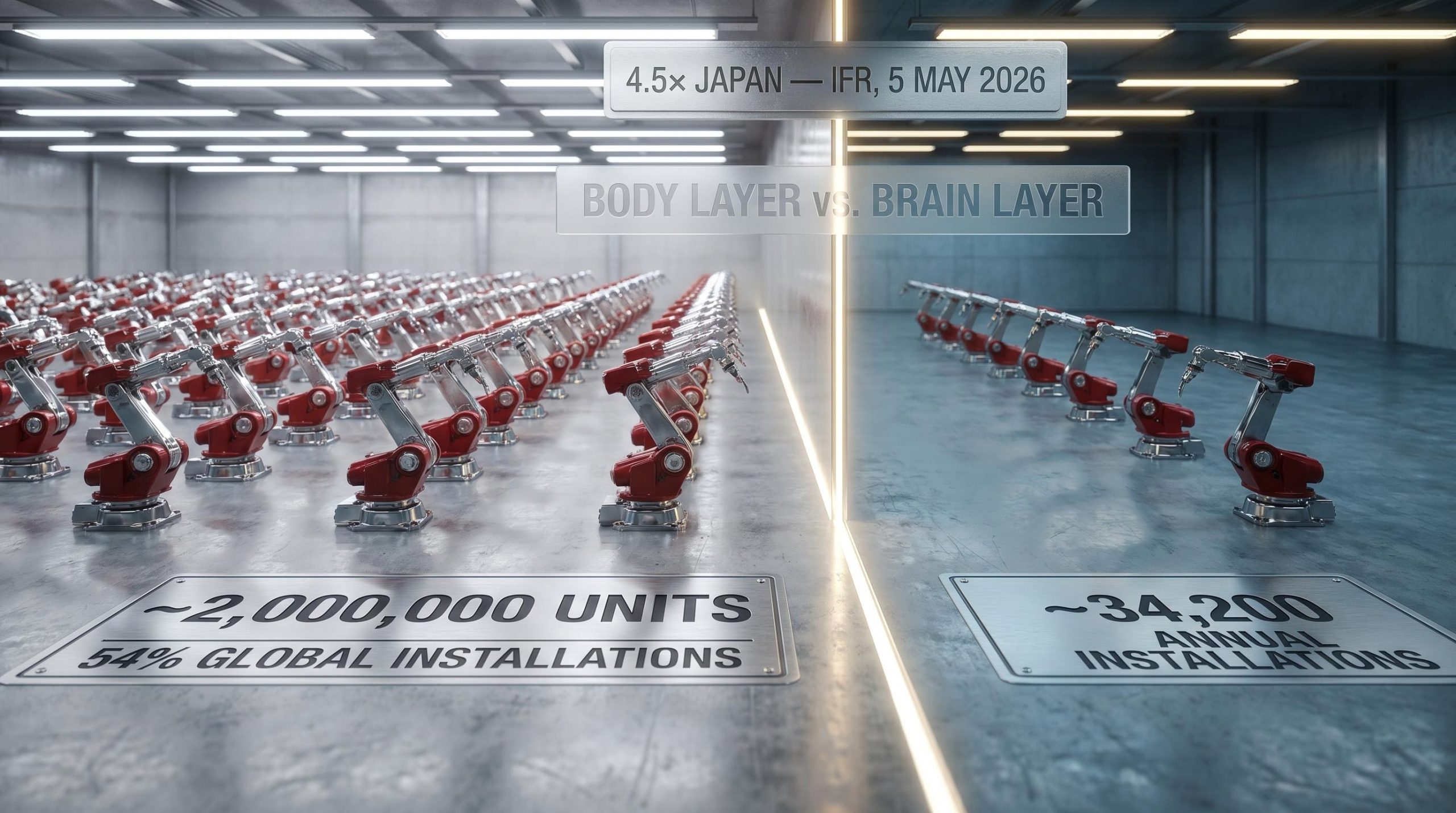

China operates approximately 2 million industrial robots in its manufacturing sector, roughly 4.5 times more than Japan, the world’s second-largest robotics nation. That single figure, published by the International Federation of Robotics (IFR) on 5 May 2026, reframes the entire debate about which superpower is winning the artificial intelligence race.

The conventional scorecard for the US-China AI competition focuses on semiconductor fabrication, large language model performance, and compute cluster scale. That scorecard misses an entire layer of the contest. An Alpine Macro report published on 12 May 2026 argues that the real battleground has shifted to what its chief geopolitical strategist Dan Alamariu calls the “body layer”: physical robot deployment density, state-funded embodied AI training infrastructure, and the manufacturing ecosystems that translate robot scale into compounding learning advantages. This analysis unpacks the structural logic behind China’s physical AI strategy, examines where the US model is genuinely exposed, and draws out the investment and geopolitical implications of a competition increasingly being won on factory floors rather than GPU clusters.

China’s deployment scale is not an incremental lead; it is a structural one

The numbers establish the gap before the mechanism needs explaining.

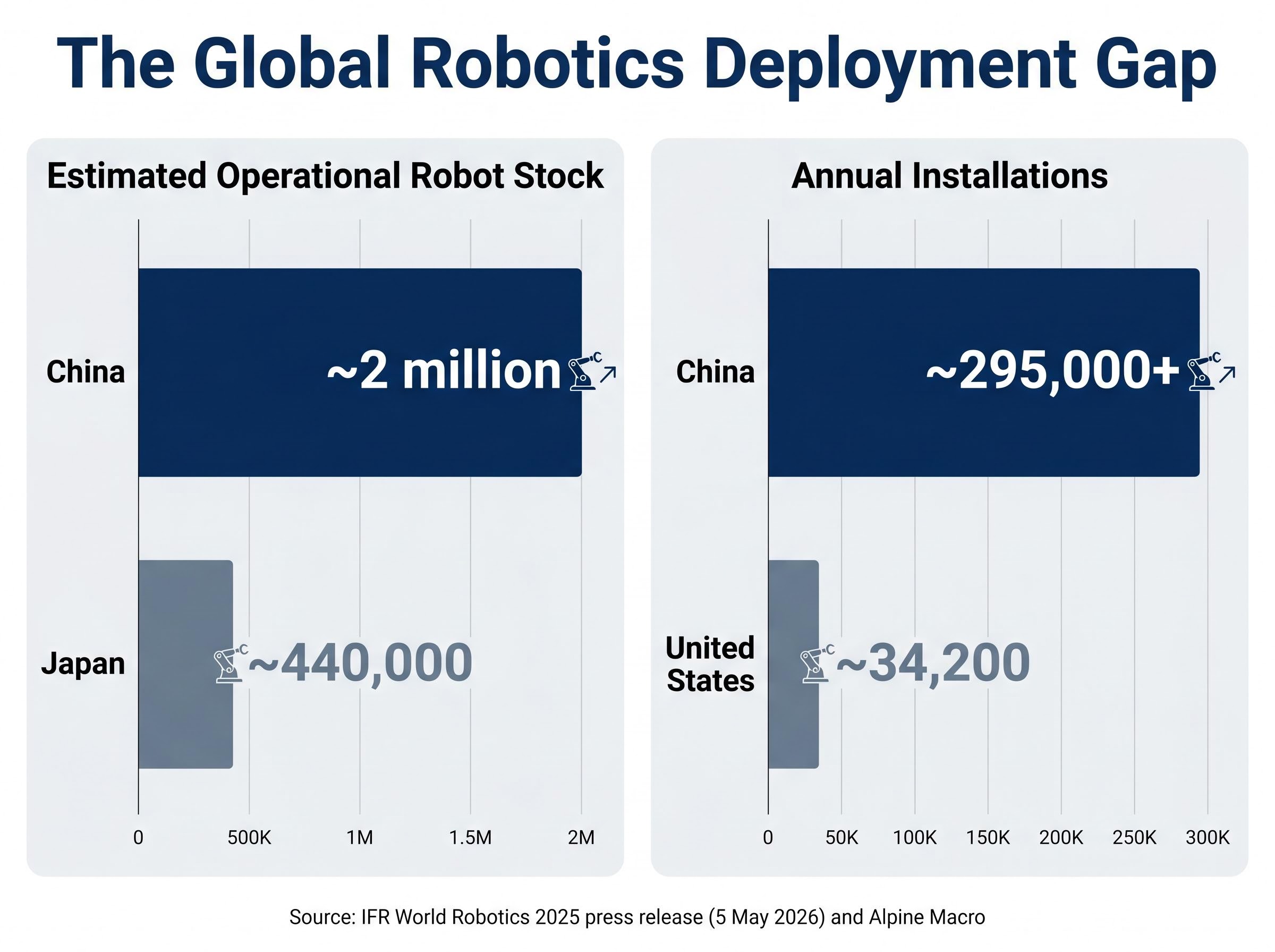

China’s operational industrial robot stock of approximately 2 million units is roughly 4.5 times Japan’s, the world’s second-largest robotics nation, according to the IFR’s May 2026 data.

| Nation | Estimated Operational Robot Stock | Annual Installation Share (Global) | Domestic Supplier Share |

|---|---|---|---|

| China | ~2 million | 54% | 57% (2024) |

| Japan | ~440,000 | N/A | N/A |

| United States | ~34,200 annual installations | N/A | N/A |

Source: IFR World Robotics 2025 press release, 5 May 2026. US figure reflects annual installations via Alpine Macro; operational stock not separately reported.

The domestic supplier trajectory sharpens the picture. Chinese robot manufacturers grew their share of domestic installations from 30% in 2020 to 57% in 2024. In the metals and machinery sector, Chinese suppliers now command 85% domestic market share. 64% of all industrial robots deployed in the global electronics industry are installed in China, with Chinese manufacturers supplying 59% of that segment.

This is not simply a deployment story. It is an industrial capability story. China is not reliant on foreign robotics OEMs to sustain its deployment pace, which insulates the trajectory from trade restrictions in ways that pure consumer electronics supply chains are not.

The connection to AI is direct. Every additional hour of real-world robot operation generates sensor data, failure modes, and corrective feedback that improves the next generation of physical AI models. China’s installed base is running that experiment at a scale no other nation can match. Global installations are forecast to surpass 700,000 units in 2028 at a compound annual growth rate of approximately 7%, according to the IFR, meaning China’s absolute installation advantage widens in unit terms even if its percentage share holds steady.

The IFR World Robotics 2025 report provides the foundational deployment figures underlying this analysis, including China’s 54% share of annual global installations, an operational stock exceeding 2 million units, and a forecast of approximately 10% average annual growth in Chinese manufacturing robotics through 2028.

When big ASX news breaks, our subscribers know first

How the AI contest splits into distinct competitive arenas, with different leaders in each

Alpine Macro’s Alamariu frames the US-China AI contest as a two-layer competition, and the distinction matters because each layer compounds differently.

The “brain layer” encompasses frontier AI software, semiconductor design, and the compute infrastructure that powers large language models. The US leads here. Its companies dominate model development, its CHIPS Act investment is reshaping domestic semiconductor manufacturing, and its simulation infrastructure (led by platforms such as NVIDIA Cosmos) remains the most advanced in the world.

The “body layer” is different. It encompasses physical robot deployment, embodied AI training facilities, and the domestic manufacturing ecosystems that supply and sustain them. China leads here, and the lead is widening.

The two layers matter on different time horizons:

- Brain layer (US-led): Advantages in model performance and chip design. These advantages are replicable through licensing, open-source diffusion, and talent migration. The compounding mechanism is intellectual, and it travels.

- Body layer (China-led): Advantages in physical deployment scale and real-world operational data accumulation. These advantages compound physically: each hour of robot operation generates sensor data and failure-mode feedback that improves the next generation of models. This compounding mechanism does not travel; it requires installed hardware running at scale.

China holds 54% of all annual global industrial robot installations, according to the IFR’s May 2026 World Robotics press release. Investors and policymakers who assess the AI race solely through the semiconductor scorecard are working with an incomplete map of the contest.

Asian hardware supply chains are capturing a disproportionate share of the physical infrastructure investment underpinning the global AI buildout: hyperscalers including Microsoft, Alphabet, Amazon, and Meta collectively forecast approximately $725 billion in 2026 AI capital expenditure, with roughly 75% directed toward hardware that flows primarily through Korean and Taiwanese manufacturers.

Why real-world robot operation produces physical AI capabilities that digital training alone cannot replicate

Understanding the mechanism behind China’s physical AI lead requires separating two types of artificial intelligence that are often conflated.

Embodied AI refers to AI systems that learn from physical interaction with the real world through sensors, actuators, and feedback loops. These systems operate in factories, warehouses, and logistics hubs, manipulating objects, navigating spaces, and adapting to unpredictable physical conditions. This is structurally different from AI trained on text, images, or synthetic simulation, which operates entirely within digital environments.

The difference matters because of how each type of data compounds:

- Deployment at scale: A large fleet of industrial robots operates across thousands of factory environments simultaneously.

- Real-world operational hours: Each robot generates continuous streams of sensor data, capturing friction, material variation, environmental interference, and equipment wear.

- Failure modes and corrective feedback: Every malfunction, miscalibration, or unexpected outcome becomes a training signal that simulation cannot fully anticipate.

- Model improvement: Aggregated operational data feeds back into improved AI models with better physical intuition.

- Next-generation deployment: Improved models are deployed to an even larger installed base, accelerating the loop.

According to the Alpine Macro report (12 May 2026), the Wuhan Hubei Humanoid Robot Innovation Center is estimated to generate approximately 100 hours of usable embodied training data per day. This figure originates from the Alpine Macro report and has not been independently verified from a public primary source.

The US approach relies more heavily on high-fidelity simulation environments, with NVIDIA Cosmos representing the leading platform. Simulation offers genuine advantages: the ability to generate large volumes of varied training scenarios without deploying physical hardware at scale. Whether simulation-derived training data produces equivalent physical AI capability to real-world operational data remains an open empirical question. No major public study has quantitatively resolved this as of mid-2026. The analytical point is that the US is betting heavily on simulation as a substitute, and that bet remains unproven in the physical AI domain.

How Beijing’s policy architecture is designed to compound the physical AI advantage

China’s 15th Five-Year Plan (2026-2030) places robotics “at the heart of China’s modern industrial system,” with AI research explicitly directed toward physical applications with robots as main drivers of economic growth, according to the IFR’s May 2026 framing. This is not a continuation of past automation policy. It is a deliberate strategic escalation.

Alamariu argues that state capitalism is a “prerequisite” for winning the physical AI race: the directed investment model enables infrastructure build-out that private markets would underfund because the returns are long-dated and diffuse.

The logic holds that state-directed investment funds specialised training facilities, pilot industrial zones, and domestic supplier subsidies at a speed and scale that market-driven allocation struggles to match. Beijing has directed “billions of dollars” into specialised development funds targeting robotics and embodied AI, according to Alpine Macro, though no itemised fund-level figures have been verified from public sources.

China’s AI investment timeline also creates an important distinction between deployment ambition and revenue realisation: overall IT budget growth has collapsed to a record-low 4.8% in 2026 even as AI’s share of those same budgets nearly doubles, a divergence that reflects capital reallocation toward physical infrastructure and compute rather than software procurement.

The cost-reduction data from Unitree Robotics offers the most investor-legible evidence that state-backed manufacturing density produces market outcomes that pure software investment does not generate.

| Period | Unit Sales | Average Unit Price (RMB) |

|---|---|---|

| 2023 (full year) | 5 | ~593,000 |

| Jan-Sep 2025 | 3,551 | ~168,000 |

Source: Alpine Macro, 12 May 2026. These figures originate from private research and have not been verified from public company filings.

That price trajectory mirrors the early electric vehicle story. Morgan Stanley’s 2024 analysis framed China’s dense manufacturing ecosystems, government support, and data accumulation as paralleling the EV and battery supply chain precedent, a model for rapid market leadership in manufacturing-intensive technology sectors. If humanoid hardware follows the same cost curve, Chinese manufacturers could commoditise robots that US and European firms currently price as premium product.

Where the US leads, and where its physical AI position is genuinely exposed

The US brain-layer lead is genuine and significant. American companies dominate frontier model development. The CHIPS Act is channelling substantial federal investment into domestic semiconductor manufacturing. NVIDIA‘s simulation infrastructure remains the most advanced platform for synthetic AI training. None of this is in dispute.

The exposure lies beneath the software.

Where US simulation leadership does and does not compensate

NVIDIA Cosmos and similar high-fidelity simulation environments offer the ability to generate large volumes of varied training scenarios without physical hardware at scale. This is a real capability advantage. Whether simulation-derived training data produces equivalent physical AI outcomes to real-world operational data at deployment scale has not been resolved in public research as of mid-2026. The US is placing a significant strategic bet on simulation as a substitute for the physical deployment density China has built. That bet may prove correct, but it remains empirically unproven in the physical AI domain.

NVIDIA’s simulation strategy, centred on the Cosmos platform for generating synthetic physical training data, is being pursued as a direct counterweight to China’s real-world deployment density, but the company’s China data-centre revenue has already collapsed from roughly $6 billion in FY2024 to near zero, narrowing its commercial runway in the market where that physical data is being generated at scale.

The supply chain dependency problem is where the structural vulnerability sharpens.

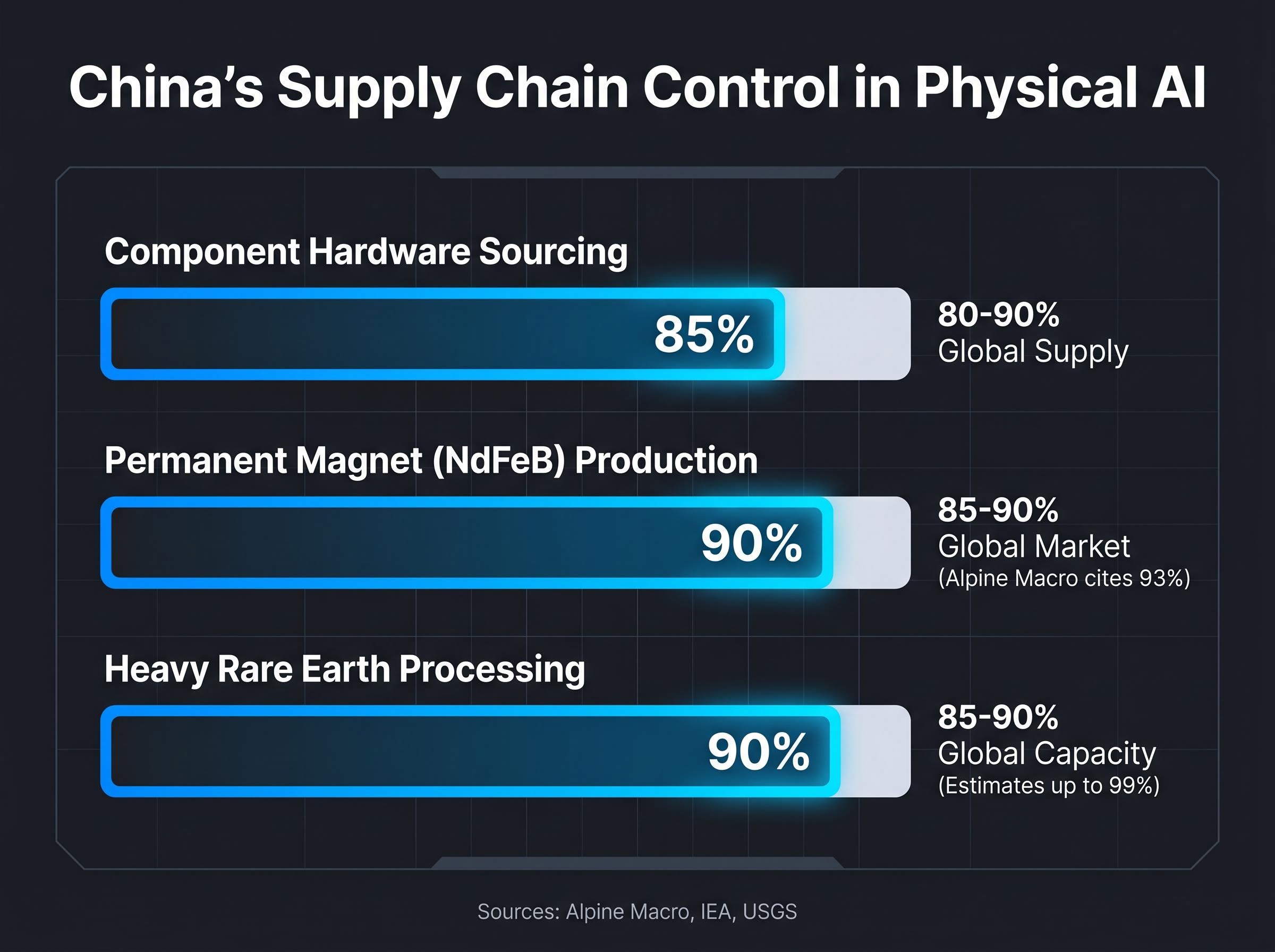

- Component hardware sourcing: China is estimated to supply 80-90% of critical hardware components used globally in robotics, according to Alpine Macro.

- Permanent magnet production: China holds approximately 85-90% of the global NdFeB magnet market (public sources consistently cite over 80%; Alpine Macro cites 93%).

- Heavy rare earth processing: China controls approximately 85-90% of global processing capacity, with some private research estimates reaching 99% for heavy rare earths specifically (public sources from the IEA and USGS cite over 80% as a consistent floor).

USGS rare earth processing data consistently places China’s share of global processing capacity in the 85-90% range, a figure that underpins the structural supply chain vulnerability facing US robotics manufacturers who depend on Chinese-controlled NdFeB magnet production for actuator components.

Robotic actuators, the components that enable physical movement, depend on high-performance NdFeB magnets. Any escalation scenario between the US and China affects US robotics production disproportionately because the supply chain bottleneck sits in Chinese-controlled processing.

International diversification efforts across the US, EU, Japan, and Australia are underway but remain incremental. No major 2026-dated commissioning of large-scale non-Chinese heavy rare earth processing has been identified in public sources. US annual industrial robot installations of approximately 34,200 units compare to China’s approximately 295,000+, a gap that software leadership alone does not close.

No 2026-dated US federal programme has been identified that explicitly targets the embodied AI or physical robotics manufacturing gap at a scale comparable to China’s 15th Five-Year Plan commitment.

Self-reinforcing dynamics, and what they mean for the decade ahead

The structural advantages described in previous sections are not static snapshots. They are self-reinforcing loops.

China’s deployment scale generates real-world training data. That data improves physical AI models. Improved models make the next generation of robots more capable and cheaper. Cheaper, more capable robots drive further deployment. State-directed investment funds the infrastructure that sustains each turn of the loop, while domestic supplier dominance insulates the supply chain from external disruption.

The relevant question is no longer whether China has a physical AI lead, but whether the US and allied economies can construct a credible policy and investment response before the embodied AI training data gap becomes as entrenched as China’s rare earth processing dominance.

The EV and battery supply chain precedent, as framed by both Morgan Stanley and Alpine Macro, is the most historically instructive parallel. State-directed manufacturing scale produced durable market leadership despite initial quality gaps. The pattern is familiar; the domain is new.

At a global installation CAGR of approximately 7% through 2028, China’s absolute installation advantage widens in unit terms even if its percentage share holds steady. For the physical AI gap to narrow materially, several conditions would need to change simultaneously:

- US domestic robotics manufacturing would need to scale dramatically beyond current installation volumes

- Supply chain diversification for rare earths and permanent magnets would need to move from incremental to structural

- Simulation would need to be proven equivalent to real-world data for physical AI training at deployment scale

- A policy commitment equivalent in scope to the Five-Year Plan architecture would need to emerge from market-driven economies

The outcome is not predetermined. The window for a structurally effective response from market-driven economies is narrowing, and the compounding logic of China’s physical deployment advantage makes each year of delay more consequential than the last.

Geopolitical risk pricing around the US-China relationship has recently been skewed by summit optimism, with equity markets bidding up assets on the basis of atmosphere rather than confirmed policy outcomes, a dynamic that makes it harder for investors to accurately calibrate the structural supply chain and technology transfer risks that the physical AI competition depends on resolving.

The industrial front: a key battleground in the AI competition

The US-China AI contest has a physical dimension that is structurally distinct from software and semiconductor competition, and China currently holds compounding advantages in that physical dimension. The deployment scale, the domestic supplier base, the state-directed investment architecture, and the supply chain control are all reinforcing one another.

Genuine uncertainty remains. The simulation-versus-real-world data question is unresolved. US policy responses could accelerate. The EV precedent is an analogy, not a guarantee.

The specific investor and strategic implication is clear: portfolios and policy positions calibrated only to the brain-layer scorecard are exposed to a category of risk that the benchmark leaderboard does not capture. The primary sources for tracking this competition include the IFR World Robotics 2025 full publication (forthcoming), USGS Mineral Commodity Summaries 2026, IEA Critical Minerals 2026, and the Alpine Macro report of 12 May 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and policy shifts.