Why Social Media Stocks Are Mispricing Youth Litigation Risk

3 hrs ago

US analysts have beaten Nvidia’s earnings estimates for two consecutive years. The stock has still underperformed both the Philadelphia Semiconductor Index and the S&P 500 semiconductors sector year-to-date as of 20 May 2026. That disconnect, between consistent beats and inconsistent price appreciation, sits at the centre of how the Nvidia investment thesis is being rewritten across Wall Street.

Nvidia reports Q1 FY2027 earnings today against a backdrop where bond yields are competing with AI optimism for investor attention and where the standard GPU-centric earnings narrative is increasingly insufficient for sophisticated analysis. Analysts are no longer asking only how many GPUs Nvidia sold. They are asking how much networking, systems, and software revenue accompanied each rack deployment. What follows is an examination of what the shift from GPU vendor to full-stack AI infrastructure company means in practice, how US analysts are restructuring their valuation frameworks accordingly, and what specific metrics investors should track to evaluate whether the transformation is delivering durable revenue.

Nvidia has beaten consensus revenue and EPS estimates in every quarter for more than two years. The reward for that streak has been remarkably thin.

Wolfe Research analyst Chris Senyek has characterised Nvidia’s earnings pattern as one where consistent beats fail to produce sustained post-earnings price gains, a dynamic where investors buy the anticipation and sell the confirmation.

The numbers from the most recent full fiscal year reinforce the paradox:

At $215.9 billion in annual revenue, Nvidia has reached a scale where asking whether the company beat estimates by a few hundred million dollars produces diminishing analytical signal. The market is pricing forward expectations, not backward beats. That shifts analytical weight toward guidance, product mix evolution, and infrastructure diversification signals. Investors who continue to evaluate Nvidia solely through quarterly beat-and-raise optics are working with an incomplete model. Understanding why the framework needs updating is the prerequisite to building a more durable thesis.

Q2 FY2027 guidance language has historically moved Nvidia’s stock more than the reported quarter itself, a dynamic that holds regardless of macro conditions; with the 10-year Treasury yield at 4.604% and WTI crude elevated, any ambiguity in the forward outlook carries larger downside consequences than it would in a lower-rate environment.

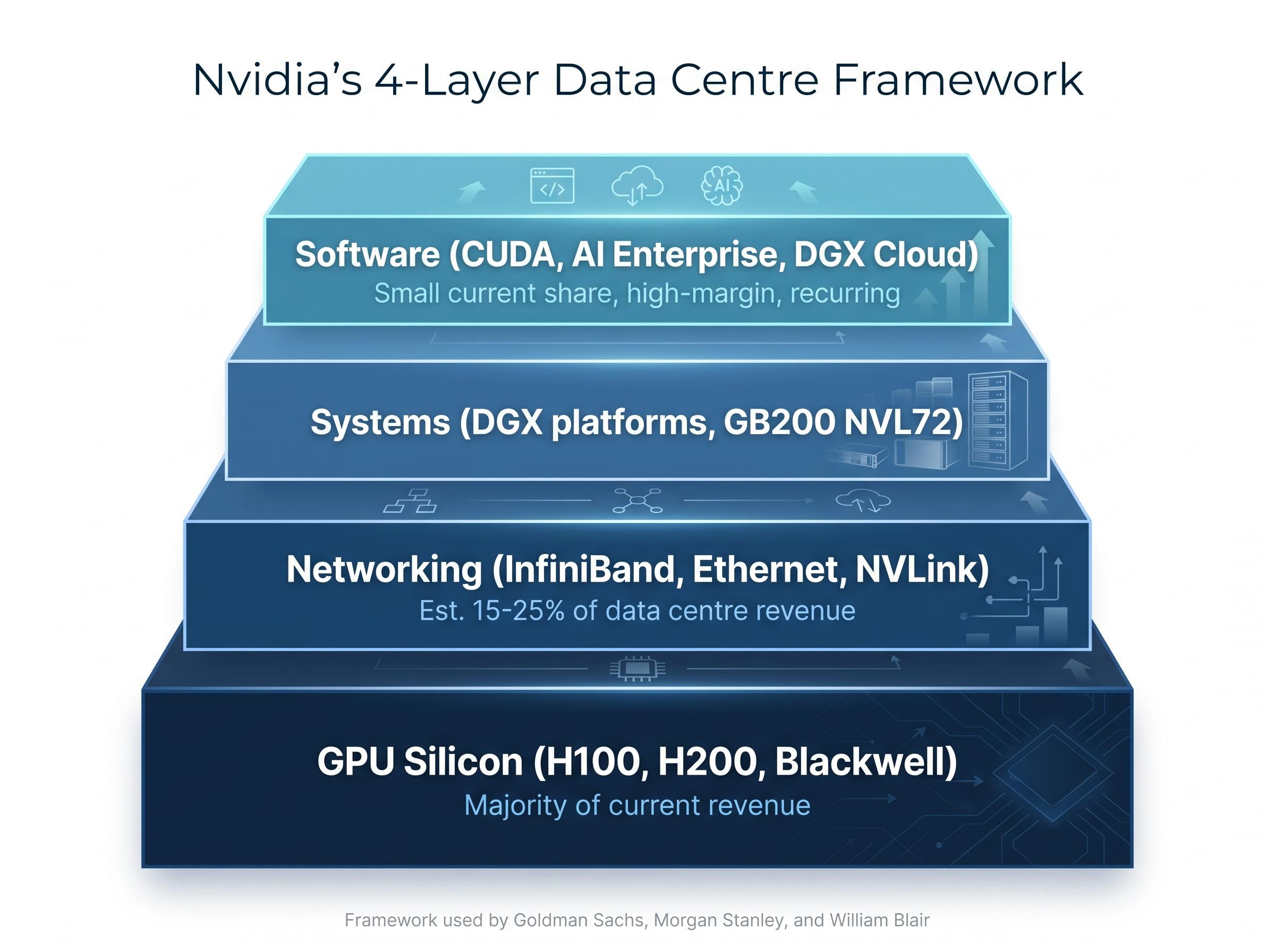

US analysts at Goldman Sachs, Morgan Stanley, and William Blair now decompose Nvidia’s data centre business into four distinct revenue layers. The framework is not marketing language; it is the structure these firms use to model forward revenue and margin trajectories.

| Layer | What it includes | GAAP disclosure status | Analyst materiality assessment |

|---|---|---|---|

| GPU silicon | H100, H200, Blackwell accelerators | Embedded in Data Centre segment | Majority of current revenue |

| Networking | InfiniBand, Ethernet, NVLink | No standalone line item | Estimated at 15-25% of data centre revenue; growing faster than GPU units |

| Systems | DGX platforms, GB200 NVL72 rack configurations | No standalone line item | Increasing as rack-level sales replace chip-level sales |

| Software | CUDA, AI Enterprise, DGX Cloud | No standalone line item | Small current share; strategically high-margin and recurring |

Nvidia does not break out networking or software as separate GAAP line items. That absence is itself informative: the business is integrated by design. Jensen Huang’s framing in the Q4 FY2026 release aligned explicitly with the analyst framework:

“Data center revenue was driven by strong demand for the NVIDIA HGX platform, including both H100 and H200 GPUs, and our end-to-end networking and software stacks.”

Investors who reconstruct the four layers analytically gain a more accurate picture of margin structure and growth durability than those reading only segment totals.

CUDA, AI Enterprise, and DGX Cloud are framed by analysts as a hedge against future GPU ASP compression from hyperscaler custom silicon competition. Software attach rates are viewed as creating ecosystem lock-in and improving the sustainability of data centre margins over time. Nvidia does not publish AI software revenue as a standalone GAAP figure; analyst estimates are embedded in qualitative commentary rather than public disclosures. The transition from qualitatively important to quantitatively material is what the street is watching for.

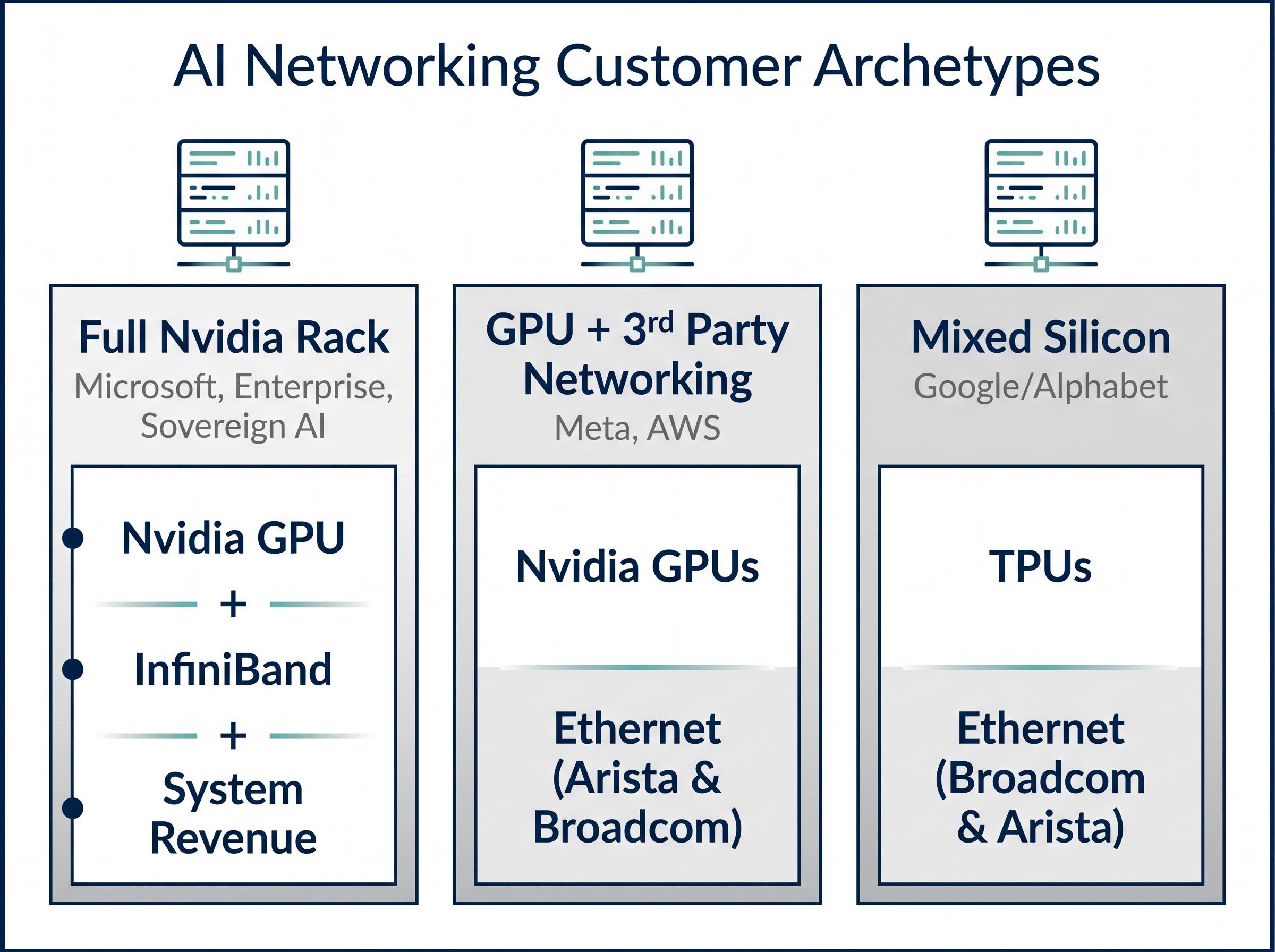

Nvidia’s InfiniBand networking (built on the Mellanox acquisition) functions as the de facto standard for large-scale AI training clusters. Lower latency, higher scalability, and in-network computing features such as SHARP give hyperscalers reason to purchase the full Nvidia rack rather than mixing vendors.

Morgan Stanley has described Nvidia as a “system and networking company, not just a GPU vendor,” arguing that investors should increasingly separate attach revenue from core GPU ASPs when modelling data centre growth.

The counterargument is specific and named. Meta Platforms has leaned heavily into Ethernet-centric AI cluster design using Arista Networks switches and Broadcom silicon, which limits Nvidia’s networking revenue penetration even where GPU sales remain strong. Amazon Web Services has similarly built its networking infrastructure around Ethernet with Broadcom and Arista-based solutions, reducing Nvidia’s networking share relative to deployments where InfiniBand dominates.

Cisco’s $1 billion AI networking restructuring announced on 14 May 2026 reinforces the competitive pressure that Ethernet-based AI networking is placing on InfiniBand deployments: Arista, Broadcom, and now a restructured Cisco are all competing for the switching and fabric revenue that Nvidia captures in full-rack deployments but loses in Ethernet-preference environments.

Three customer archetypes illustrate where networking revenue attaches and where it does not:

Enterprise and sovereign AI customers represent the highest-value networking segment. These buyers typically lack internal expertise to design custom networks and therefore purchase integrated Nvidia systems more readily than hyperscalers. Goldman Sachs has framed networking and software as “high-margin layers” that improve the sustainability of data centre margins. Networking revenue does not arrive automatically with every GPU sale; understanding which customer segments generate full-rack revenue versus GPU-only revenue is where the modelling precision lives.

The structural argument and the product-roadmap argument converge in Blackwell. Nvidia’s GB200 NVL72 and related configurations are marketed as rack-level AI factories, integrating GPUs, InfiniBand and NVLink networking, storage, and system management as a single turnkey purchase.

The per-rack revenue expansion follows three sequential steps:

Blackwell-generation systems carry higher networking intensity per GPU than Hopper-generation products. That means more networking and software revenue attaches to each rack than in prior cycles. Analysts recommend updating per-rack revenue models upward for Blackwell relative to Hopper assumptions.

William Blair, which carries an Outperform rating on Nvidia, has framed networking plus system ASP per rack as potentially matching or exceeding the GPU portion over time. The firm’s projected Q2 FY2027 revenue guidance above $90 billion reflects sustained demand trajectory into Blackwell ramp.

Higher system ASPs and greater software attach are expected to sustain or expand gross margins relative to the Hopper cycle. Standalone GPU gross margins may face pressure as competition grows, but integrated system and software layers are expected to offset this at the blended segment level. For investors, Blackwell’s networking intensity is a revenue model assumption with direct implications for gross margin forecasts and the durability of data centre segment growth beyond GPU unit counts.

The traditional semiconductor evaluation framework, price-to-earnings relative to semiconductor peers and quarterly EPS beat size, systematically undervalues Nvidia’s platform and infrastructure characteristics. Analysts at Goldman Sachs, Morgan Stanley, and William Blair all recommend treating it as a platform company instead.

An investor using semiconductor-sector P/E benchmarks alone will perpetually conclude that Nvidia looks expensive. The question is whether those benchmarks are the right measuring stick, and the analyst consensus is increasingly that they are not.

| Metric | What it measures | Limitation for Nvidia analysis |

|---|---|---|

| Quarterly EPS beat | Backward-looking execution vs. consensus | Market already prices forward; beats alone do not drive sustained appreciation |

| P/E vs. semiconductor peers | Relative valuation within chip sector | Misses platform, software, and recurring revenue characteristics |

| Blended system ASP per rack | Total revenue captured per deployment | Not disclosed by Nvidia; requires analyst reconstruction |

| Networking revenue attach rate | Non-GPU revenue generated per GPU sold | Varies dramatically by customer segment; no GAAP disclosure |

| Software attach rate | Recurring and high-margin revenue trajectory | Currently qualitative; no standalone GAAP figure published |

Goldman Sachs recommends treating the four layers (GPU silicon, networking, systems, software) as distinct value drivers. William Blair’s vertically integrated AI platform framing forms the basis for assigning higher and more durable valuation multiples than a traditional GPU vendor would warrant. The blended system ASP per rack and software attach rate are the two metrics that capture what per-chip ASP does not: the compounding revenue from the layers built around the GPU.

The bear case against Nvidia’s infrastructure thesis is not that GPU demand disappears. It is that the non-GPU layers scale more slowly and unevenly than the bull case assumes.

Three distinct risk vectors warrant close tracking:

CUDA ecosystem lock-in is the moat characteristic that separates Nvidia from commodity accelerator manufacturers: Morningstar’s wide-moat rating framework applied to AI semiconductor companies treats proprietary software ecosystems and switching costs as the durable earnings advantages that justify premium valuation multiples over a full capital expenditure cycle.

Nvidia does not break out revenue concentration by individual hyperscaler customer in public filings, which limits precise modelling of the first risk.

Enterprise and sovereign AI adoption is the segment most critical to the non-GPU revenue thesis, and the pace of enterprise uptake remains the highest uncertainty in current analyst models. Software revenue scaling, from qualitatively important to quantitatively material, is the key transition point analysts are watching for in future earnings releases.

Nvidia’s long-term revenue story is not resolved by asking whether GPU demand persists. It is resolved by asking whether the networking, systems, and software layers scale in proportion to, or faster than, GPU revenue as AI capital expenditure matures.

Today’s Q1 FY2027 earnings call is a near-term test of this thesis. Beyond headline revenue, the signals to track are Q2 FY2027 guidance, any management commentary on systems and networking mix, and software attach trajectory. Investors who track Nvidia as a platform company with four compounding revenue layers are working with a structurally more accurate framework than those benchmarking it as a cyclical GPU hardware manufacturer.

Readers building or updating their Nvidia position models should review the Q1 FY2027 earnings transcript for management language on networking and systems contribution, not only the headline revenue and EPS figures.

Investors wanting to translate the four-layer platform framework into a specific portfolio decision will find our full explainer on Nvidia versus Broadcom valuations, which unpacks why Nvidia trades at approximately 24x forward earnings despite continued revenue acceleration while Broadcom commands 37x on contract-backed certainty, and examines whether both names can coexist in a single AI infrastructure allocation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The updated Nvidia investment thesis treats the company as a full-stack AI infrastructure platform with four revenue layers: GPU silicon, networking, systems, and software. Analysts at Goldman Sachs, Morgan Stanley, and William Blair argue this framework produces more accurate valuation models than benchmarking Nvidia against traditional semiconductor peers.

Nvidia has beaten consensus revenue and EPS estimates for more than two years, yet its stock has still lagged both the Philadelphia Semiconductor Index and the S&P 500 semiconductors sector year-to-date as of May 2026. Analysts describe this as a pattern where investors buy the anticipation and sell the confirmation, meaning the market prices forward expectations rather than rewarding backward beats.

Analysts recommend tracking blended system ASP per rack, networking revenue attach rate, and software attach rate alongside headline EPS, as these capture the compounding revenue from the non-GPU layers that quarterly beat size does not reflect. Q2 FY2027 guidance language and management commentary on networking and systems mix are also highlighted as higher-signal indicators than the reported quarter itself.

Nvidia earns networking revenue through InfiniBand, Ethernet, and NVLink products that attach to GPU sales, but the attach rate varies significantly by customer. Enterprise and sovereign AI customers typically purchase full integrated Nvidia racks and generate the highest networking attach, while hyperscalers like Meta and AWS that prefer Ethernet-based designs limit Nvidia's networking revenue even when buying Nvidia GPUs.

Three key risks are identified: hyperscaler custom silicon (Google TPUs, Amazon Trainium, Azure Maia) reducing full-rack adoption; Ethernet-preference deployments at Meta and AWS limiting InfiniBand networking attach; and potential GPU ASP pressure from AMD and Intel competition. Analysts note that CUDA ecosystem lock-in and rapid product cadence are the primary moats against these risks.