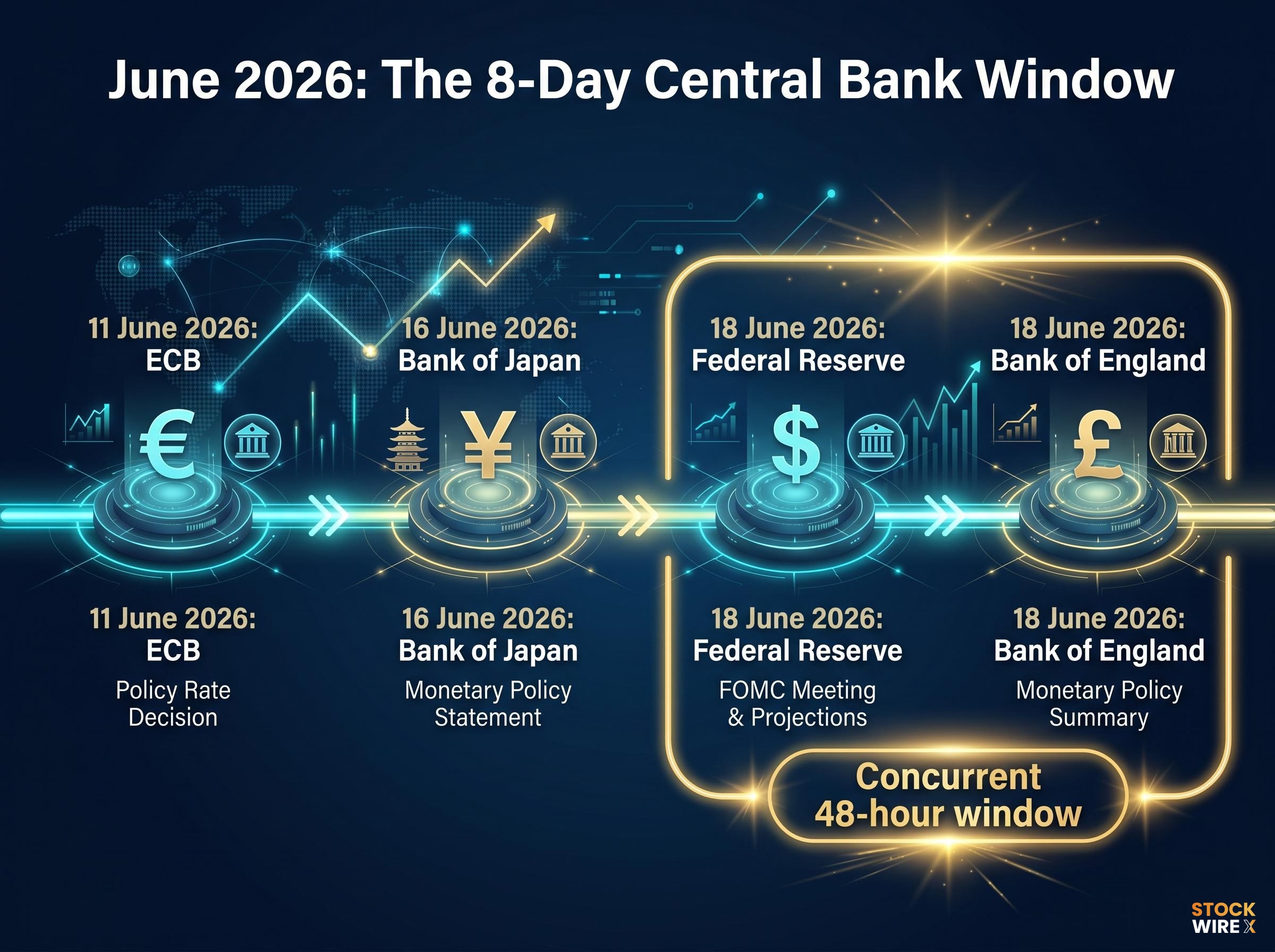

Five of the world’s most systemically important central banks will deliver interest rate decisions within an eight-day window in June 2026. The European Central Bank opens on 11 June, the Bank of Japan follows on 16 June, and the Federal Reserve and Bank of England both land on 18 June, a concentration of policy events with no close modern precedent. The window arrives as policymakers confront genuine macro uncertainty: the Strait of Hormuz has been closed since February 2026, disrupting roughly a quarter of global seaborne oil trade, and a late-May ceasefire has raised hopes for gradual supply normalisation without guaranteeing it. Simultaneously, the Federal Reserve is preparing for its first meeting under new Chair Kevin Warsh, whose publicly expressed scepticism toward core Fed communication tools has placed market participants on alert for procedural as well as policy signals. This analysis maps each institution’s specific policy dilemma, explains why the clustering of decisions amplifies rather than merely adds market risk, and identifies the cross-asset channels most exposed to simultaneous or divergent signals from the June window.

Eight days that rewrote the central banking calendar

The schedule itself tells a story. Four institutions, four decisions, eight days, and a closing act on 18 June in which the Fed and the Bank of England move within the same 48-hour window.

| Institution | Decision date | Primary policy dilemma |

|---|---|---|

| ECB | 11 June 2026 | Reading the inflation trajectory under heavy energy import exposure to the Hormuz disruption |

| Bank of Japan | 16 June 2026 | Managing the conflict between domestic inflation and yen pressure driven by near-total oil import dependence |

| Federal Reserve | 18 June 2026 | First meeting under new Chair Kevin Warsh; communication posture as consequential as the rate itself |

| Bank of England | 18 June 2026 | Concurrent with the Fed decision, compressing market digestion of two G10 outcomes into a single session |

Why compression matters more than volume

In a typical month, markets absorb one major central bank signal, reprice, and then prepare for the next. That sequential digestion breaks down when four systemically important institutions move in a single trading week. Each additional decision is not simply more news; it is a multiplier on the speed at which markets must process conflicting or reinforcing signals. When the ECB’s tone on 11 June has not yet been fully digested before the BoJ speaks on 16 June, and both feed into the interpretive frame applied to the Fed and BoE just two days later, the compounding effect is structural, not arithmetic.

When big ASX news breaks, our subscribers know first

The energy shock that every policymaker in the room is watching

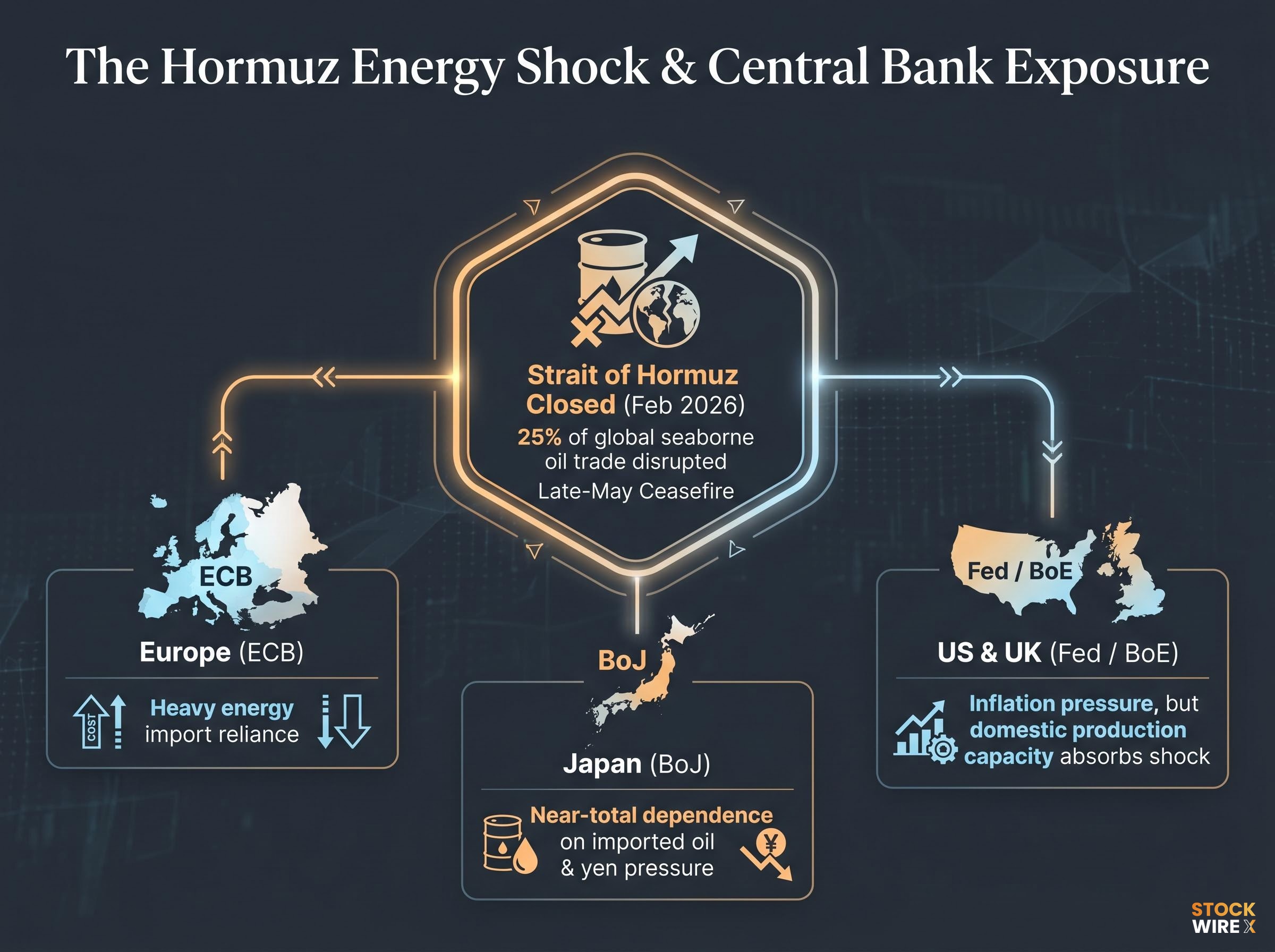

The Strait of Hormuz has been closed since February 2026, and its effects have not remained contained to the oil market. The disruption has rippled through manufacturing input costs, freight rates, and consumer energy bills across every major economy represented in the June window.

The closure has disrupted approximately 25% of global seaborne oil trade, embedding inflationary pressure into the global economy for more than three months.

The World Bank Commodity Markets Outlook, published in April 2026, quantified the supply disruption at approximately 10.1 million barrels per day removed from global markets in March alone, a figure that contextualises why the Hormuz closure has generated persistent inflationary transmission rather than a brief price spike.

A diplomatic breakthrough reached in late May has raised the prospect of a gradual reopening. If the ceasefire holds, Brent crude could retreat toward pre-conflict levels over time. That word, “gradually,” carries real weight: inflationary effects already embedded in freight contracts, manufacturing supply chains, and energy hedging positions since February will not unwind within weeks, even under the most optimistic scenario.

The Hormuz oil risk premium is not expected to decompress quickly even under a confirmed ceasefire, with the IEA projecting a two-year supply chain recovery timeline and VLCC daily hire rates tracking near $110,000 per day as a real-time measure of how far physical markets remain from normalisation.

What makes this relevant to every June decision is that policymakers cannot yet know whether the ceasefire will prove durable or how quickly energy prices will respond. They must set rates in an environment of genuine uncertainty about whether the single largest common input cost is rising, stable, or beginning to fall.

The exposure is not uniform:

- Europe faces among the highest vulnerability due to heavy reliance on energy imports, making the ECB’s inflation read directly sensitive to the pace of supply normalisation

- Japan is exposed through near-total dependence on imported oil, amplifying yen pressure and complicating every dimension of BoJ calibration

- The United States and United Kingdom face the same directional pressure on inflation, though with somewhat greater domestic energy production capacity to absorb the shock

This shared backdrop is what transforms the June window from a busy calendar week into a moment of synchronised policy uncertainty.

How the ECB and Bank of Japan are navigating the same pressure from opposite starting points

The ECB and BoJ face the same external energy shock. The similarity ends there. The structural differences between the two economies mean the same disruption produces opposite policy tensions, and the sequencing of their decisions within the eight-day window adds an additional layer of analytical complexity.

ECB: reading the signal on the normalisation runway

The ECB delivers first, on 11 June. Europe’s energy import dependence means the Hormuz closure has fed directly into the eurozone’s inflation readings, and the ECB’s assessment of whether that pressure is peaking, persistent, or beginning to ease will carry weight well beyond Frankfurt.

For global markets, the ECB’s tone functions as a signal for how much runway remains in the broader rate normalisation cycle. A hawkish hold suggests energy-driven inflation is proving stickier than hoped, tightening the window for rate reductions across other jurisdictions. A dovish lean, particularly if tied to early ceasefire effects on energy costs, could open space for other central banks to follow.

Because the ECB moves five days before the Fed, its signal will shape the interpretive frame markets carry into every subsequent June decision.

Bank of Japan: when your currency and your inflation point in different directions

The BoJ follows on 16 June, and its dilemma is among the most complex of any institution in the window. Japan’s near-total dependence on imported oil means the Hormuz closure has simultaneously pushed domestic inflation higher and weakened the yen, as elevated energy import costs widen the trade deficit.

Bank of Japan analysis of import price transmission documents how rising energy raw material costs, including crude oil, propagate through Japan’s producer price indexes before reaching consumer prices, a sequencing that lengthens the lag between a commodity shock and its full inflationary impact on domestic demand.

The tensions the BoJ must weigh include:

- Tightening policy to address above-target inflation, which risks further economic slowdown

- Holding or easing to support growth, which risks accelerating yen depreciation and importing even more inflation through energy costs

- Calibrating communication in the knowledge that whatever the Fed signals two days later on 18 June could shift yen dynamics regardless

Even by the BoJ’s own historically complex standards, the June meeting represents an unusually constrained set of options.

Kevin Warsh’s first meeting and what happens if the Fed stops explaining itself

The federal funds rate has held at 3.50-3.75% across three consecutive FOMC meetings heading into June, and the 17-18 June session is not widely expected to produce an immediate change. The market-moving variable is not the rate itself. It is how the Fed communicates.

For over a decade, two tools have anchored the way markets price future US rate expectations:

The dot plot (the quarterly chart showing each FOMC member’s interest rate projection) and the post-meeting press conference (which allows the Chair to contextualise the decision in real time) have become the primary instruments through which forward expectations are set.

Warsh has previously expressed scepticism toward both. His concerns, drawn from pre-Chair commentary, centre on whether these tools constrain future policy flexibility by pre-committing the Fed to market-implied paths:

The four FOMC dissents recorded at the April 28-29 meeting, the most at any single Fed meeting since 1992, represent the fractured committee inheritance Warsh receives at the June meeting; the 30-year Treasury yield reaching 5.14% in May has tightened financial conditions independently of the rate itself, adding another dimension to whatever communication posture he adopts.

- The dot plot provides a visible map of where individual FOMC members expect rates to land in coming years, which markets treat as soft guidance. Removing or downgrading it would force participants to price rate expectations from economic data alone, without the anchor of the Fed’s own projections.

- Post-meeting press conferences allow the Chair to shape narrative in real time. Any signal that Warsh intends to reduce their frequency or specificity would widen the interpretive gap between what the Fed decides and what markets believe the Fed intends next.

The June meeting’s quarterly economic projections will be the first window into how new Fed leadership assesses the US economy under current conditions: inflation running materially above the 2% target, a cooling labour market, and Hormuz-related energy uncertainty that remains unresolved. Whether Warsh treats the projections as authoritative guidance or begins to distance the institution from them will be a signal in itself.

A Fed that stops pre-signalling is a structurally different counterparty for every risk asset priced against US rate expectations.

Why June 18 is the most concentrated 48 hours in recent market history

The Bank of England and the Federal Reserve both deliver decisions on 18 June 2026. The two most closely watched central banks outside Asia will move before markets can fully absorb either outcome individually.

Under normal conditions, currency markets process central bank signals sequentially. A Fed decision reprices the dollar, and participants adjust GBP/USD positioning in the days that follow before the BoE speaks. On 18 June, that digestion window collapses. GBP/USD, US Treasuries, UK gilts, and global equity risk appetite will all be exposed to simultaneous repricing from two independent policy signals.

The BoE’s own decision context is shaped by the same inflationary and energy cost pressures affecting the broader June window. Its signal is not isolated from the Hormuz disruption or the global rate normalisation question; it is embedded within both. The concurrent timing simply means its market impact will be processed in parallel with the Fed’s rather than in sequence.

The asset classes most directly exposed to the 18 June concurrent dynamic include:

- GBP/USD, which faces simultaneous directional inputs from both institutions

- US Treasuries, repricing on the Fed signal while absorbing spillover from the BoE

- UK gilts, sensitive to the BoE decision and to any divergence from the Fed’s tone

- Global equity risk appetite, which must absorb conflicting or reinforcing signals within a single trading session

The cross-asset fault lines running through the June window

The preceding institutional analyses converge on a single question: what happens when signals from four central banks interact within a compressed trading week, rather than arriving in the orderly sequence markets are built to process?

Three primary channels carry the risk.

| Asset class | Primary central bank driver(s) | Risk scenario |

|---|---|---|

| EUR/USD | ECB (11 June) vs Fed (18 June) | Divergent tone on inflation trajectory compresses repricing into days rather than weeks |

| USD/JPY | BoJ (16 June) and Fed (18 June) | BoJ yen management complicated by Warsh communication shift; oil-import vulnerability adds commodity dimension |

| GBP/USD | BoE and Fed (both 18 June) | Simultaneous outcomes eliminate the sequential digestion that normally separates two G10 signals |

| Sovereign bond yields | All four institutions | Yield moves across major markets interact and amplify within a single week rather than across a full cycle |

| Global equities | All four institutions | Conflicting directional signals from divergent central banks pressure risk appetite within a condensed window |

The amplification dynamic is straightforward: yield moves and currency repricing that markets would normally absorb sequentially across weeks could interact within a single trading session if signals diverge.

The ceasefire introduces a counterweight to the pure volatility narrative. If Brent crude retreats toward pre-conflict levels, the inflationary impulse could ease across multiple jurisdictions simultaneously, potentially producing a coordinated softening of tone from several institutions at once, the relief scenario that would reduce rather than amplify cross-asset stress.

The next major ASX story will hit our subscribers first

What this window tells us about how interconnected monetary policy has become

June 2026 is not an anomaly in the calendar. It is a demonstration of how tightly coupled central bank policy cycles have become. Four institutions nominally operating independently are shaped by the same energy shock, the same above-target inflation dynamics, and the same currency cross-effects from each other’s decisions.

The Asian rate tightening cycle triggered by Bank Indonesia’s shock 50-basis-point hike in May 2026 illustrates how the same Hormuz-linked energy costs and dollar strength that shape the four June G10 decisions are simultaneously pressuring emerging market central banks into defensive hikes, with Goldman Sachs projecting the Bank of Korea, Reserve Bank of India, and Taiwan’s central bank to follow in H2 2026.

The Warsh communication uncertainty adds a new variable to this interdependence. A Fed that provides less forward guidance does not reduce uncertainty; it redistributes it. Every asset class priced against US rate expectations, and every central bank calibrating its own stance relative to the Fed’s, would need to operate with a wider margin of ambiguity. The cost of that ambiguity is not evenly distributed; it concentrates in the currency and fixed income markets that rely most heavily on the Fed’s forward signalling infrastructure.

How each institution navigates the June window will itself become a signal. The ECB’s willingness to move first sets a tone. The BoJ’s handling of its yen-inflation conflict reveals the limits of independent calibration under a shared shock. The Fed’s communication posture under Warsh establishes the informational baseline for the remainder of 2026. And the BoE’s concurrent decision with the Fed tests whether markets can process two G10 outcomes simultaneously without dislocating.

The resolution of these eight days will shape rate expectations and central bank credibility through the second half of 2026.

June 2026 as the stress test no policymaker scheduled but every investor must prepare for

Three compounding uncertainties define the June window:

- The energy price trajectory under a ceasefire that is real but whose durability remains unknown, with inflationary effects embedded in global supply chains since February

- The communication posture of a new Fed Chair whose scepticism toward forward guidance tools could alter the informational structure markets have relied on for over a decade

- The possibility of divergent or reinforcing signals from four institutions within eight days, a compression that eliminates the sequential digestion markets are built around

The federal funds rate at 3.50-3.75% is the baseline from which any June signal will be read. Three consecutive holds have placed the Fed in a prolonged pause, making the quarterly economic projections under Warsh the most concrete near-term data point on how new leadership reads the US economic path.

The late-May ceasefire entered the picture after those three consecutive holds, shifting the inflationary calculus for every institution simultaneously. Whether it holds, and how quickly energy prices respond, is genuinely unknown at the time each policymaker enters the room.

How each institution communicates its decision will matter as much as the decision itself. The June window will not resolve in a single week; its outcomes will shape the rate cycle narrative, market positioning, and central bank credibility through the second half of 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding central bank decisions, energy market developments, and asset price movements are speculative and subject to change based on evolving economic conditions.