Hormuz Prices Have Normalised. Geopolitical Inflation Risk Has Not.

47 mins ago

Whirlpool reported Q1 2026 North American operating profit of $6 million, down 96% from $149 million a year earlier. Its chief executive compared current US appliance demand to conditions last seen during the 2008 global financial crisis. The dividend has been suspended. The share price sits at its lowest level since December 2011. That result did not arrive in isolation. It landed alongside McDonald’s warning that fuel costs are crushing its lowest-income customers, Shake Shack recording the worst single-session stock decline in company history, and Brent crude oscillating between $96 and $115.30 a barrel in a single trading week. The Iran conflict, now in its third month, has become a direct tax on American household budgets, and corporate earnings are starting to price it. What follows reads three Q1 2026 earnings reports as a diagnostic tool: where exactly consumer demand is breaking down, which income segments are absorbing the most stress, and what Whirlpool’s result specifically signals about conditions that typically precede broader economic deterioration.

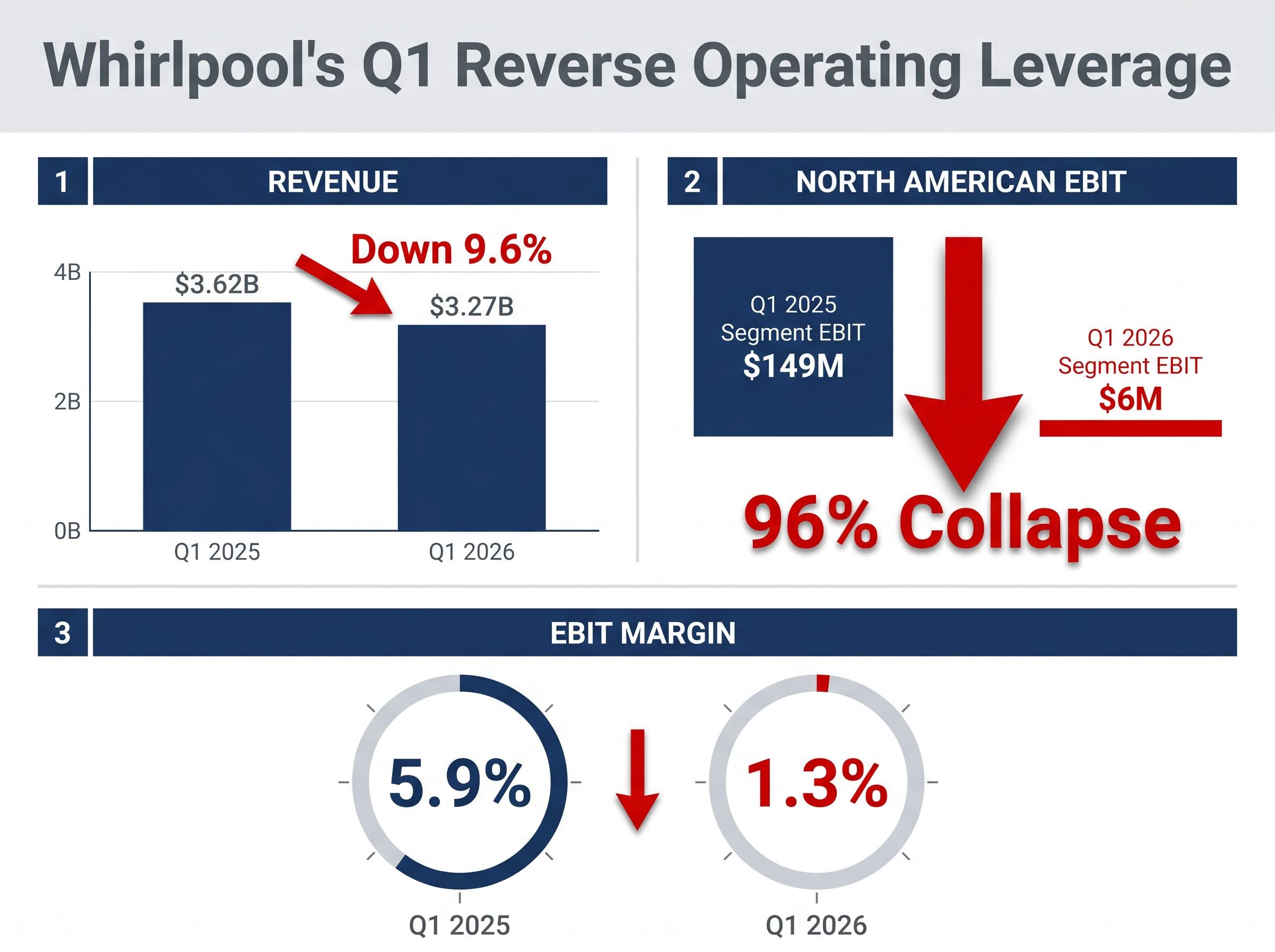

The deterioration unfolded across every line item. Whirlpool reported Q1 revenue of $3.27 billion, down 9.6% year-over-year and 7% below the $3.51 billion analyst consensus. Adjusted earnings per share came in at negative $0.56, against a consensus expectation of positive $0.62. Ongoing EBIT margin compressed to 1.3%, a decline of 4.6 percentage points from the prior year.

The North American segment told the sharpest story. Revenue fell 7.5% to $2.24 billion, a meaningful decline but not catastrophic in isolation. Segment EBIT, however, collapsed 96% to $6 million from $149 million. That gap between a 7.5% revenue miss and a 96% profit collapse is not a revenue problem; it is operating leverage working in reverse across a capital-intensive manufacturing base where fixed costs do not flex with volume.

| Metric | Q1 2025 Actual | Q1 2026 Actual | Consensus Estimate |

|---|---|---|---|

| Revenue | $3.62B | $3.27B | $3.51B |

| Adjusted EPS | $0.62 | -$0.56 | $0.62 |

| EBIT Margin | 5.9% | 1.3% | N/A |

| North American Segment EBIT | $149M | $6M | N/A |

Management then suspended the dividend entirely, redirecting cash to service over $900 million in debt. That decision reframed the quarter: this was not a company managing a soft patch, but one repositioning its capital allocation for a structurally lower demand environment.

The divergence between headline retail figures and underlying household financial conditions has become one of the most closely watched US recession risk indicators in 2026, with the personal savings rate at 4.0% in February signalling that a significant portion of apparent consumer strength is being funded by buffer drawdowns rather than income growth.

CEO Marc Bitzer compared current US appliance demand conditions to the 2008 global financial crisis, describing consumer sentiment as the lowest in approximately 50 years.

The share price fell 11.9% on the day, extending the year-to-date decline to 42%.

Whirlpool makes refrigerators and washing machines, but the signal embedded in its earnings extends well beyond the appliance aisle. Consumer durables, particularly big-ticket household appliances, are among the first discretionary categories that households defer when income comes under pressure. A broken dishwasher gets replaced; a functioning but ageing one stays in the kitchen. That distinction between necessity and discretion is what makes the sector a coincident-to-leading indicator of broader consumer financial health.

Whirlpool management disclosed that necessity-driven demand, replacement of broken units, accounts for over 60% of industry volume and remained relatively resilient through Q1. The remaining 40%, discretionary upgrades, new-home purchases, renovation-linked demand, bore the full weight of the contraction.

Renovation-linked demand for appliances is directly coupled to housing market activity, and with new single-family home sales down 17.6% in January 2026 to their lowest monthly reading since 2013, the discretionary upgrade segment of Whirlpool’s revenue base was facing a structural headwind before the Iran conflict added a second layer of household budget pressure.

Three data points frame the severity:

The Conference Board Consumer Confidence Index dropped 9.7 points in January 2026 to a 12-year low, a reading that economists noted reflected deteriorating expectations about both current conditions and the six-month outlook, consistent with the deferral behaviour Whirlpool’s volumes subsequently confirmed.

US appliance industry demand fell 7.4% in Q1, with March alone declining 10%. That acceleration through the quarter suggests the trend was worsening, not stabilising.

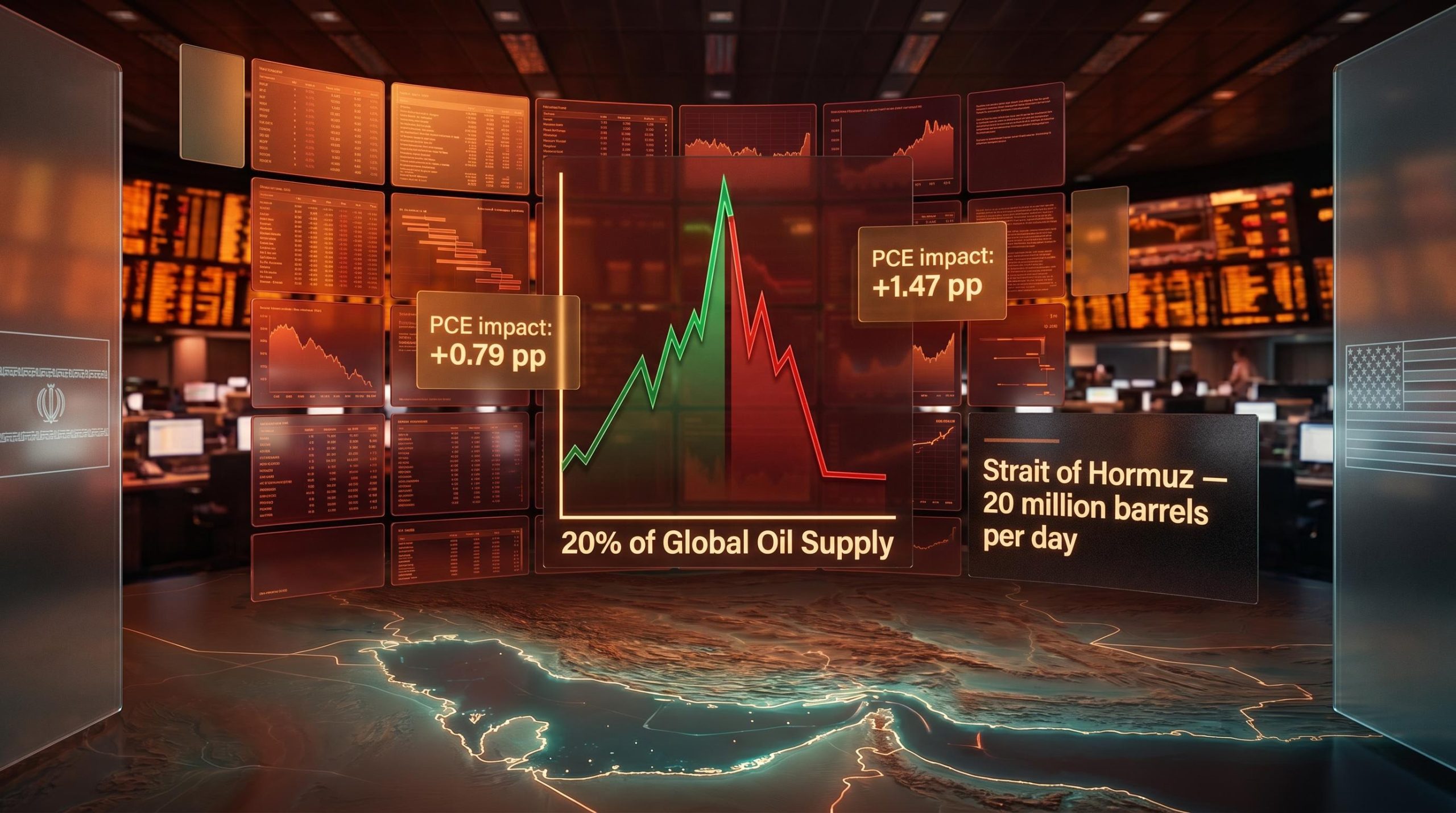

The transmission mechanism from the Strait of Hormuz to a family’s decision not to buy a refrigerator runs through a single channel: fuel costs. The Iran conflict, which began in late February 2026, elevated crude prices, which raised petrol and energy costs, which compressed household disposable income, which suppressed spending on big-ticket discretionary items. Each link in that chain is now visible in earnings data.

The oil price transmission mechanism from Strait of Hormuz disruption through to retail gasoline and then household disposable income operates with a lag of roughly two to four weeks at each stage, which is why Q1 earnings reports are capturing only the first wave of consumer budget compression from a conflict that began in late February 2026.

Brent crude reached an intraweek high of $115.30 a barrel and a low of $96 a barrel in the week of 8 May 2026. As of 7 May, it sat at approximately $101 a barrel. That volatility itself is a cost: households and businesses cannot price a resolution into their spending plans when the barrel price swings $19 in five trading sessions.

The major bank forecasts capture the uncertainty that is paralysing consumer planning:

| Institution | Near-Term Brent Forecast | Full-Year 2026 View | Key Variable Identified |

|---|---|---|---|

| Citigroup | $110/barrel (revised up $15) | Elevated through H1; reopening base case end of May | Iran’s capacity to endure blockade for years |

| Goldman Sachs | $90/barrel (Q2, revised down from $99) | ~$100 April-May, easing toward $90 by Q4 | Negotiation progress timeline |

| J.P. Morgan | Near-term spike acknowledged | ~$60/barrel average for full year | Long-term supply fundamentals |

Citigroup’s Max Layton characterised Iran’s government as potentially capable of enduring the blockade for years rather than months, a timeline that, if accurate, would sustain household budget pressure well beyond current earnings cycles.

As of 7 May, Iran is reviewing a US proposal, and President Trump has paused military escorts as part of the negotiating posture. Neither development constitutes resolution.

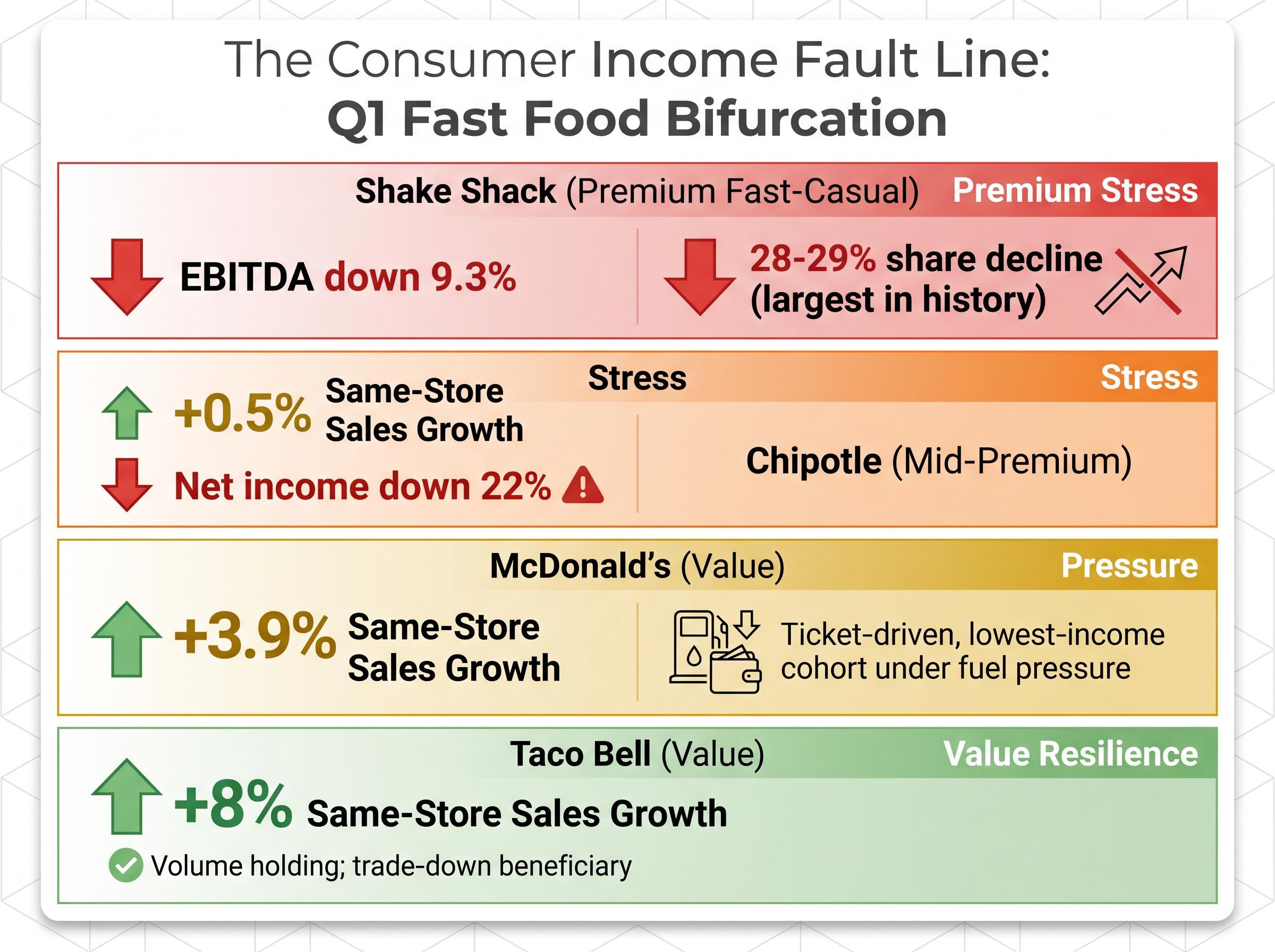

McDonald’s reported Q1 2026 revenue of $6.52 billion, up 9% year-over-year, and adjusted earnings per share of $2.83, beating the $2.74 consensus estimate. US comparable sales rose 3.9%, but the growth was driven by higher average ticket, not traffic. Management explicitly flagged that fuel costs are disproportionately pressuring its lowest-income customer cohort and described the consumer environment as “at best stagnant and potentially worsening.”

The value tier is not collapsing. It is absorbing stress through trade-down behaviour: Taco Bell posted same-store sales growth of 8% in the same period. Lower-income consumers are still eating out, but they are choosing the cheapest options available and spending more of their budget on fuel to get there.

Shake Shack told the opposite story. Revenue of $366.7 million (up 14.3%) missed the $370.8 million estimate. Adjusted earnings per share came in at $0.00 against a $0.12 consensus. EBITDA fell 9.3% to $37.0 million as the company absorbed beef cost increases in the low-teens percentage range rather than passing them to customers. The share price dropped approximately 28-29% in a single session, the largest decline in company history.

| Company | Tier | Same-Store Sales Growth | Key Stress Signal |

|---|---|---|---|

| Taco Bell | Value | +8% | Volume holding; trade-down beneficiary |

| McDonald’s | Value | +3.9% | Ticket-driven, not traffic; lowest-income cohort under fuel pressure |

| Chipotle | Mid-Premium | +0.5% | Net income down 22%; near-flat comps |

| Shake Shack | Premium Fast-Casual | +14.3% (revenue) | EBITDA down 9.3%; absorbing input costs; 28-29% share decline |

The pattern is structurally consistent across a wider peer set. Amazon (net sales up 17%) and Costco (strong sales) held at the value-oriented, high-volume end. Home Depot posted revenue growth of 9.4% but experienced margin compression. The bifurcation follows a clear income line: middle-income households are not exiting consumption but trading down, while premium-tier companies are sacrificing their own margins to retain increasingly price-sensitive customers.

A bad quarter becomes a structural demand signal when management tells investors not to expect recovery. Whirlpool cut its full-year 2026 EPS guidance from approximately $6.23 to $3.00-$3.50, roughly a 50% reduction against prior guidance and well below the $4.73 analyst consensus.

Whirlpool’s full-year EPS guidance was cut from approximately $6.23 to a range of $3.00-$3.50, a reduction of roughly 50%, signalling that management does not anticipate a near-term recovery in discretionary demand.

The company’s compensating actions reinforce that reading. In order of implementation:

These are not responses to a temporary disruption. Stacking 14% in cumulative price increases onto a consumer base already deferring purchases is a bet that necessity-driven replacement demand can absorb higher prices even as discretionary demand remains depressed.

The next confirmatory data point arrives on 14 May 2026, when the Census Bureau releases April 2026 retail sales figures. The most recent data, March 2026, showed a 1.9% month-over-month increase and 4.2% year-over-year growth. If April’s reading decelerates, the demand destruction documented in Whirlpool’s guidance gains broader empirical support.

Across three Q1 earnings reports, a coherent US consumer demand picture has emerged. Discretionary spending on big-ticket durables has entered territory that Whirlpool’s own CEO compared to the 2008 financial crisis. Value-tier consumption is holding through trade-down behaviour. Premium and mid-tier margins are being compressed as companies absorb input cost inflation rather than pass it to customers who are already pulling back.

The single largest identifiable variable in the demand outlook is the resolution of the Strait of Hormuz blockade, because it directly determines the fuel cost trajectory that is the primary transmission mechanism for the income compression documented across these earnings reports.

As of 7-8 May 2026, Iran is reviewing a US proposal, and Trump has paused military escorts. The outcome remains unresolved. Whirlpool management has stated it views current consumer sentiment as unsustainably depressed and expects a rebound, but has offered no timeline.

Whirlpool, McDonald’s, and Shake Shack collectively map the US consumer demand contraction across income segments and spending categories with more precision than any single macroeconomic data release currently available. Discretionary durables are in contraction. Value-tier spending is holding through volume. Premium margins are being sacrificed to retain customers.

What remains unknown will arrive soon. The 14 May retail sales release will either confirm or complicate the demand destruction narrative. Hormuz negotiation developments will determine whether household budget pressure eases by summer or persists into the second half. For investors monitoring the consumer sector, those two signals carry more weight in the near term than any earnings revision model.

For investors who want to contextualise the current consumer demand destruction within a longer-run framework, our deep-dive into high gasoline prices and stock market history documents that the S&P 500 has fallen an average of 11% in the six months after national gasoline prices have breached $4.00 per gallon, with sustained episodes historically associated with peak-to-trough declines averaging 41%, a distribution that frames the stakes of Hormuz resolution timing for equity markets.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced are subject to market conditions and various risk factors. Past performance does not guarantee future results.

US consumer demand is under significant pressure in 2026, driven by elevated fuel costs from the Iran conflict, a 12-year low in consumer confidence, and projected consumption growth of just 1.9%, the weakest non-pandemic reading since 2013. Discretionary spending on big-ticket items like appliances has seen the sharpest deterioration, while value-tier spending is holding through trade-down behaviour.

Whirlpool's North American segment EBIT collapsed 96% to $6 million from $149 million a year earlier because operating leverage worked in reverse: a 7.5% revenue decline across a capital-intensive manufacturing base with largely fixed costs wiped out nearly all profitability. Discretionary appliance upgrades, which represent roughly 40% of industry volume, bore the full weight of consumer demand contraction.

Higher oil prices from the Strait of Hormuz disruption raise petrol and energy costs for households, directly compressing disposable income and reducing spending on big-ticket discretionary items like appliances. This transmission from crude prices to consumer budgets typically operates with a lag of two to four weeks at each stage, meaning Q1 2026 earnings captured only the first wave of budget pressure from a conflict that began in late February 2026.

Whirlpool suspended its dividend entirely to redirect cash toward servicing over $900 million in debt, a decision management framed as repositioning capital allocation for a structurally lower demand environment rather than managing a temporary soft patch. The company also cut its full-year 2026 EPS guidance by roughly 50%, from approximately $6.23 to a range of $3.00-$3.50.

The Census Bureau's April 2026 retail sales release on 14 May 2026 is the next key confirmatory data point; if the reading decelerates from March's 1.9% month-over-month increase, it would provide broader empirical support for the demand destruction documented in Whirlpool's earnings. Developments in Hormuz negotiations are the other critical variable, as a resolution would directly ease the fuel cost pressure that is the primary driver of household budget compression.