Why AI Disruption Risk Is Mispriced Across Financial Data Stocks

1 hr ago

A financial market with ten approved competitors has, for more than fifty years, functioned as if it has two. That fact should bother anyone who believes competition erodes concentration over time.

The explanation is not a single barrier. It is a system of interlocking mechanisms, regulatory, informational, economic, and institutional, that makes S&P Global’s competitive position not just defensible but, for most rational market participants, not worth attacking even when alternatives exist. Most investors understand that network effects and regulatory barriers exist as concepts. What this piece does is map the specific institutional machinery that keeps S&P’s moat self-reinforcing.

After this, you will have a working model of how a data-benchmark business constructs a moat that is structural and institutional rather than technological or brand-based, and why that distinction is the one that matters most when evaluating durability.

In 1975, the U.S. Securities and Exchange Commission (SEC) introduced the category of Nationally Recognised Statistical Rating Organisations (NRSROs), a designation that embedded approved agency ratings directly into broker-dealer capital requirement rules. An NRSRO designation was not a quality award; it was a prerequisite for regulatory use. Only ratings from designated agencies counted when banks and brokerages calculated their capital adequacy.

The initial designees were:

By approximately 2010, the SEC had expanded that list to 10 NRSROs, a figure that remained stable through 31 December 2025.

The expansion should have redistributed market share. It did not.

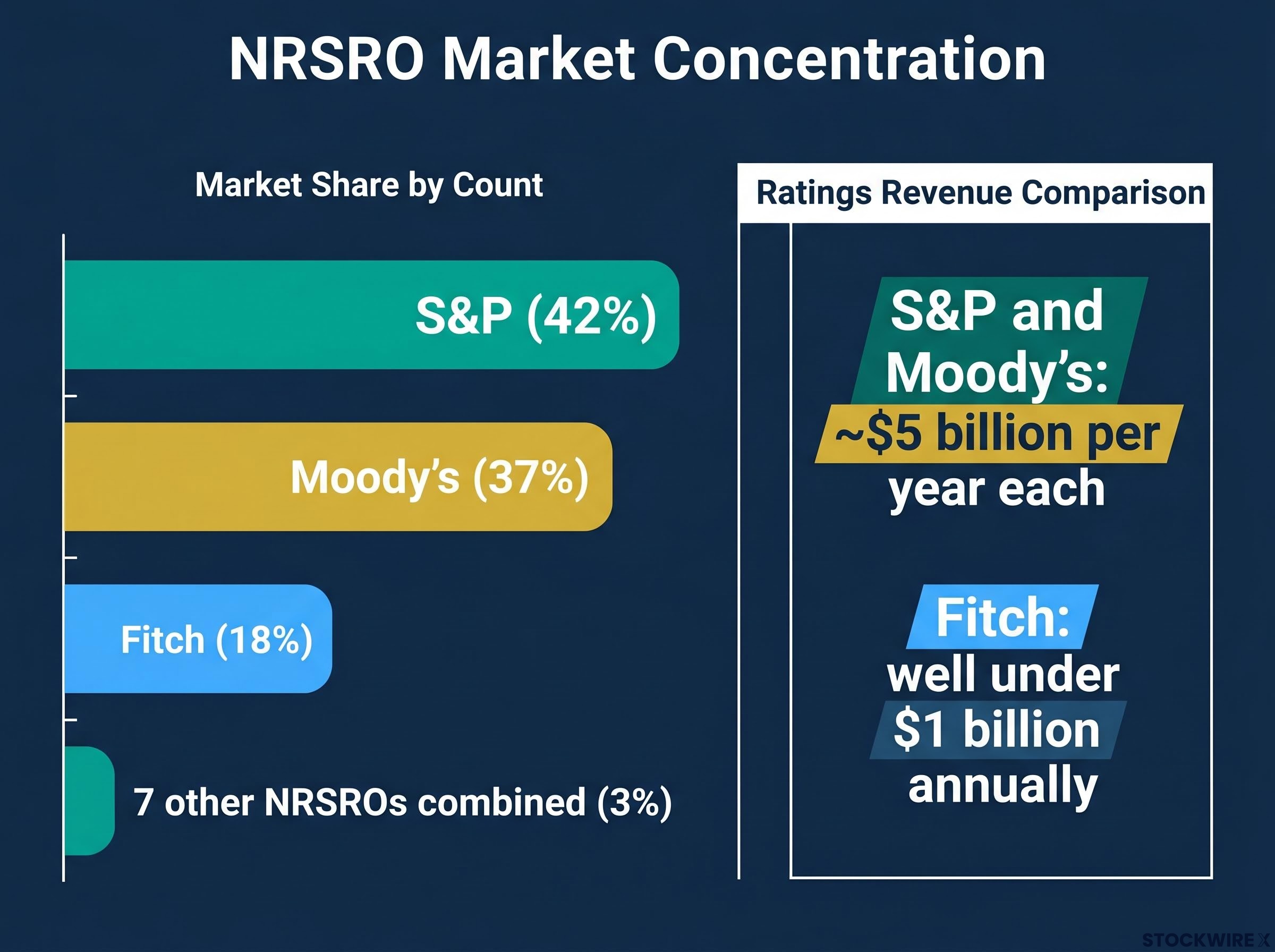

S&P holds approximately 42% of the ratings market by count, Moody’s approximately 37%, Fitch approximately 18%, and all other NRSROs combined approximately 3%.

That concentration, barely moved by tripling the number of approved competitors, tells you that the 1975 designation created the opening conditions for dominance, but something else entirely explains why those conditions never closed. The regulatory origin was the catalyst. The moat is the system that formed around it.

Morningstar’s framework identifies five moat sources, intangible assets, switching costs, network effects, cost advantage, and efficient scale, and S&P Global’s structural position draws on at least three of them simultaneously, a combination that moat analysts associate with the most durable competitive positions.

Academic research on the oligopolistic dominance of the Big Three rating agencies confirms that post-Dodd-Frank regulatory reforms intended to open the market produced no meaningful redistribution of share, with the dominant trio retaining a collective global share exceeding 99% in sovereign credit ratings.

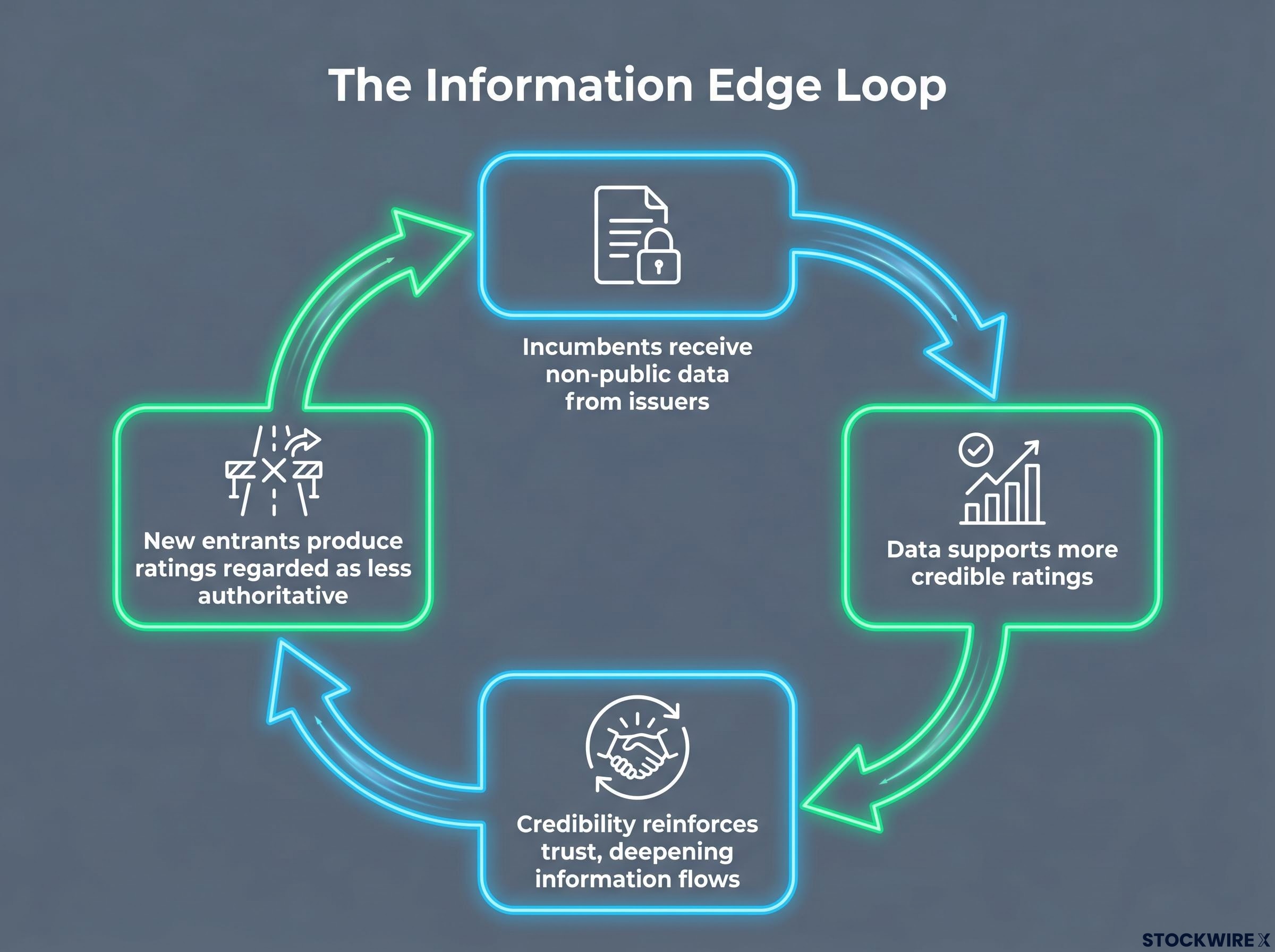

Large issuers do not rate themselves. They share non-public financial data, projections, internal statements, and granular exposure details, with rating agencies under confidentiality arrangements. They do this because ratings built solely on public information are less informative and therefore less credible to the investors who rely on them.

That sharing is selective. Issuers choose counterparties they trust with sensitive internal data, and trust is built over decades of relationship capital and legal infrastructure. The SEC’s own conflict-of-interest rules explicitly acknowledge this practice of non-public information sharing between issuers and agencies.

The result is a self-reinforcing loop that no analytical model, however superior, can short-circuit:

What this tells you about the NRSRO expansion is straightforward: approval to rate is a necessary condition for competing, not a sufficient one. A new agency with NRSRO status still faces a cold-start problem with no easy technical solution. It needs issuers to trust it with confidential data before those issuers have any track record of working with it.

For large, frequent issuers, paying for two ratings from the dominant agencies is economically rational. Two concordant ratings from S&P and Moody’s can modestly tighten credit spreads (the premium investors charge for default risk) by enough to outweigh the incremental fee for the second opinion. Issuers do the maths and choose the pair.

Once a second major-agency rating is in place, the economics of adding a third shift decisively against the issuer. The incremental spread benefit of a further opinion diminishes to the point where it no longer covers the additional fee, because market participants already regard dual coverage from the dominant pair as adequate validation. The issuer is paying for something the market is not pricing, and rational issuers stop at two.

No coordination or agreement is required for this outcome. Thousands of individual issuers, each making their own cost-benefit calculation, collectively lock in a two-player centre. The equilibrium holds because it is rational for each participant independently.

| Tier | Agencies | Market share | Structural role |

|---|---|---|---|

| Dominant pair | S&P, Moody’s | ~79% combined | Default pair for large global issuers; jointly purchased |

| Third player | Fitch | ~18% | Competes in specific segments; structurally capped by limited demand for a third rating |

| All others | 7 remaining NRSROs | ~3% combined | Narrow niches; mainstream market does not need additional opinions |

The scale disparity reinforces the picture. Each of S&P and Moody’s produces ratings revenues in the region of approximately $5 billion per year. Fitch, which is privately held and therefore harder to measure precisely, is estimated to generate well under $1 billion annually from the same activity. The cost base that each dominant agency carries in its ratings division alone is understood to surpass Fitch’s entire top line, a gap that compounds as the incumbents continue to scale.

The practical implication: even a well-capitalised new entrant with NRSRO status faces not a regulatory barrier but an economic one. The market simply does not need another rating once the dominant pair is already engaged.

S&P and Moody’s ratings appear in places most investors encounter without thinking about why:

This is not brand loyalty. The moat here is a coordination problem. Switching the standard does not require one issuer or one investor to change their mind. It requires lawyers, investors, regulators, and institutions to revise documents and processes simultaneously. The switching cost is not measured in dollars; it is measured in legal and systems complexity across thousands of independent actors.

S&P itself describes its ratings as a “common and transparent global language for investors”, a candid acknowledgement that its letter grades function less as a product and more as shared infrastructure.

The concept is transferable. Any firm that successfully embeds itself as a shared reference in legal, regulatory, and financial infrastructure achieves a durability that purely product-quality-based competitors cannot match. The question is never whether a better scale can be built. It is whether the entire ecosystem would coordinate to adopt it.

The same logic applies to the index business. The S&P 500 is embedded in passive funds that replicate it, active manager reporting that benchmarks against it, derivatives markets with large notional volumes tied to it, and financial media that uses it as shorthand for “the market.”

Once those contracts, reporting systems, and marketing materials are tied to a benchmark, switching requires ecosystem-wide coordination, precisely the same structural barrier that protects the ratings scales. The S&P 500’s committee governance, where a panel exercises judgment about inclusions and exclusions rather than following a purely mechanical formula, adds a further differentiator. That discretionary overlay makes the index harder to commoditise and harder for algorithmic alternatives to replicate exactly.

The moat is real. It is not unconstrained.

On the index side, the largest passive managers have negotiating leverage that matters:

On the ratings side, regulatory oversight imposes behavioural constraints:

Credit market stress, including the rising default rates that Fitch projected at 4.5% to 5.0% for leveraged loans in 2026, creates a paradox for rating agency economics: deteriorating credit quality generates more rating activity and therefore more revenue for the dominant agencies, reinforcing the commercial case for issuers to remain engaged with the established pair.

Operating margins for the ratings and indices segments sit in the 60%-70% range at the segment level, confirmed by company disclosures through 2023-2025.

Those margins tell you the business remains extraordinarily profitable. The constraints are real but bounded: fee compression is ongoing, regulatory risk is genuine, but neither Vanguard switching to a competing index nor a new NRSRO gaining meaningful market share constitutes a structural threat under present conditions.

For anyone evaluating S&P Global as a business, the distinction between margin pressure (real, ongoing) and structural displacement risk (low, structurally rationed) is the single most important analytical separation to make. Dismissing the moat because fees are under pressure is one error. Overstating durability by ignoring that regulatory violations carry real consequences is the other.

The moat’s deepest source of strength is not any single mechanism. It is the alignment of individual incentives across every class of ecosystem participant, each of whom rationally chooses the incumbent even when no single actor wants the status quo to be permanent.

The causal chain, built over five decades, stacks as follows:

Each layer reinforces the others. Approximately 50% of total S&P Global revenue is subscription-type, providing compounding stability independent of transaction cycle volatility. That revenue split is the financial signature of institutional embeddedness: clients do not churn from infrastructure they are built around.

The correct test for moat durability in a data-benchmark business is not whether a better product emerges. It is whether incentive alignment across ecosystem participants changes. As long as dual ratings remain economically rational, S&P scales remain embedded in mandates, and the S&P 500 remains the default benchmark, displacement requires simultaneous coordinated action by multiple classes of rational actors who each individually benefit from the status quo. That is a collective action problem, and collective action problems tend to persist.

A better analytical model will not do it. A new NRSRO will not do it. Fee compression will not do it. The genuine displacement conditions are narrower and more specific:

Each of these requires simultaneous, uncoordinated action by thousands of independent actors, issuers, investors, regulators, asset managers, lawyers, all of whom currently benefit from the existing standard. That is not a single barrier to surmount. It is a system of barriers that must all be surmounted simultaneously by parties who have no mechanism to coordinate.

Fifty-plus years of structural persistence, through the addition of seven more NRSROs, through the 2008 financial crisis, through enforcement actions and fee compression, produced no meaningful redistribution of market share away from the dominant pair.

For anyone who follows financial regulation or benchmark governance, the signal to watch is not competitive product launches by new raters. It is changes to the regulatory rules that make NRSRO status a capital-requirement prerequisite, because that is the foundational layer everything else sits on. Until that changes, the incentive alignment holds, and the moat compounds.

For investors who want to translate the structural analysis here into a portfolio decision, moat investing in practice involves applying both a quality screen and a valuation discipline, selecting companies that pass the competitive advantage threshold only when they trade at a discount to intrinsic value estimates.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

An economic moat refers to the structural advantages that protect a company from competition. For S&P Global, the moat is built from at least three simultaneous sources: regulatory barriers created by NRSRO designation, information asymmetry from long-standing issuer relationships, and the embedding of its ratings scales and indices as shared infrastructure across legal, regulatory, and financial systems.

NRSRO approval is a necessary condition for competing, not a sufficient one. New entrants face a cold-start problem: they lack the issuer relationships needed to access non-public financial data, which makes their ratings less credible to the market regardless of methodological quality, and the dual-rating economics of large issuers rationed demand away from additional competitors before they could gain traction.

Once an issuer holds two concordant ratings from S&P and Moody's, the incremental spread benefit from a third rating no longer covers the additional fee, because the market already treats the dominant pair as adequate validation. Thousands of issuers independently reach this conclusion, which collectively locks in the two-player centre without any coordination or agreement.

Displacement would require simultaneous, uncoordinated action across thousands of independent actors: a regulatory overhaul removing NRSRO-based capital rules, an ecosystem-wide shift in institutional mandates away from S&P and Moody's scales, and a coordinated migration away from the S&P 500 across passive funds, derivatives markets, and performance reporting, each of which constitutes a collective action problem with no current coordination mechanism.

Operating margins for S&P Global's ratings and indices segments sit in the 60%-70% range at the segment level, confirmed by company disclosures through 2023-2025, with approximately 50% of total company revenue coming from subscription-type arrangements that provide stability independent of transaction cycle volatility.