European Stocks Hit Highs While Institutional Money Stays Out

16 mins ago

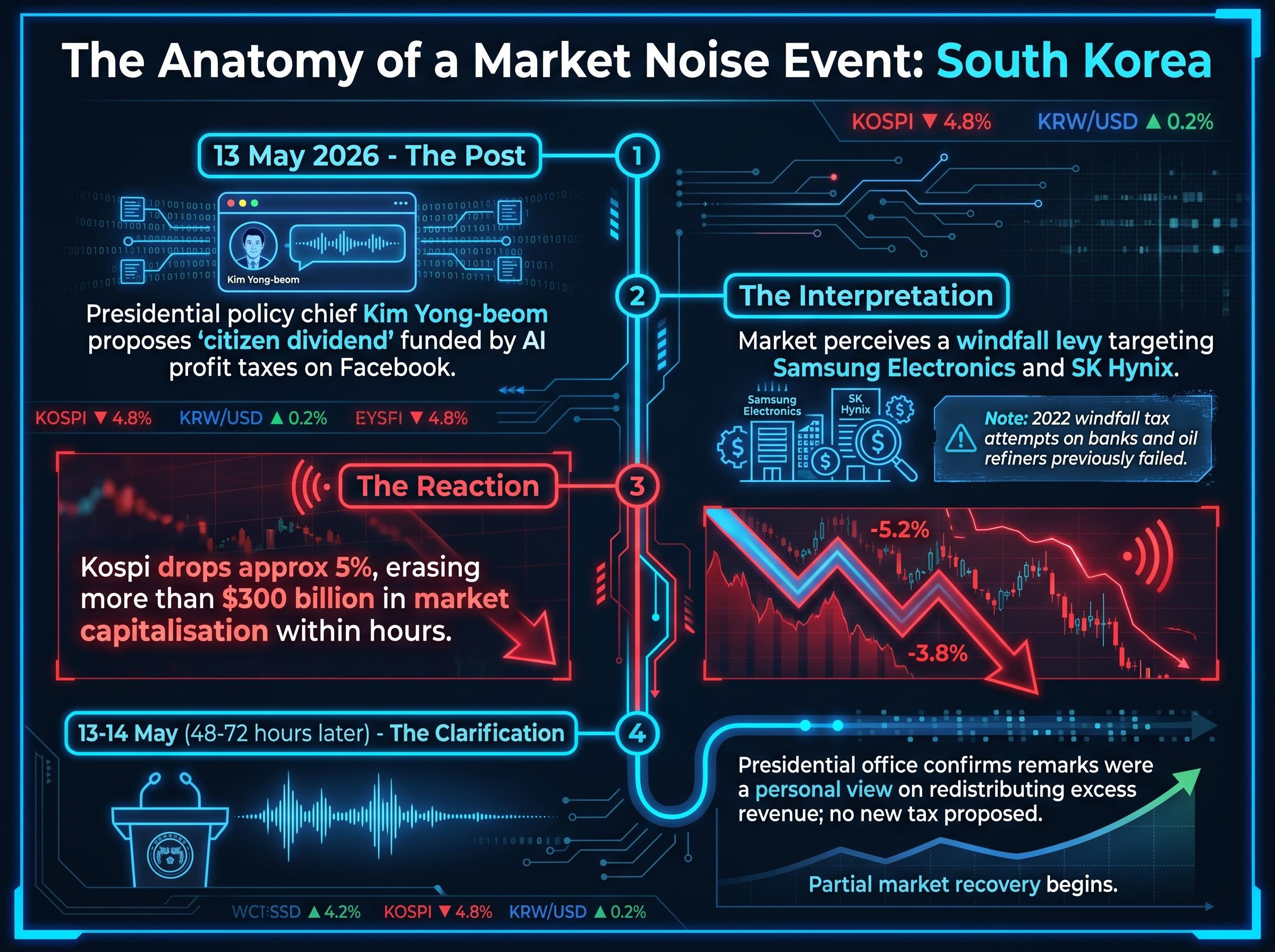

On 13 May 2026, a single Facebook post by a South Korean presidential advisor erased more than $300 billion in market capitalisation within hours. No bill had been drafted. No vote had been called. The market had reacted to a comment.

Within a single week in May 2026, three separate jurisdictions produced three structurally different tax policy events, each triggering a distinct market response. South Korea’s semiconductor selloff was driven by a miscommunication. The Netherlands’ contested 36% unrealised gains tax was navigating Senate resistance months after passing the lower house. Australia’s federal budget formally replaced a 27-year-old capital gains discount with a new regime. Each event demands a different analytical response from investors.

This analysis uses all three cases to build a practical framework for distinguishing tax policy noise from genuine policy signal, assessing the probability of enactment, and calibrating market reactions accordingly. The goal is a structured method for evaluating any future tax policy announcement without either overreacting or dismissing real risk.

Equity markets price the expected present value of future after-tax cash flows. When new information about a potential tax change reaches the market, that information gets incorporated immediately, not when the law takes effect. This forward-pricing mechanism is why a Facebook post about a hypothetical tax can move stocks within minutes, and why a budget announcement scheduled for July 2027 implementation begins shaping portfolio decisions in May 2026.

The market does not, however, price in the full stated impact of every announcement. It applies a probability discount. A formal budget measure backed by a governing majority receives a heavier weighting than an informal social media post by an advisor. Event-study research covering the US 2003 dividend tax cut and Obama-era capital gains proposals confirms this pattern: announcement effects are real, but their magnitude tracks the perceived likelihood of enactment in the form announced.

The NBER research on the 2003 dividend tax cut found that markets incorporated tax policy changes at announcement rather than at enactment, but that the magnitude of price adjustment tracked the perceived probability of the policy passing in its stated form, a finding that directly supports probability-discounting as the correct analytical posture for investors evaluating any new tax proposal.

The distinction that matters most is between policy noise, communications with no legislative substance, and policy signal, changes with a credible path to law. The three May 2026 cases map onto this spectrum precisely.

Each requires a different analytical tool, not a uniform reaction.

Presidential policy chief Kim Yong-beom posted on Facebook in mid-May 2026, proposing a “citizen dividend” funded by taxes on AI profits. Markets read the post as a windfall levy aimed directly at South Korea’s dominant semiconductor firms. Samsung Electronics and SK Hynix, the two most heavily weighted stocks on the Kospi, bore the brunt of the interpretation.

The Kospi dropped approximately 5%, erasing more than $300 billion in market capitalisation within hours of the post.

The presidential office moved to clarify within 48-72 hours. Officials stated that Kim Yong-beom’s remarks reflected a personal view on redistributing excess tax revenue already collected, not a proposal for any new corporate or windfall tax. Korean chip stocks began a partial recovery in the days following the 13-14 May clarification.

The chip stock contagion crossed borders within a single session, with US-listed names including Micron, AMD, and Nvidia all declining before any official denial had been issued, illustrating how quickly an informal communication can propagate across connected markets when elevated valuations leave little buffer against regulatory uncertainty.

The gap between what was said, what was heard, and what was confirmed tells the story of this case:

South Korea’s 2022 attempts at windfall taxes on banks and oil refiners failed due to finance ministry and industry opposition, a precedent that further undermined the plausibility of the market’s initial interpretation. Investors who recognised the distinction between an informal communication and a legislative proposal could have avoided selling into the trough of a noise-driven event.

The Dutch Box 3 tax debate traces back to the 2021 Supreme Court ruling (Kerstarrest), which struck down the prior deemed-return system as incompatible with European human rights law. The government spent several years designing a replacement that would tax actual returns rather than a notional yield.

On 12 February 2026, the Lower House (Tweede Kamer) approved the Actual Return in Box 3 Act. The legislation introduces a flat 36% rate on actual returns, explicitly including unrealised and paper gains on equities, bonds, and cryptocurrency. The effective date is 1 January 2028, creating a nearly two-year window of legislative uncertainty.

| Legislative Stage | Date | Key Detail |

|---|---|---|

| Supreme Court ruling (Kerstarrest) | 2021 | Prior deemed-return system struck down as incompatible with human rights law |

| Lower House vote | 12 February 2026 | Flat 36% rate on actual returns, including unrealised gains, approved |

| Senate questions submitted | April 2026 | 36 pages of detailed questions sent to Tax Minister Eelco Eerenberg |

| Targeted effective date | 1 January 2028 | Nearly two-year implementation window remains subject to amendment |

The Dutch Senate cannot amend legislation directly. It can only accept or reject, which creates political pressure for government-initiated modifications before a final vote. The government has signalled willingness to pursue targeted amendments, including a refund mechanism for unrealised gains that subsequently reverse and expanded startup classification criteria.

The most controversial provision, taxing gains that have not been realised, is precisely the one facing the strongest resistance. Partial amendment remains the most probable outcome. Dutch equity returns remained positive after the lower house vote, indicating the market has not priced this as a severe negative in its current form. The tax applies to Dutch taxpayers, not foreign investors holding Dutch-listed assets, which limits the direct international market impact.

The core controversy in unrealised gains taxation is the liquidity problem it creates: investors may owe real tax bills funded from liquid assets or borrowing rather than from sale proceeds, which is why the Dutch Senate’s 36 pages of questions to the Tax Minister focused heavily on illiquid portfolios, valuation disputes, and the risk of forced asset sales rather than the headline rate itself.

The 2026-27 Australian Federal Budget, announced on 12-13 May 2026, introduced two headline capital gains tax measures:

Negative gearing changes announced in the same budget apply only to residential property losses and do not affect equity investors directly.

The reforms had been anticipated for several months before the formal announcement, which reduced the scope for market surprise. This gradual pricing-in illustrates the distinction from South Korea: when a policy change arrives through a formal channel with full government backing, the market has typically begun discounting the probability well before budget night.

Historical evidence from US and UK markets does not consistently show that capital gains rate increases produce sustained equity declines. The relationship between statutory rate changes and market direction is weaker than headline commentary typically implies.

The 14-month implementation lag nonetheless creates a window in which behavioural responses, particularly accelerated asset disposals before the effective date, could themselves shape market dynamics in Australian equities.

ASX asset class positioning under the new regime is not uniform: passive ETFs, dividend-paying blue-chip equities, and superannuation are structurally better placed than high-turnover funds, direct property, and trust distributions, because the interaction between the 30% CGT floor, the removal of the 50% discount, and the trust distribution minimum tax hits each structure differently.

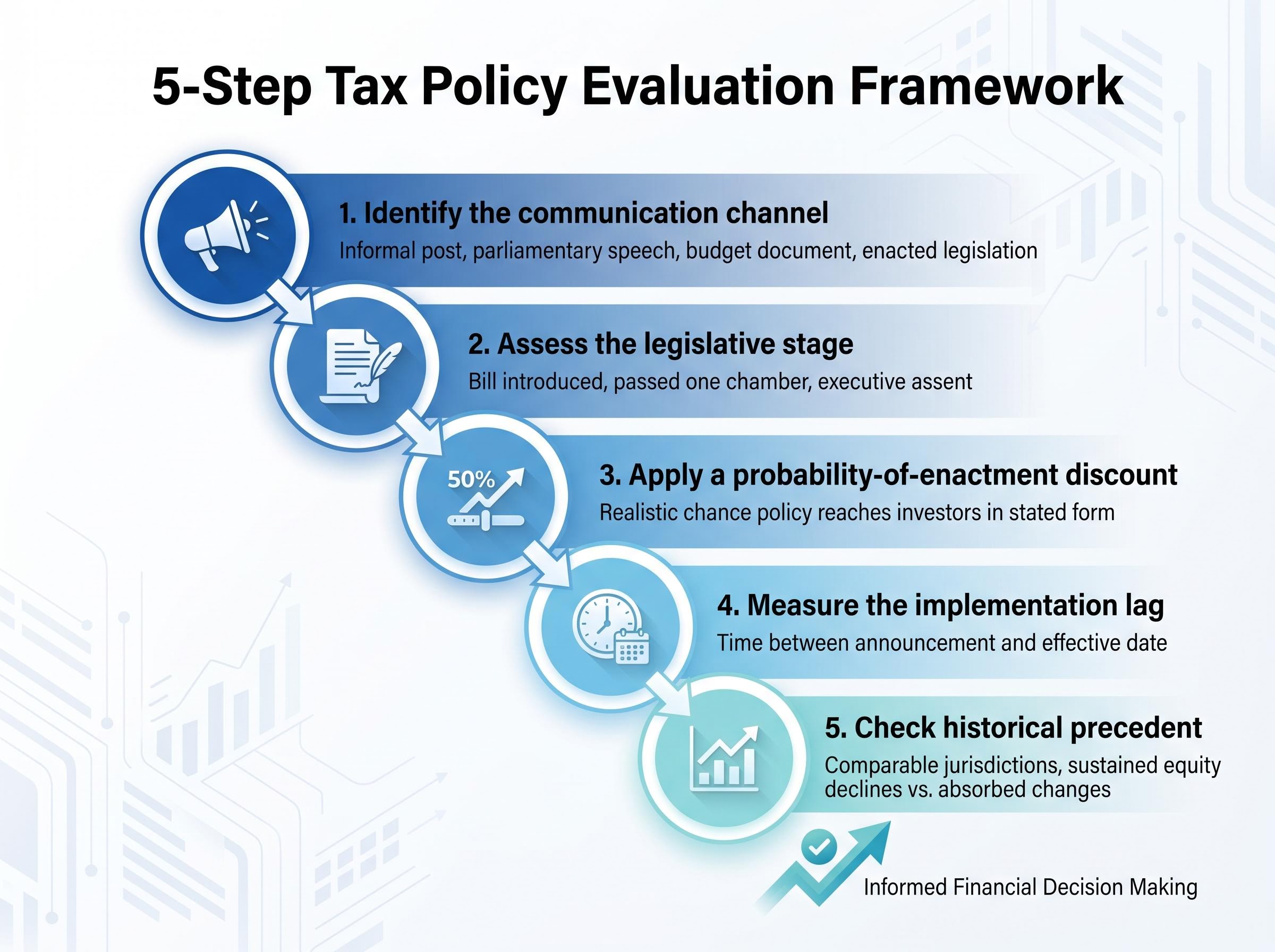

The three 2026 cases supply the raw material for a structured evaluation process. The first question is not “how bad is the rate?” but “what kind of event is this?”

Investors encountering a tax policy headline can apply a five-step checklist:

The behavioural trap is overreacting to severe-sounding numbers. A 36% tax on unrealised gains and a $300 billion market cap erasure are attention-grabbing headlines. Neither, as of mid-May 2026, has produced a sustained equity decline in the affected market or sector.

| Case | Communication Type | Legislative Stage | Analytical Response |

|---|---|---|---|

| South Korea | Informal social media post | None (no bill introduced) | Treat as noise; monitor for clarification before acting |

| Netherlands | Parliamentary vote | Passed lower house; Senate review pending | Discount for amendment probability; assess scope limits |

| Australia | Formal budget announcement | Government-backed; parliamentary passage expected | Higher enactment probability; use implementation lag for positioning |

The speed of recovery is itself informative. South Korea’s full clarification cycle completed within 48-72 hours, with partial recovery confirmed. That rapid reversal is characteristic of a noise event. UK energy sector and Spanish financial sector windfall taxes similarly did not produce sustained stock declines in the affected sectors, reinforcing that even enacted measures are absorbed more readily than announcement-day volatility suggests.

Tax policy risk sits on a spectrum. At one end is noise: communications carrying no legislative substance, such as an advisor’s social media post. At the other end is enacted law with a fixed implementation date and no further amendment path. The market’s task, and the investor’s task, is to locate each new event on that spectrum in real time.

The 2026 cases demonstrate that even severe-sounding enacted provisions do not always produce worst-case market outcomes. Dutch equity returns remained positive after the lower house approved a 36% unrealised gains tax, in part because the scope is limited to Dutch taxpayers (not foreign holders of Dutch-listed assets) and because amendments remain probable. South Korea’s Kospi began recovering within days of the informal clarification, with no formal legislative action required.

Pre-2025 event-study literature confirms a broader pattern: markets tend to over-discount tax policy risk at announcement and partially re-rate as legislative uncertainty resolves.

Sectoral rotation toward franked dividend income is one of the more counterintuitive consequences of the CGT overhaul: removing the 50% discount raises the relative after-tax value of fully franked dividends, which analysts expect to drive increased weighting toward banks, telcos, utilities, and infrastructure on the ASX as the July 2027 effective date approaches.

Policy noise events produce sharper initial selloffs relative to actual legislative risk precisely because the market lacks information to calibrate probability. A Facebook post offers no bill text, no committee analysis, and no vote count to assess. The result is a reaction sized to the worst-case interpretation.

Rapid recovery after clarification is characteristic of noise events. Sustained repricing over months is characteristic of genuine policy signal being absorbed. The distinction is itself a diagnostic tool.

The three 2026 cases confirm that the most important variable in evaluating a tax policy market event is not the severity of the stated rate but the credibility and legislative stage of the communication. Neither the South Korean chip scare, the Dutch unrealised gains law, nor the Australian CGT reform has, as of May 2026, produced a sustained equity market decline in the affected sector or index.

Open questions remain. Whether the Dutch Senate will materially amend the unrealised gains provision could determine how other European jurisdictions approach similar reforms. Whether Australian investors accelerate disposals ahead of July 2027 will shape domestic equity flows. Whether AI-sector taxation re-emerges as a formal policy debate in South Korea will test whether the May noise event was an early signal of a longer political conversation.

Investors encountering the next tax policy headline should apply the evaluation framework before making portfolio decisions: identify the communication channel, locate the proposal on the legislative spectrum, apply a probability discount, and let the speed of any recovery or sustained repricing inform the final assessment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding legislative outcomes and market behaviour are speculative and subject to change based on political developments and market conditions.

Tax policy risk is the possibility that proposed or enacted changes to tax law will reduce the after-tax value of investments, either by increasing rates on gains, dividends, or profits. Markets typically begin pricing this risk at the moment of announcement, not when legislation actually takes effect.

A presidential advisor posted on Facebook about a citizen dividend funded by AI profit taxes, which markets interpreted as a windfall levy targeting Samsung and SK Hynix. Within hours the Kospi dropped around 5%, erasing over $300 billion in market cap, before the presidential office clarified it was a personal view with no new tax proposed.

Investors should apply a five-step check: identify the communication channel, assess the legislative stage, apply a probability-of-enactment discount, measure the implementation lag, and review historical precedent from comparable jurisdictions to see whether similar measures produced sustained declines.

The Dutch Box 3 tax applies only to Dutch taxpayers, not to foreign investors holding Dutch-listed assets, which limits direct international market impact. The legislation passed the lower house in February 2026 but still faces Senate review and probable amendment before its January 2028 effective date.

The 14-month window between the May 2026 budget announcement and the July 2027 effective date may prompt some investors to accelerate asset disposals to lock in the existing discount, while also raising the relative after-tax value of fully franked dividends, favouring banks, telcos, utilities, and infrastructure stocks on the ASX.