How Wesfarmers’ AI Strategy Is Built to Compound Returns

6 hrs ago

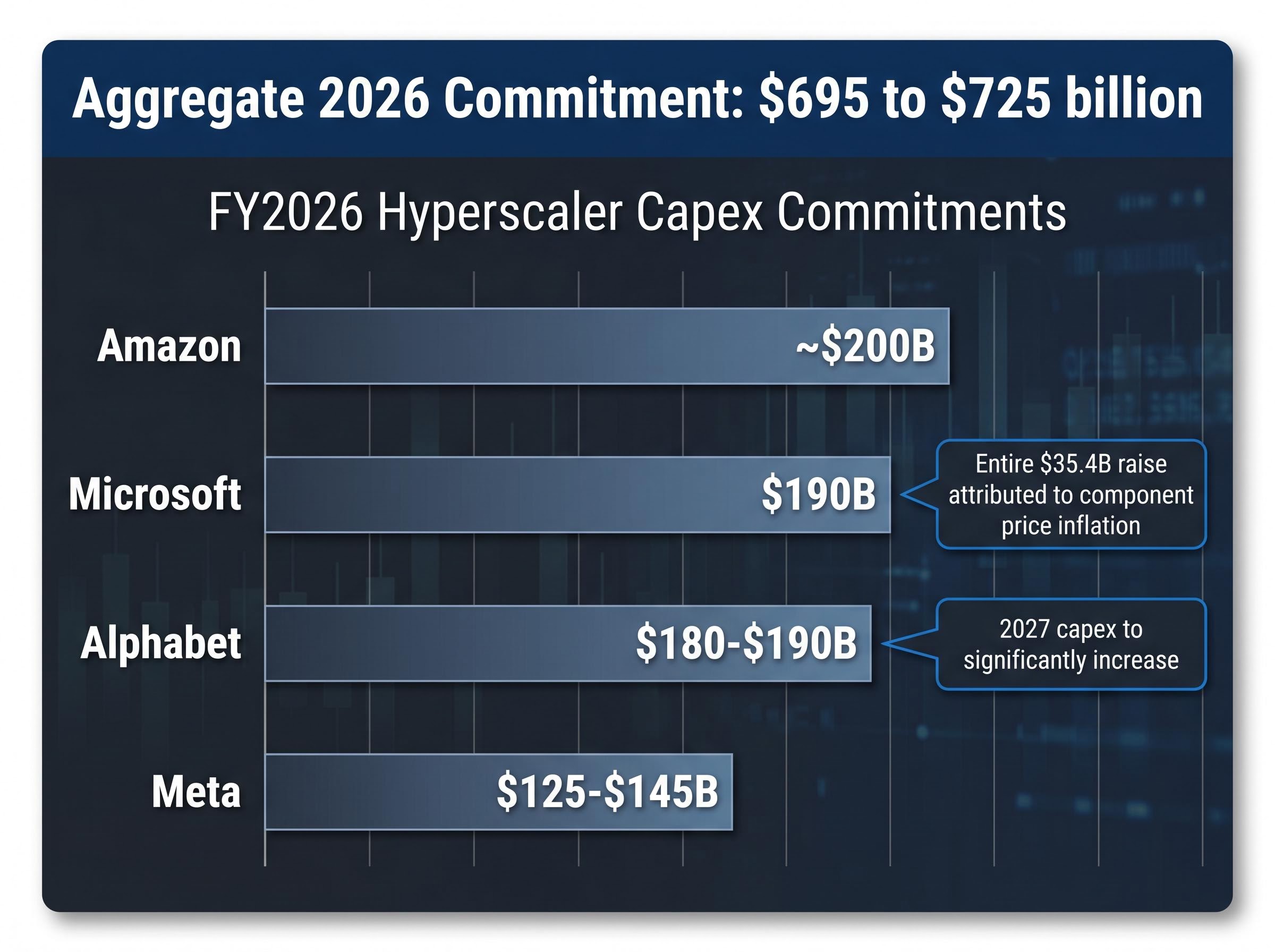

$695 to $725 billion. That is the aggregate capital expenditure commitment from Microsoft, Alphabet, Amazon, and Meta for 2026 alone, and every one of them raised guidance mid-cycle. The AI buildout is not decelerating. But the stocks riding it are not all equal.

The most recent earnings season produced a sharp bifurcation. Companies with proprietary silicon platforms and vertically integrated AI demand beat expectations and were rewarded. Commodity hardware suppliers beat on revenue and watched their shares fall anyway. Morningstar’s May 2026 sector analysis rates technology as the most undervalued sector at an 11% discount to fair value, yet simultaneously flags some hardware names as among the most overvalued in its coverage universe. The same theme is producing opposite outcomes depending on where in the stack a company sits.

What follows breaks down the structural logic separating wide-moat AI infrastructure leaders from commodity hardware plays, using Q1 2026 earnings data and Morningstar’s stock-level ratings to give readers a concrete framework for evaluating AI exposure in a portfolio.

The numbers arrive not as a single headline but as a sequence. Microsoft raised its FY2026 capex to $190 billion. Alphabet lifted its range to $180-$190 billion and signalled a “significant increase” for 2027. Amazon committed $200 billion, backing AWS’s fastest growth in 15 quarters. Meta raised its full-year target to $125-$145 billion despite actual Q1 spend of $19.84 billion coming in below the $27.57 billion estimate.

Taken individually, each raise could be dismissed as a single management decision. Taken together, the $695-$725 billion aggregate is a coordinated infrastructure cycle.

The most instructive detail sits inside Microsoft’s raise. CFO Amy Hood attributed the entire $35.4 billion increase to component price inflation, not new data centre projects.

Microsoft CFO Amy Hood attributed the entire $35.4 billion capex raise to higher component prices, not new projects, signalling that pricing power in this cycle sits with semiconductor suppliers, not with the hyperscalers writing the cheques.

That single attribution reframes who benefits from the spending. Alphabet’s language reinforced the demand side: CEO Sundar Pichai described the company as “compute constrained in the near term” and committed to a 2027 capex increase, a forward signal that supply has not caught up with demand. AWS posted $37.59 billion in Q1 revenue (up 28% year-on-year) at an operating margin of 37.7%, demonstrating that infrastructure spending is converting into profitable cloud demand, not just cost accumulation.

The financing structure behind the spending adds a layer that revenue figures alone do not reveal: hyperscaler debt issuance reached approximately $121 billion in 2025, roughly four times the five-year average, with another $100 billion projected in 2026, meaning the infrastructure cycle is increasingly funded by leverage rather than operating cash flow.

| Company | FY2026 Capex Commitment | Key Management Commentary |

|---|---|---|

| Microsoft | $190B | Entire $35.4B raise attributed to component price inflation |

| Alphabet | $180-$190B | “Compute constrained”; 2027 capex to “significantly increase” |

| Amazon | ~$200B | AWS fastest growth in 15 quarters; 37.7% operating margin |

| Meta | $125-$145B | Full-year raised despite below-estimate Q1 actual spend |

The term “wide moat” originates from Morningstar’s equity classification system. It describes a company whose competitive advantages are durable enough to sustain above-average returns for 20 years or more. In the AI infrastructure stack, the operative mechanism is not brand recognition or regulatory protection. It is switching costs: the financial, technical, and operational expense a customer would incur to replace a supplier.

Two companies illustrate structurally distinct versions of this lock-in. Broadcom builds custom accelerator chips (XPUs) for hyperscalers through co-development agreements that embed its silicon into the customer’s proprietary architecture. Six major hyperscaler customers now run on Broadcom’s XPU platforms. Replacing Broadcom would mean redesigning the chip, requalifying the hardware, and rewriting the software stack built around it. Nvidia, by contrast, sells a standardised GPU, but its CUDA software ecosystem creates a switching-cost layer above the hardware. Developers who build on CUDA face retraining costs and compatibility risks if they move to a competing platform.

Morningstar’s economic moat ratings define the criteria separating wide-moat companies from narrow or no-moat peers, with the 20-year durability threshold acting as the gating standard that places Nvidia and Broadcom in a structurally different category from commodity hardware vendors posting equally strong near-term revenue.

In both cases, the moat is architectural. The customer’s own infrastructure becomes dependent on the supplier’s design.

Commodity storage, networking, and general-purpose compute benefit from AI-driven demand surges. Revenue growth can be substantial during a build cycle. The distinction is durability. Once supply catches up to demand, commodity vendors lose pricing leverage because their products are substitutable.

These same vendors face input cost pressure from the component inflation that gives custom silicon suppliers their pricing power. The asymmetry compounds: custom silicon makers pass through higher prices to captive customers, while commodity hardware vendors absorb higher input costs without equivalent ability to raise their own.

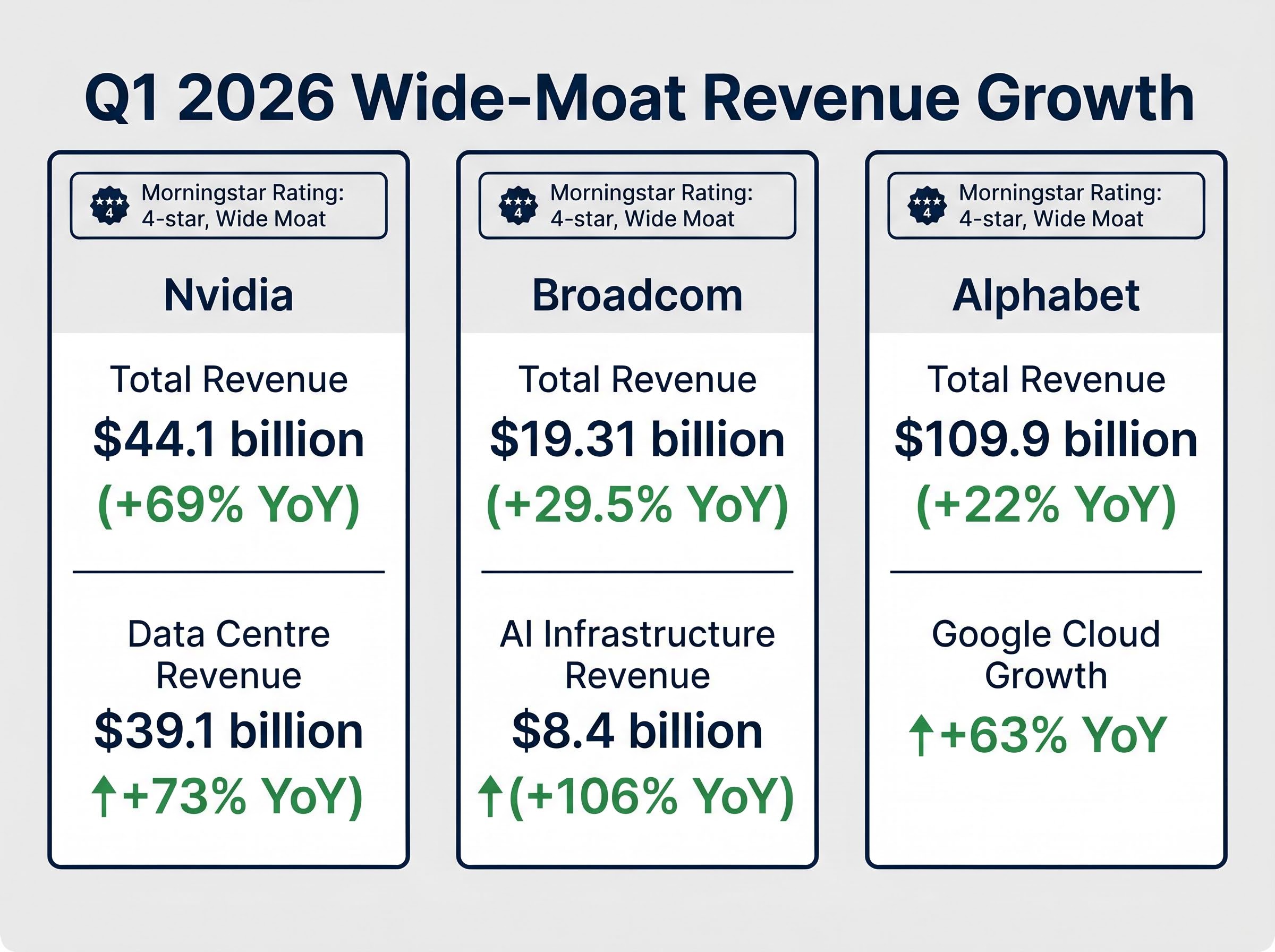

The Q1 2026 results from Nvidia, Broadcom, and Alphabet do not merely show strong quarters. They show the wide-moat thesis converting into reported numbers at scale, each through a distinct mechanism.

Nvidia’s Data Centre segment posted $39.1 billion in revenue, up 73% year-on-year. Total revenue reached $44.1 billion, a 69% increase. There is no deceleration signal in these figures.

Broadcom reported total revenue of $19.31 billion (up 29.5% year-on-year), with AI infrastructure revenue of $8.4 billion, a 106% year-on-year surge now representing 44% of total revenue. The quarter’s clearest proof of switching-cost lock-in came from a single announcement.

Broadcom CEO Hock Tan confirmed OpenAI as the company’s sixth major custom silicon customer. The two companies are co-developing a custom AI inference engine estimated at $10 billion or more, with mass production expected by late 2026.

A $10 billion co-development programme does not unwind easily. It is the definition of embedded switching costs at scale.

Alphabet posted $109.9 billion in revenue (up 22% year-on-year, its highest growth rate since 2022) and net income of $62.57 billion (up 81% year-on-year). Google Cloud grew 63% year-on-year, powered by internal AI demand that converts into external cloud revenue. This is vertical integration functioning as a moat: Alphabet’s own AI models drive infrastructure utilisation, which drives cloud revenue, which funds further capex.

AMD offers a secondary data point. Data Centre revenue reached $5.8 billion, up 57% year-on-year, demonstrating competitive traction at a scale still significantly behind Nvidia’s.

| Company | Q1 2026 Revenue Growth (YoY) | AI / Data Centre Growth (YoY) | Morningstar Rating |

|---|---|---|---|

| Nvidia | 69% | 73% (Data Centre) | 4-star, Wide Moat |

| Broadcom | 29.5% | 106% (AI Revenue) | 4-star, Wide Moat |

| Alphabet | 22% | 63% (Google Cloud) | 4-star, Wide Moat |

| AMD | 38% | 57% (Data Centre) | — |

Ciena reported Q1 2026 revenue of $1.43 billion, up 33% year-on-year. Adjusted earnings per share of $1.35 beat the headline estimate. The stock fell.

The decline came on weak full-year guidance and supply chain risk signals that the headline numbers obscured. This is the commodity trap in its clearest form: a company can ride the same AI infrastructure demand wave, beat on revenue and earnings, and still see its shares punished because the market is pricing the sustainability of the margin, not the size of the quarter.

Western Digital presents a quieter version of the same pattern. Revenue of $2.82 billion rose 27% year-on-year. Analyst ratings clustered at neutral and hold. Growth is not translating into a moat re-rating because the market recognises that general-purpose storage demand is cyclical, not structural.

The mechanism is straightforward. The same component price inflation that gives Broadcom and Nvidia pricing leverage creates input cost pressure for commodity hardware vendors. Custom silicon makers pass higher prices to customers locked into proprietary platforms. Commodity vendors absorb higher costs without equivalent ability to raise their own.

Supply chain bottlenecks, particularly memory shortages and grid power constraints, are now restricting the speed at which approved capex budgets convert into deployed infrastructure, creating a timing mismatch between hyperscaler commitment announcements and actual hardware vendor revenue recognition.

Morningstar’s May 2026 analysis projects that commodity hardware operating margins will compress materially once the current supply-demand imbalance corrects, as pricing power reverts from temporary scarcity to structural substitutability.

The warning signs apply beyond these two names:

Technology remains the most undervalued sector in Morningstar’s coverage universe as of May 2026, trading at an 11% discount to fair value even after April’s 17% rally. That discount did not exist two months earlier.

The timing matters. On 30 March 2026, the Morningstar US Growth Index was down more than 9% year-to-date and the Technology Index was down over 11%. Morningstar recommended rotating from energy and value into technology and AI at that point. Growth stocks then advanced approximately 12% in April. Technology advanced approximately 17%. The barbell reallocation thesis played out in real time, and the sector still has not closed the valuation gap.

Within technology, the dispersion is as important as the discount. Nvidia and Broadcom carry 4-star wide-moat ratings, positioning them as undervalued within an already undervalued sector. Ciena and Western Digital are flagged as overvalued. Small-cap equities sit at the deepest overall discount, 18% below fair value as of April 2026.

Semiconductor market concentration now sits at a record 13% of total US equity market capitalisation, a level that exceeds dot-com era peaks and means that even a selective correction in AI hardware names carries index-level implications for broadly diversified portfolios.

The $695-$725 billion in aggregate hyperscaler capex for 2026 is not a number that permits scepticism about the cycle’s existence. Alphabet’s commitment to “significantly increase” spending in 2027 extends the horizon further. AWS’s 37.7% operating margin at scale confirms that infrastructure spending is generating returns, not just consuming capital.

The market is not, however, rewarding the cycle indiscriminately. Microsoft shares fell approximately 5% in after-hours trading despite beating on revenue and raising capex guidance. The composite US equity price-to-fair-value ratio stood at 0.95 at the end of April 2026, recovering from a trough of 0.88 at end of March, but the recovery has been selective.

Alphabet CEO Sundar Pichai stated the company is “compute constrained in the near term,” framing the capacity gap as a demand confirmation rather than a supply warning.

Nvidia, Broadcom, and Alphabet sit at the intersection of Morningstar’s 4-star wide-moat ratings and structural demand that has not yet normalised. Commodity hardware names sit at the intersection of strong near-term revenue and a margin compression trajectory that the market is already pricing in.

The AI infrastructure cycle rewards precision, not participation. Knowing which side of the wide-moat divide a stock sits on may be the most important analytical decision an AI-focused investor can make in this market.

Inference cost economics introduce a risk that hardware revenue figures do not surface: if generative AI applications remain structurally unprofitable at scale, hyperscalers face pressure to decelerate capital deployment, which would unwind the demand signal that currently underpins semiconductor valuations regardless of moat width.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A wide-moat stock, as defined by Morningstar, is a company whose competitive advantages are durable enough to sustain above-average returns for 20 years or more. In AI infrastructure, this typically means proprietary silicon platforms, software ecosystem lock-in, or co-development agreements that make it costly for customers to switch suppliers.

Microsoft, Alphabet, Amazon, and Meta have collectively committed between $695 billion and $725 billion in capital expenditure for 2026, with each company raising its guidance mid-cycle, signalling that the AI buildout is accelerating rather than slowing.

Commodity hardware companies like Ciena saw share price declines after beating revenue estimates because the market was pricing in weak full-year guidance and the lack of structural pricing power, not just the size of the quarter. Investors recognised that margins are vulnerable once supply normalises and temporary scarcity pricing fades.

Morningstar's 4-star, wide-moat ratings on companies like Nvidia and Broadcom indicate they are undervalued within an already discounted technology sector, while overvalued flags on commodity names like Ciena and Western Digital signal margin compression risk. Checking the price-to-fair-value ratio alongside the moat rating helps investors avoid overpaying within the AI theme.

Key warning signs include a post-earnings share price decline despite a revenue beat, full-year guidance that lags the headline quarterly growth rate, analyst ratings clustering at neutral or hold, and the absence of any proprietary platform or co-development lock-in with major hyperscaler customers.