Nvidia just guided Q2 FY2027 revenue to $91 billion while explicitly assuming zero contribution from Chinese data centre compute sales. Strip away the headline beat, and that single sentence is the most analytically significant thing management communicated on 20 May 2026. Q1 FY2027 revenue of $81.61 billion arrived roughly 3% above an already elevated consensus, with adjusted earnings per share of $1.87 beating by approximately 6% and Data Centre revenue of $75.2 billion growing 92% year on year. Those figures are large enough to stand on their own, yet the after-hours stock reaction, a decline of approximately 1.0%-1.5%, signals that investors are searching for the next layer of meaning rather than celebrating the current quarter. This analysis unpacks what the results actually mean beneath the headline numbers: what the China-zero guidance construct implies about optionality, what the Vera CPU announcement signals about Nvidia’s long-term addressable market, and what an $80 billion buyback plus a 25x dividend increase communicates about management’s view of the company’s own trajectory.

The numbers that matter, and the one figure hiding in the footnotes

The Q1 FY2027 beat was broad-based, touching every metric that institutional models track closely. The table below summarises the reported figures against consensus and prior-year comparisons.

| Metric | Reported | Consensus | Beat/Miss | Year-on-Year Change |

|---|---|---|---|---|

| Revenue | $81.61B | ~$78-79B | ~3% beat | Strong growth |

| Adjusted EPS | $1.87 | ~$1.77 | ~6% beat | Significant increase |

| Data Centre Revenue | $75.2B | ~$73B | ~3% beat | +92% |

| Adjusted Gross Margin | 75.0% | ~74.5% | +50 bps | Expansion |

In isolation, these are confirmation numbers. The demand environment for AI accelerators has been signalling strength for over a year, and the Q1 results validate that signal rather than surprise with it.

The Q2 guidance figure is where the analytical weight sits. Nvidia guided Q2 FY2027 revenue to $91.0 billion, plus or minus 2%, against a consensus of approximately $87.2 billion, a beat of roughly $3.8 billion at the midpoint. More importantly, the company’s 8-K filing contained an explicit disclosure that reframes the entire number.

Nvidia’s 8-K Filing Disclosure: The company stated it is “not assuming any Data Center compute revenue from China” in its Q2 FY2027 outlook. This language appeared directly in the earnings release and was foregrounded by management, making it a deliberate signal about optionality rather than a conservative accounting footnote.

That construct converts the guidance from a standalone beat into an asymmetric optionality statement. Any relaxation of US export restrictions on advanced AI accelerators sold into China would be additive to a figure that already clears consensus by $3.8 billion.

Institutional investors at BlackRock, Goldman Sachs, and Vanguard have largely formalised their treatment of China upside as a call option on geopolitical resolution, building price targets on US and allied market demand alone, a framework that makes the zero-China Q2 guide easier to interpret once the analytical starting point is clear.

The BIS semiconductor export licensing policy for China establishes the formal framework governing which advanced AI accelerator products require individual licences before sale into Chinese data centres, making it the direct regulatory mechanism that any future easing of restrictions would need to modify before Nvidia could recognise revenue from that market.

When big ASX news breaks, our subscribers know first

What management’s “largest buildout in human history” claim actually tells investors

How rental pricing signals something beyond ordinary hardware cycles

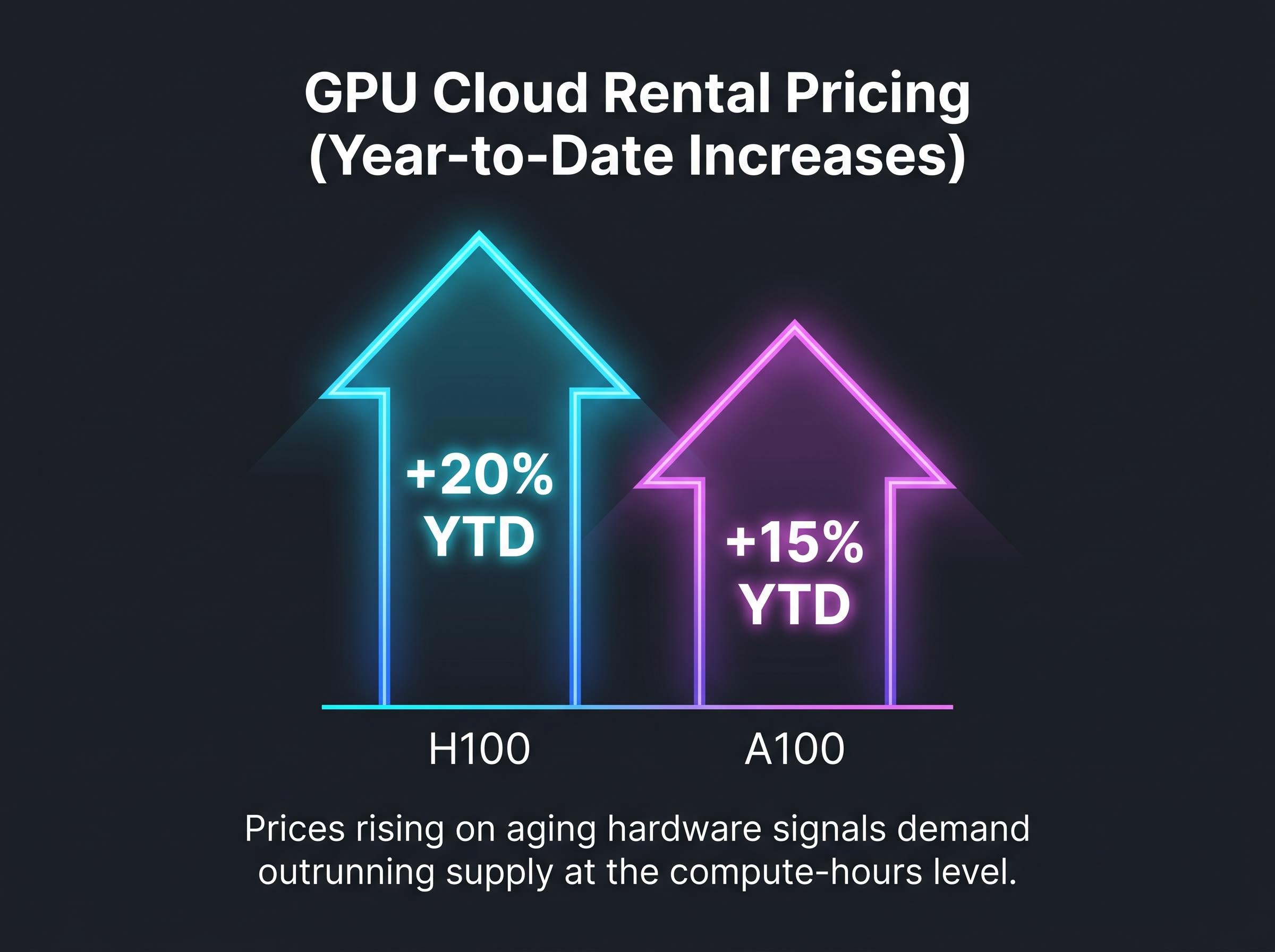

Hardware rental prices typically decline as equipment ages and newer generations enter the market. What is happening in the GPU cloud rental market as of Q1 FY2027 runs counter to that pattern. H100 rental pricing increased approximately 20% year to date, and A100 cloud pricing rose approximately 15% over the same period, according to management commentary during the earnings call. When prices rise on hardware that is past its peak depreciation curve, the signal is that utilisation rates are running at or near capacity, meaning demand is outrunning supply not just at the silicon level but at the compute-hours level.

Management framed this by stating that the platform’s value now exceeds its depreciable hardware life. That is the core claim behind the pricing observation, and it distinguishes the current demand cycle from ordinary hardware refresh patterns.

Nvidia’s characterisation of the current environment as “the largest buildout in human history” is a large claim, but the pricing data lends it specific empirical support. The hyperscaler capex commitments reinforce the picture from the demand side:

- Microsoft is maintaining elevated AI and data centre capex to support Azure capacity and OpenAI workload growth through 2026.

- Alphabet has flagged growing data centre and AI infrastructure spend, encompassing both TPU and GPU procurement.

- Amazon is executing an AWS infrastructure build that includes third-party GPU procurement alongside its own Trainium and Inferentia silicon development.

- Meta has raised its multi-year AI infrastructure capex range, investing heavily in GPU clusters for its AI development programmes.

A precise consolidated 2026 AI-specific total across all four firms is not available from a single public source, but the directional signal is consistent: all four are spending more, not less. Management noted that Nvidia revenue growth should outpace hyperscaler capex growth, a claim that the Q1 results and Q2 guidance appear to support at least directionally.

The hyperscaler capex trajectory heading into this earnings cycle provided the demand-side foundation for Nvidia’s guide: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion on AI infrastructure in Q1 2026 alone, with full-year 2026 combined guidance reaching approximately $725 billion, a figure that management’s claim about outpacing hyperscaler capex growth was tested against.

What Nvidia is as a business in 2026, and why that matters for evaluating the results

Readers who approach Nvidia as a traditional semiconductor company risk misinterpreting the Q1 results entirely. Data Centre segment revenue of $75.2 billion represented approximately 92% of total Q1 FY2027 revenue. The segment sells GPUs, networking equipment (including InfiniBand, acquired through the Mellanox acquisition), and associated systems designed for AI training and inference workloads. This is not a diversified chipmaker; it is an AI infrastructure company with a hardware delivery mechanism.

The software layer matters as much as the silicon. CUDA, Nvidia’s proprietary programming model, means that the ecosystem of AI frameworks, libraries, and developer workflows is tightly coupled to Nvidia hardware. Switching costs are not primarily about hardware performance; they are about the years of software tooling and developer muscle memory built on top of CUDA. That coupling creates a moat that competitors have yet to displace as of May 2026.

The competitive alternatives fall into three categories:

- AMD GPU competition: The Instinct MI300 series has gained hyperscaler trial traction in early 2026, framed by customers as a diversification effort rather than a direct displacement of Nvidia’s position.

- Hyperscaler custom silicon: Google TPU v5, Amazon Trainium and Inferentia, and Microsoft Maia each represent proprietary silicon investments targeting specific workloads, reducing single-vendor dependency over time.

- Other accelerator vendors: Intel’s Gaudi line and smaller entrants are present in the market but have not achieved the scale needed to alter competitive share dynamics measurably.

No quantified post-January 2026 market share shift data is available for competitive analysis. The qualitative picture is one of diversification pressure rather than displacement.

The Vera CPU announcement and what a new addressable market means for Nvidia’s growth ceiling

Nvidia has operated almost exclusively in the GPU and accelerator market for the entirety of its Data Centre segment’s rise. CPUs have been Intel and AMD territory. The Vera CPU announcement, timed to this earnings cycle, represents a deliberate expansion into server CPU workloads where hyperscalers are already engaged as partners. Management identified a new total addressable market (TAM) of approximately $200 billion, a figure framed as representing a market Nvidia had not previously targeted, meaning it is incremental to existing segments rather than a redistribution of share within them.

The CPU-to-GPU deployment ratio compressing from a historical 1:8 toward 1:1 in agentic AI infrastructure is the structural driver behind the Vera CPU TAM claim, with research from Georgia Tech and Intel finding that CPU tool processing accounts for 50-90% of total latency in agentic workflows, making CPUs a co-requirement alongside GPU clusters rather than a secondary component in next-generation data centre builds.

The distinction matters. When a company already dominating one segment identifies a $200 billion adjacent market and announces that major hyperscalers and system manufacturers are already engaged as partners, the TAM claim carries structural credibility rather than being purely aspirational.

Management’s Vera Rubin Commentary: Nvidia characterised its Vera Rubin architecture as likely to be more commercially successful than Grace Blackwell, with all leading frontier AI model developers expected to adopt it immediately upon availability. Management also stated that supply is anticipated to be constrained throughout Vera Rubin’s entire commercial life.

That supply constraint framing is not incidental. It signals that management expects demand to exceed manufacturing capacity from launch through the product’s entire cycle, a condition that, if accurate, would support pricing power and margin durability across the architecture’s lifespan.

What the capital return programme communicates about management’s confidence in the trajectory ahead

Capital return decisions commit real cash rather than expressing an aspiration. That distinction makes them among the most credible forward-looking signals available to outside investors. Nvidia’s announcement in this earnings cycle included an $80 billion share buyback authorisation and a quarterly dividend increase from $0.01 to $0.25 per share, a 25x increase. Approximately $20 billion was returned to shareholders in Q1 FY2027 alone.

How does this differ from routine capital return activity?

- Scale of the buyback authorisation: $80 billion represents a significant portion of any reasonable free cash flow forecast and signals that management views its own shares as an attractive use of capital at current valuations, an implicit statement about internal confidence.

- Magnitude of the dividend reset: A 25x increase is not a routine yield adjustment. It is a structural reset of Nvidia’s capital return policy, signalling that the cash generation profile is both large and durable enough to support a materially higher ongoing commitment.

- Timing alongside forward guidance: Announcing this capital return scale in the same release as a $91 billion Q2 guide built on zero-China assumptions suggests management sees cash generation headroom even beyond the already elevated revenue trajectory.

Pre-earnings analyst price targets reflected growing confidence in the company’s trajectory, with KeyBanc raising its target to $300 and Bank of America raising to $320 ahead of the 20 May release.

The next major ASX story will hit our subscribers first

What the post-results stock reaction reveals about where consensus expectations now sit

Nvidia declined approximately 1.0%-1.5% in after-hours trading following a release that beat on every major metric. On the same evening, the S&P 500 rose 1.1%, the Nasdaq gained 1.5%, and US Treasury yields fell 7-10 basis points on progress in US-Iran diplomatic discussions. The general risk-on backdrop was supportive. Nvidia’s after-hours reaction was not macro-driven; it was specific to positioning.

The decline reflects a market that had already priced in a beat of this magnitude and is now asking what the next increment of upside looks like. The April FOMC minutes, also released in the same session, added a layer of complexity: a majority of participants signalled openness to rate increases if inflation remains persistently elevated, with market pricing implying approximately 14 basis points of Fed rate cuts through year-end 2026 as of 21 May.

Bull case catalysts from here

- China export restriction easing: Any policy relaxation represents pure additive upside to the zero-China $91 billion Q2 guide.

- Vera CPU TAM materialisation: Nvidia entering a $200 billion market it has not previously addressed, with hyperscaler partnerships already confirmed.

- Vera Rubin supply ramp: Meeting anticipated demand from frontier AI model developers on schedule would extend the pricing power and margin dynamics observed in Q1.

Beijing’s import block on H200 shipments, operating through informal buyer pressure rather than formal regulation, explains why the US policy shift from presumption-of-denial to case-by-case review in January 2026 has not translated into commercial revenue despite Washington clearing sales to Alibaba, Tencent, and ByteDance.

Bear case risks to monitor

- Hyperscaler capex cycle risk: If any of the four major customers moderates spending, Nvidia’s revenue concentration in Data Centre amplifies the impact.

- Rising rate environment: FOMC minutes signal policy tightening risk that historically pressures high-multiple growth equities.

- Competitive displacement: AMD MI300 traction and hyperscaler custom silicon investment represent medium-term diversification pressure, even if near-term displacement remains limited.

- Geopolitical binary: If US-Iran tensions re-escalate and oil prices rebound, the macro backdrop supporting the 20 May equity rally reverses.

The after-hours reaction is not a signal that the results were disappointing. It is a signal about where consensus expectations have moved and what incremental catalysts the market now requires.

The supercycle thesis, tested against one quarter’s results

Three elements of the Q1 FY2027 results provide meaningful confirmation that the demand substrate behind AI infrastructure spending is durable and broadening. The $91 billion Q2 guide built on zero-China assumptions demonstrates that non-China demand alone exceeds prior consensus. The H100 and A100 rental pricing increases confirm that utilisation rates, not just procurement volumes, are running at elevated levels. The Vera CPU’s $200 billion TAM expansion, with hyperscaler partnerships already in place, signals that Nvidia’s addressable revenue ceiling is rising, not static.

What remains unresolved is equally important:

- Whether Vera Rubin’s supply ramp meets demand on schedule, as management anticipates supply constraints throughout its commercial life.

- Whether Vera CPU hyperscaler partnerships translate into revenue at the scale the $200 billion TAM implies, given that CPU markets have their own entrenched competitive dynamics.

- Whether the rate environment deteriorates enough to create valuation compression even against strong fundamentals; data showing the MSCI Asia Pacific Index declined in 16 of 19 weeks over the prior five years during periods when the US 10-year Treasury yield rose by 20 basis points or more illustrates the macro sensitivity facing high-growth equity names.

One quarter cannot confirm or deny a multi-year structural thesis, but it can shift the probability distribution. This quarter’s results shift it meaningfully toward confirmation on the demand side while leaving the supply ramp, moat durability, and macro questions appropriately open.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.