Options markets are pricing a post-earnings swing of roughly plus or minus 5.8% in Nvidia shares when the chipmaker reports Q1 FY2027 results after the close on Wednesday, May 20. On a company carrying one of the largest market capitalisations in global equities, that implied move translates into hundreds of billions of dollars of value at stake in a single session.

The report arrives at a moment when the AI infrastructure buildout has produced a demand backstop without precedent. Four hyperscalers have committed an aggregate $710-$725 billion in 2026 capital expenditure, and Wall Street has been revising Nvidia earnings estimates upward in the days immediately preceding the print. At the same time, a China export licensing variable introduced by Jensen Huang’s May 13-15 Beijing visit and a rate-sensitive macro backdrop mean the market’s reaction to even a comfortable beat is far from guaranteed.

What follows is a framework covering the consensus numbers the Street expects, the hyperscaler capex signal underpinning Nvidia’s demand thesis, how options-implied volatility translates into practical position risk, the China wildcard that could move the stock independently of headline results, and the macro conditions capable of overriding a strong quarter. The goal: a complete risk-and-opportunity picture before the bell on May 20.

What Wall Street expects from Nvidia on May 20

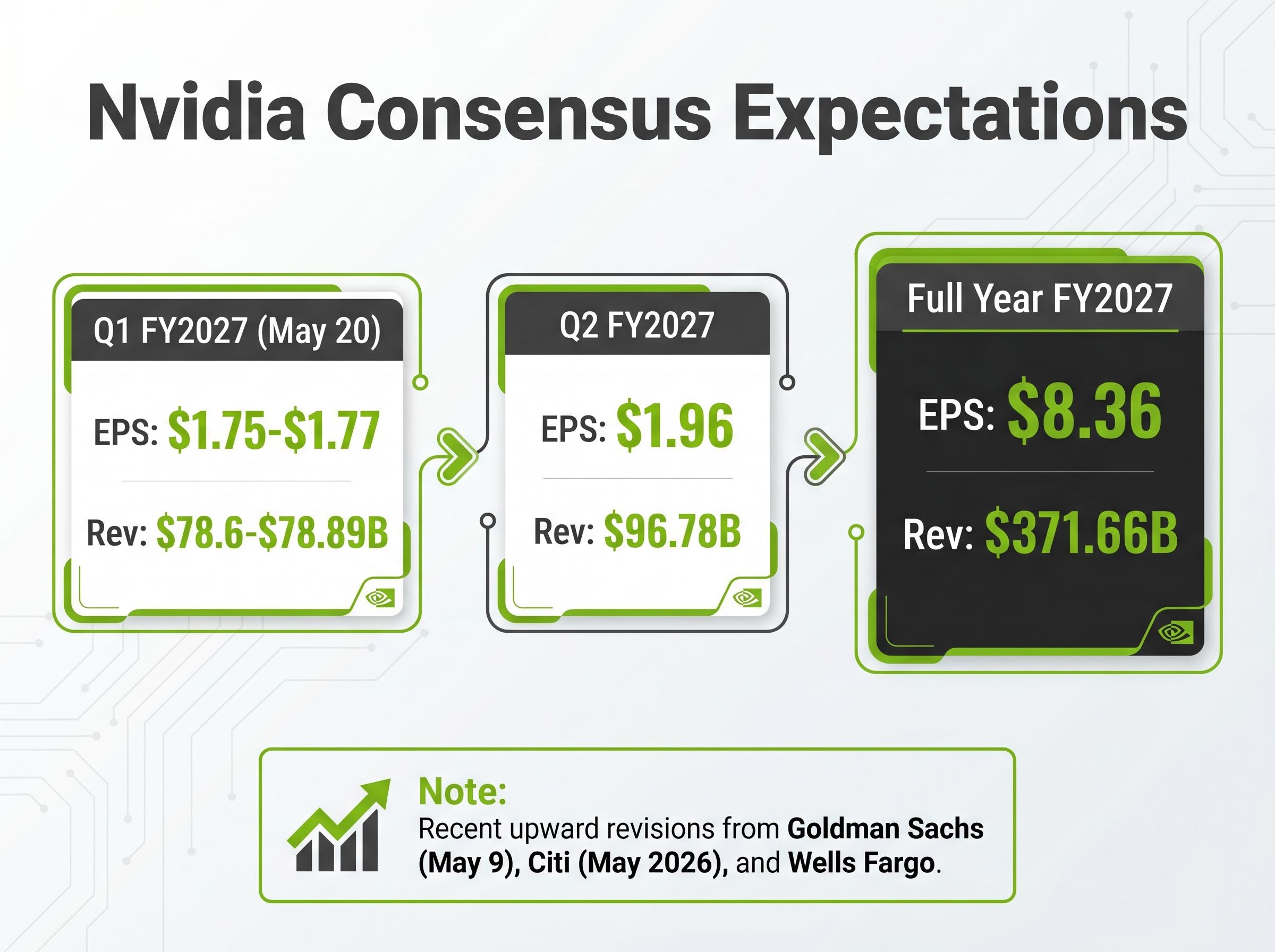

The published consensus heading into the print sits at an adjusted EPS of $1.75-$1.77 on revenue of $78.6-$78.89 billion. Those are the figures the headline reaction will be measured against.

| Period | EPS (Adjusted) | Revenue |

|---|---|---|

| Q1 FY2027 (May 20 print) | $1.75-$1.77 | $78.6-$78.89B |

| Q2 FY2027 (next quarter) | $1.96 | $96.78B |

| Full Year FY2027 | $8.36 | $371.66B |

The published number, however, is not the real bar. In the week of May 9-16, multiple banks pushed their estimates higher, narrowing the room for a positive surprise.

Goldman Sachs raised its targets on May 9. Citi issued an updated note in May 2026. Wells Fargo revised upward in the same window. The effective whisper number now sits above the published consensus, and that is the threshold the stock reaction will price against.

Forward guidance matters at least as much as the backward-looking print. Next-quarter consensus of $1.96 EPS on $96.78 billion in revenue, and the full-year target of $8.36 EPS on $371.66 billion, will determine whether any beat translates into sustained price appreciation or a sell-the-news reaction.

When big ASX news breaks, our subscribers know first

Why $710 billion in hyperscaler capex is the most important demand signal Nvidia has ever had

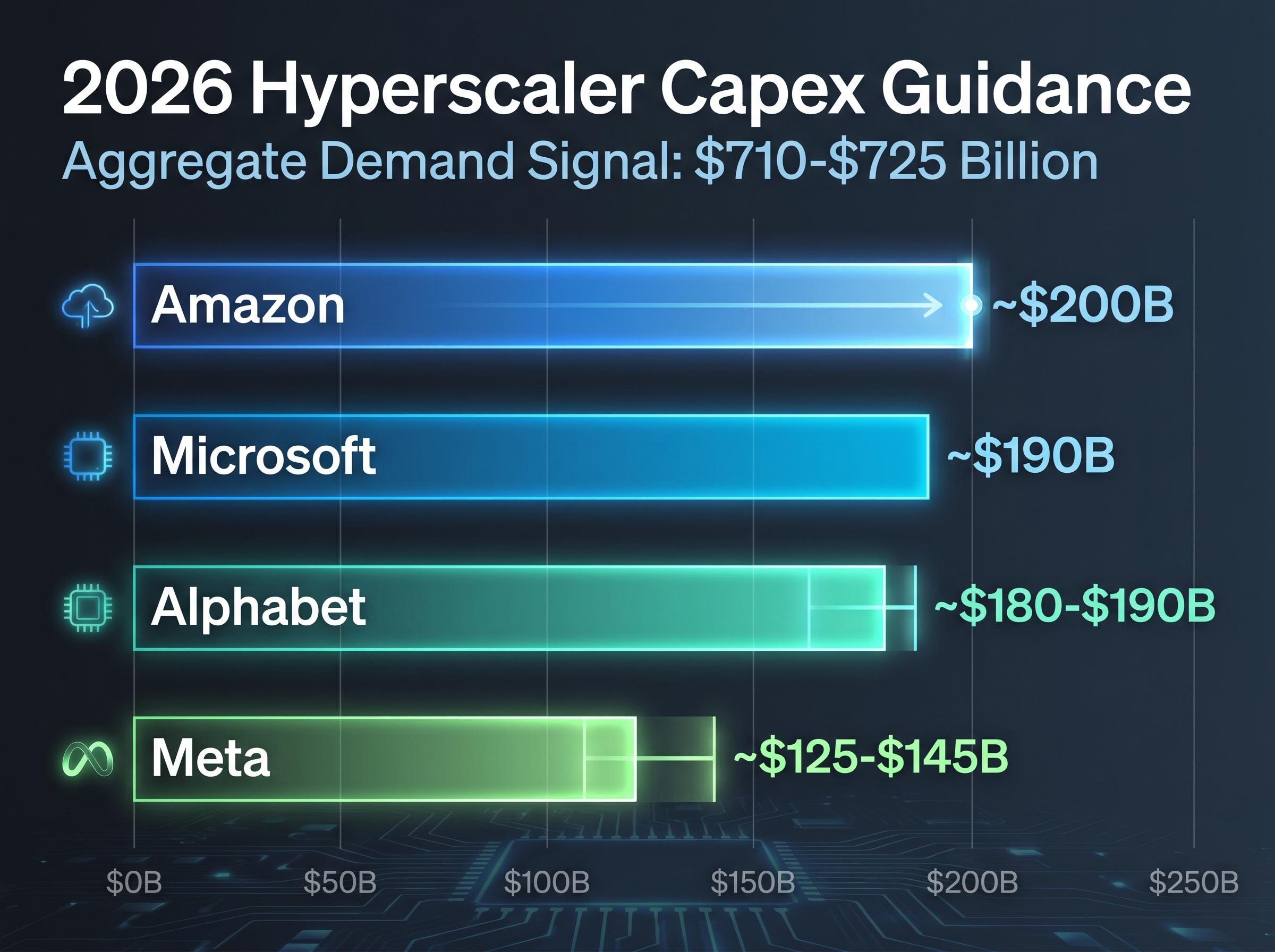

Four companies account for the vast majority of Nvidia’s data centre revenue pipeline, and each has independently committed to a 2026 capital expenditure budget that dwarfs anything seen in prior AI investment cycles.

| Hyperscaler | 2026 Capex Guidance | Signal for Nvidia |

|---|---|---|

| Amazon | ~$200B | Largest single capex commitment; broad AI infrastructure build |

| Microsoft | ~$190B | Azure GPU capacity expansion tied to enterprise AI demand |

| Alphabet | ~$180-$190B | Cloud and AI model training driving sustained GPU procurement |

| Meta | ~$125-$145B | AI research infrastructure and inference capacity buildout |

The aggregate: approximately $710-$725 billion in stated 2026 capital expenditure across four buyers. These are not aspirational projections. They are forward commitments made on public earnings calls, and they represent upward revisions from guidance issued before Q1 2026 results.

For Nvidia, this spending translates directly into order book visibility. The demand picture is distributed across four independent buyers with distinct AI strategies, which makes it structural rather than concentrated. It functions as a floor, not a ceiling, for the revenue trajectory Wall Street is modelling into 2027.

The hyperscaler capex trajectory extends well beyond 2026, with Q1 2026 alone accounting for $130 billion across the four buyers and the combined annual run rate already pointing toward a $1 trillion threshold by 2027, a figure that reframes the current demand cycle as structural rather than cyclical.

Understanding what Nvidia’s implied options move actually means for your position

The plus or minus 5.8% implied move figure circulating ahead of the May 20 print is derived from the price of an at-the-money (ATM) straddle, a combination of a call option and a put option at the same strike price, both expiring immediately after the earnings release. The combined cost of those two options reflects how much the market collectively expects the stock to move in either direction on results day.

The three things this figure communicates:

- Magnitude of expected swing: The market is pricing a roughly 5.8% move as the most likely outcome, meaning anything within that range would be considered “expected” volatility

- Options premium environment: The straddle price reflects current implied volatility levels, which indicate how expensive it is to buy protection or speculation heading into the event

- Uncertainty relative to prior quarters: Comparing the current implied move to Nvidia’s prior two earnings reactions reveals whether the market sees this print as more or less uncertain than recent results

Implied post-earnings move: approximately plus or minus 5.8% on Thursday, May 21. Sources: MarketChameleon, Barchart, and OptionsAI (live data as of May 17, 2026).

One distinction worth noting: the implied move captures expected magnitude, not direction. An ATM straddle does not predict whether the stock moves up or down. It prices the size of the swing, leaving directionality to the earnings result itself.

For investors who want a structured method for evaluating whether the current straddle cost represents fairly priced risk or an overpriced premium, our dedicated guide to earnings season options pricing walks through a 5-step framework covering implied volatility comparison, historical move benchmarking, and the mechanics of volatility crush that collapses premiums immediately after the release.

Translating the implied move into a position-sizing framework

An investor holding Nvidia shares can use the 5.8% figure as a practical calibration tool. If the implied move represents the market’s best estimate of how much the position could shift in value overnight, it provides a concrete input for evaluating whether the current position size is appropriate relative to portfolio risk tolerance.

For a leveraged position, the implied move amplifies accordingly. A 2x leveraged exposure faces an effective implied swing closer to 11.6%, which changes the risk calculus materially. Professional traders routinely use this data to reduce position size ahead of binary events or to add hedging protection through options structures.

This is not financial advice but a framework for understanding how implied volatility data informs risk management decisions.

The China wildcard: what Jensen Huang’s Beijing visit means for forward guidance

Jensen Huang’s May 13-15 trip to Beijing, travelling alongside President Trump, placed the China question at the centre of the May 20 guidance narrative. The visit included direct discussions on H20 chip availability and the export licensing pathway for Nvidia’s China-facing product line, according to media reports.

The H20 licensing mechanics create an unusual bilateral structure where the controlling barrier has shifted from Washington to Beijing: BIS moved to a case-by-case review standard in January 2026, making the US policy environment structurally more permissive, while Beijing’s customs block has prevented commercial shipments from completing, meaning US authorisation and Chinese commercial access are now decoupled.

The bull case is straightforward: favourable H20 licensing commentary or any signal that export restrictions are easing would open a revenue stream that current consensus does not fully price. China represented a meaningful portion of Nvidia’s historical data centre revenue, and restoring even partial access would add upside optionality that the Street would move to model.

The bear case carries equal weight. Any language indicating restriction escalation, or a conspicuous absence of progress on H20 availability, would remove that upside optionality and could weigh directly on forward revenue guidance. The absence of positive commentary may itself be interpreted as a negative signal.

What to listen for in the May 20 guidance call on China

Positive scenario signals to listen for:

- Specific H20 unit volume or revenue guidance for the China market

- Management language indicating improved licensing conditions or regulatory engagement

- Forward demand commentary that includes Chinese customers in the pipeline

Negative scenario signals to monitor:

- Vague or evasive language when analysts ask about China revenue contribution

- References to ongoing regulatory uncertainty without a concrete timeline

- Any mention of charges, write-downs, or inventory adjustments tied to China-facing products

China is the one dimension of the May 20 report where a single sentence in the guidance call could move the stock independently of the headline EPS number. Investors following the H20 licensing story will be better positioned to interpret management commentary in real time.

The next major ASX story will hit our subscribers first

The macro conditions that could override a strong earnings beat

Nvidia’s fundamentals do not exist in isolation. Rising long-term Treasury yields create a valuation headwind for high-multiple growth stocks by increasing the discount rate applied to future earnings, and this relationship is particularly acute for a company trading at the forward multiples Nvidia commands.

The global bond sell-off that pushed US 30-year Treasury yields above 5% for the first time since 2007 on May 15, 2026, alongside UK gilt yields hitting their highest since 1998 and Japanese JGB yields reaching an all-time record, represents the macro backdrop against which Nvidia’s May 20 result will be judged, compressing equity risk premiums across high-multiple growth names precisely at the moment of the print.

The timing compounds the risk. The FOMC minutes release is also scheduled for May 20, and the minutes are expected to reflect growing support for removing the easing bias from the Federal Reserve’s stance. This release covers Jerome Powell’s final meeting as Fed Chair, adding interpretive weight to any hawkish language.

The three macro variables with the most direct channel of impact on Nvidia’s post-earnings stock reaction:

- Rising yields: UK 10-year gilt yields rose more than 25 basis points in the prior week, with US Treasury yields moving in tandem, compressing equity risk premiums for growth names

- FOMC hawkish signal risk: If minutes indicate the Fed is hardening its posture against further easing, rate-sensitive selling pressure could dampen or override a strong beat

- Geopolitical risk-off: Middle East tensions and broader equity market indecision, visible in a doji pattern on the Nasdaq weekly chart where prices closed marginally lower and near the midpoint of the week’s range, signal that sentiment is fragile heading into the print

FOMC minutes due May 20: Expected to reflect growing support for removing the easing bias from the Fed’s forward guidance, representing Jerome Powell’s final meeting as Fed Chair. Market pricing implies approximately 35% probability of a Bank of England rate increase in mid-June and 78% probability of a Bank of Japan hike on June 16, reinforcing the global tightening backdrop.

Nvidia can report a strong beat and still underperform if macro conditions produce a risk-off reaction. The earnings result and the macro environment are two separate inputs, and both need to co-operate for the stock to reward a positive print.

Nvidia enters May 20 with the strongest demand backdrop in its history, and the most complex reaction setup

The demand thesis is clear. Hyperscaler capex of $710-$725 billion provides a structural floor beneath Nvidia’s revenue trajectory. Pre-earnings estimate revisions from Goldman Sachs, Citi, and Wells Fargo signal that Street confidence is building into the print. The full bull scenario requires a clean beat on the headline numbers, constructive China guidance, and a macro environment willing to absorb the result.

The complexity lies in the variables that sit outside Nvidia’s control. The three-to-four signals investors should watch for, in the order they will become available:

- Headline EPS and revenue versus the effective whisper number (released after market close on May 20): whether results clear the raised bar set by pre-earnings revisions

- China and H20 guidance language on the earnings call (conference call on May 20 evening): specific commentary on licensing, China revenue outlook, and H20 availability

- Forward revenue and EPS guidance versus consensus (same call): whether next-quarter and full-year guidance match or exceed the $96.78 billion Q2 revenue and $8.36 full-year EPS targets

- Thursday May 21 price action in the context of FOMC minutes and the macro tape: whether the post-earnings stock reaction holds through the first full session, or whether macro conditions dampen the move

The options market has quantified the risk: a plus or minus 5.8% expected swing, with the consensus bar already raised by recent revisions. Thursday, May 21 is the primary market verdict session. Investors who have mapped the demand backdrop, the China wildcard, and the macro overlay are positioned to interpret the result, not simply react to it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding earnings expectations, hyperscaler capital expenditure, and market reactions are subject to change based on market developments and company performance.