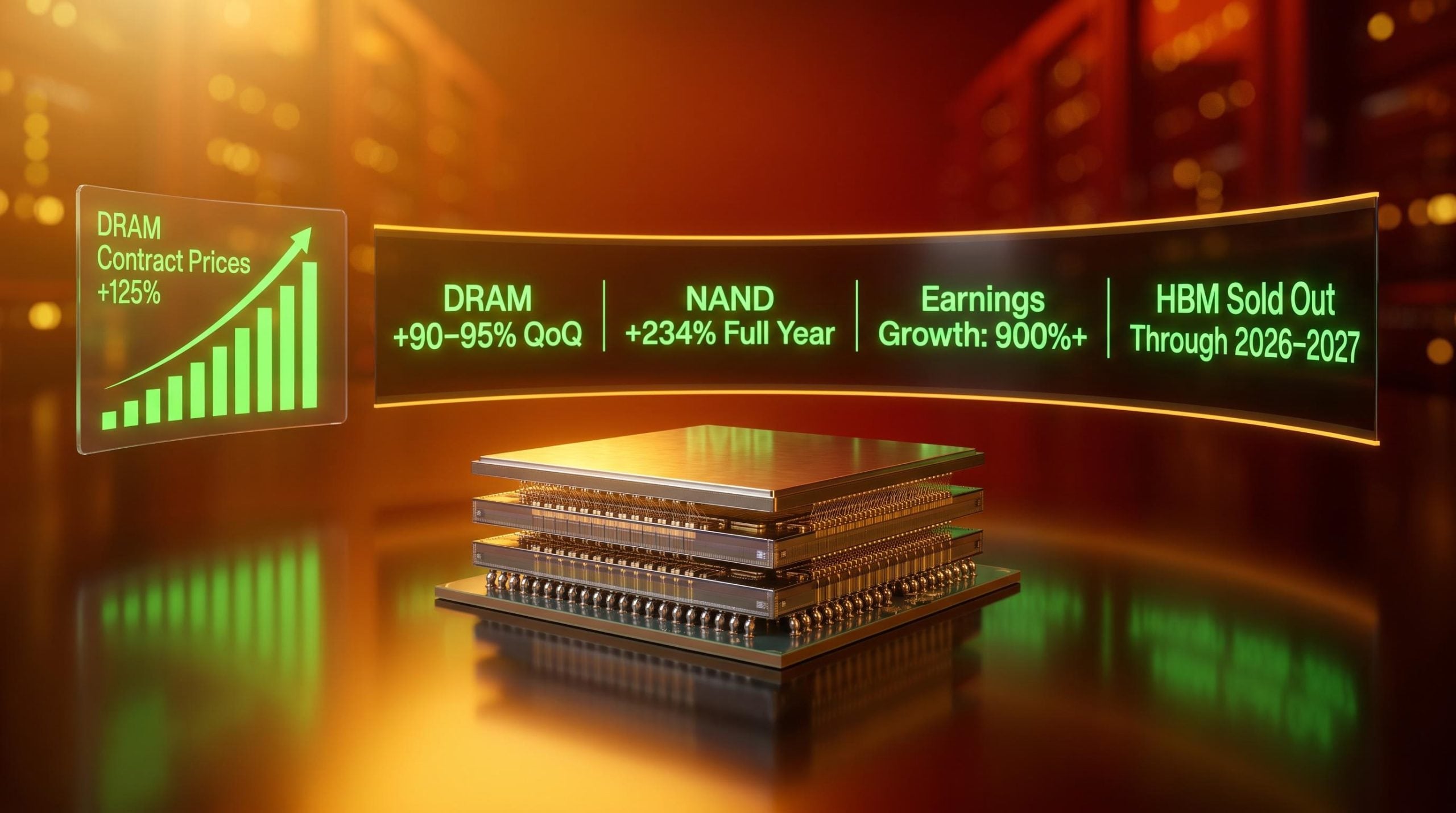

Memory chip earnings just delivered one of the most extreme year-over-year growth figures in semiconductor history: more than 900% in a single quarter. The number is not a company-specific windfall. It is the direct output of a global shortage that is reshaping the entire technology supply chain.

The shortage is not a temporary inventory blip. It is the product of years of constrained capital expenditure colliding with AI data centre demand that is both enormous and largely indifferent to price. The companies that make DRAM, NAND flash, and high-bandwidth memory (HBM) are experiencing pricing power they have rarely held before. The buyers who cannot secure supply are facing a strategic disadvantage they cannot afford to ignore.

Here is what triggered this moment, why supply cannot simply expand to meet demand, and what the shift to multi-year deposit-backed contracts means for every part of the technology ecosystem, from hyperscalers to device makers to equipment suppliers.

How memory chip prices reached their most extreme levels in a generation

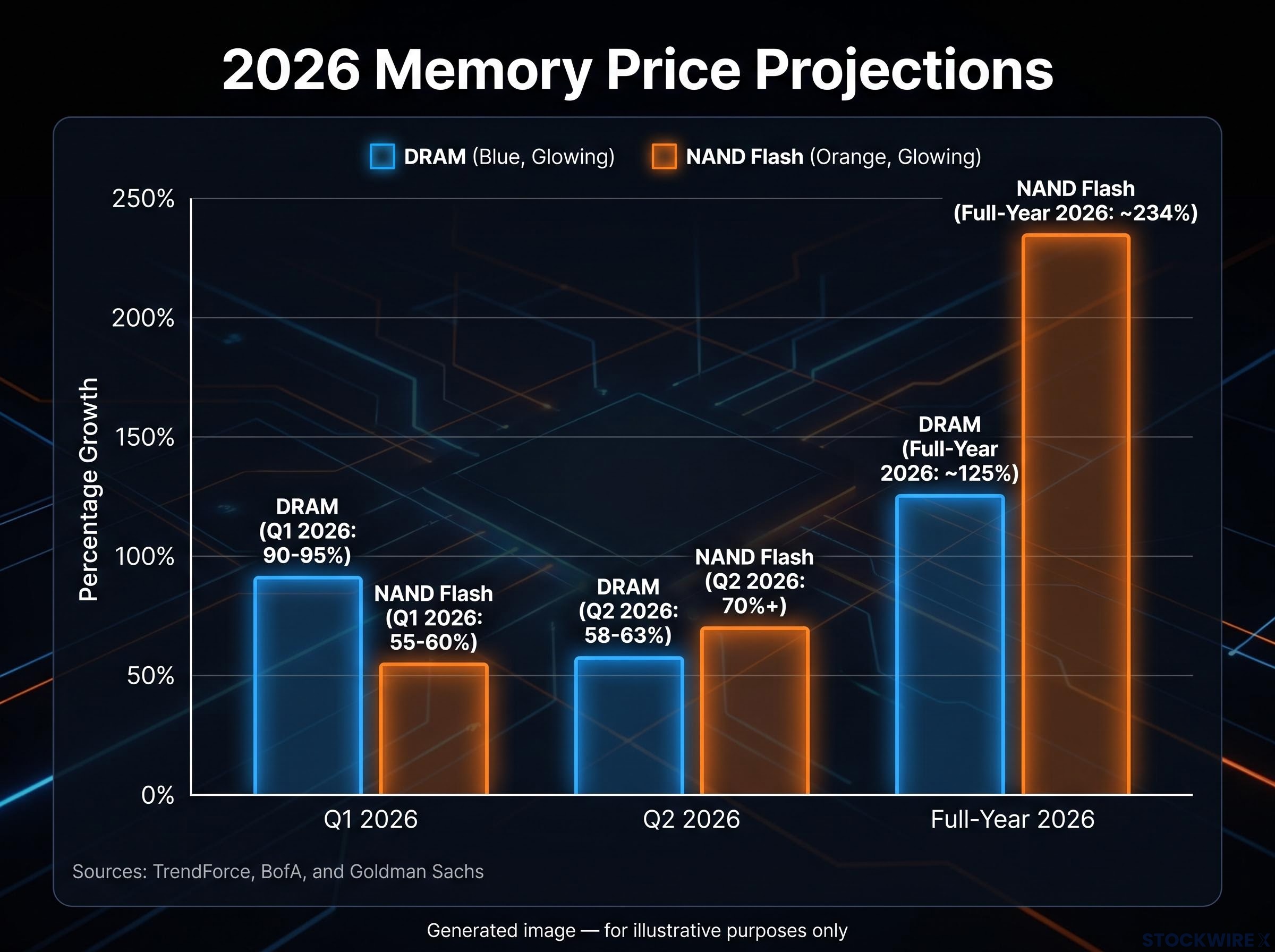

The price movements came in contract markets, not spot markets, and they came fast. DRAM contract prices surged 90-95% quarter-over-quarter in Q1 2026, then climbed a further 58-63% in Q2 2026. NAND flash followed a similar trajectory: up 55-60% in Q1, with subsequent quarterly gains exceeding 70% in some forecasts.

For the full year, projections from TrendForce, BofA, and Goldman Sachs point to DRAM prices rising approximately 125% and NAND prices rising approximately 234%.

| Memory Category | Q1 2026 QoQ Change | Q2 2026 QoQ Change | Full-Year 2026 Projection |

|---|---|---|---|

| DRAM | 90-95% | 58-63% | ~125% |

| NAND Flash | 55-60% | 70%+ (forecast) | ~234% |

These are negotiated contract prices, which means buyers sat across from suppliers, accepted these terms, and signed. That distinction matters. Spot prices can spike on sentiment. Contract prices of this magnitude tell you the shortage is structural and that procurement teams at some of the world’s largest technology companies concluded they had no alternative.

HBM capacity has been sold out at major producers through 2026-2027. There is no incremental supply available to absorb new demand in the highest-value memory category.

When big ASX news breaks, our subscribers know first

What a 900% earnings surge actually signals about the memory market’s structure

In Q1 2026, memory companies recorded year-on-year earnings growth of more than 900%, a figure highlighted by Phillip Securities Research. Over the same period, share prices across the memory segment rose by roughly 95%.

The headline figure is striking, but what it reveals about the industry’s structure matters more than the number itself. The three companies that dominate global memory production all reported results of this magnitude at the same time:

- Samsung: The world’s largest memory producer by revenue, manufacturing DRAM, NAND, and HBM

- SK hynix: The dominant supplier of HBM for AI accelerators, with the most advanced stacked-die production

- Micron: The sole major US-headquartered memory producer, a significant DRAM and NAND supplier

When three companies in the same commodity-adjacent market all deliver earnings growth of this scale simultaneously, it signals industry-wide pricing power rather than individual operational excellence. That distinction is what determines how long these conditions can persist. A single company outperformance can be competed away. An industry-wide pricing regime supported by structural supply constraints is a different proposition entirely.

Memory chip stocks reflected this structural repricing rapidly, with Micron, Sandisk, and SK Hynix posting combined gains exceeding 250% over 30 days as sold-out HBM capacity, a threatened Samsung labour strike, and US-China trade policy shifts converged to move markets.

Why fabs cannot simply build their way out of the shortage

Supply relief is not arriving soon, and the reasons compound on each other.

- Capital lead times are measured in years, not quarters. A memory fabrication plant, or fab, is among the most capital-intensive factories in the world. The sequence from investment decision to volume production, which includes installing tools, qualifying processes, and achieving viable yields, typically runs 18-24 months at minimum. Capacity decisions made in 2025-2026 are unlikely to deliver meaningful output before late 2027.

- The 2022-2023 glut embedded caution into the industry’s investment posture. A severe oversupply around 2022-2023 crashed memory prices and punished producers that had overbuilt. That experience left Samsung, SK hynix, and Micron structurally reluctant to add aggressive new capacity in the current cycle, even as prices signal extreme tightness.

- AI products are crowding out everything else. Existing fab capacity is heavily weighted toward high-margin AI-oriented products, particularly HBM and data-centre DRAM. Every wafer allocated to HBM is a wafer not producing memory for PCs, smartphones, or consumer devices. The same cleanroom space serves both markets, and AI is winning the allocation decision.

18-24 months: The minimum ramp timeline from investment decision to volume production for a new memory fab, according to industry analysis from TrendForce and manufacturer commentary.

For any company or buyer planning memory procurement over the next 12-18 months, this timeline means the shortage is not a condition to wait out. It is a reality to plan around.

What HBM is and why it sits at the centre of the shortage

HBM, or high-bandwidth memory, is the single memory category generating the most intense demand pressure. If you have encountered the term in coverage of AI infrastructure, here is what it actually is and why it matters differently from standard memory.

HBM differs from conventional DRAM in three ways:

- Architecture: HBM uses a stacked-die design, where multiple memory chips are layered vertically and connected through microscopic pathways called through-silicon vias, rather than placed side by side on a circuit board

- Bandwidth: The stacked architecture and very wide memory interface deliver dramatically higher data throughput than standard DRAM, which is what AI workloads require

- Primary use case: HBM is purpose-built for AI accelerators such as NVIDIA GPUs and Google TPUs, where the speed at which data moves between the processor and memory determines how fast models can train and run

The architectural complexity adds meaningfully to production qualification and ramp lead times. Stacking dies and bonding them reliably at scale is harder than producing flat DRAM modules. That is why HBM capacity cannot be expanded as quickly as standard memory, even when producers want to.

AI demand for HBM is price-inelastic. Hyperscalers and AI chip designers treat it as strategic infrastructure, not a component they will trade down from when prices rise. That combination of architectural complexity and buyer willingness to pay at nearly any price makes HBM the sharpest pressure point in the entire shortage.

The HBM pricing cascade through the supply chain amplifies at each stage: Bernstein projects a 2-2.5x HBM contract price increase for 2027, and because GPU vendors apply margin preservation on input costs, that increase reaches hyperscalers at roughly four times the original memory price movement.

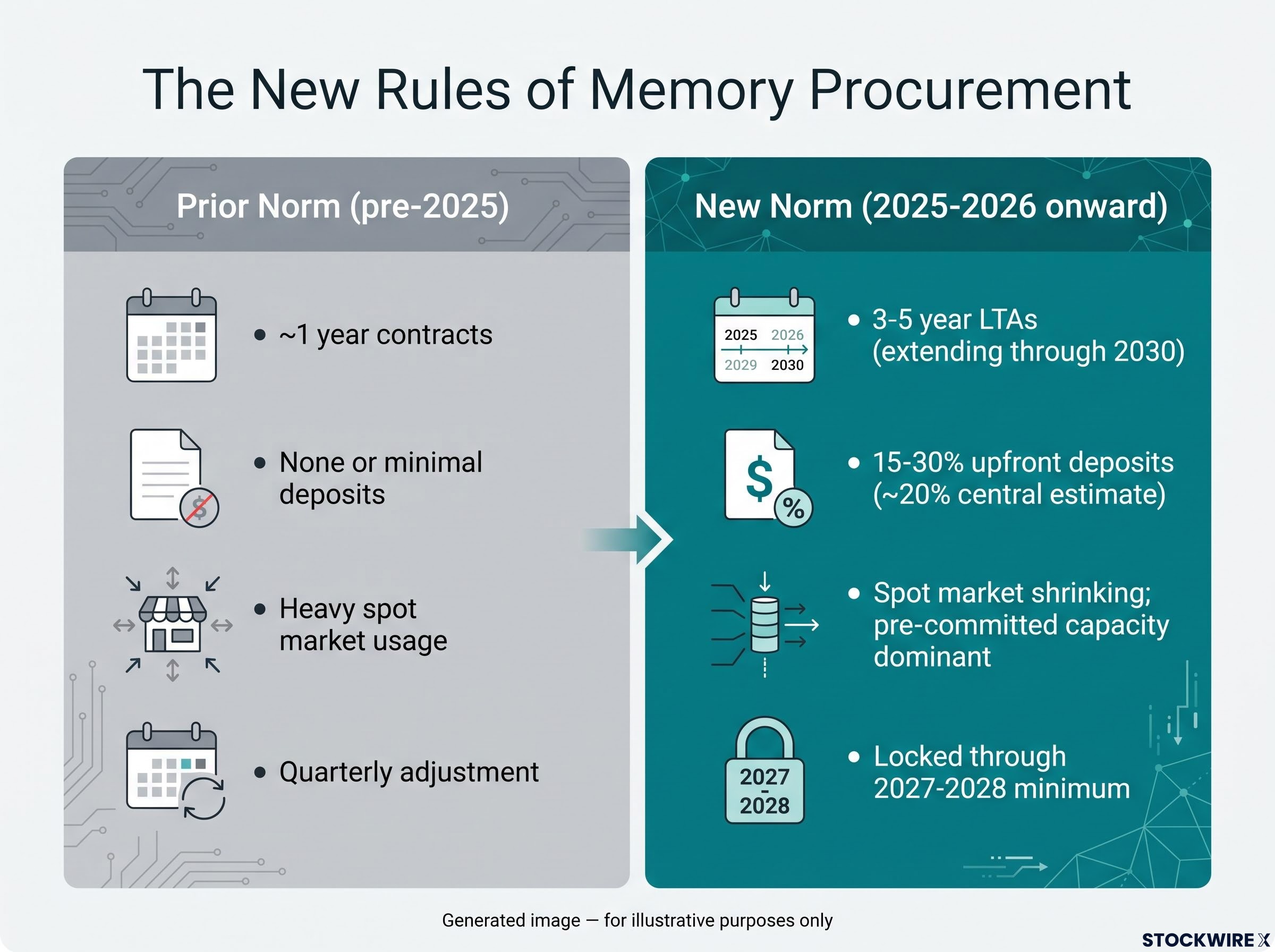

How the shortage has rewritten the rules of memory procurement

Before 2025, memory procurement worked on short cycles. Contracts typically lasted about one year. Buyers relied heavily on the spot market to adjust volumes and capture price dips. Flexibility was the default strategy.

That model is gone.

| Attribute | Prior Norm (pre-2025) | New Norm (2025-2026 onward) |

|---|---|---|

| Contract duration | ~1 year | 3-5 year LTAs, extending through 2030 |

| Deposit requirement | None or minimal | 15-30% of contracted volume (~20% central estimate) |

| Market reliance | Heavy spot market usage | Spot market shrinking; pre-committed capacity dominant |

| Supply security horizon | Quarterly adjustment | Locked through 2027-2028 minimum |

Samsung and SK hynix have confirmed multi-year agreements with customers including Microsoft and Google, securing supply through at least 2027-2028, according to TrendForce and company reporting. Tool and equipment suppliers indicate that the forward horizon on their own order books has lengthened considerably as a result of these customer commitments, with visibility now running to the close of 2027.

15-30% upfront deposits (approximately 20% as a central estimate) are now required under long-term memory supply agreements, according to Phillip Securities Research and industry reporting from Global Semi Research.

The deposit requirement is the clearest signal that buyers no longer trust spot market access to deliver the memory they need. They are prepaying for future supply, tying up capital years in advance, and sacrificing procurement flexibility to guarantee access. Memory is no longer treated as a commodity to be sourced on demand. It is being procured like strategic infrastructure.

The next major ASX story will hit our subscribers first

Winners, losers, and the buyers caught in the middle

The shortage’s effects are not evenly distributed. Each stakeholder group occupies a distinct position, and the dividing line runs between those who secured long-term supply and those who did not.

| Stakeholder Group | Position | Primary Benefit or Cost | Key Companies |

|---|---|---|---|

| Memory Producers | Primary beneficiaries | Exceptional pricing power, margin expansion, multi-year revenue visibility | Samsung, SK hynix, Micron |

| Equipment Makers | Strong secondary beneficiaries | Extended order books, forward visibility through 2027+ | ASML, Applied Materials, Lam Research |

| Hyperscalers | Beneficiaries with trade-offs | Guaranteed supply access at the cost of capital and flexibility | Microsoft, Google, Amazon, Meta |

| Device Makers | Negatively affected | Higher input costs, potential shortages, margin compression | PC, smartphone, consumer electronics OEMs |

Memory producers hold the strongest hand. Deposit-backed contracts reduce their exposure to the demand volatility that caused the 2022-2023 downturn, while pricing power is expanding margins to levels the industry has rarely sustained.

Equipment makers including ASML, Applied Materials, and Lam Research benefit from the producer side of the equation. Rather than building new fabs, memory companies are directing investment toward performance upgrades on tools within their existing cleanrooms, sustaining strong services demand for equipment suppliers and pushing confirmed order visibility out to 2027 and beyond, according to BofA and Goldman Sachs analyst notes.

Hyperscalers have secured their position, but at a cost. The capital tied up in deposits and the lost flexibility of short-duration contracts are the price of guaranteed access. For companies building AI infrastructure at scale, that trade-off is rational. For device makers who cannot match those commitments, the picture is considerably worse: higher input costs, fabs prioritising AI products over consumer memory, and limited ability to pass the full cost increase to end consumers.

The memory price forecast through 2028 carries concrete consequences for device makers: S&P Global Ratings confirmed on 11 June 2026 that the repricing cycle extends through at least 2028, while HP’s Q1 2026 disclosures showed memory’s share of laptop bill-of-materials costs rising from 15-18% to approximately 35%.

What the supercycle’s staying power means for the next two years

The structural case for extended tightness rests on four reinforcing conditions: price-inelastic AI demand, producer caution inherited from 2022-2023, 18-24 month ramp timelines for new capacity, and long-term contract lock-in that is steadily shrinking the spot market.

The current memory chip supercycle differs from prior DRAM upcycles in one critical respect: AI data centre operators now account for an estimated 70% of total memory shipment volumes, making the demand base structurally resistant to the consumer-led corrections that ended previous pricing peaks.

Supercycle conditions are broadly expected to extend through 2027-2028, according to BofA, TrendForce, and commentary from SK hynix and Samsung. Structural tightness could persist toward 2030 if demand continues at current trajectories and capacity additions remain disciplined.

Three variables will determine whether conditions tighten further, stabilise, or begin to ease:

- New fab investment announcements from Samsung, SK hynix, and Micron, which would signal the industry’s willingness to add capacity despite the 2022-2023 overcapacity trauma

- AI infrastructure spending trajectories from hyperscalers, which determine whether demand growth sustains or moderates

- The pace of long-term contract adoption, which is shrinking spot market volume and amplifying price volatility for any buyer still relying on spot procurement

For any organisation making technology infrastructure decisions in the next 24 months, the supply outlook means the cost and availability of memory should be treated as a planning constraint, not a background variable.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking projections regarding supply timelines and pricing are subject to change based on market developments and company decisions.