Meta Stock: Why Morgan Stanley Ignores the Cloud Hype at $775

2 hrs ago

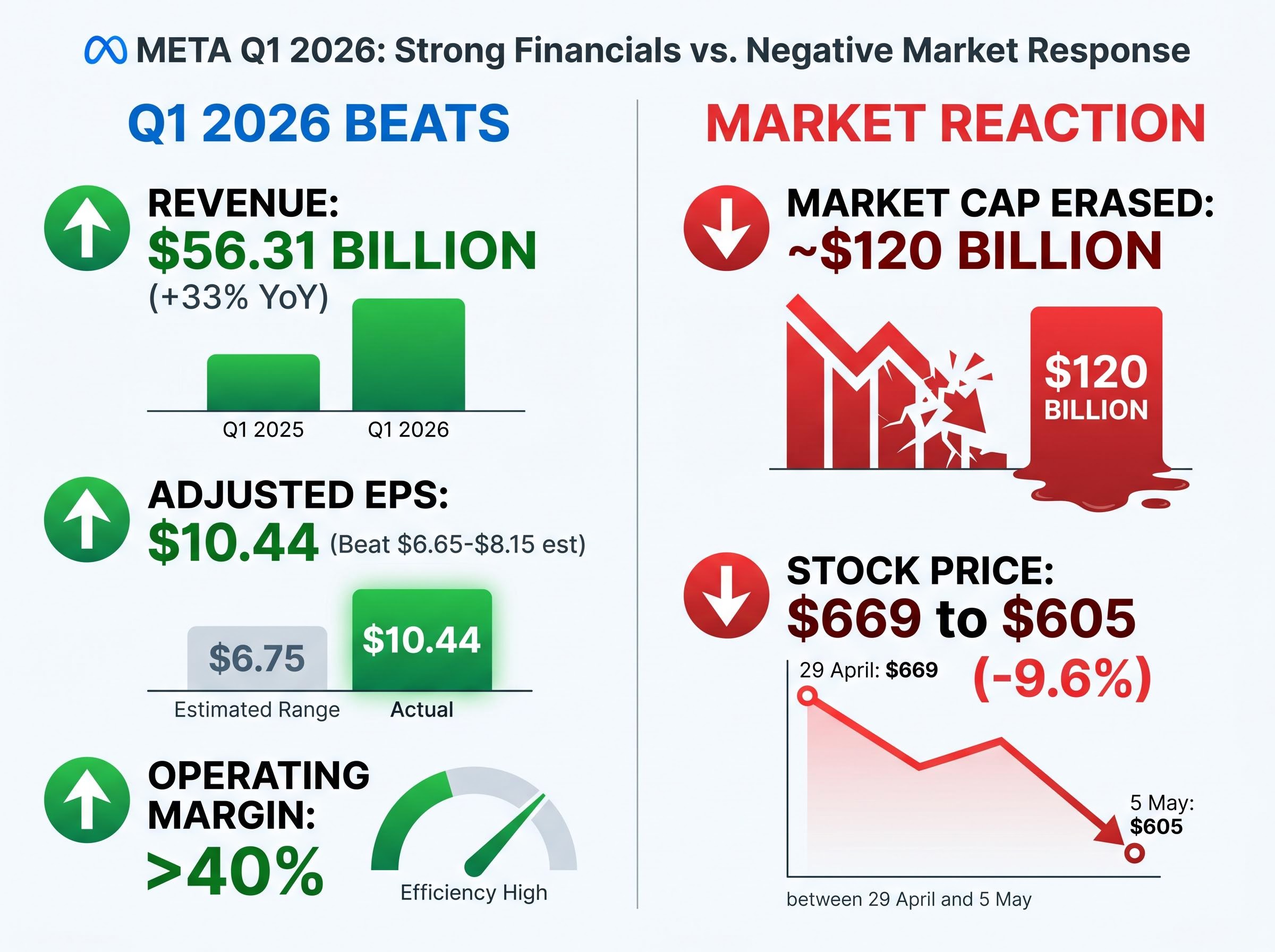

Meta Platforms reported 33% revenue growth, 60% EPS expansion, and record user engagement across its family of apps in Q1 2026. The market responded by erasing approximately $120 billion in market capitalisation overnight. Between the 29 April after-hours earnings release and the 5 May close, META shares fell from roughly $669 to approximately $605, a decline of 9.6% with no recovery established. The disconnect between one of the strongest quarterly performances in mega-cap tech and one of the sharpest post-earnings selloffs of the year is not a glitch in market logic. It is the logic working exactly as designed. What follows is an unpacking of why the market sold a strong quarter, what the capex escalation signals about Meta’s strategic bet on artificial intelligence, and how the bull and bear cases stand as of this week.

The headline numbers from Q1 2026 were not ambiguous. Every major line moved in the right direction simultaneously.

The EPS beat alone tells the story of how strong this quarter was. Actual earnings of $10.44 against estimates as low as $6.65 represent the kind of upside surprise that, under normal circumstances, sends a stock sharply higher rather than lower.

Facebook and Instagram individually reached all-time engagement highs. A sequential dip in user figures was attributed to geopolitical internet disruptions in Iran and Russia rather than organic churn. The beat was broad-based: ad revenue, user engagement, and operating margins all moved together. This was not a single-line fluke.

Understanding the strength of the quarter is the necessary starting point. Without it, the selloff looks like a reaction to weak results. It was not.

The numbers that moved the stock were not in the Q1 results. They were in the forward guidance.

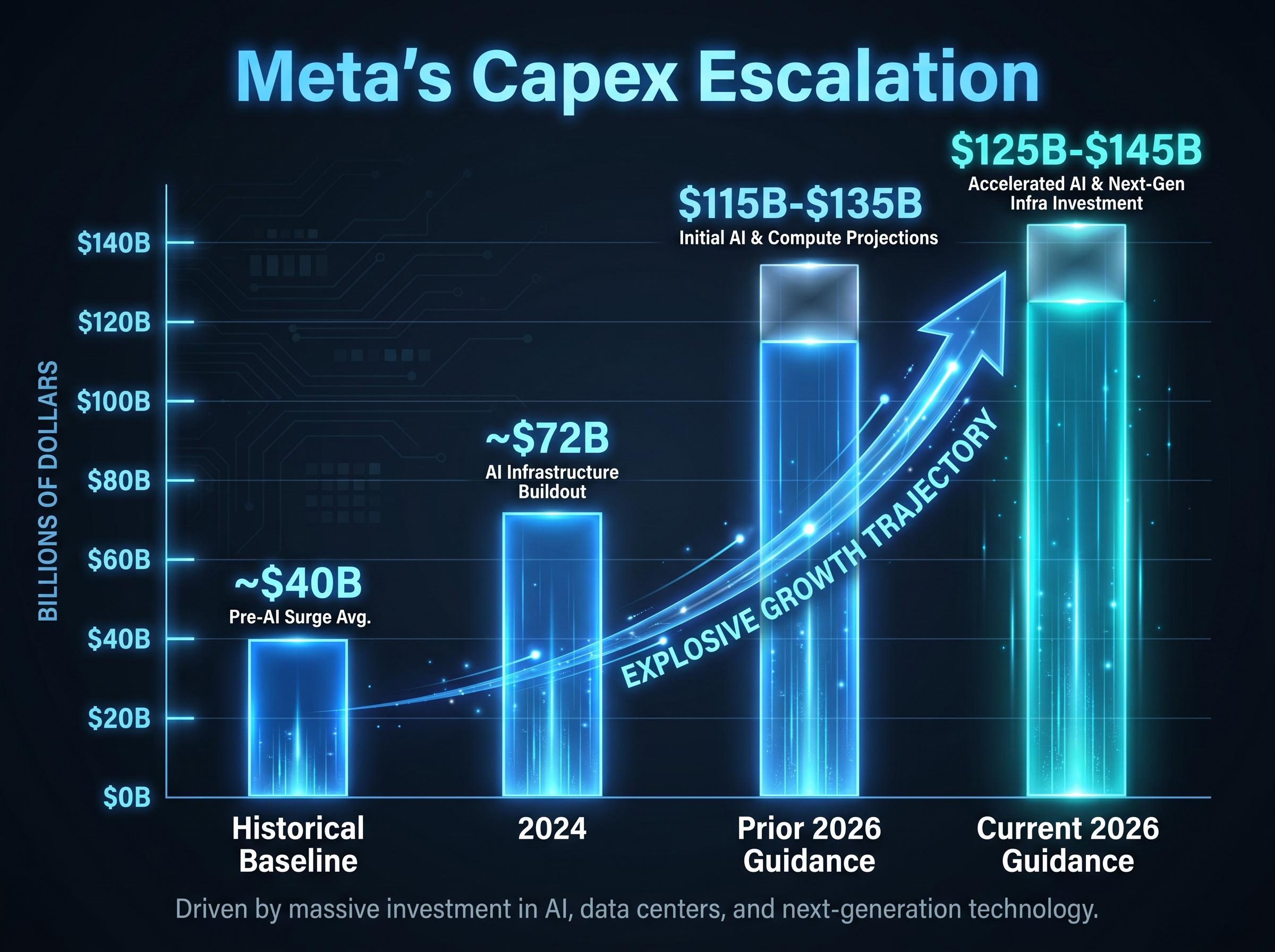

Meta raised its full-year 2026 capital expenditure guidance to $125-$145 billion, up from prior guidance of $115-$135 billion. Q1 alone accounted for $19.8 billion in capex. To grasp the scale of the escalation, the trajectory over recent years tells the story more clearly than any single figure.

| Period | Approximate Capex | Key Driver |

|---|---|---|

| Historical baseline | ~$40B annually | Data centre and network infrastructure |

| 2024 | ~$72B | Initial AI infrastructure scale-up |

| Prior 2026 guidance | $115-$135B | Expanded AI compute and training capacity |

| Current 2026 guidance | $125-$145B | Revised compute requirements; MTIA chip deployment |

In Q1 alone, contractual infrastructure commitments rose by $17 billion, and total incremental spending commitments over the following one to two years reached approximately $107 billion. Meta also carries a $50 billion debt load on its balance sheet, and stock buybacks appeared paused during the quarter.

Meta’s revised guidance does not exist in isolation: hyperscaler capex commitments across Amazon, Microsoft, Alphabet, and Meta reached $130 billion in Q1 2026 alone, with combined full-year 2026 projections approaching $725 billion, a scale that is reshaping both semiconductor supply chains and the debt markets funding the build.

The figure that spooked investors most was not a number. It was a disclosure.

Meta’s CFO acknowledged on the earnings call that the company had materially underestimated its compute requirements. For a company already guiding to $130 billion at the midpoint, the admission that even this figure might prove insufficient removed the ceiling investors were trying to price. If the current guidance already reflects an undercount, future revisions could push the figure higher still.

The shift to multi-year cloud and infrastructure commitments represents a structural change in how Meta finances its AI build. These are not single-quarter expenses that can be dialled back. They are contractual obligations extending years into the future.

The capex figure only makes sense in the context of what it is purchasing. Meta’s AI investment is not speculative research; it is already generating measurable returns across several product lines.

The distribution advantage is worth isolating. Meta’s AI products deploy to a user base exceeding 3 billion people, a scale that no standalone AI company can replicate. Every improvement in ad targeting, content recommendation, or creative tooling compounds across that base immediately.

Mark Zuckerberg framed AI on the earnings call as enabling a computing paradigm that extends beyond smartphones, positioning Meta to capture value across consumer interactions, commerce, and content creation at a scale the company has not previously attempted.

On the hardware side, Meta’s in-house MTIA chip strategy (developed in partnership with Broadcom) is designed to lower per-unit compute costs structurally compared to purchasing Nvidia GPUs or consuming AWS and Google Cloud capacity. Whether it delivers on that promise will determine a significant portion of the long-term return on the capex programme.

The Meta selloff offers a clean example of a pricing mechanism that confuses investors across every earnings season: stock prices reflect discounted expectations of future cash flows, not backward-looking earnings beats. A company can simultaneously report strong results and fall if the market’s estimate of future earnings deteriorates.

The broader tech earnings pattern in Q1 2026 confirms that Meta’s experience was not idiosyncratic: all five major US tech companies beat estimates, yet only Alphabet and Apple saw immediate post-earnings stock gains, as investor attention across the sector pivoted from reported results to the forward trajectory of combined AI infrastructure commitments now estimated at $650-$725 billion.

The mechanism works in three steps:

The specific dynamics in Meta’s case reinforced the pattern. The Q1 EPS beat included a one-time tax benefit. Analysts trimmed FY2026 EPS estimates from approximately $42.10 to $41.25, partly reflecting the normalisation of that benefit and partly reflecting higher projected cost growth of approximately 35%.

| Metric | Pre-Earnings Estimate | Post-Earnings Estimate | Direction |

|---|---|---|---|

| FY2026 Revenue | $225.4B | $227.8B | +1.1% |

| FY2026 EPS | $42.10 | $41.25 | -2.0% |

Revenue estimates rose 1.1% on the Q1 beat. EPS estimates fell 2.0% on the capex and cost outlook. That divergence, revenue up but earnings down, is the market’s way of saying: the top line is growing, but more of it will be consumed before it reaches the bottom line. Meta’s official Q2 guidance of $58-$61 billion sits comfortably above the consensus estimate of approximately $58.2 billion, and approximately 47 analysts maintain a Moderate Buy consensus with an average price target around $834-$839. The market is not bearish on Meta’s revenue trajectory. It is repricing the cost of funding the AI infrastructure that sustains it.

The debate over Meta’s capex programme has crystallised around a single question: is this Amazon Web Services in its early chapters, or is this the metaverse build all over again? Sophisticated investors hold structurally coherent positions on both sides.

Investor perspective: Bill Ackman has publicly described Meta as “very inexpensive,” with approximately 10% of his fund’s capital allocated to the position, a significant concentration bet on the AI infrastructure thesis playing out.

The split is genuine. Approximately 47 analysts covering Meta lean Moderate Buy, with an average target of $834-$839, but the range of outcomes embedded in that consensus is unusually wide for a company of this size.

The Meta earnings reaction is a case study in a tension that will define how investors assess every major AI infrastructure spender through the remainder of 2026: the gap between backward-looking earnings strength and forward-looking capital commitment uncertainty.

At approximately $605 per share as of 5 May, the Family of Apps segment trades at roughly 16x earnings when Reality Labs is excluded from the valuation. Under a base scenario of mid-to-high teens revenue growth with a 20-25x forward multiple, five-year return projections range from approximately 100-300%. Under more conservative assumptions (8% revenue growth, 15x multiple with margin compression), annualised returns fall closer to 7%.

The width of that outcome distribution, from 7% annualised under conservative assumptions to 100-300% cumulative under a base-to-optimistic case, captures the genuine uncertainty the market is pricing. At $605, investors are not paying for certainty in either direction.

For any company making large-scale AI infrastructure commitments, three questions determine whether the capex is investment or overhead:

Meta answers the second question favourably and the first unfavourably. The third remains open. Whether the $130 billion midpoint capex figure is the foundation of a generational competitive advantage or a repeat of the metaverse-era overbuild depends on AI monetisation timelines that no analyst can predict with confidence today.

Investors who want to stress-test the Meta valuation against broader market cycle analysis will find our full explainer on AI stock bubble frameworks, which applies the Shiller CAPE ratio (currently at 40.11), Minsky’s financing stages, and three additional analytical tools to the question of whether current AI infrastructure valuations reflect genuine revenue generation or speculative excess.

The selloff was not irrational. It reflected a rational forward-looking repricing of free cash flow expectations in response to a capex guidance shift that materially changes the earnings trajectory. Two paths remain viable. If AI monetisation delivers at the scale Meta is building for, the current capex programme will look like the early chapters of one of the great infrastructure investment stories. If timelines slip or returns disappoint, the metaverse parallel becomes the more relevant frame.

The Q2 2026 earnings call will be the first opportunity for management to demonstrate whether the CFO’s compute underestimation was a one-time recalibration or the beginning of a pattern of upward revisions. That distinction will matter more than any single quarter’s beat.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Meta stock fell roughly 9.6% despite strong Q1 results because the company raised its full-year 2026 capital expenditure guidance to $125-$145 billion, which led analysts to cut FY2026 EPS estimates as more cash flow would be absorbed by infrastructure spending before reaching shareholders.

Meta reported Q1 2026 revenue of $56.31 billion (up 33% year on year), adjusted EPS of $10.44 well above estimates, operating margin above 40%, and daily active people of approximately 3.3 billion across its Family of Apps.

Meta is deploying its $125-$145 billion capex budget primarily on AI infrastructure, including data centres, compute capacity, and its in-house MTIA chip programme developed with Broadcom, all designed to support AI-driven advertising tools, content recommendations, and the Meta AI platform.

Meta's current 2026 guidance of $125-$145 billion compares to an approximate historical baseline of $40 billion annually and roughly $72 billion in 2024, representing a dramatic multi-year escalation driven by AI infrastructure requirements.

The bull case holds that Meta's profitable ad business funds the AI build organically and the infrastructure mirrors Amazon's early AWS investment cycle, while the bear case argues Meta lacks an external cloud revenue signal to validate the spend and the pattern resembles its own 2021-2022 metaverse overbuild.