What the 14.4% US Corporate Profit Margin Actually Tells You

10 mins ago

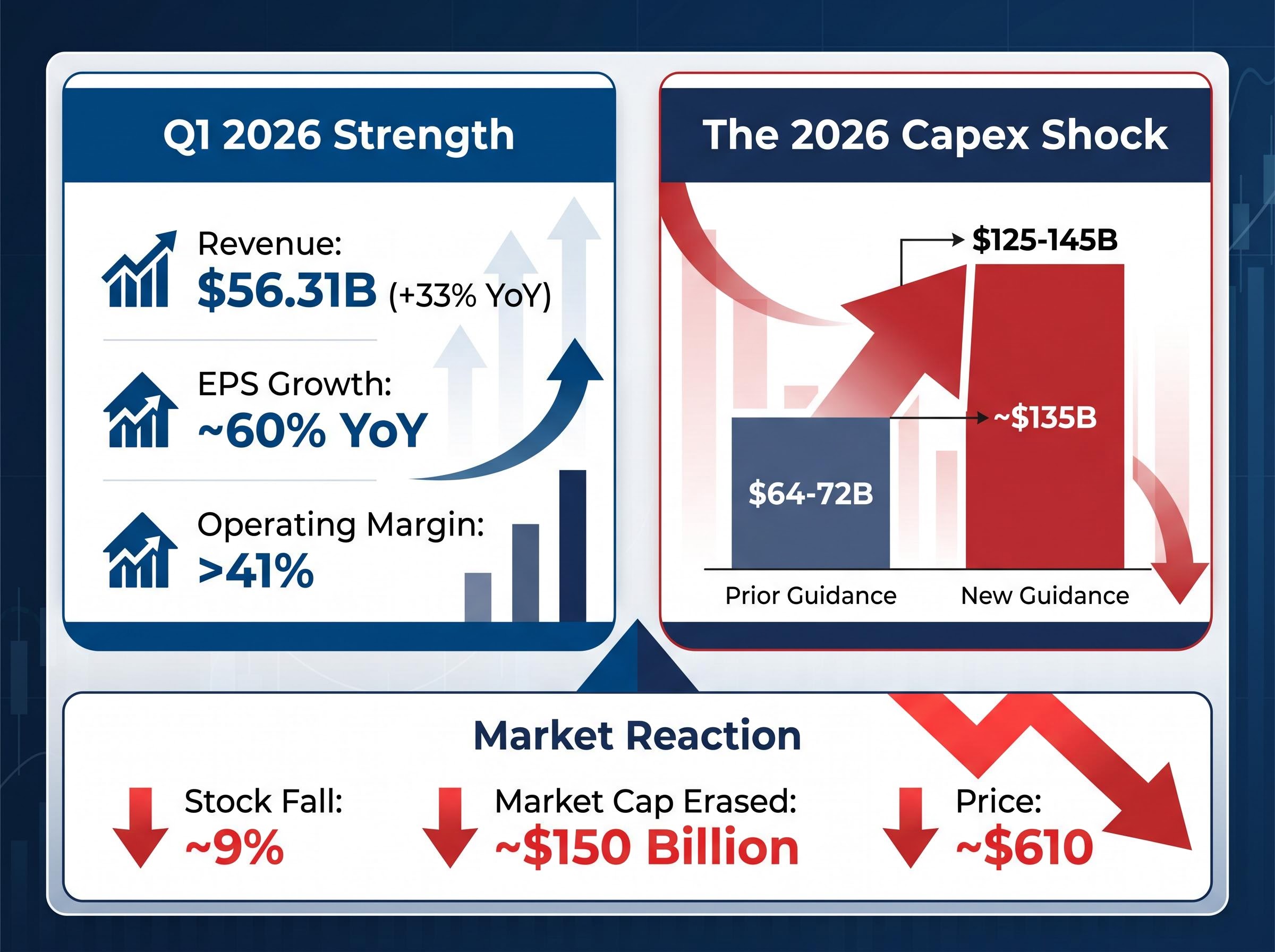

Meta Platforms reported 33% year-over-year revenue growth in Q1 2026, expanded operating margins past 40%, and still watched its stock fall roughly 9% to approximately $610, erasing around $150 billion in market capitalisation in a single session. That disconnect, a fundamentally strong business punished by the market, is precisely where stock valuation analysis becomes actionable. The question is not whether Meta is a good company. It is whether $610 compensates investors for the specific risks embedded in that number: a near-doubling of capital expenditure guidance, open-ended litigation exposure, and a Reality Labs drag that distorts every headline multiple. What follows is a scenario-based valuation framework, conservative, base, and optimistic, calibrated to the company’s actual Q1 2026 financials. Readers will leave with a replicable method for evaluating high-growth technology stocks where non-core divisions and legal risk complicate what the earnings multiple appears to say.

On paper, Q1 2026 was one of Meta’s strongest quarters in years. The headline numbers spoke clearly:

None of those figures explain a 9% single-session decline. The market was not reacting to Q1. It was reacting to what comes next.

Full-year 2026 capital expenditure guidance was raised to $125-145 billion, with a midpoint of approximately $135 billion. That represents a near-doubling from prior guidance of $64-72 billion.

Annual capex has escalated from roughly $40 billion to $72 billion and is now projected at approximately $130 billion, a spending trajectory that has no close precedent among advertising-funded technology companies.

Investors are discounting future earnings power based on the magnitude and speed of that spending escalation, not the Q1 result itself. The distinction matters. A stock that falls on good news is not necessarily mispriced. It may be correctly pricing a structural earnings headwind that the current quarter’s results do not yet reflect.

The selloff was not isolated to Meta: the broader growth stock discount reached 21% below fair value in late March 2026, a level Morningstar data shows has appeared less than 5% of the time since 2011, with technology equities accounting for approximately 42% of the category’s concentrated losses.

The figure most frequently cited in bullish cases for Meta is 16x forward earnings. That number is real, but it requires a specific definition of “earnings” to produce.

The 16x applies to Meta’s family-of-apps (FOA) segment in isolation, meaning it excludes Reality Labs entirely and assigns zero value to AI infrastructure investments. FOA is priced at approximately 16x FY2027 estimated earnings per share of roughly $45. On that basis, the stock trades at parity with or at a slight discount to Alphabet’s Search and YouTube business at approximately 16-16.5x forward price-to-earnings.

The comparison is instructive, but structurally imperfect. Alphabet and Amazon direct substantial capex toward cloud infrastructure that generates revenue from paying third-party customers. Meta’s capex is internally directed, funding AI models and hardware that must prove their value through Meta’s own ad products. That difference means a dollar of Meta capex carries more execution risk than a dollar of Amazon Web Services capex, and peer multiple comparisons must account for it.

The hyperscaler capex trajectory across Microsoft, Alphabet, Amazon, and Meta now exceeds $610 billion collectively for 2026, nearly double 2024 levels, and investor focus has shifted decisively from the scale of infrastructure deployment toward proof of commercial software monetisation and measurable return on investment.

| Company | Segment Basis | Forward P/E | EV/EBITDA | Operating Margin |

|---|---|---|---|---|

| Meta (FOA only) | Family of Apps | ~16x | ~14x | ~41% |

| Alphabet | Search / YouTube | ~16-16.5x | ~13x | Varies by segment |

| Amazon | AWS / Ads blend | ~18x | ~15x | Varies by segment |

| Snap | Consolidated | ~8x | N/A | Growth-constrained |

| Consolidated | ~12x | N/A | Below peer average |

Any honest valuation of Meta requires a sum-of-parts approach: FOA earnings power, Reality Labs as a net present value drag, and AI infrastructure as either a call option or a capex burden depending on the scenario assumed.

Reality Labs has been a consistent cash consumer with no near-term profitability path disclosed. Its losses suppress consolidated earnings, which makes the consolidated price-to-earnings ratio higher than the FOA-only figure. JPMorgan’s sum-of-parts model treats Reality Labs as a net present value drag, not a zero, which is a more conservative and arguably more honest treatment than simply excluding the division and pretending it does not exist.

The earnings multiple, in other words, is a function of the denominator an analyst chooses to use. Investors who apply a single headline P/E without separating the segments are comparing incommensurable things.

Scenario modelling makes the investment decision explicit. Each case below rests on a specific set of assumptions; the value of the exercise is clarifying which assumptions the investor accepts.

| Scenario | Revenue Growth | Terminal Multiple | Margin Assumption | Implied 5-Year Return |

|---|---|---|---|---|

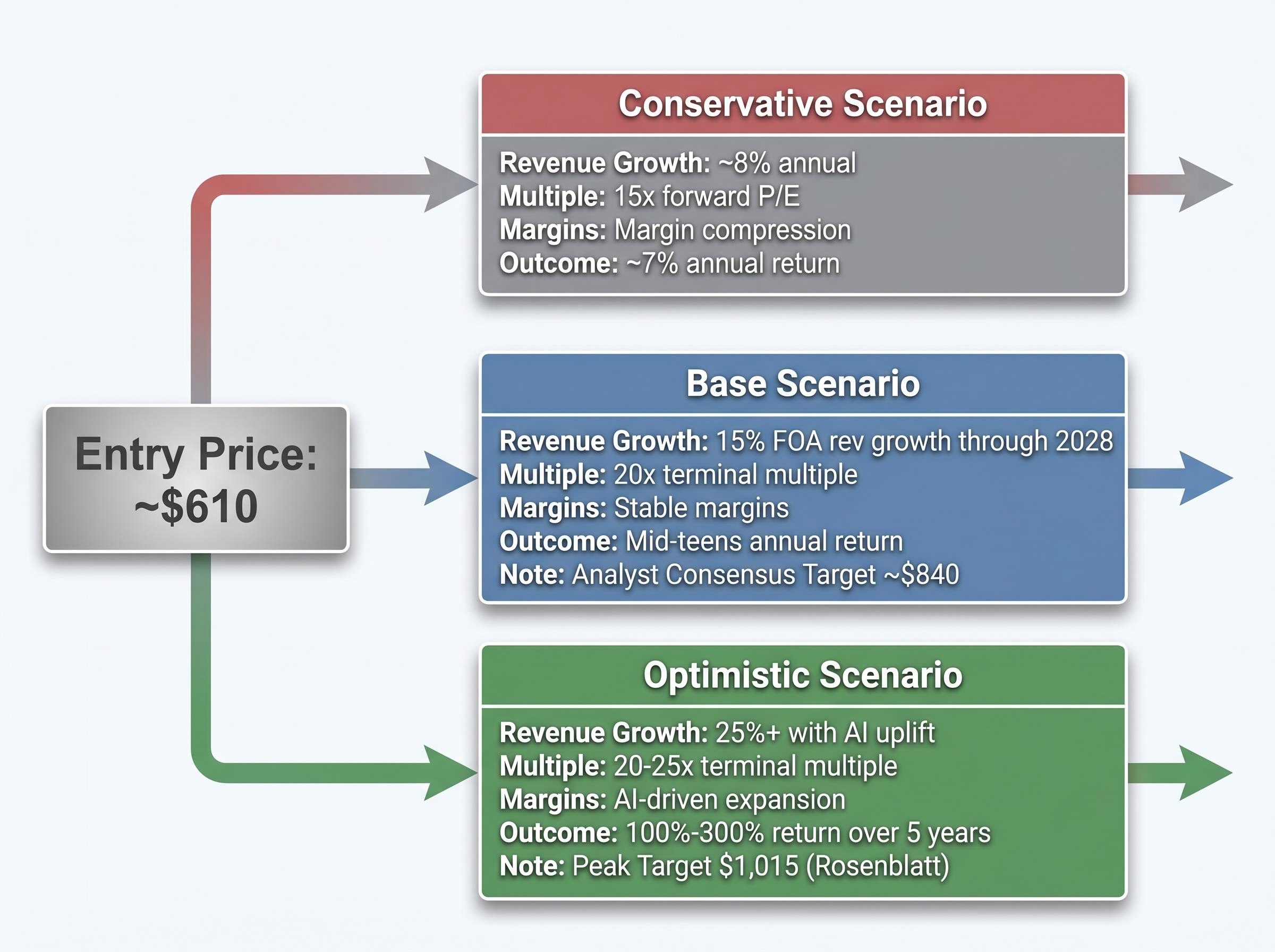

| Conservative | ~8% annual | 15x forward earnings | Margin compression | ~7% annual |

| Base | Mid-to-high teens | 20x | Stable margins | Mid-teens annual |

| Optimistic | 25%+ with AI uplift | 20-25x | AI-driven expansion | 100%-300% over 5 years |

The conservative case anchors to the 2022 precedent, when FOA revenue declined approximately 1%, and applies a 15x terminal multiple with margin compression. It produces an estimated 7% annual return, roughly equivalent to a broad market index with concentrated single-stock risk.

Morgan Stanley’s Brian Nowak models a base case of 15% FOA revenue compound annual growth through 2028, with AI monetisation contributing 5% of revenue by 2029. That trajectory supports a 20x multiple and mid-teens annual returns from the $610 entry point.

The optimistic case requires the most: 25%+ revenue growth sustained by AI-driven margin expansion, a multiple re-rating to 20-25x, and total returns of 100%-300% over five years. Rosenblatt’s Barton Crockett, who carries the highest major analyst target at $1,015, anchors the ceiling.

The $1,015 target, the highest among major sell-side firms, assumes “superintelligence labs yield material revenue uplift by 2028,” a specific and falsifiable claim that separates this scenario from generic optimism.

The analyst consensus target sits at approximately $840, with a range from $725 to $1,015. Investors who cannot articulate which scenario they are underwriting, and which assumptions must resolve favourably, are buying a narrative rather than a position.

Investors applying AI stock valuation frameworks beyond the earnings multiple, including the Shiller CAPE ratio at 40.11 and Minsky’s financing stage model, find that hyperscalers have moved from hedge financing into speculative financing, with more than $75 billion in bonds issued since September 2025 and annual borrowing projected at approximately $140 billion.

Meta faces aggregate litigation exposure estimated between $8 billion and $60 billion, stemming primarily from youth mental health claims tied to Instagram and Facebook. A range that wide sounds unmodelable. It is not, provided it is converted into per-share terms.

JPMorgan applies a 5-10% haircut to its discounted cash flow model for litigation risk. At the $610 price level, that translates to approximately $30-$61 per share, a tractable discount range that can be incorporated into any scenario framework.

Key active proceedings include:

Harvard’s algorithmic harm judicial primer, published in February 2026, establishes a formal framework for how courts assess foreseeable risk in platform design cases, which is directly relevant to the MDL proceedings centred on Instagram’s algorithmic content delivery.

Some analysts have drawn comparisons to tobacco litigation, citing addictive design and disclosure disputes. The comparison carries weight on the liability theory but breaks down structurally: Meta’s revenue model is not physically addictive in the same way, and algorithmic changes could resolve certain claims without financial settlement. The analogy is informative, not predictive.

Meta’s Q1 2026 10-Q (filed 1 May 2026) reflects general accrued liabilities of $13.326 billion. An $8.03 billion tax benefit in the quarter provides a partial financial offset against litigation-related reserves.

KOSA, if enacted, could require algorithmic changes that reduce engagement-driven revenue, representing a structural rather than one-time financial risk. This legislative dimension is harder to price than direct settlement exposure and represents a tail risk rather than a base case. Investors should monitor Senate progress on S.1748 alongside the MDL trial timeline as the two most material near-term legal catalysts.

Institutional positioning is a signal about market structure, not a substitute for valuation work. The skill lies in weighting different types of institutional action by what each one actually reveals.

Key institutional positions as of recent filings:

Ackman has publicly characterised Meta as “very inexpensive” and “irrationally cheap” at recent lows, a statement that carries weight primarily because of the concentration it accompanies: 10% of a fund in a single name is a conviction signal that passive accumulation is not.

On the other side, JPMorgan’s Doug Anmuth downgraded Meta to Neutral on 30 April 2026, specifically citing the massive AI spending forecast as sufficient cause to move off Overweight. Short interest at approximately 2.1% of float remains low, indicating limited conviction among active short sellers.

Each of these positions carries a different informational weight for investors evaluating the stock:

The 92% buy or strong buy analyst consensus and the approximately $840 consensus price target provide context, but consensus has been wrong before, in both directions.

The analysis above points to a single, definable investment proposition. Owning Meta at $610 is a bet that AI infrastructure generates measurable revenue by 2028-2029, not simply a bet on a well-run advertising company.

Owning Meta at $610 is a bet that AI infrastructure generates measurable revenue by 2028-2029. Investors who believe the capex programme is a bridge to nowhere should not own the stock at any multiple derived from AI-enhanced earnings estimates.

Approximately 65% of analysts expect measurable revenue returns from the $125-145 billion capex programme by 2028-2029. JPMorgan and Goldman Sachs model AI capex-to-revenue ratios peaking at approximately 25% in 2027 before declining. The two data points to monitor going forward are that ratio’s trajectory and litigation developments in the MDL, where a Q4 2026 trial could materially reprice legal risk.

The sector-wide capex reaction was consistent across the earnings season: all five major US tech companies beat Q1 2026 estimates, yet only Alphabet and Apple delivered immediate stock gains, as combined 2026 AI infrastructure commitments of $650-725 billion across the four major hyperscalers became the dominant variable in how the market priced each name irrespective of reported earnings quality.

The replicable framework developed across this analysis applies to any high-growth technology holding where non-core divisions and legal exposure complicate the headline multiple:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A sum-of-parts valuation assigns separate values to each business division, such as Meta's Family of Apps and Reality Labs, rather than applying a single multiple to consolidated earnings. It matters for Meta because Reality Labs generates consistent losses that inflate the headline price-to-earnings ratio and obscure the true earnings power of the core advertising business.

The market reacted to Meta's full-year 2026 capital expenditure guidance being raised to $125-145 billion, nearly double prior guidance, rather than the Q1 results themselves. Investors are pricing in the risk that this unprecedented spending level will compress future earnings before AI infrastructure generates measurable revenue returns.

Meta faces aggregate litigation exposure estimated between $8 billion and $60 billion, primarily from youth mental health claims tied to Instagram and Facebook. JPMorgan applies a 5-10% haircut to its discounted cash flow model for this risk, which translates to approximately $30-$61 per share at the $610 price level.

The conservative scenario assumes roughly 8% annual revenue growth and a 15x terminal multiple, producing an estimated 7% annual return. The base case targets mid-to-high teens growth with a 20x multiple for mid-teens annual returns, while the optimistic case requires 25% or more growth with AI-driven margin expansion and projects total returns of 100%-300% over five years.

Approximately 92% of analysts carry a buy or strong buy rating on Meta, with a consensus price target of around $840 and a range spanning from $725 to $1,015. The highest major sell-side target of $1,015, from Rosenblatt's Barton Crockett, assumes superintelligence labs generate material revenue by 2028.