10 Approved Rivals, Yet S&P Global’s Moat Keeps Compounding

1 hr ago

FactSet has lost roughly half its market value in under two years. The stock peaked near $484 in November 2024 and traded around $242 in early July 2026, a scale of de-rating typically reserved for businesses facing existential change. The question worth asking is not whether the selloff is justified. It is whether the market has priced the right risk, or simply the loudest one.

The decline followed a broader pattern. Reuters reported that AI tool launches, including from Anthropic, triggered a sweeping selloff across data analytics and software names as investors repriced displacement risk across information services. The investment debate now centres on whether financial data incumbents are genuinely disrupted, or whether the AI disruption narrative has been applied too bluntly across business models with very different structural defences.

Here is a working framework for separating the two. What follows distinguishes the financial data businesses that face real near-term displacement from those carrying structural moats that the current AI-discount trade is failing to price correctly, and it gives you the specific screening axes to apply to any name in the sector.

The same price chart reads two ways. For one camp, FactSet’s roughly 50% decline from its November 2024 high to approximately $242 in mid-2026 is warranted disruption pricing: a desktop terminal model losing its relevance as AI-native tools eat into its core use case. For the other, it is a case study in market overreach, where fear of a technology shift has compressed the multiple of a business with high recurring revenue, strong cash generation, and emerging AI monetisation.

Both readings contain something real. The selloff was not a single event but an accumulation of three trigger categories:

Redburn’s core thesis: Clients will increasingly consume financial data “in an unbundled way,” bypassing the proprietary terminal interface entirely in favour of API-fed, AI-native workflows.

That thesis is analytically sound for the terminal segment specifically. Where it overgeneralises is in applying the same unbundling logic to embedded infrastructure businesses that operate under entirely different switching cost dynamics. The 50% de-rating tells you the terminal model faces real structural pressure. It does not tell you that every financial data business deserves the same discount.

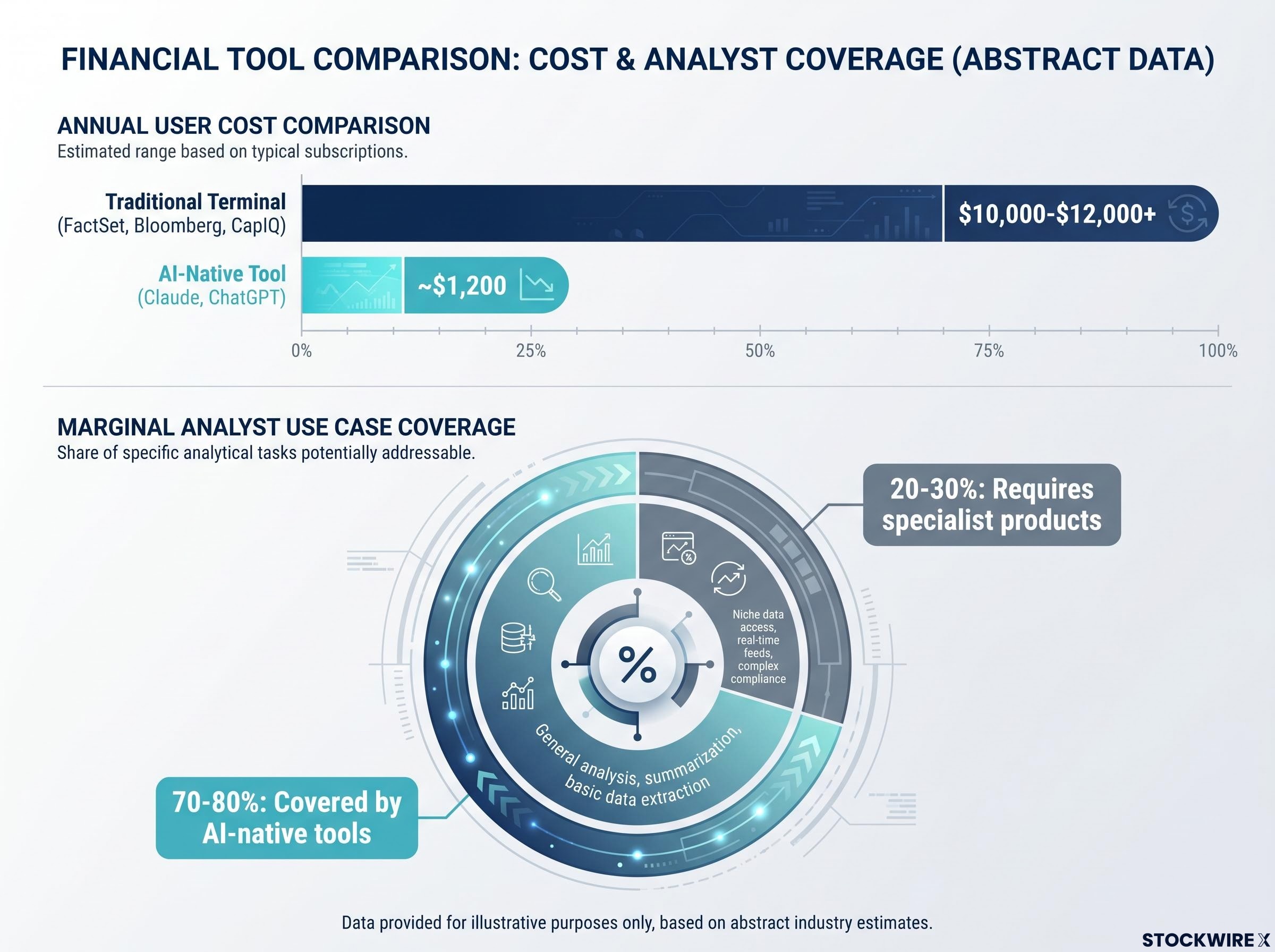

The cost comparison is where the displacement thesis moves from theory to arithmetic. Annual licensing for a FactSet terminal seat runs in the region of $10,000, while AI-native research tools from providers like Anthropic and OpenAI are coming to market at around $100 per user per month, equating to roughly $1,200 annually. The gap between those two figures is not a rounding difference; it spans an entire order of magnitude.

The order-of-magnitude cost gap between terminal licensing and AI-native alternatives is a specific instance of a broader structural shift: per-seat pricing vulnerability is now the central liability for any analytical software business whose core deliverable is information access rather than workflow execution.

| Tool Category | Approximate Annual Cost Per User | Primary Switching Cost |

|---|---|---|

| Traditional terminal (FactSet, Bloomberg, CapIQ) | $10,000-$12,000+ | Interface retraining, migrated settings (low operational risk) |

| AI-native research tool (Claude, ChatGPT) | ~$1,200 | Minimal; subscription-based, no integration layer |

| Embedded workflow platform (loan/ECM systems) | Varies widely | Multi-month integration, compliance sign-off, parallel runs |

For a marginal analyst whose workflow is primarily search and document analysis, AI-native tools can cover an estimated 70-80% of use cases. The remaining 20-30% may require specialist products, but the full terminal bundle is no longer the only way to access what most users need most of the time.

The terminal model’s moat has always been behavioural and experiential, not structural. Terminal contracts tend to run on multi-year cycles, with clients using renewal negotiations as leverage to extract pricing concessions. When a firm does change providers, the practical disruption amounts to little more than staff retraining and the transfer of saved settings.

Contrast that with embedded systems. Replacing a loan management platform or regulatory reporting tool inside an investment bank involves multi-month integration projects, parallel runs, data migration, and compliance sign-off. The cost of failure (missed trades, broken reporting, operational losses) dwarfs the annual software fee. That distinction, switching cost heterogeneity, is the single most important variable in assessing AI displacement risk across financial data businesses. AI capability alone is not the deciding factor.

The market has treated “financial data infrastructure” as a coherent asset class with uniform AI exposure. It is not. It contains two fundamentally different risk profiles that happen to share an industry label.

RBC Capital Markets has argued that vertical platforms managing deep regulatory configurations are effectively AI-proof, because replicating years of embedded compliance context is far harder than rebuilding an interface; a five-question framework for separating defensible SaaS platforms from genuinely displacement-exposed software businesses applies the same logic at the individual stock level.

Morgan Stanley drew the line explicitly in research on AI disruption moats, distinguishing between data owners and ecosystem linchpins on one side and pure aggregators on the other. Firms like MSCI (indices) and Moody’s (ratings) own branded datasets that function as a common language for markets. Their value is tied to trust, regulation, and network effects, not the delivery interface. AI does not erase the economics of those franchises.

Morgan Stanley’s framing: Integration into client workflows is a core moat that makes disruption “costly and risky,” positioning deeply embedded products as utilities rather than discretionary research tools.

The embedded infrastructure calculus operates on different terms entirely. When a product touches revenue-generating or compliance-critical processes, operational and regulatory risk dominates over interface preference. Three conditions characterise genuinely high-switching-cost infrastructure:

If a financial data business you are evaluating meets those three conditions, the AI-disruption discount the market is applying is likely mispriced downward. That stock may deserve a materially different multiple than the terminal-exposed peers it is being grouped with.

The binary framing, AI replaces terminals or terminals survive untouched, misses the more likely outcome. Incumbents are beginning to capture revenue from AI adoption itself, and the mechanism is structural rather than defensive.

Where AI models excel is in reasoning and synthesis across large volumes of text and data. Where they fall short, on their own, is in delivering the data accuracy, auditability, and regulatory compliance that institutional users require. That shortfall creates a natural division of labour: AI handles the inference and synthesis work while governed vertical data platforms supply the verified, traceable inputs that regulated workflows depend on.

AI commoditisation risk does not apply uniformly across the ecosystem: BCA Research’s Peter Berezin identifies economies of scale, network effects, and proprietary data as the three conditions separating companies that will capture durable AI profits from those that will bear the cost of the transition without capturing the returns.

Regulated financial institutions cannot deploy AI-generated outputs into production workflows without auditable data provenance. Model risk management requirements, explainability standards, and compliance frameworks mean that an AI tool generating a loan risk assessment or a regulatory filing needs to prove where every data input came from and how it was validated. AI models alone cannot do that. Trusted vertical data platforms can, and that is where the complementarity creates monetisable value.

The model risk management requirements for AI outputs in regulated institutions set explicit standards for data provenance, explainability, and validation, standards that AI-native tools generating loan risk assessments or regulatory filings must satisfy before any production deployment is permissible.

Three incumbent monetisation strategies are already visible in the market:

Morgan Stanley argues that advanced AI is likely to strengthen incumbents with scale and trusted data by lowering the cost of code, data cleansing, and interface design, allowing faster innovation and deeper competitive advantages.

This MCP connector revenue stream at FactSet is modest in absolute size but meaningful in what it signals structurally. It indicates that even the most terminal-exposed incumbent is not simply an AI casualty but a potential beneficiary of the AI data access market. The terminal-as-victim framing captures only part of the value picture.

The preceding analysis produces a practical screening tool rather than an academic taxonomy. Three axes, evaluated in sequence, give you a calibrated displacement assessment for any financial data business.

| Business Type | Data Ownership | Workflow Integration | AI Displacement Risk |

|---|---|---|---|

| Branded index/ratings provider | High (proprietary, regulated) | Deep (benchmark-linked mandates) | Low |

| Terminal-model aggregator | Low (third-party data) | Shallow (interface-dependent) | High |

| Embedded workflow platform | Variable | Deep (compliance-critical) | Low to moderate |

| Mixed-exposure diversified player | Mixed | Mixed across segments | Requires segment-level analysis |

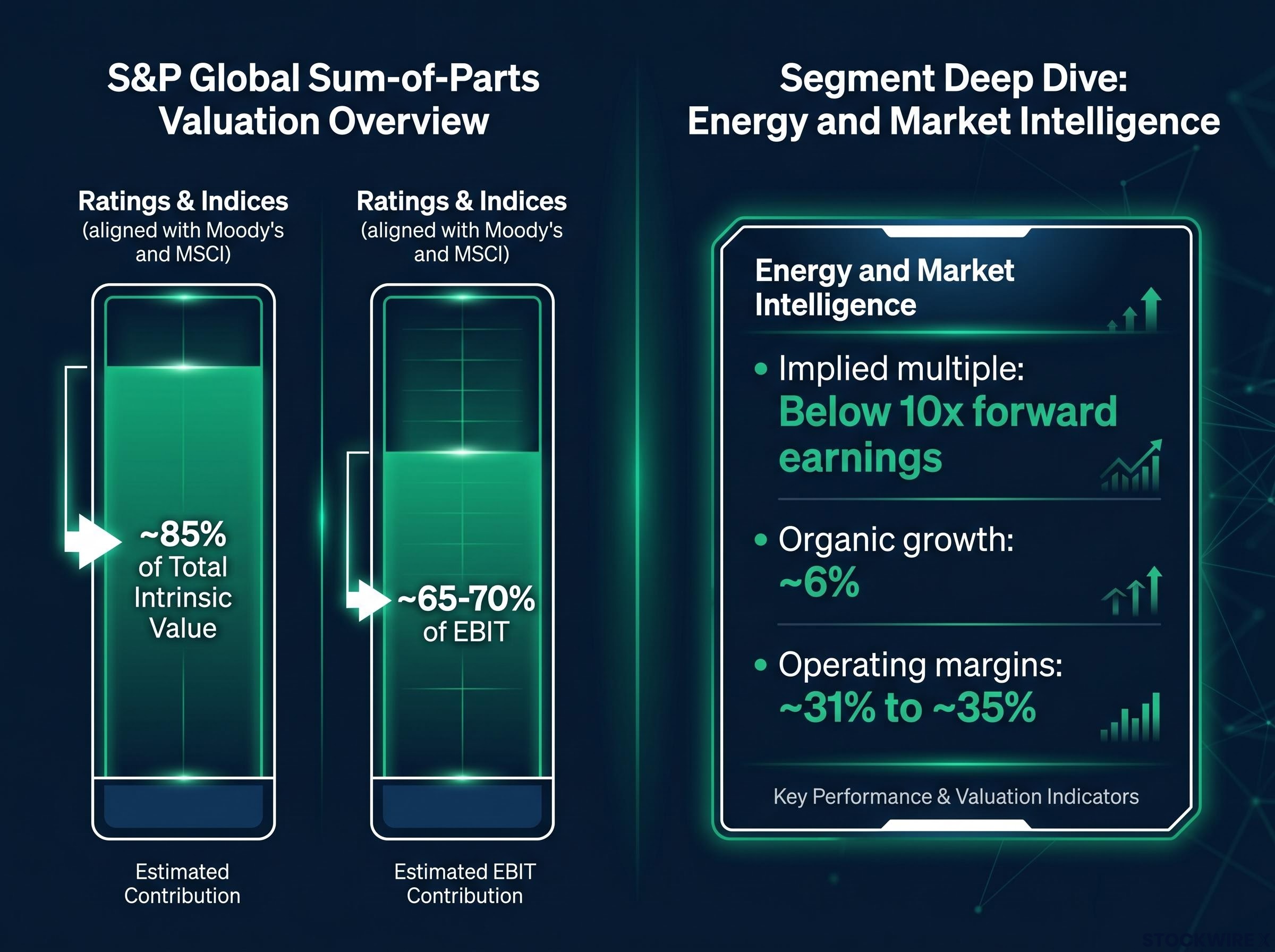

S&P Global illustrates why blunt AI discounts fail. Its Market Intelligence division has sustained organic revenue growth of roughly 6% per year across the past three to four years, while lifting operating margins from around 31% to close to 35% over the same period. That is not a business in structural decline. Yet on a sum-of-parts basis, as Magellan has observed, stripping out a ratings valuation in line with Moody’s and an indices valuation in line with MSCI would leave the remaining businesses (energy and market intelligence combined) implying a multiple of below 10 times forward earnings. The ratings and indices businesses contribute roughly 85% of total intrinsic value while representing only around 65-70% of EBIT. The market is discounting the intelligence division to near-distressed levels while underappreciating the higher-quality businesses that drive the majority of value.

The time horizon matters too. Near-to-medium-term: pricing pressure and incremental seat loss in terminals, with AI-native entrants gaining share at the margin. Medium-to-long-term: gradual replatforming of workflows, with incumbents often providing the AI-augmented infrastructure layer rather than being displaced by it.

The market has correctly identified terminal-model pressure. It has incorrectly applied a uniform AI discount across embedded infrastructure and diversified players whose majority value sits in non-terminal businesses. The analytical error is category-level, not company-level, and it creates identifiable conditions for repricing.

Three signals, tracked across quarterly earnings cycles, will tell you whether the mispricing is correcting:

Magellan’s sum-of-parts observation: Applying peer-consistent valuations to the ratings and indices businesses leaves the energy and market intelligence segments priced at below 10 times forward earnings, a level that implies deterioration in divisions where the underlying financial performance points in the opposite direction.

Ryan Joyce, Deputy Portfolio Manager at Magellan Global Equities Investment Team, built an initial position in S&P Global during late 2025 and added to it after the February 2026 market selloff, a sequence that reflects a judgment that the prevailing blended multiple was failing to give adequate credit to the non-terminal parts of the business.

Sum-of-parts mispricing of the kind visible in S&P Global, where the market applies a blended multiple that undervalues high-quality segments by attributing their earnings to a lower-rated peer group, is one of the more reliable sourcing signals for investors constructing a pipeline of overlooked positions in well-covered large-cap names.

The correction is not a single catalyst. It is a pattern of reported evidence that accumulates over quarters. That distinction matters. If you hold financial data names or are evaluating entry points, the three monitoring signals above convert this analysis from a one-time read into an ongoing thesis you can track against real-world data. The difference between conviction and exposure is knowing what you are watching for.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

AI disruption risk in financial data refers to the threat that AI-native tools, such as those from Anthropic and OpenAI, will replace traditional terminal and analytics platforms by delivering similar research capabilities at a fraction of the cost, roughly $1,200 per year versus $10,000-$12,000 for a traditional terminal seat.

FactSet shed roughly 50% from its November 2024 peak near $484 to around $242 by mid-2026, driven by AI tool launches from providers like Anthropic, analyst downgrades citing unbundling risk from firms including Rothschild and Co Redburn, and quarterly earnings that failed to demonstrate enough AI-era growth acceleration to counter the displacement narrative.

The key variable is switching cost heterogeneity: terminal-model aggregators face real pressure because their switching costs amount to little more than staff retraining, while embedded workflow platforms wired into compliance-critical or revenue-generating processes require multi-month integration projects, parallel runs, and regulatory sign-off, making displacement far costlier and less likely.

Incumbents are capturing AI revenue through data connectivity fees (FactSet charges customers additional fees to connect Claude via its MCP interface), AI-augmented analytics sold as premium tiers, and workflow automation tools built on existing verified data platforms, positioning them as infrastructure providers to AI models rather than casualties of them.

Applying peer-consistent valuations to S&P Global's ratings business (in line with Moody's) and its indices business (in line with MSCI) leaves the energy and market intelligence divisions implying a multiple of below 10 times forward earnings, despite the Market Intelligence segment delivering roughly 6% organic revenue growth and margin expansion from around 31% to close to 35% over three to four years.