BofA Flags S&P 500 Decision Point With 6,850 Downside Target

4 hrs ago

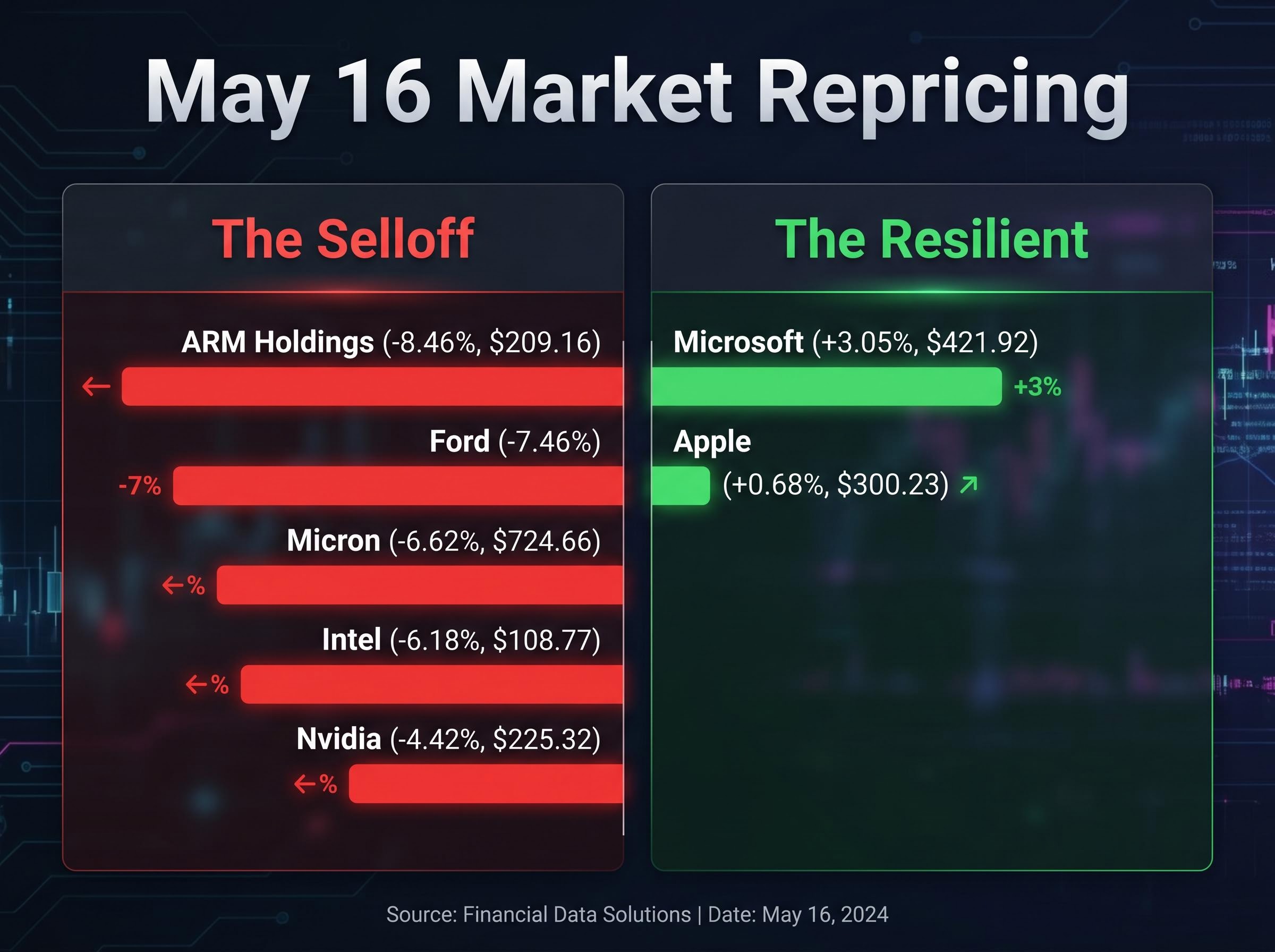

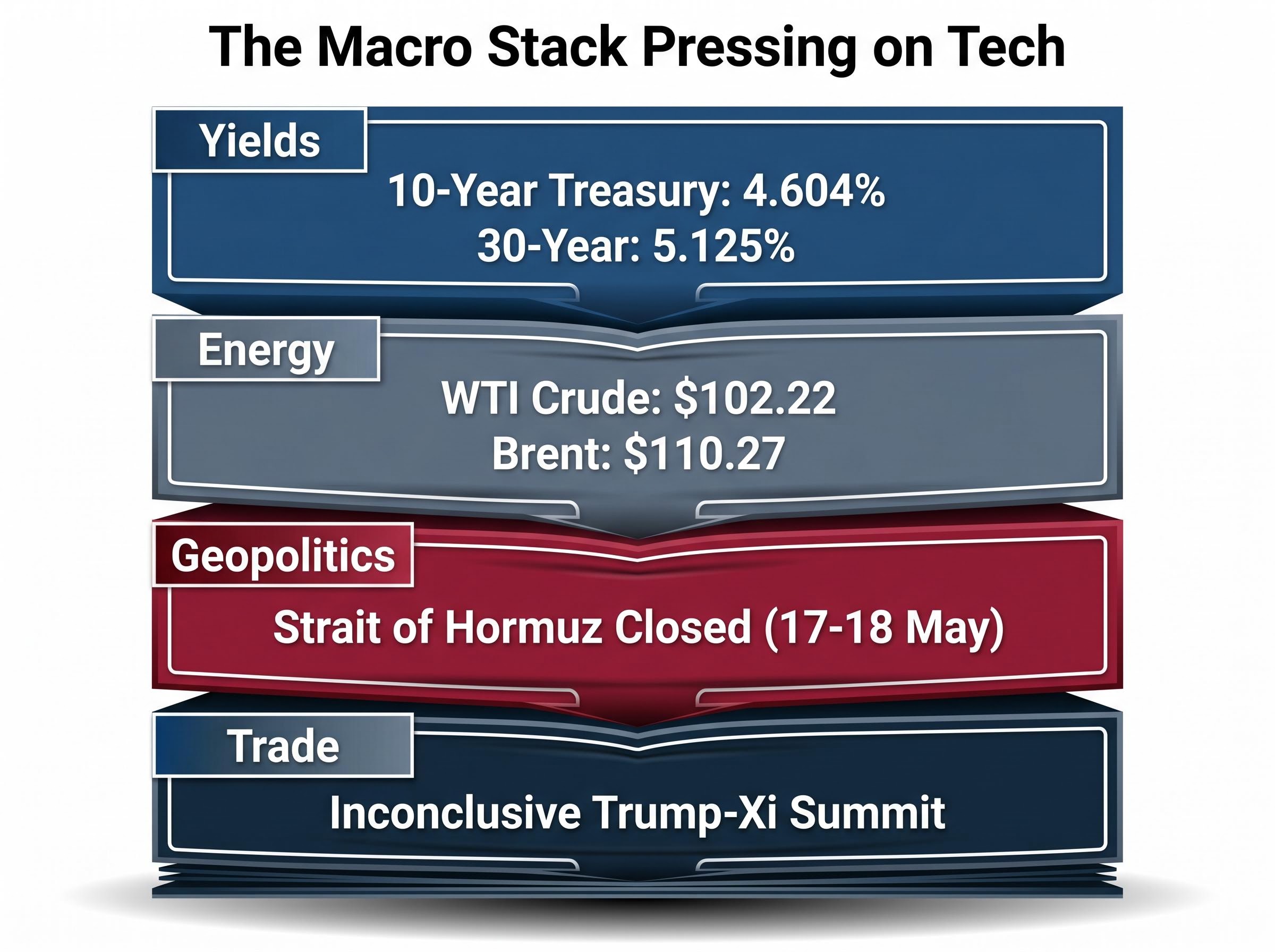

The semiconductor sector limped into earnings week carrying visible damage. ARM Holdings fell 8.46% to $209.16 on Friday, 16 May. Micron dropped 6.62% to $724.66. Intel shed 6.18% to $108.77. Nvidia itself closed at $225.32, down 4.42%. Beyond chips, Ford lost 7.46%, the S&P 500 fell 1.2%, and the Nasdaq slid 1.5%. The selloff was broad, coordinated, and landed two trading days before the company that arguably built the AI rally reports quarterly results. Nvidia releases Q1 FY2027 earnings on Wednesday, 20 May, after market close, into a backdrop of a 10-year Treasury yield at 4.6%, oil above $100 a barrel, and an inconclusive Trump-Xi summit that resolved nothing on export controls. The question facing investors is no longer whether AI demand is real. It is whether that demand is large enough, durable enough, and imminent enough to justify prices after seven consecutive weeks of S&P 500 gains. What follows is a framework for reading the numbers that matter on Wednesday, understanding how those numbers ripple through the broader tech trade, and using Thursday’s Walmart report to stress-test the macro assumptions underneath it all.

Friday’s semiconductor rout was not a collection of isolated stock moves. It was a sector-wide repricing of AI risk, driven by stretched valuations colliding with elevated yields and unresolved geopolitical friction.

Friday’s repricing landed across a sector already carrying semiconductor valuation extremes that vary sharply by name: Micron trades below 9x forward earnings while Intel sits near 101x, a dispersion that explains why a sector-level selloff affects individual stocks very differently depending on where each name sits in the valuation distribution.

The damage was specific and widespread:

The VIX rose 6.78% to 18.43 on the same session, a clear signal that hedging demand was climbing across the broader market, not just within tech.

With the 10-year Treasury yield at 4.604%, higher discount rates pressed down on the valuations of long-duration growth names. The market was front-running earnings anxiety. For investors, the distinction matters: if Friday’s selloff reflected genuine fundamental concern about AI spending durability, a strong Nvidia print may not fully reverse the damage. If it was mechanical, yield-driven derating, a beat could snap prices back quickly.

Three figures will determine whether Nvidia’s Wednesday report stabilises the AI trade or accelerates the repricing that began on Friday. Each carries a different signal, and none of them is the headline EPS number.

| Metric | What Nvidia guided or reported | Why it moves the stock |

|---|---|---|

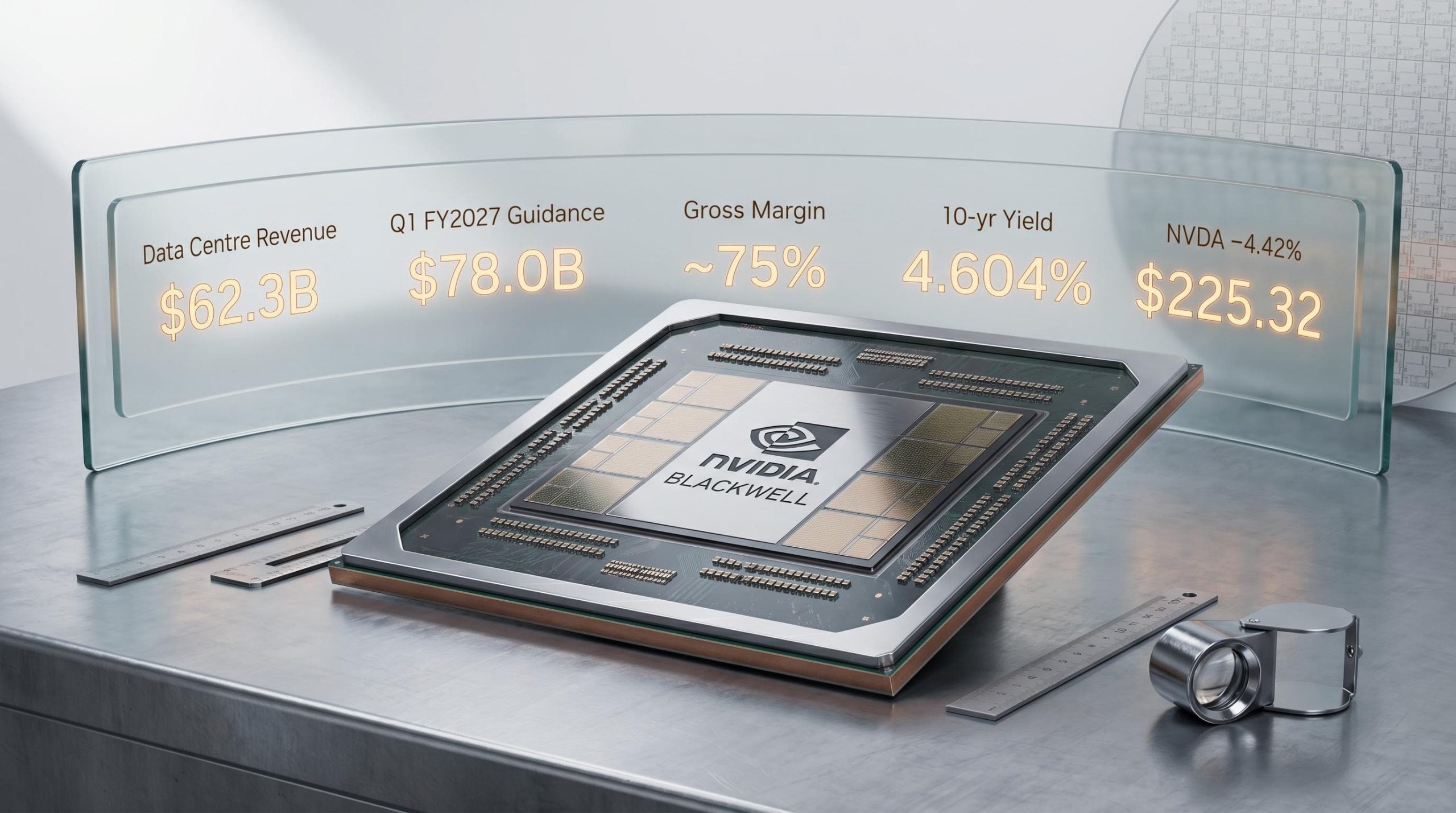

| Data Centre revenue | Q4 FY2026 record of $62.3 billion (up 22% QoQ, 75% YoY); FY2026 full-year $193.7 billion | The single largest revenue line and the direct measure of hyperscaler AI spending commitment |

| Non-GAAP gross margin | Guided to approximately 75.0% (plus or minus 50 bps) | Signals Blackwell pricing power versus rising input costs from HBM memory and CoWoS packaging |

| Q2 FY2027 forward guidance | Not yet issued; Q1 revenue guided at $78.0 billion (plus or minus 2%, excluding China Data Centre compute) | Forward outlook language historically moves Nvidia’s stock more than the reported quarter |

Data Centre revenue is the headline metric. The $62.3 billion Q4 figure set the benchmark. Whether Q1 sustains that trajectory or shows deceleration as the Hopper cycle matures will shape how the Street models FY2027 run-rate revenue.

Gross margin at 75% is the second signal. If Nvidia holds mid-70s margins while ramping Blackwell production, it confirms pricing power against tight HBM supply and constrained TSMC advanced packaging capacity. Any compression would be read as evidence that the cost of scaling AI infrastructure is catching up with demand.

The third number, Q2 guidance, arguably carries the most weight. Approximate Street consensus places Q1 EPS near $1.70, though this figure remains unverified through free public sources and should be treated as directional. The asymmetry is well established in Nvidia’s recent reporting history: strong forward guidance on Blackwell demand can overcome a minor EPS miss, while cautious language on shipment pace can erase gains even on a numerical beat.

The quarter Nvidia is reporting looks backward. The question institutional capital is actually pricing looks forward: is the Blackwell cycle unfolding on the timeline the AI trade requires?

The structural tension underneath that question is a well-documented capex-to-revenue lag of 18-24 months, a window in which hyperscaler spending is already committed but the inference revenue justifying it remains unproven at scale.

Nvidia introduced the Blackwell platform at GTC in March 2025, positioning it as the successor to the Hopper architecture that powered the 2023-2025 AI buildout. The transition from Hopper to Blackwell is the structural inflection point. Microsoft, Meta, Alphabet, and Amazon committed capital expenditure based on assumptions about Blackwell’s performance and availability. Wednesday’s commentary on shipment timing, production scale, and customer commitment levels will either validate or complicate those assumptions.

Key risk factors for the Blackwell ramp include:

Nvidia’s decision to exclude China Data Centre compute revenue from its $78.0 billion Q1 guidance is not a temporary adjustment. The inconclusive Trump-Xi Beijing summit, which concluded without major agreements, reinforces that export controls are a structural headwind rather than a negotiating position awaiting resolution.

For investors holding Microsoft, Meta, Alphabet, or AMD, the Blackwell commentary is a direct read on AI infrastructure capex over the next 12 to 18 months, with downstream implications for cloud margins and software adoption curves.

Many investors hold Nvidia exposure indirectly, through broad tech ETFs, hyperscaler positions, or semiconductor index funds. Understanding the transmission mechanism between Nvidia’s Data Centre revenue and those holdings turns Wednesday’s report from a single-stock event into a portfolio-level signal.

The causal chain operates in four steps:

The Philadelphia Semiconductor Index (SOX) is the sector-wide barometer that captures the first-order effect. The second-order effect flows through the cloud names.

Broadcom’s custom ASIC model represents the alternative structural position within the same AI buildout: while Nvidia’s GPU revenue is tied to the Blackwell ramp timeline, Broadcom’s locked-in multi-year contracts with Google and Meta extend through at least 2029 and command a forward multiple of approximately 37x, with both names frequently coexisting within the same hyperscaler data centre.

A strong Nvidia report with firm Blackwell guidance would likely be read as confirmation that AI capex is intact despite macro headwinds. SOX constituents, Microsoft (which closed at $421.92, up 3.05% on Friday despite the broader selloff), Meta, Alphabet, and Amazon would be the direct beneficiaries. The resilience Microsoft showed on the same day chip names sold off already hinted at where the market sees AI cloud demand holding.

At a 10-year yield of 4.6%, the margin for guidance disappointment is narrow. High-multiple AI names are priced for continued spending acceleration. Cautious Blackwell commentary or gross margin compression would trigger valuation repricing across the SOX, and the damage would not stop at semiconductors. Software names trading on AI adoption assumptions would face the sharpest compression.

The same Nvidia earnings print would be received differently in a different rate or geopolitical environment. The macro backdrop is not background colour; it is an active force multiplier on the market’s reaction.

| Macro factor | Implication for Nvidia and AI tech |

|---|---|

| 10-year Treasury yield at 4.604% | Compresses valuations of long-duration growth stocks; raises the bar for guidance quality |

| WTI crude above $100 ($102.22) | Inflationary pressure delays Fed easing; drags consumer spending that Walmart will quantify |

| Strait of Hormuz reported effectively closed (17-18 May) | Sustains geopolitical risk premium in energy; Brent at $110.27 |

| Trump-Xi summit without agreement | No relief on China export controls; structural headwind for Nvidia’s addressable market |

| Above-forecast inflation print (prior week) | Reinforces higher-for-longer rate expectations; narrows the margin for earnings disappointment |

The 10-year yield at 4.604% and the 30-year at 5.125% represent the most structurally significant macro factor for growth equity pricing. Higher real yields increase the discount rate applied to future earnings, meaning the same EPS beat delivers less valuation lift than it would in a lower-rate environment.

The yield pressure is not an isolated US phenomenon: the synchronised sovereign bond selloff spanning US Treasuries, UK gilts, and Japanese JGBs reflects four reinforcing drivers, including above-consensus inflation, elevated energy prices, contagion from rising US term premia, and a geopolitical risk premium, that collectively push back the timeline for rate relief growth stocks require.

The Federal Reserve Financial Stability Report, published in May 2026, noted that equity valuations remained elevated while the equity risk premium stayed well below its historical average, a combination that leaves growth stocks with limited cushion against guidance disappointments when Treasury term premiums are simultaneously rising.

Trump’s Truth Social warning to Iran, posted on Sunday, 17 May, added another layer of uncertainty to an already pressured energy picture. With WTI at $102.22 (up $1.20, or 1.19%) and the Strait of Hormuz disrupted, the inflationary impulse is direct: higher gasoline prices compress consumer spending and push back the timeline for Federal Reserve rate cuts that growth stocks need for multiple expansion.

Investors who understand this multiplier effect can calibrate their reaction more precisely. A small beat in this environment may produce less upside than the same beat would have delivered a quarter ago.

Walmart reports Q1 FY2026 results on the morning of Thursday, 22 May, less than 18 hours after Nvidia’s conference call. The pairing is not coincidental in its analytical value. Nvidia tests whether AI infrastructure demand can sustain the tech rally. Walmart tests whether the U.S. consumer can sustain the economy underneath it.

Three metrics deserve attention:

With WTI at $102.22, the connection between Walmart’s results and the broader inflation picture is direct. Oil above $100 feeds into gasoline prices, which compress discretionary spending, which shows up in Walmart’s category mix before it shows up in GDP data.

Walmart shares were down 0.76% heading into the week. If the consumer is weakening, the soft-landing thesis that supports corporate AI capex spending becomes harder to sustain. If Walmart shows resilient traffic with value-oriented baskets, the macro foundation holds, at least for now.

The analysis above points to a specific framework for reading this week’s two reports. Not every data point deserves a portfolio response, and distinguishing signal from noise before results arrive is more valuable than reacting after them.

The five-point decision framework:

Nvidia’s conference call begins at 5:00 PM ET on Wednesday, 20 May. The EPS figure will arrive first. The guidance language will arrive during the call. For investors evaluating their tech exposure, the second is more consequential than the first.

The two reports function as a paired test. Nvidia measures AI infrastructure demand from the supply side. Walmart measures U.S. consumer health from the demand side. Both confirming strength, or both disappointing, would send a cleaner signal than a split result.

A split outcome, where Nvidia beats while Walmart weakens, or vice versa, would suggest a divergence between the AI spending cycle and the broader economic foundation. Apple, which closed at $300.23 (up 0.68% on Friday despite the selloff), and Microsoft at $421.92 (up 3.05%) already illustrate that the market is differentiating within tech. This week’s two reports will sharpen that differentiation or resolve it.

S&P 500 futures were down 0.3% and Nasdaq 100 futures were down 0.4% on Sunday evening, 17 May. The market is not waiting passively.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Nvidia releases its Q1 FY2027 earnings after market close on Wednesday, 20 May, with the conference call beginning at 5:00 PM ET.

Data Centre revenue is the single most important metric, as it directly measures hyperscaler AI spending commitment; the Q4 FY2026 record of $62.3 billion sets the baseline investors will compare against.

The Friday, 16 May selloff reflected stretched AI valuations colliding with a 10-year Treasury yield at 4.6%, unresolved China export control uncertainty, and broader geopolitical friction, causing sector-wide repricing before any earnings figures were reported.

Nvidia's Data Centre revenue signals the pace of AI accelerator purchases by cloud hyperscalers; strong results typically support capital expenditure commitments at Microsoft, Meta, Alphabet, and Amazon, while cautious guidance can trigger valuation compression across AI-linked software and cloud names.

Walmart's Q1 FY2026 results on Thursday, 22 May, provide a read on U.S. consumer health; if consumer spending is weakening under oil above $100 a barrel, the soft-landing thesis supporting corporate AI capital expenditure becomes harder to sustain.