ThaiBev at 10x Earnings: Value Trap or Hidden Opportunity?

1 hr ago

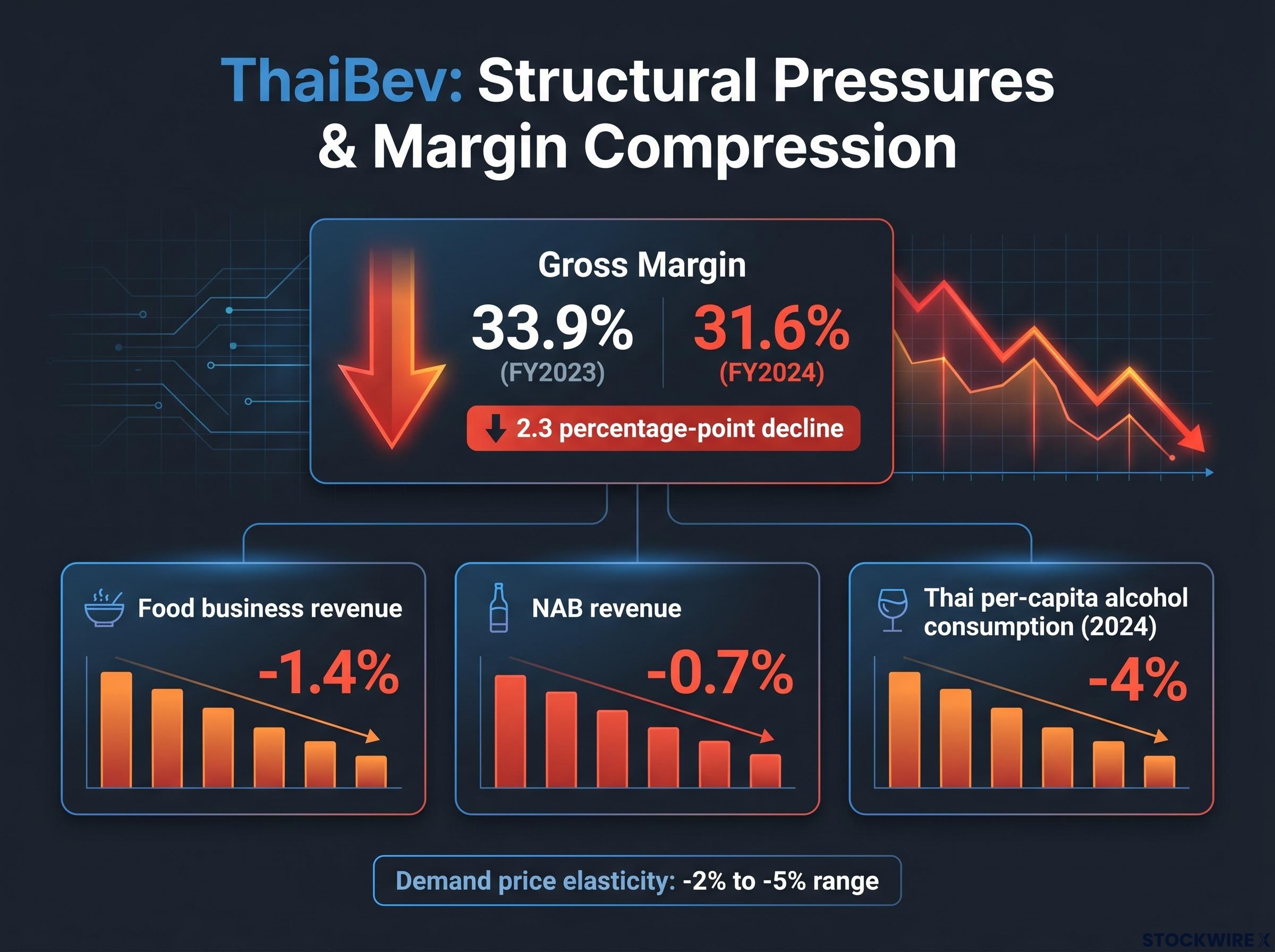

ThaiBev’s gross margin fell 2.3 percentage points in a single fiscal year. The cause was not a competitive attack or an operational misstep. It was a tax hike.

The response from management is a product category most analysts were not watching closely: ready-to-drink spirits. Across Southeast Asia, consumer purchasing power is under structural pressure from a convergence of excise increases, inflation, and stagnant household incomes. For a conglomerate whose profit engine is a high-excise-duty spirits business, that combination is not a bad quarter; it is a sustained squeeze on the margin structure that underwrites the entire group.

ThaiBev’s five-part strategic pivot, with RTD spirits as its most analytically interesting lever, is a real-world case study in how consumer-facing companies engineer margin resilience when volume growth is off the table. Here is what the RTD move reveals about restructuring profitability under constraint, and why that pattern is worth understanding before the next earnings cycle.

This is not cyclical softness. ThaiBev is confronting a stagflationary dynamic at the household level: prices and taxes are rising faster than incomes, and discretionary categories like alcohol absorb the full force of that compression. The shocks have compounded rather than arrived in sequence:

The stagflationary consumer squeeze ThaiBev is navigating in Southeast Asia has a structural counterpart in developed markets: Q1 2026 earnings across US consumer discretionary sectors confirmed that price-sensitive demand destruction is not a regional phenomenon but a cross-geography pattern when household budgets are compressed faster than incomes recover.

The financial imprint is visible across ThaiBev’s segments. Food business revenue declined approximately 1.4%, explicitly linked to softer consumer spending. Non-alcoholic beverage (NAB) revenue fell roughly 0.7% despite increased brand investment. Thai per-capita alcohol consumption slipped around 4% in 2024, reflecting the combined weight of tightening regulation and deteriorating household budgets.

Gross margin compressed from 33.9% (FY2023) to 31.6% (FY2024), a 2.3 percentage-point decline driven primarily by excise hikes across ThaiBev’s core markets.

That compression is not a rounding error. It tells you that ThaiBev’s pricing power is being eroded from the regulatory side at the same time consumer budgets are being squeezed from the household side. Demand price elasticity for core products sits in the -2% to -5% range, meaning excise-driven price increases directly destroy volume. The company cannot simply raise prices to recover margin.

For regional alcohol producers, meeting evolving compliance requirements absorbs an estimated 3-5% of margin, a burden that sits on top of the direct earnings hit from excise hikes. With excise rates running at 58% for beer and 48% for spirits, the tax burden is not a background condition; it is a defining feature of the operating environment. Understanding why ThaiBev’s strategic response is structurally motivated, rather than opportunistic, starts here.

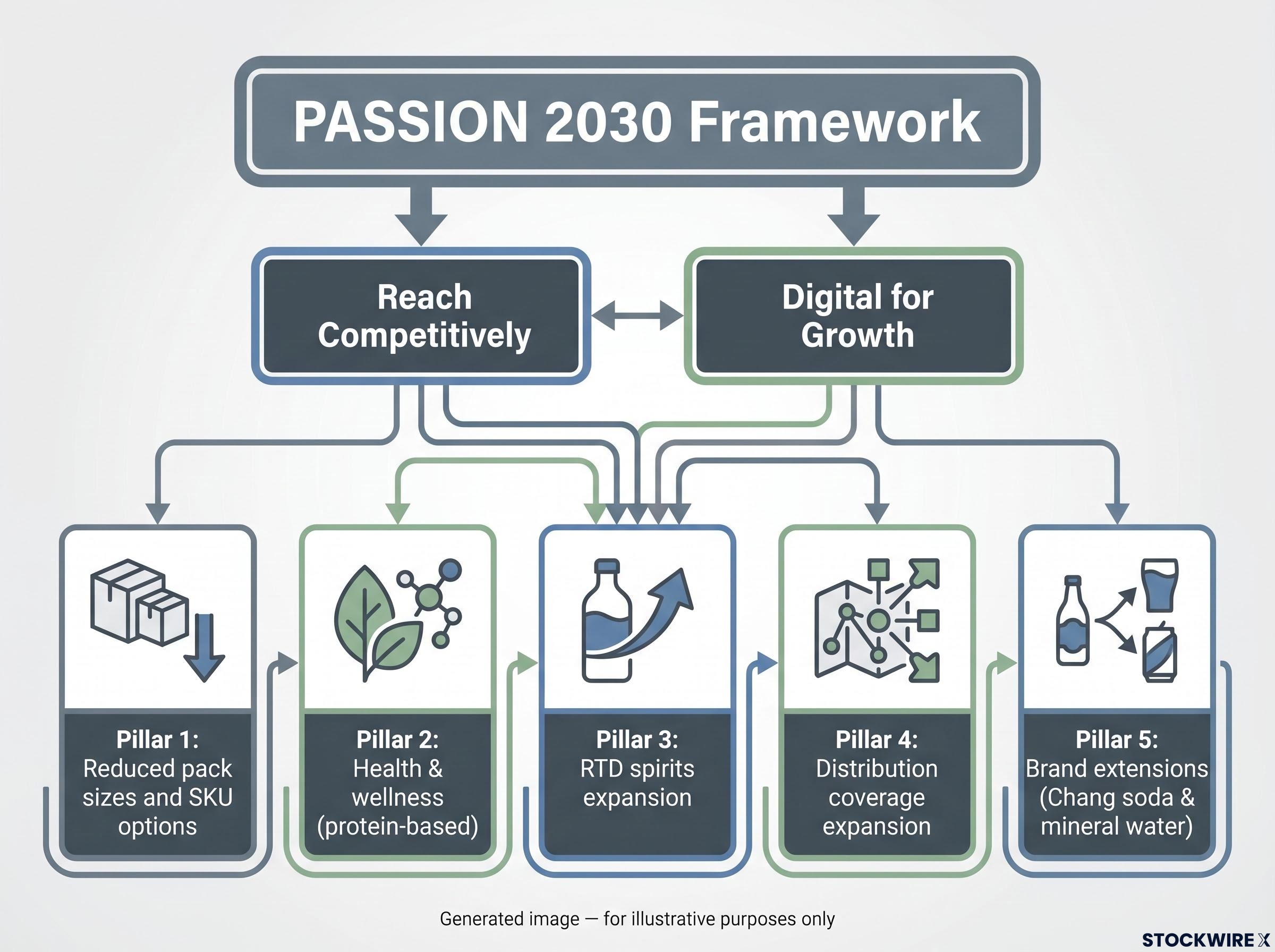

ThaiBev’s public strategy sits under the PASSION 2030 framework, built on two formal pillars: “Reach Competitively” (comprehensive distribution coverage with cost-competitive logistics) and “Digital for Growth” (using digital tools to sharpen customer insights and improve efficiency). Those are the containers. The substance lives in five tactical pillars that map onto the framework:

A multi-pillar consumer brand turnaround under demand pressure is not unique to ThaiBev: Starbucks’ concurrent strategic restructuring illustrates how large consumer-facing companies across different geographies converge on similar tactical responses, including operational efficiency, digital investment, and portfolio rebalancing, when volume growth is unavailable and margin protection becomes the primary objective.

Not all five pillars carry the same evidentiary weight. Distribution coverage, NAB diversification (approximately THB 49.3 billion in revenue for the nine months ended June 2025), and the Chang brand extensions into soda and mineral water are well documented in ThaiBev’s own public disclosures. The spirits segment remains the highest-margin, largest gross-profit-contribution segment within the group.

Specific pack-size programmes and the protein-based wellness pipeline originate primarily from Phillip Securities Research rather than direct corporate guidance. They are directionally consistent with standard FMCG practice and global beverage trends, but they carry more uncertainty about timing and scale. That evidence hierarchy matters: pillars backed by corporate disclosure represent committed capital allocation decisions, while analyst-interpreted pillars may be accurate but remain less certain.

RTD spirits sits in between, well supported by the strategic logic and capital-light rationale, but with limited public disclosure on specific SKUs, volume contribution, or segment-level economics. It is also the most analytically interesting pillar. The next section explains why.

The margin case for RTD spirits starts with tax classification. In Thailand, excise rates differ materially by product category. A prior policy change set beer excise at 58% and spirits excise at 48%, a ten-percentage-point differential that directly shapes per-unit economics. If Thai regulations treat RTD spirits in a way that yields a lower effective excise burden per unit of retail price than standard beer, then shifting consumption from beer to RTD spirits raises gross margin per unit even when the consumer pays a comparable shelf price.

That tax-classification mechanism is the core of the thesis. It means RTD spirits is not a product innovation story; it is a margin-engineering decision.

The second dimension is capital intensity. ThaiBev already operates large-scale spirits manufacturing and bottling assets. Industry practice confirms that layering RTD formats onto existing spirits infrastructure typically requires formulation adjustments, label approvals, and filling-line modifications, not greenfield plants. The incremental margin arrives off an installed fixed-cost base, improving return on invested capital (ROIC) without raising balance-sheet risk.

According to IWSR data, RTDs were projected to grow approximately 12% in volume between 2022 and 2027, outpacing traditional beer and spirits. The 2022-2025 portion of that projection is now largely historical; the 2026-2027 portion remains forward-looking.

The IWSR RTD category projections covering 10 key global markets show the segment reaching USD 40 billion by 2027, with cocktails, long drinks, and premium products identified as the primary growth vectors, a composition that maps directly onto the convenience and premiumisation-lite positioning ThaiBev is targeting with its RTD spirits expansion.

Globally, RTDs sit at the intersection of convenience, controlled cash outlay per occasion, and what the industry calls “premiumisation-lite”: consumers access a cocktail-like experience at a lower absolute price point than a full bottle of spirits. The US Craft Beverage Modernization Act illustrates the broader pattern: when regulators carve out differentiated tax rules for RTDs, producers capture higher margins at comparable shelf prices. Unverified data from studied markets suggests RTD spirits dollar sales may be running at approximately +40% year-over-year in 2026, though that figure should be treated directionally rather than as a precise benchmark.

| Attribute | Beer | RTD spirits |

|---|---|---|

| Relative excise burden | Higher | Lower (at comparable retail price) |

| Gross margin profile | Lower | Higher |

| Capital required for expansion | Higher (dedicated brewing assets) | Lower (leverages existing spirits infrastructure) |

| Cannibalisation direction | Loses share to RTD spirits | Draws from beer segment |

The capital-light point is the one worth sitting with. In a high-cost-of-capital, low-demand-visibility environment, a growth lever that improves margin off existing assets without raising the balance sheet is structurally more attractive than one requiring fresh capital. That distinction is what separates RTD from most of ThaiBev’s other strategic options.

The instinct when a company launches a product that competes with its existing lines is to flag cannibalisation as a risk. In ThaiBev’s case, the economics suggest the opposite conclusion.

RTD spirits are explicitly positioned to draw consumers from the beer segment. Internal cannibalisation is not an unintended consequence but an acceptable, and potentially desirable, outcome. The logic is straightforward: spirits are ThaiBev’s highest-margin segment, beer is more competitive and more tax-exposed, and repeated excise hikes have forced beer price increases that erode volume. If RTD spirits substitute low-margin beer units with high-margin RTD units, group economics improve even if total volume is flat.

Two scenarios make the point:

In either case, internal displacement is margin-accretive. RTD spirits do not need to displace the core spirits franchise; they only need to provide a higher-margin alternative to beer within ThaiBev’s portfolio and a defensive option against encroachment from rival beer or flavoured malt beverages.

The same underlying logic applies to ThaiBev’s pack-size pillar. Sachet economics, the practice of offering smaller pack sizes at lower absolute cash outlay even at higher per-unit prices, maintains category participation among cash-constrained consumers who might otherwise exit entirely. Rather than cutting list prices (which are hard to reverse and destructive to margin), downsizing packs preserves per-unit economics while keeping the consumer in the brand ecosystem. Both tactics share a common principle: restructuring the unit of sale to protect margin when the demand environment will not support volume growth.

“Cannibalisation risk” in a multi-category portfolio is frequently overstated when the cannibalising product carries a higher margin. Management’s willingness to accept internal displacement signals confidence in the RTD margin differential rather than desperation.

The regulatory environment is genuinely two-directional, and resolving it artificially in either direction would misrepresent the operating conditions.

Restrictive developments:

Liberalising developments:

Regional alcohol producers face an estimated compliance cost burden of 3-5% of margin, a layer of expense that sits on top of, and amplifies, the direct earnings compression caused by rising excise duties.

The tension between public-health restriction and tourism-driven liberalisation defines the conditions under which ThaiBev operates. The excise differential between beer (58%) and spirits (48%) illustrates the heterogeneity at the category level: different product formats are taxed and regulated differently.

That heterogeneity creates an active portfolio management opportunity. A company that deliberately reweights its product mix toward categories with more favourable regulatory treatment is not passively reacting to policy but strategically exploiting it. The distinction affects how you should assess the durability of any margin improvement: if the improvement depends on a regulatory differential that could be legislated away, it is less durable than if it stems from structural capital efficiency. For ThaiBev, the RTD strategy appears to benefit from both, which is partly why it is the most interesting lever in the toolkit.

The excise differential between beer at 58% and spirits at 48% is precisely the kind of tax policy signal that separates genuine structural margin shifts from short-term regulatory noise; markets that fail to distinguish between the two tend to misprice both the downside risk and the recovery opportunity in consumer goods equities.

The lasting value of ThaiBev’s case sits not in the company-specific detail but in the transferable framework it illustrates. Four strategic lessons emerge:

The baseline problem remains the gross margin compression from 33.9% to 31.6%. The RTD pivot is designed to address it, and the margin mechanics, tax classification advantage, and capital-light expansion logic are analytically sound. But a complete assessment requires acknowledging what cannot yet be confirmed from public data: RTD volume contribution, specific Thai excise differentials for RTD products, and the precise scope of the wellness pipeline remain inferential until ThaiBev provides segment-level RTD disclosure.

That evidence caveat is not a weakness to bury. Knowing what you can and cannot confirm from available data is as analytically important as the thesis itself. The confirmed elements, gross margin compression, NAB scale, distribution strategy, brand extensions, establish that the strategic response is real and capital is being allocated. The inferential elements establish that the full earnings materiality of the RTD lever remains to be proven.

For readers wanting to assess whether ThaiBev’s strategic commitments represent genuine capital allocation discipline or aspirational positioning, our dedicated guide to evaluating management capital allocation covers the per-share return frameworks, insider ownership signals, and red-flag patterns that professional investors use to distinguish compounders from restructuring stories that stall.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking projections, including IWSR growth estimates and analyst-derived strategic interpretations, are subject to change based on market developments and company performance.

ThaiBev is expanding into ready-to-drink spirits formats that carry a lower excise burden (48%) than its beer products (58%), allowing the company to improve gross margin per unit at comparable retail prices by shifting its sales mix away from the more heavily taxed beer segment.

ThaiBev's gross margin declined 2.3 percentage points from 33.9% to 31.6% in FY2024, driven primarily by repeated excise duty hikes across its core markets of Thailand, Myanmar, and Laos, which the company could not offset through price increases without destroying volume.

ThaiBev layers RTD formats onto its existing spirits manufacturing and bottling infrastructure, requiring only formulation adjustments, label approvals, and filling-line modifications rather than new plants, so incremental margin improvement arrives without raising balance-sheet risk.

Because spirits are ThaiBev's highest-margin segment and beer is more tax-exposed, RTD spirits substituting beer units shifts the portfolio mix toward higher margins; even if total volume is flat, group gross margin and EBITDA improve when lower-margin beer units are replaced by higher-margin RTD units.

PASSION 2030 is ThaiBev's strategic framework built on two formal pillars, competitive distribution reach and digital-led growth, which house five tactical responses to constrained demand: reduced pack sizes, health and wellness products, RTD spirits expansion, distribution coverage growth, and brand extensions such as Chang-branded soda and mineral water.