Most retail investors researching small-cap stocks spend the bulk of their time on price and valuation. Professional small-cap investors weight management assessment equally. Identifying a cheap stock is only half the problem; the other half is determining whether the people running the business will compound that value or destroy it. The asymmetry matters because approximately 35% of Russell 2000 companies were unprofitable as of June 2024, according to Russell Investments. A universe with that many loss-making operators requires active elimination of low-quality management teams rather than passive exposure. This guide covers the specific frameworks used by professional small-cap investors to evaluate management credibility: how to cross-check claimed track records against per-share returns, the red flags that raise the threshold for proceeding, the dilution mechanics that erode shareholder value, and the valuation discipline that makes management quality assessment and price analysis mutually reinforcing rather than separate exercises.

How dilution hides inside headline growth numbers

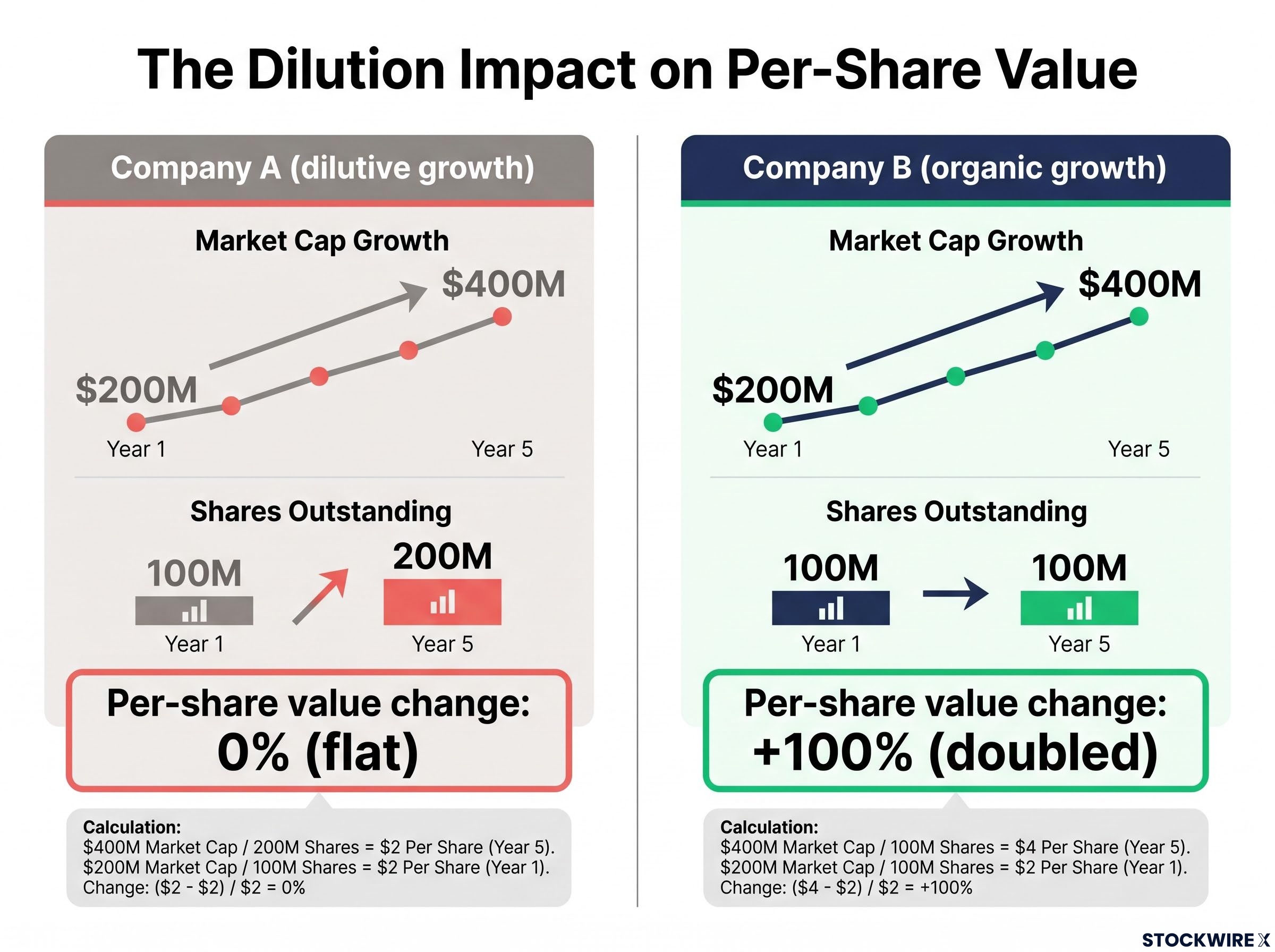

A company’s market capitalisation can double over five years while its long-standing shareholders earn nothing. The mechanism is straightforward: successive equity raises expand the share count, inflating headline figures while diluting each individual shareholder’s claim on earnings and book value.

Management teams frequently cite market-cap growth in investor presentations without disclosing the dilution required to achieve it. Per-share return analysis strips out that distortion. Tracking earnings per share, book value per share, and intrinsic value per share over time reveals whether value is being created for existing shareholders or simply redistributed to new ones.

The professional standard: Cross-referencing stated track records against per-share returns, rather than accepting headline figures at face value, is described by practitioners at Seneca Financial Solutions as one of the most commonly overlooked tools in small-cap analysis.

The distinction becomes concrete when comparing two hypothetical companies, both of which doubled their market capitalisation over five years:

| Metric | Company A (dilutive growth) | Company B (organic growth) |

|---|---|---|

| Market cap: Year 1 | $200M | $200M |

| Market cap: Year 5 | $400M | $400M |

| Shares outstanding: Year 1 | 100M | 100M |

| Shares outstanding: Year 5 | 200M | 100M |

| Per-share value change | 0% (flat) | +100% (doubled) |

Both companies doubled their market cap. Only one doubled shareholder value. The per-share lens is where credibility problems first surface, and it is the foundational quality-control step before any management-presented track record is accepted at face value.

For investors building their first systematic approach to management assessment, our full explainer on per-share fundamental metrics walks through earnings per share, book value per share, return on equity, and revenue growth in a structured framework, covering how to read each metric against sector peers and why no single figure tells the complete story.

When big ASX news breaks, our subscribers know first

Verifying management credibility through independent evidence

Scepticism toward management claims is a starting posture, not an endpoint. The professional process moves beyond doubt into structured verification: checking what management says against what suppliers, competitors, customers, and industry peers observe independently.

According to Ben Richards and Luke Laretive at Seneca Financial Solutions, this verification network is built through sustained engagement, approximately two to four company meetings per day over roughly fifteen years. That cadence generates a contact base across industries deep enough to triangulate any management team’s credibility claims within days.

The quality of information also varies by the type of interaction. Transactional investor-relations meetings, where management delivers a rehearsed pitch, yield qualitatively different data than relationship-based conversations that include candid discussion of operational challenges, competitive threats, and execution risks. The latter generates insights that promotional presentations are designed to omit.

Insider ownership serves as a complementary alignment signal. Madison Small Cap Fund’s March 2026 commentary cited a CEO with an approximately 4% ownership stake in Matador Resources as a meaningful conviction factor, reasoning that significant personal capital at risk aligns management incentives with shareholders more credibly than compensation structures alone.

The distinction between equity granted as compensation and equity purchased with personal capital is central to board alignment and insider ownership analysis, because only the latter puts directors in genuinely the same position as outside shareholders when prices fall.

What retail investors can replicate from this process

Individual investors lack the meeting cadence and industry network that institutional practitioners accumulate over decades. The verification principle, however, is fully transferable.

- Listen to competitor earnings calls for references to the management team or company in question

- Track supplier commentary in industry publications and trade press

- Review employee feedback patterns on platforms such as Glassdoor as a proxy for internal culture

- Cross-reference management statements in shareholder letters against actual delivery in annual reports over three to five years

- Examine former employee profiles on LinkedIn and commentary in regulatory filings for consistency with the company’s public narrative

The objective is triangulation, not confirmation. The reader should actively search for inconsistencies between what management communicates and what the available evidence shows. A single contradiction may have an innocent explanation; a pattern of contradictions rarely does.

Capital raises in small caps: pricing the inevitable

Capital raises are not aberrations in small-cap investing. They are near-certainties. The question is not whether a company will raise equity, but when it will raise, at what price, and how the proceeds will be deployed.

Ben Richards at Seneca Financial Solutions describes a twelve-month signalling standard: credible management teams should be communicating capital raise intentions approximately a year before they occur. This lead time gives investors the opportunity to assess dilution impact, model the effect on per-share value, and adjust position sizing before the event rather than after it.

The net effect of a capital raise on per-share value depends on two variables: the price at which new shares are issued relative to intrinsic value, and the quality of the capital deployment that follows. A raise priced above intrinsic value and deployed into a high-return project can be accretive. A raise priced at a distressed discount and deployed into working capital to cover operating losses is destructive.

A surprise capital raise at a distressed price is not simply a market event. It is a credibility failure, new negative information about management’s transparency, planning, and respect for existing shareholders.

Before any capital raise occurs, four questions sharpen the assessment:

- Has management discussed funding needs at any point in the preceding twelve months?

- At what price relative to intrinsic value would a raise become dilutive to per-share value?

- What specific purpose would the raised capital serve?

- How would the raise affect per-share earnings and book value at the proposed issue price?

Treating dilution as a probability to be priced in advance, rather than a surprise to be absorbed after the fact, changes both position sizing and monitoring discipline over a multi-year holding period.

How red flags stack to break the risk-reward calculation

No single red flag disqualifies a small-cap investment outright. What each flag does is raise the required margin of safety. Stack enough of them and the risk-reward calculus breaks down regardless of price.

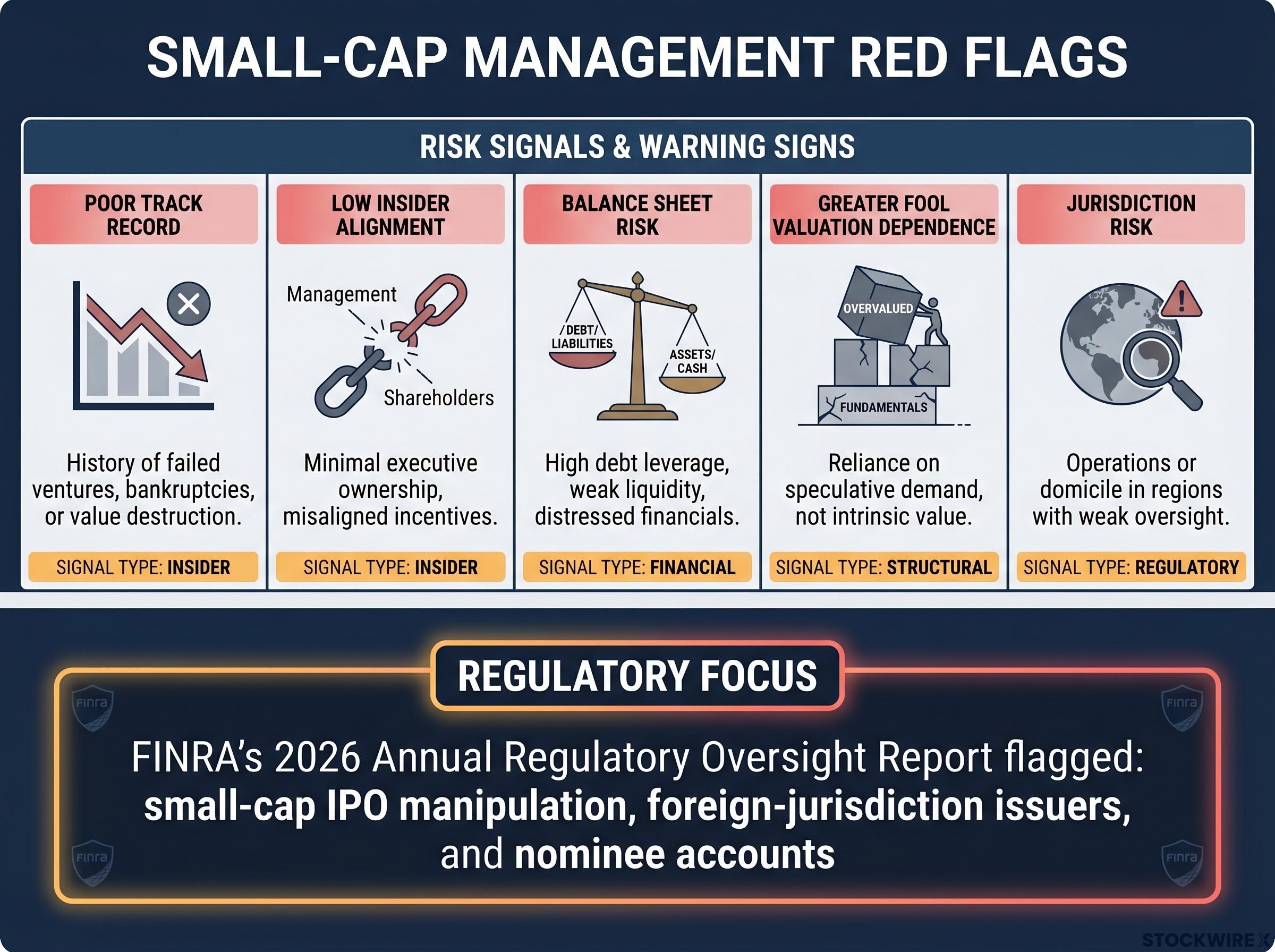

The core red flag categories, as described by Ben Richards at Seneca Financial Solutions, span five dimensions:

| Red flag | Signal type | Observable indicator | Threshold question |

|---|---|---|---|

| Poor track record | Insider | Prior ventures with value destruction or shareholder dilution | Has this team delivered per-share value before? |

| Low insider alignment | Insider | Negligible ownership, compensation misaligned with shareholders | Does management have meaningful personal capital at risk? |

| Balance sheet risk | Financial | High net debt in a cyclical business with volatile cash flows | Can this business service its obligations through a downturn? |

| Greater fool valuation dependence | Structural | Valuation requires a subsequent buyer to pay an even higher price | Does the investment thesis depend on someone else overpaying? |

| Jurisdiction risk | Regulatory | Foreign domicile with uncertain capital repatriation pathways | Can shareholders reliably access the value if the thesis plays out? |

Broader market dynamics reinforce these structural risks. In late 2025, Boston Partners and Marquette Associates identified a rotation toward speculative, pre-revenue names amid retail-driven momentum, with profitable companies temporarily lagging. FINRA’s 2026 Annual Regulatory Oversight Report flagged small-cap IPO manipulation, foreign-jurisdiction issuers, and nominee accounts as ongoing examination priorities, providing external corroboration that these risks are not theoretical.

The FINRA 2026 Annual Regulatory Oversight Report identifies small-cap IPO manipulation, foreign-jurisdiction issuers, and nominee accounts as active examination priorities, confirming that the structural risks associated with jurisdiction and issuer integrity in this asset class are receiving formal regulatory attention.

When a red flag is context-dependent rather than disqualifying

A weak balance sheet in a business where earnings are accelerating rapidly may be an acceptable risk. If management has demonstrated the capacity to service debt, has a credible refinancing timeline, and the earnings trajectory is compressing leverage ratios quarter by quarter, the balance sheet snapshot tells a different story than the balance sheet trajectory.

Context and trajectory matter as much as the static reading. The operative concept is flag stacking: one red flag raises the required margin of safety modestly. Two flags in combination raise it substantially. Three or more in combination may render the investment untenable at any reasonable price, because the probability of management-driven value destruction becomes too high to offset with discount alone.

Why valuation discipline and management assessment are inseparable

Discounted cash flow models carry a specific limitation in small-cap analysis: for early-stage or cyclical businesses, small changes in discount rate assumptions or terminal value estimates produce wildly different outputs. Luke Laretive at Seneca Financial Solutions describes the practitioner emphasis as falling on narrative shifts in consensus multiples rather than precise model outputs. The risk is false precision, a DCF that implies certainty where none exists.

Intrinsic value estimation and margin of safety are reinforcing tools: the terminal value assumption alone typically drives 60-80% of a DCF model’s implied value, which is precisely why small-cap investors who weight management quality heavily are effectively stress-testing the most assumption-sensitive component of any valuation model.

The margin-of-safety alternative resolves this. A wide gap between the current price and any reasonable intrinsic value estimate makes minor modelling errors immaterial. Consider two scenarios:

- A stock trading at 20x earnings against a perceived fair value of 15x implies approximately 25% downside if the thesis is wrong. The margin for analytical error is thin.

- A stock trading at 7x earnings against the same 15x fair value makes modelling assumption errors largely irrelevant. The discount is wide enough to absorb significant analytical imprecision.

Management quality connects directly to this framework. A management team that is credibly compounding per-share value makes a wide margin of safety more defensible, because the intrinsic value estimate has a reasonable probability of rising over time. A management team with multiple red flags requires an even wider margin, because the risk of value destruction offsets the price discount.

Being wrong on a discount rate or terminal value matters much less when a stock is deeply undervalued relative to any reasonable estimate of intrinsic value. The margin of safety is the mechanism that makes qualitative management assessment and quantitative valuation mutually reinforcing.

The contrast between approaches clarifies the practical difference:

- DCF-reliant approach: Key input is discount rate and terminal growth; primary risk is false precision; management quality weighting is low; best suited to stable, predictable businesses

- Narrative-and-margin-of-safety approach: Key input is current price versus reasonable intrinsic value range; primary risk is thesis deterioration; management quality weighting is high; best suited to small caps where forecasting uncertainty is structural

Small-cap price-to-earnings multiples have reportedly traded more than 30% below large-cap averages, though this figure should be treated with caution as it has not been independently verified. If directionally accurate, it contextualises why margin-of-safety approaches are structurally attractive in the asset class: the starting valuation discount provides a larger buffer for the analytical uncertainty that small caps inherently carry.

Buy, hold, and sell decisions as evidence of management quality standards

The frameworks described in earlier sections manifest as observable buy, hold, and sell decisions in professional fund portfolios. Four case studies illustrate the pattern.

Baron Small Cap Fund’s ownership of IDEXX Laboratories over approximately 17 years saw the company’s market capitalisation grow from roughly $2 billion to $41 billion, according to the fund’s Q2 2025 letter. The case demonstrates management quality as a primary return driver: the compounding occurred not because the initial purchase was cheap, but because the management team executed consistently enough to justify holding through multiple market cycles.

Madison Small Cap Fund’s March 2026 commentary highlighted Matador Resources as an example of entrepreneurial culture and insider alignment, with the CEO’s ownership stake cited as a supporting factor in maintaining conviction through periods of sector volatility.

FPA Queens Road Small Cap Value rebalanced toward higher-quality holdings in 4Q 2025, defining quality through earnings consistency, capital allocation discipline, and balance sheet strength. The rebalancing was an explicit quality-rotation decision, not a quantitative screen.

The observable management-quality signals across these cases reduce to four:

- Long-term per-share compounding as evidence of sustained execution

- Insider ownership as an alignment proxy between management and shareholders

- Guidance credibility and consistency of delivery against stated targets

- Leadership stability as a condition for thesis continuity

The sell signal: when management assessment becomes a reason to exit

Baron Small Cap Fund also demonstrated the reverse of the IDEXX case, exiting positions following weakened guidance or missed earnings where management credibility deteriorated. Artisan US Small-Cap Growth cited leadership transitions in its 4Q 2025 commentary as a specific factor that triggered position review or exit, treating unplanned management change as a disruption to the original investment thesis.

The specific deterioration signals that professional managers treated as exit triggers include weakened guidance, missed earnings targets, unannounced leadership transitions, and surprise capital raises. These signals are most useful as confirmations of a pre-existing credibility concern rather than first-time assessments. Ongoing reassessment after entry is as important as pre-entry diligence. Management quality is not a static variable; it requires continuous monitoring against the same per-share return and credibility standards applied at the point of initial investment.

For investors wanting to distinguish genuine thesis deterioration from illiquidity-driven price swings, our dedicated guide to small-cap price volatility examines how professional managers maintained conviction through portfolio drawdowns of 30% or more when no new fundamental information had been released, and outlines a three-question checklist for evaluating any sharp price move before acting.

What separates a management team worth holding from one worth passing on

The professional standard for evaluating small-cap management reduces to five criteria, each covered in the preceding sections and each independently verifiable:

- Per-share return history: Track EPS, book value per share, and intrinsic value per share over time, not headline market-cap growth

- Independent verification: Cross-check management claims through suppliers, competitors, customers, employee commentary, and regulatory filings rather than relying solely on investor-relations presentations

- Capital raise advance signalling: Credible management teams communicate funding needs approximately twelve months before they raise, giving shareholders time to assess dilution impact

- Insider alignment: Meaningful personal ownership stakes and compensation structures that tie management outcomes to shareholder outcomes

- Margin-of-safety pricing: A valuation discount wide enough to absorb modelling error, with the required margin increasing for each red flag present

The threshold question is not whether management is exceptional. It is whether the available evidence is sufficient to justify the risk. In a universe where 35% of Russell 2000 companies are unprofitable and most active managers have historically struggled to outperform, the bar for proceeding is high by default. The process described by Seneca Financial Solutions, two to four meetings per day over fifteen years, represents the professional standard. Retail investors who apply even a partial version of this methodology, particularly per-share return analysis and independent verification, operate at a materially higher standard than the majority of market participants.

Russell Investments small-cap profitability research published in July 2025 placed the share of unprofitable US small-cap companies above 40%, reinforcing why passive exposure to the Russell 2000 carries meaningful management-quality risk that active elimination frameworks are designed to address.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and small-cap investments carry additional risks including lower liquidity and higher volatility.

—