Why AI Makes Markets Safer Daily but Riskier in a Crisis

2 hrs ago

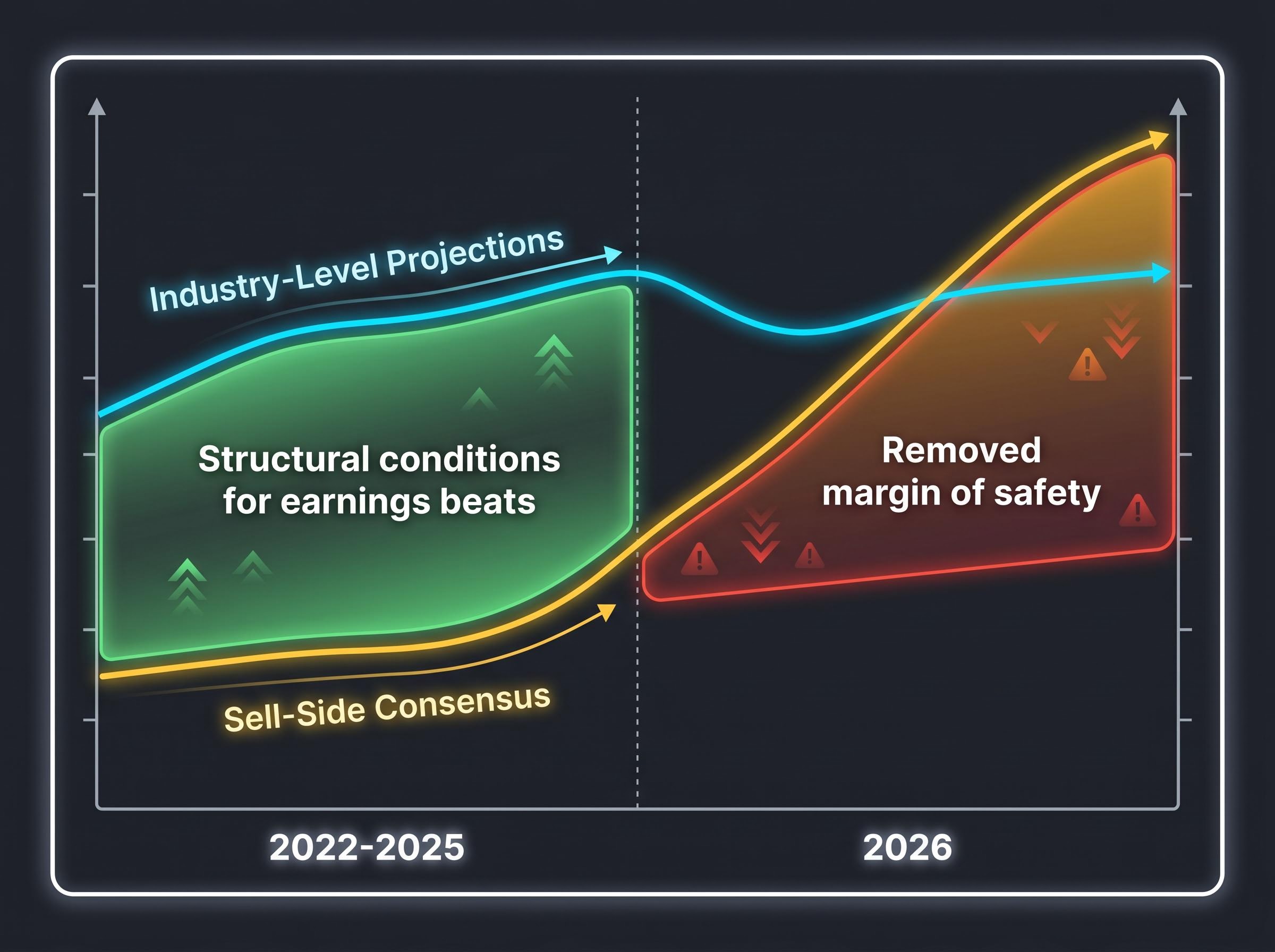

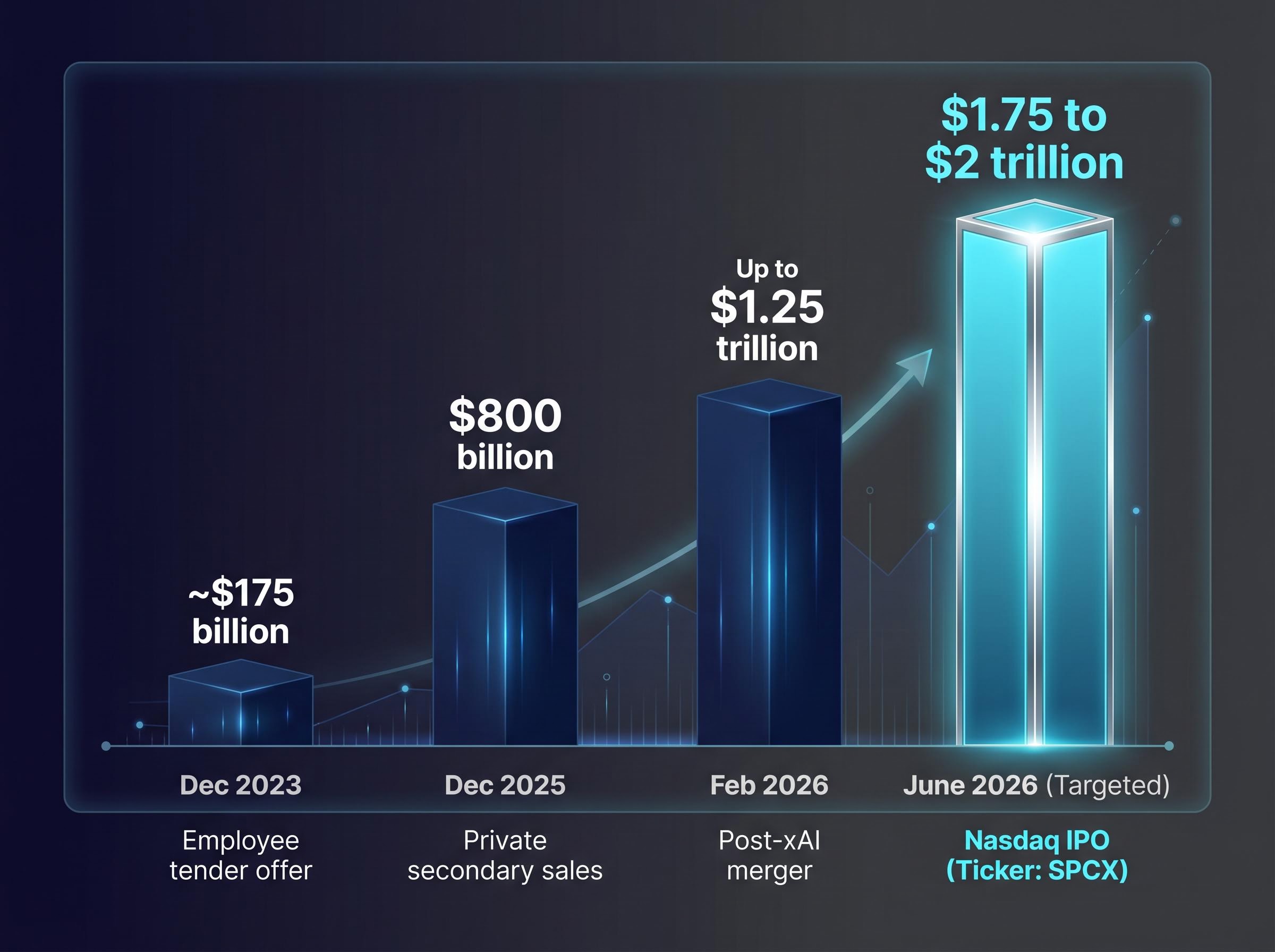

For roughly three to four years, Wall Street’s earnings expectations for the technology sector ran below industry-level forecasts. That gap between what analysts predicted and what the sector delivered was a reliable tailwind, generating quarter after quarter of beats that rewarded overweight positioning. The gap has now reversed. Sell-side consensus forecasts for technology growth have climbed above independent industry-level estimates, and Fisher Investments has responded by moving underweight the sector. Simultaneously, the IPO pipeline is accelerating in scale: SpaceX has confidentially filed for a June 2026 Nasdaq listing targeting a valuation of $1.75 to $2 trillion, with a cohort of large venture-backed names queuing behind it. Technology sector valuation, in this environment, is no longer a question of whether the businesses are strong. It is a question of whether the price already reflects that strength, and whether growing share supply will test prices that leave no margin for error.

For approximately three to four years leading into 2026, a quiet structural advantage powered technology returns. Industry-level growth forecasts for the sector consistently exceeded what sell-side analysts had baked into their models. The result was predictable and profitable: companies reported earnings that beat consensus, share prices responded, and the cycle repeated.

The pattern mattered because it was self-reinforcing. Conservative analyst estimates meant that merely decent results looked exceptional. Investors who recognised the gap could position accordingly, confident that the bar was low enough to clear.

For readers wanting to build a deeper foundation for interpreting these dynamics, our full explainer on why stocks fall on record profits walks through the mechanics of earnings surprises, the role of forward guidance in overriding headline beats, and the research on how retail investors respond asymmetrically to negative versus positive surprises.

BofA Global Fund Manager Survey (2025): Global managers are most overweight US tech since before the 2021 peak, a positioning extreme that Bank of America strategists characterise as a contrarian warning signal.

AI enthusiasm drove the reversal. Rapid upward revisions in sell-side models, fuelled by surging demand narratives around artificial intelligence infrastructure and cloud spending, closed the gap between analyst consensus and industry-level projections, then surpassed it. JPMorgan equity strategists described the shift as consensus moving “from skepticism to exuberance.”

The speed of the revision matters as much as the direction. Michael Hanson of the Fisher Investments Investment Policy Committee has noted that the three-to-four-year window of analyst underestimation is over. The sector’s businesses have not deteriorated. The price of owning them no longer reflects a conservative assumption.

The phrase appears in nearly every major bank’s 2025-26 equity outlook. Goldman Sachs, Morgan Stanley, JPMorgan, and BlackRock all use variations of it when describing US technology. What it means in practice is more uncomfortable than the phrase suggests.

When expectations are fully embedded in a stock’s price, a result that merely meets forecasts produces no additional return. The upside from beating consensus shrinks, because the beat was already assumed. Any shortfall, however small, produces disproportionate downside, because the price had no cushion.

Arm Holdings provided the clearest recent illustration of priced-for-perfection dynamics when it delivered a clean Q4 FY2026 beat with above-consensus guidance, then saw shares fall approximately 8% after CEO Rene Haas disclosed a supply gap covering only half of a $2 billion AGI CPU demand figure; the beat was already priced in, and the execution risk was not.

| Metric | US Tech Sector | Broad S&P 500 |

|---|---|---|

| Expected EPS growth direction | Mid-teens (per FactSet/Bloomberg consensus) | High single digits to low double digits |

| Analyst sentiment characterisation | “Stretched,” “priced for perfection,” “richly valued” | Neutral to moderately optimistic |

| Fund manager positioning | Most overweight since pre-2021 peak | Broadly neutral |

Note: Precise consensus EPS figures are proprietary to data providers. Directional characterisations reflect publicly available institutional commentary from Goldman Sachs, Morgan Stanley, JPMorgan, BlackRock, and Schroders.

Schroders described US tech in 2025 as “over-owned and richly valued, with earnings expectations unusually elevated.” Goldman Sachs noted that “estimate revisions are front-loaded, leaving less room for positive surprises.” The high bar these institutions identify is not an abstract concern. It creates a negatively skewed return distribution: the ceiling for outperformance compresses while the floor for underperformance widens.

Strong fundamentals and poor near-term returns are not contradictory outcomes when valuations are stretched. They are the expected outcome.

The supply-side argument operates independently of whether an IPO candidate is a strong business. The mechanism is straightforward, and it follows a logical chain.

Renaissance Capital (2026 YTD): US IPOs have raised $28.4 billion in proceeds, a 155.2% increase year-over-year, despite fewer total deals (63 priced, down 17.1%). The pattern is clear: fewer deals, but dramatically larger average deal size.

Renaissance Capital IPO market data for 2026 confirms the pattern described above: total proceeds of $28.4 billion represent a 155.2% year-over-year increase, concentrated across fewer deals, which means average deal size has risen sharply and the capital absorption required per listing has grown accordingly.

Fisher Investments frames float as the variable that determines actual supply pressure. A company listing 5% of its shares versus 50% produces a very different market impact, and the distinction matters more than headline valuation.

Arm Holdings listed with a relatively constrained free float in September 2023, which initially supported the price but contributed to volatility as lockup expiry approached. Reddit, completing its IPO in March 2024, saw supply overhang weigh on price momentum as additional shares entered the market. Instacart experienced post-lockup price softness driven by the same dynamic.

The pattern is consistent across all three: float size and lockup expiry dynamics directly influenced aftermarket performance, regardless of the underlying business strength. The mechanism is structural, not company-specific.

SpaceX filed its confidential draft registration statement with the SEC on 1 April 2026. The company is targeting a June 2026 listing on the Nasdaq under the ticker SPCX, with a valuation target of $1.75 to $2 trillion.

| Date | Transaction type | Implied valuation |

|---|---|---|

| December 2023 | Employee tender offer | ~$175 billion |

| December 2025 | Private secondary sales | $800 billion |

| February 2026 | Post-xAI merger secondaries | Up to $1.25 trillion |

| June 2026 (targeted) | Nasdaq IPO | $1.75-$2 trillion |

A listing at even the low end of that range would dwarf the $28.4 billion in total IPO proceeds raised across all US listings in 2026 to date. The capital absorption required to support institutional allocations of that magnitude is substantial.

Investors wanting to stress-test the numbers behind that headline figure will find our deep-dive into SpaceX’s $2 trillion valuation case useful; it works through the EBITDA multiples, analyst downside scenarios, and the base-rate data on how large IPOs have performed against broader benchmarks over three-year horizons.

SpaceX is not the only name in the queue. The broader pipeline of large venture-backed candidates includes:

Fisher Investments’ underweight in technology is explicitly not a judgement about the sector’s business quality. Michael Hanson of the Fisher Investments Investment Policy Committee has framed it as a judgement about whether the price paid for that quality is rational given the expectations now embedded in it.

Fisher Investments positioning: The underweight reflects a view that expectations already embedded in technology prices are too high relative to likely outcomes, not a view that the sector’s businesses have weakened.

Returns are a function of expectations versus outcomes, not outcomes alone. A sector can deliver strong earnings growth and still underperform if that growth was already priced in. The distinction matters because it separates business analysis from investment analysis.

The BofA Fund Manager Survey finding of peak overweight positioning reinforces this logic. When positioning is crowded, the marginal buyer who would drive further appreciation may already own the stock.

Market breadth deterioration reinforces the crowding concern: as of early May 2026, only 22% of S&P 500 stocks outperformed the index on a 30-day basis, a 30-year low, with 28 members accounting for half of recent returns, a configuration that historically preceded 5-15% drawdowns roughly 80% of the time in comparable episodes since 1994.

Large IPO waves tend to cluster when investor optimism is elevated and issuers can command premium valuations. Fisher Investments treats a busy IPO window not only as a supply event but as a sentiment gauge: companies accelerate listings when they believe public-market pricing will be most generous.

The 2020-21 SPAC peak illustrated what peak-cycle issuance looks like. That wave collapsed, and the return to traditional listings in 2025-26 represents a more disciplined but equally telling signal. Issuers are choosing to list now because the window is favourable, a choice that over 15-20 years of increasing regulatory burden has made less attractive, meaning each new wave reflects a deliberate calculation.

The interaction with the expectations framework is direct. Elevated sentiment sustains high valuations, but it also concentrates the risk of disappointment when the cycle turns. Investors who can read the signal gain an early-warning capability.

Three indicators form a practical framework for interpreting these conditions:

The two risks compound. Stretched expectations mean any earnings miss is punished disproportionately. Growing supply means capital that might have supported incumbent prices is being redirected toward new listings. Neither risk requires the sector’s businesses to weaken; both operate on the price side of the equation.

Fisher Investments’ current positioning reflects this combination: underweight technology, with overweight allocations directed toward areas where expectations remain lower relative to fundamentals. The firm’s estimate of approximately 3% global GDP growth for 2026 suggests a backdrop where broad market tailwinds are modest, making sector selection the primary driver of relative returns.

Three questions apply to any portfolio with meaningful technology exposure:

Stretched expectations plus growing supply plus high quality does not equal a sell signal. It equals a defensible reason for caution, and for ensuring that portfolio positioning reflects what the price already assumes rather than what the business deserves.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements regarding future market conditions, earnings expectations, and IPO timelines are speculative and subject to change based on market developments and company performance. Past performance does not guarantee future results.

Priced for perfection means analyst earnings expectations are already fully embedded in a stock's price, so merely meeting forecasts produces no additional return while any shortfall is punished disproportionately, creating a negatively skewed return distribution.

AI enthusiasm drove rapid upward revisions in sell-side models, pushing analyst consensus above independent industry-level growth estimates for the first time in roughly three to four years, removing the structural tailwind that had generated consistent earnings beats.

A listing targeting $1.75-$2 trillion would require substantial institutional capital reallocation, diverting buying pressure away from existing technology holdings and adding significant new float supply to an already expensive market.

Fisher Investments frames its underweight as a judgement about price rather than business quality: returns depend on outcomes versus expectations, and when expectations are fully priced in, even strong earnings growth can produce poor relative returns.

Large IPO waves tend to cluster when investor optimism is elevated, so a surge in high-value listings signals that issuers believe public-market pricing is near its most generous, which historically coincides with peak-cycle sentiment and elevated valuation risk.