Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

54 mins ago

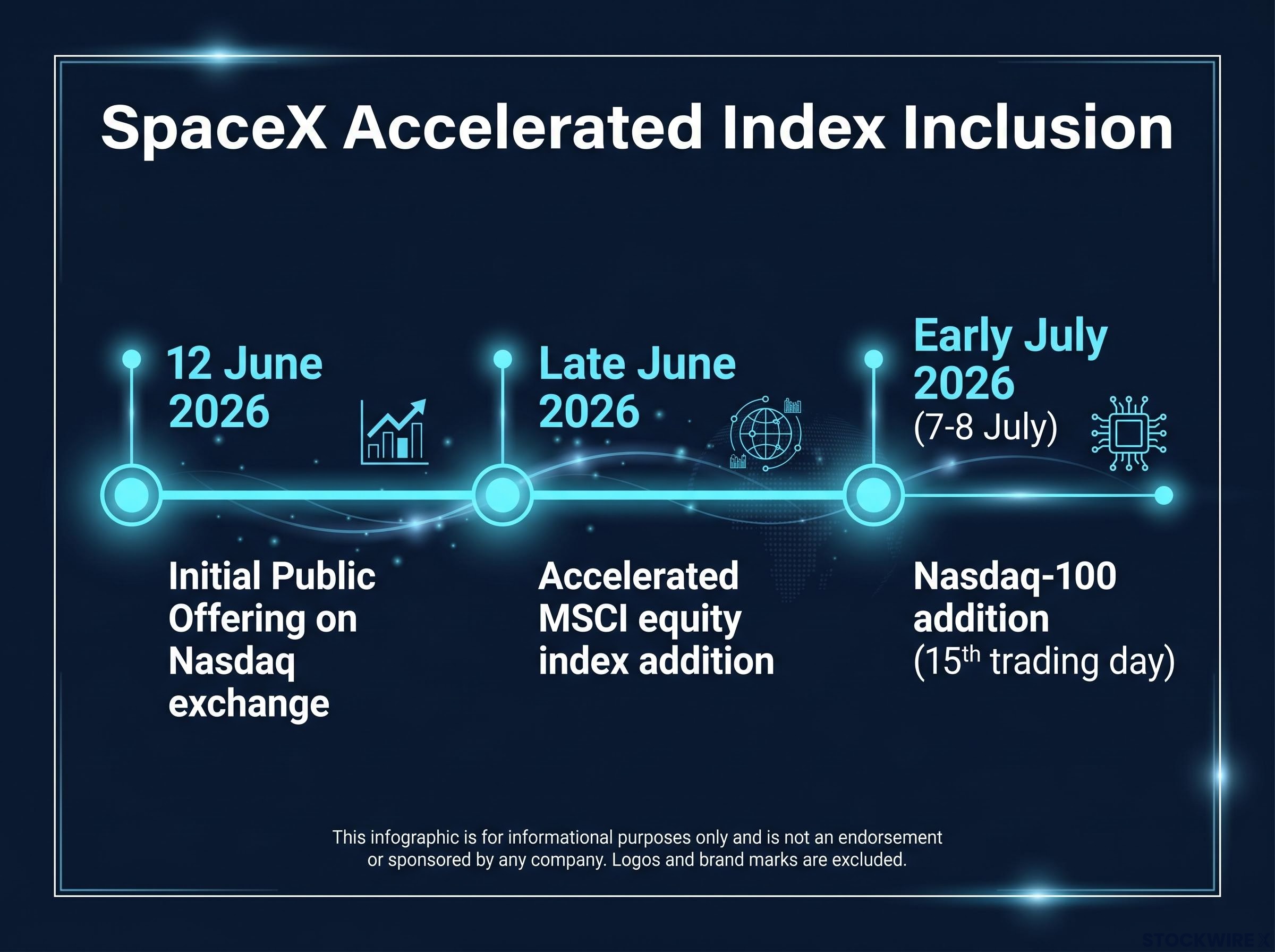

SpaceX joined the Nasdaq-100 on its 15th day as a publicly traded company, one of the fastest index entries on record. The June 12 IPO, an expedited MSCI inclusion in late June, and a Nasdaq-100 addition in early July 2026 compressed what normally takes months into a timeline measured in weeks.

If you own a Nasdaq-100 fund such as QQQ or QQQM, that speed matters for a specific reason: you now hold SpaceX whether you chose to or not. The stock entered your portfolio through index rules, not through any decision you made. That is already the case for millions of investors.

Here is what actually happened, what it means mechanically, and how to think about it without making a move you will regret. The structural facts separate cleanly from the noise once you see how the pieces fit together.

The sequence was fast enough to feel disorienting. Three separate index events unfolded in under a month:

The Nasdaq-100 tracks 100 of the largest non-financial companies listed on the Nasdaq exchange. Widely regarded as a leading technology-oriented benchmark globally, it underpins hundreds of ETFs and managed funds built to mirror its composition.

SpaceX entered at a market capitalisation of approximately $2 trillion, with an estimated weight of roughly 1% of the index. That weight may land well under 1% once free-float adjustments are applied.

The IPO record claims around SpaceX are more complicated than the headlines suggest: in nominal terms SpaceX raised $75 billion, a genuine record, but Aramco’s 2019 proceeds convert to roughly $2.21 trillion in 2026 dollars, meaning the valuation record does not hold in real purchasing-power terms.

The speed of this sequence tells you something distinct from the IPO itself. Market infrastructure, the indices, the fund providers, the rebalancing calendars, is actively reorganising around SpaceX. That is a structural signal worth understanding on its own terms.

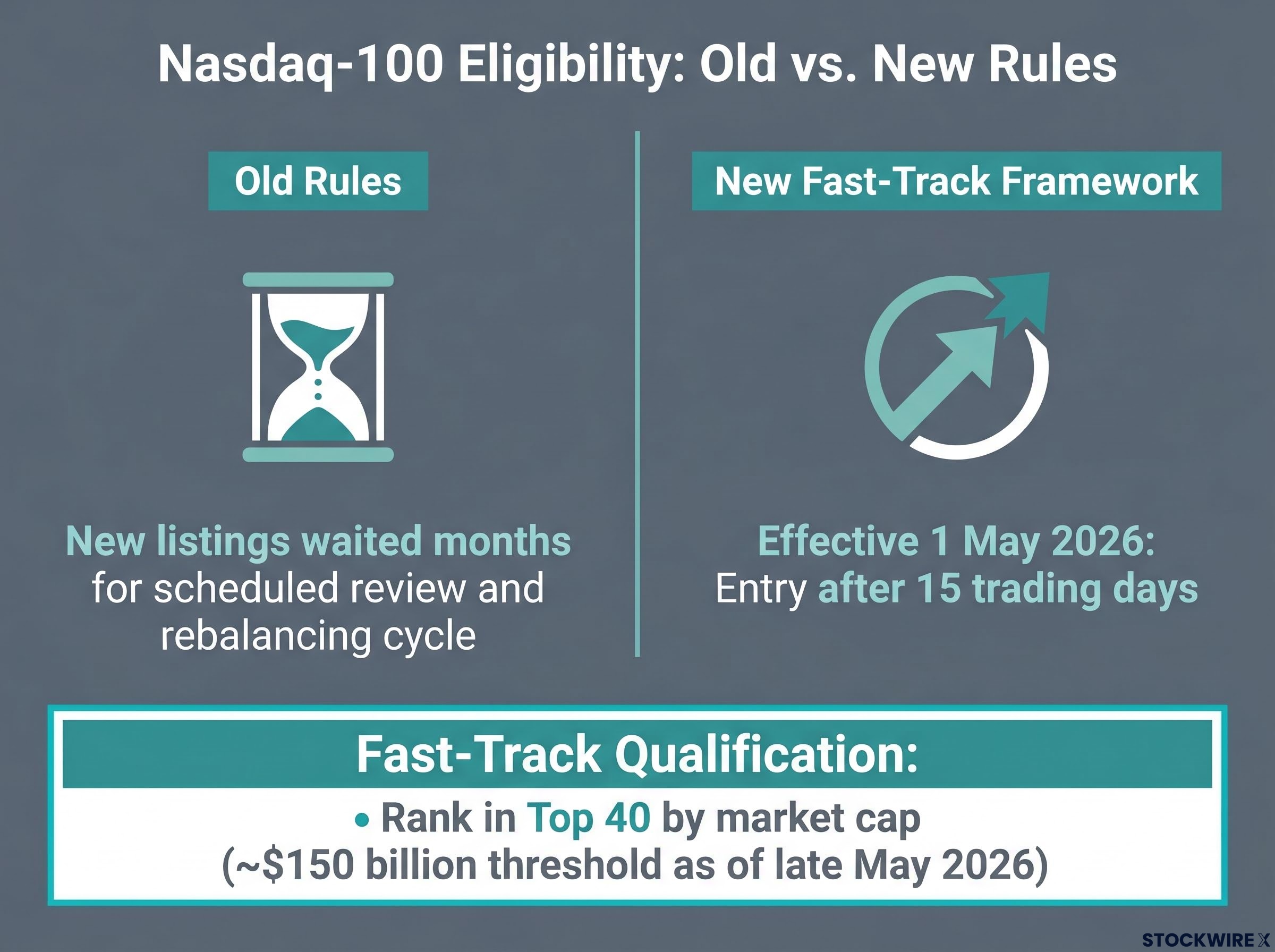

SpaceX did not receive a special exemption. It entered the Nasdaq-100 under a new eligibility framework, effective 1 May 2026, that applies to any qualifying large IPO going forward.

Under the previous rules, newly listed companies waited for the Nasdaq-100’s standard review cycle before they could be considered for inclusion. That cycle could take months. The revised rules introduced a fast-track pathway:

The bar is high. A company must be large enough at listing to rank in the top 40 of the Nasdaq-100 by market cap. SpaceX, at roughly $2 trillion, cleared it by a wide margin. OpenAI is the most frequently cited candidate that could follow the same path if and when it lists publicly.

The rule change reframes SpaceX’s rapid inclusion entirely. This is not an anomaly to be explained away. It is the first real-world test of a policy that will define how the next generation of very large IPOs interacts with the passive investing infrastructure that underpins trillions of dollars in retirement and brokerage accounts.

Every ETF and fund that tracks the Nasdaq-100 must now buy SpaceX shares to match the benchmark. That is not optional. It is rules-based demand, estimated at over $4 billion in forced passive inflows.

Over $4 billion in estimated passive buying flowed into SpaceX shares as a direct result of index inclusion. This is a mechanical fact about fund rebalancing, not a judgement about whether the stock is fairly valued at its current price.

That distinction matters because it is easy to conflate. The buying is real, but it tells you nothing about SpaceX’s revenues, competitive position, or long-term outlook.

| What index inclusion does | What index inclusion does not do |

|---|---|

| Forces passive funds to buy the stock | Change SpaceX’s revenues, profits, or competitive position |

| Increases visibility and institutional access | Validate SpaceX’s valuation at the current price |

| Creates a one-time surge of rebalancing flows | Guarantee sustained price appreciation after rebalancing |

At entry, SpaceX represents roughly $1 of every $100 invested in a Nasdaq-100 fund. That makes the direct portfolio impact real but modest. If you own QQQ, you own SpaceX now, but it is not reshaping your returns on its own.

The $4 billion in mechanical buying and the fundamental question of whether SpaceX is worth owning at $2 trillion are two separate questions. In the weeks immediately following inclusion, they are particularly easy to conflate, and particularly important to keep apart.

When market infrastructure rushes to incorporate a high-profile company across multiple indices within weeks, it often reflects elevated enthusiasm around growth themes. That makes SpaceX’s rapid, multi-index inclusion a sentiment data point worth taking seriously.

Signals that suggest elevated enthusiasm:

Signals that suggest sentiment has not yet tipped into unrestrained euphoria:

Fisher Investments noted that elevated investor enthusiasm is not, by itself, a reliable bearish signal, and that bull markets have historically persisted for extended periods, sometimes years, even when sentiment runs hot.

The ambiguity itself is informative. A market in the grip of unrestrained euphoria typically does not produce the kind of hesitation and volatility visible in SpaceX’s first weeks. That should temper both the bulls and the bears.

The passive buying story from index inclusion is only half of the supply-and-demand picture. The other half arrives in the months ahead.

Lock-up periods, the contractual windows that prevent company insiders from selling shares immediately after an IPO, typically expire 90-180 days after listing. When they do, large blocks of insider-held shares become available for sale, increasing the supply of shares in the market.

The SpaceX lock-up schedule is considerably more complex than a standard 180-day cliff, with roughly 12 distinct unlock events and a performance trigger that could release an additional 10% of eligible insider shares before Q2 earnings, concentrating potential supply pressure in specific windows rather than spreading it evenly.

Neither force cancels the other out. They operate simultaneously, and their interaction creates a specific volatility risk in the post-IPO, post-inclusion window. The passive inflows are largely a one-time event concentrated around rebalancing dates. The lock-up expirations introduce potential selling pressure that unfolds over a longer period.

For investors watching SpaceX in the coming months, this dynamic is worth monitoring. It does not predict a direction, but it does mean the post-inclusion period is more complicated than a simple demand-driven price support story.

If you hold QQQ, QQQM, or any other Nasdaq-100 tracking fund, SpaceX is already in your portfolio at a weight of roughly 1%. No action is required on your part. The addition is consistent with the fund’s existing growth and technology tilt, and your exposure is real but small.

If you do not own Nasdaq-100 products, SpaceX’s inclusion is not, by itself, a reason to buy them. Decisions about owning QQQ-style funds should rest on whether they fit your overall asset allocation, not on a single high-profile stock joining the index.

Fisher Investments argued that allowing excitement or concern about a prominent index addition to steer portfolio choices is a mistake, and that building wealth more reliably comes from maintaining patient, compounding exposure across a globally diversified portfolio.

For the vast majority of investors, the correct response to SpaceX’s Nasdaq-100 addition is no portfolio change at all. The value is in understanding why that non-decision is the right one.

The passive investing evidence underpinning the recommendation to hold QQQ-style funds without reacting to headline additions is structural rather than anecdotal: over 90% of active large-cap fund managers underperform the S&P 500 across a 20-year horizon, a failure rate that William Sharpe’s arithmetic confirms is unavoidable in aggregate after fees.

The mechanical layer is largely settled. The rules are clear: the fast-track framework effective 1 May 2026 applies to all qualifying large IPOs, not just SpaceX. The passive inflows, estimated at over $4 billion, have flowed or are flowing. The weight, approximately 1% of the Nasdaq-100 at entry, is established.

What remains genuinely open is the fundamental question: whether SpaceX at approximately $2 trillion is attractively valued for the long term. Index inclusion does not answer that. It never does.

Future mega-IPOs will encounter this same fast-track framework, making SpaceX’s entry a policy precedent as much as a market event. The next time a company lists at a valuation large enough to rank in the top 40, the same 15-day window will apply, and the same mechanical forces will activate.

Future mega-IPOs such as OpenAI and Anthropic would trigger the same fast-track sequence if they list at valuations large enough to rank in the Nasdaq-100’s top 40, and Bloomberg strategists have already flagged the concentration risk of an AI super-cap cluster forming inside the benchmark.

The disciplined investor’s position on any index addition, this one included, is informed awareness without reactive action. Understanding the mechanics is useful. Changing your portfolio because of them is usually not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Effective 1 May 2026, Nasdaq introduced a fast-track eligibility framework that allows newly listed companies to join the Nasdaq-100 after just 15 trading days, provided they rank among roughly the top 40 holdings by market capitalisation, a threshold estimated at around $150 billion. SpaceX, listing at approximately $2 trillion, cleared that bar by a wide margin.

Yes. Every ETF and fund that tracks the Nasdaq-100, including QQQ and QQQM, is required by its rules to hold SpaceX at its index weight of roughly 1%, so if you owned those funds at the time of rebalancing, SpaceX entered your portfolio automatically without any action on your part.

Index inclusion triggered an estimated $4 billion or more in forced passive inflows as funds tracking the Nasdaq-100 bought SpaceX shares to match the benchmark; this is a mechanical consequence of rebalancing rules, not a signal about whether the stock is fairly valued.

The primary risk is the interaction between the one-time passive inflows from index rebalancing and the phased unlock of insider shares through SpaceX's lock-up schedule, which involves roughly 12 distinct unlock events and a performance trigger that could release an additional 10% of eligible insider shares before Q2 earnings, creating concentrated windows of potential supply pressure.

For investors who already hold Nasdaq-100 funds, no action is required; SpaceX is already included at roughly 1% and is consistent with the fund's existing technology tilt. For those who do not own Nasdaq-100 products, SpaceX's inclusion alone is not a valid reason to buy them, as that decision should rest on overall asset allocation, not a single high-profile index addition.