The processor segment of the semiconductor industry grew 53% year-over-year in Q1 2026. One quarter later, guidance points to 67%. The growth rate is not holding steady; it is accelerating, and the gap between companies riding that wave and those outside it has become too wide to ignore.

According to Phillip Securities Research, major hyperscalers have collectively committed around US$710 billion in capital expenditure for 2026, a figure that represents an 89% jump compared to the prior year. That spending is flowing almost entirely into AI training and inference infrastructure, and it is landing unevenly across the semiconductor sector. Nvidia grew revenue 85%. Qualcomm shrank 3.5%. Same sector label. Completely different businesses.

Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion on hyperscaler AI capex in Q1 2026 alone, pushing full-year 2026 combined guidance to approximately $725 billion and setting a trajectory toward $1 trillion in annual spending by 2027.

Here is the framework for understanding which AI semiconductor stocks are positioned inside the spending wave, which sit outside it, and why treating “semiconductors” as a single investment category creates blind spots that cost you money.

How fast the AI chip boom is actually moving

The headline growth figures are large. The more important detail is that they keep getting larger.

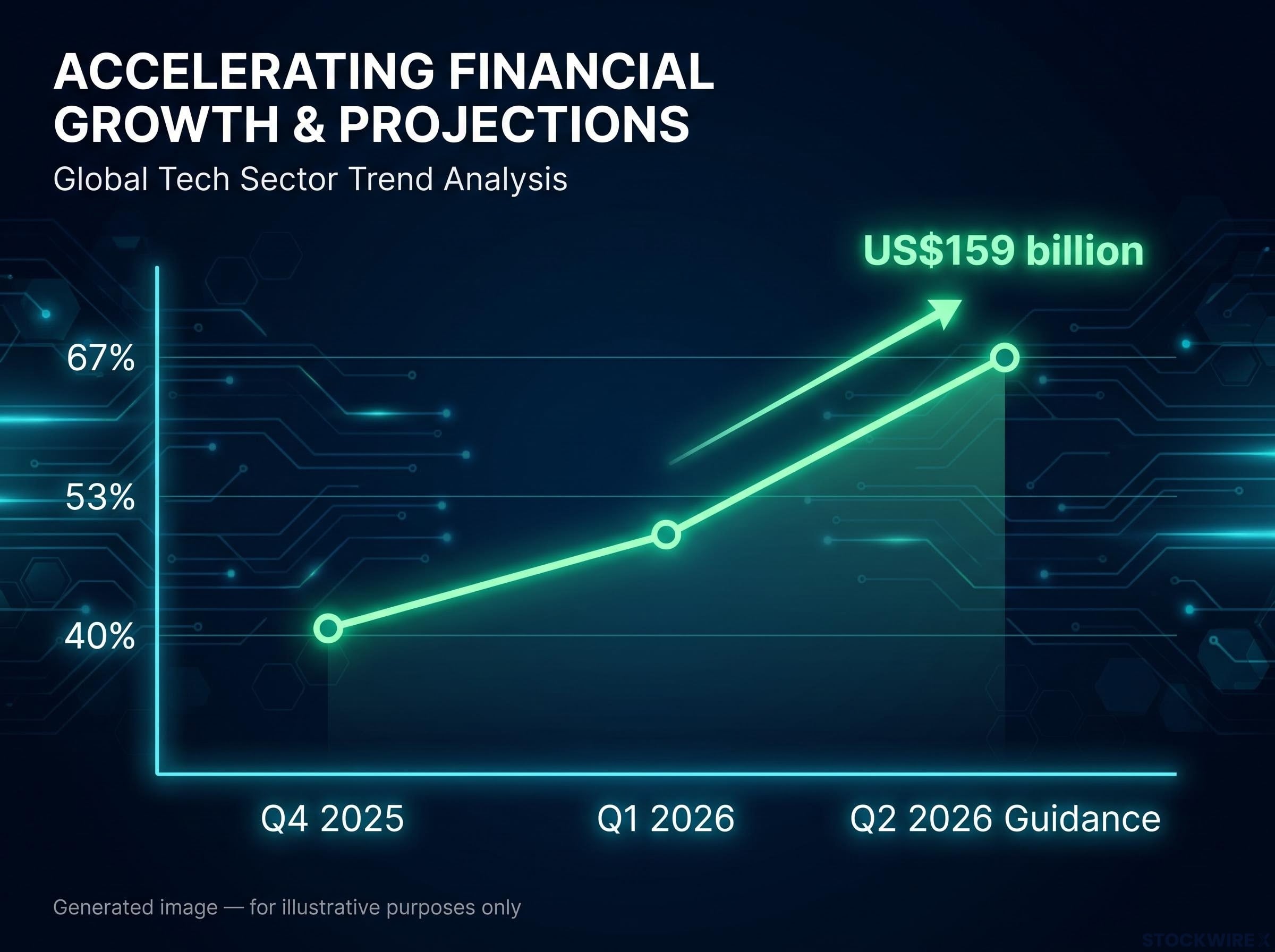

- Q4 2025: Processor segment revenue grew 40% year-over-year

- Q1 2026: That rate accelerated to 53% year-over-year

- Q2 2026 guidance: Approximately US$159 billion in revenue, projecting 67% year-over-year growth

That pattern, where the growth rate itself steepens quarter after quarter rather than reverting toward a mean, is structurally unusual. PC and smartphone cycles do not behave this way. Consumer replacement demand tends to spike and fade. What is happening in AI infrastructure is different: hyperscalers are making multi-year commitments to build out training and inference capacity, and each quarter’s spending is larger than the last.

US$710 billion: The figure that major hyperscalers have collectively guided for their 2026 capital expenditure, reflecting an 89% year-over-year increase, per Phillip Securities Research. Individual hyperscaler disclosures suggest a range of US$600-720 billion, with the US$710 billion figure falling within that band.

The sequential acceleration tells you that AI infrastructure spending has not yet reached a plateau. For investors evaluating the durability of this cycle, that distinction between “growing fast” and “growing faster each quarter” is the one that matters most.

When big ASX news breaks, our subscribers know first

Nvidia’s revenue growth rate keeps intensifying

In Q1 2026, Nvidia posted revenue of US$81.6 billion, representing 85% year-over-year growth, and delivered its third straight quarter in which the year-over-year growth rate climbed rather than moderated.

Nvidia’s SEC earnings filing for the quarter ending April 2026 provides the primary-source financial data underlying the US$81.6 billion revenue figure and the 85% year-over-year growth rate cited here, offering investors direct access to the company’s official disclosures.

Three quarters in a row. Not three quarters of high growth, which would be notable enough. Three quarters where the growth rate itself kept climbing. That pattern removes the ambiguity that normally surrounds post-product-launch demand. A typical hardware cycle sees demand spike on release and then moderate. Nvidia’s trajectory shows the opposite: hyperscaler appetite for its data-centre AI GPUs is still intensifying, driven by both AI model training and inference cluster deployment.

Nvidia remains the most direct real-time read on the health of the AI infrastructure capex cycle. When its growth rate accelerates for a third straight quarter, it tells you the underlying demand engine has not peaked. AMD and Broadcom are capturing meaningful portions of the same spending wave, but Nvidia’s scale makes its results the bellwether.

AMD and Broadcom show the AI opportunity is bigger than one company

AMD recorded Q1 2026 revenue of US$10.3 billion, a 38% year-over-year rise that marked the company’s best growth performance since 2022. The performance was driven by its data-centre segment, specifically fifth-generation EPYC server CPUs and MI-series Instinct accelerators, including the MI350 GPU line. AMD has moved beyond a pure CPU market-share story; it now offers both high-performance server processors and competitive AI accelerators, making it a genuine second source for hyperscalers building out gigawatt-scale AI infrastructure.

Broadcom told a different but equally compelling version of the same story. Its AI semiconductor revenue grew at triple-digit year-over-year rates, though the precise figures carry a source conflict. Phillip Securities Research reported total revenue of US$22.2 billion (up 48%) with AI semiconductor revenue reaching US$10.8 billion, up 143% year-over-year, while a separate audit identified Q1 FY2026 figures of US$19.3 billion (up approximately 29%) with AI semiconductor revenue of US$8.4 billion (up 106%). Readers should verify against Broadcom’s official filings. Regardless of which figures are used, the directional conclusion is the same: this was the company’s fastest revenue growth in approximately a decade.

Broadcom’s model is fundamentally different from Nvidia’s. Where Nvidia sells a general-purpose merchant GPU at scale, Broadcom designs bespoke custom accelerators (ASICs and XPUs) and AI networking silicon for a small number of very large hyperscaler customers. The fact that both models are thriving simultaneously tells you something about the size of the opportunity: hyperscaler AI budgets are large enough to sustain structurally different business strategies at the same time. For portfolio construction, that means AMD and Broadcom are not Nvidia substitutes; they are complementary exposures to the same underlying capex wave.

Broadcom’s custom accelerator model sits within a broader hyperscaler trend: Google, Meta, Amazon, and Microsoft are all developing proprietary ASIC programmes driven by the same economic logic of lower per-inference costs, improved energy efficiency, and reduced dependence on a single external chip supplier.

| Company | Q1 2026 Revenue | YoY Growth | Key AI Product | Q2 Guidance Direction |

|---|---|---|---|---|

| Nvidia | US$81.6B | +85% | Data-centre AI GPUs | Accelerating |

| AMD | US$10.3B | +38% | EPYC CPUs + MI-series accelerators | Accelerating |

| Broadcom | US$19.3B-US$22.2B* | +29%-48%* | Custom ASICs + AI networking | Accelerating |

| Qualcomm | US$10.6B | -3.5% | Handset SoCs (consumer) | -7% YoY guided |

Broadcom figures reflect a source discrepancy. Range spans the original Phillip Securities Research figures and a separate audit. Verify against official filings.

What “semiconductor exposure” actually means, and why Qualcomm is a different story

Qualcomm closed Q1 2026 with revenue of US$10.6 billion, a 3.5% year-over-year contraction, and its Q2 2026 guidance called for a further 7% year-over-year decline. It was the sole major processor company guiding for contraction while the rest of the segment guided for acceleration.

The divergence is structural, not a matter of execution. Qualcomm’s revenue base is concentrated in handset system-on-chips (SoCs), the processors that power smartphones, and connectivity silicon. Its customer base skews heavily toward Chinese OEMs, whose procurement behaviour is sensitive to memory pricing and inventory cycles. The specific headwinds weighing on results include:

- Higher memory prices squeezing the component budgets that Chinese OEMs can allocate to procurement

- Handset inventory cycle drawdowns constraining new orders

- Component cost pressures across the smartphone supply chain

- Limited participation in data-centre AI infrastructure spending

These are not temporary disruptions. They reflect the cyclical dynamics of the consumer handset market, which operates on fundamentally different demand drivers than AI infrastructure.

The contrast is stark: Nvidia grew 85%. Qualcomm shrank 3.5%. Both carry the “semiconductor” label. The label is analytically misleading.

The four buckets that actually define semiconductor sector risk

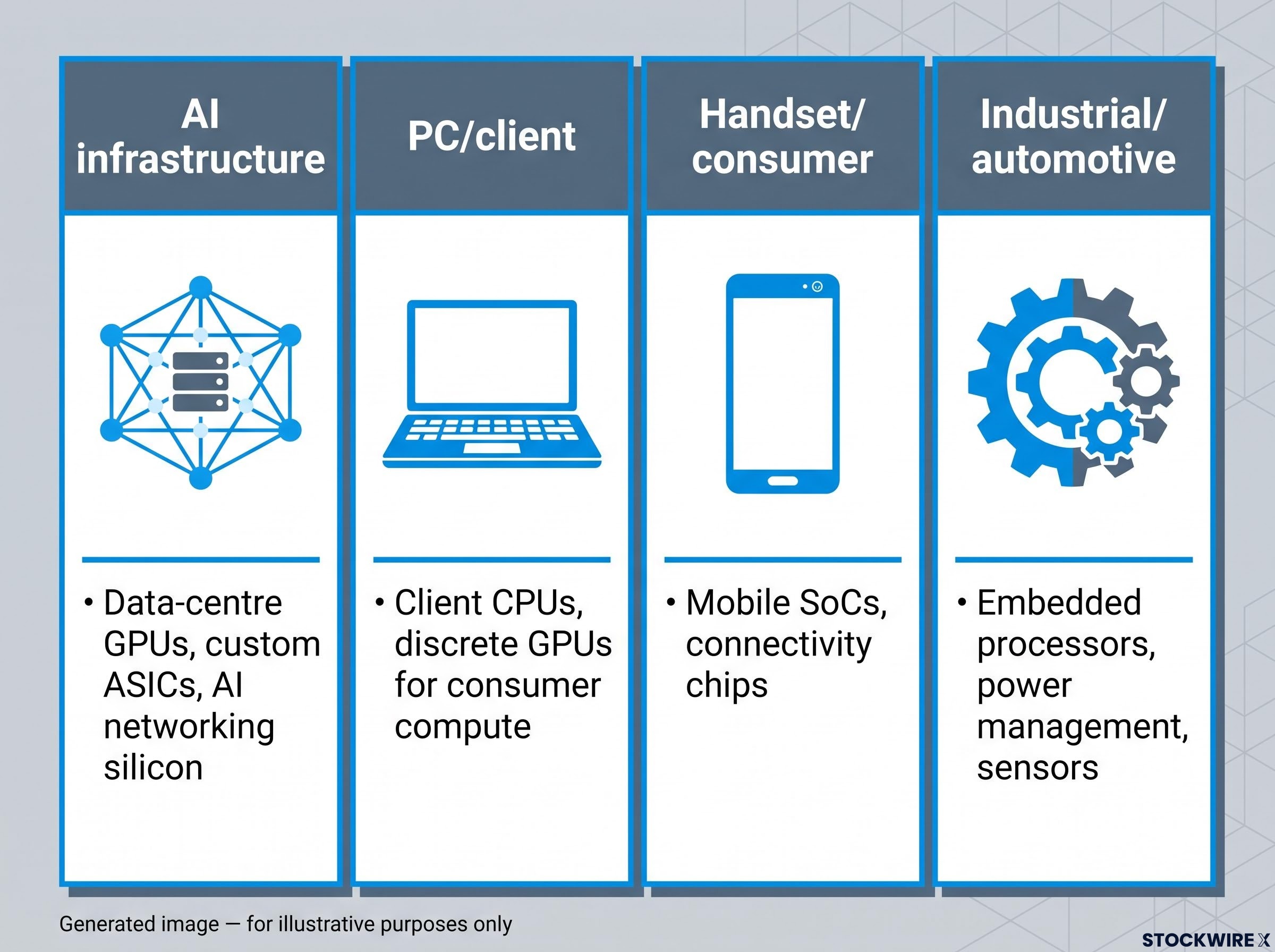

The semiconductor sector segments into at least four distinct categories, each with different demand drivers and cyclical characteristics:

- AI infrastructure: Data-centre GPUs, custom ASICs, AI networking silicon. Currently in an unusual multi-year acceleration phase.

- PC/client: Client CPUs, discrete GPUs for consumer compute. Moderate cyclical demand tied to enterprise refresh and consumer replacement.

- Handset/consumer: Mobile SoCs, connectivity chips. In active contraction as of Q1 2026, driven by inventory and memory pricing headwinds.

- Industrial/automotive: Embedded processors, power management, sensors. Slow-cycle, tied to manufacturing capex and vehicle production volumes.

End-market exposure, not sector membership, is the variable that matters for investment decisions. Q1 2026 proved it.

The next major ASX story will hit our subscribers first

What the Q2 guidance signals about the durability of the AI cycle

US$159 billion: The Q2 2026 processor segment revenue figure that Phillip Securities Research projects, equivalent to roughly 67% year-over-year growth.

That figure is the forward-looking validation of the Q1 results. Nvidia, AMD, and Broadcom all guided for continued growth acceleration. Qualcomm guided for a 7% year-over-year revenue decline. Three of four major processor companies are accelerating; the fourth is contracting.

The on-device AI thesis, where AI processing moves onto smartphones and creates a new upgrade cycle, remains a potential future catalyst for Qualcomm. But it has not yet materialised as a revenue driver at scale. Until it does, handset headwinds remain the dominant near-term dynamic.

When Q2 guidance from AI-exposed names unanimously points to acceleration, it reinforces rather than complicates the investment thesis. The AI infrastructure cycle shows no guidance-level signs of peaking, and the structural divide between AI-exposed and consumer-exposed chipmakers is, if anything, widening.

What the Q1 earnings split means for how investors should position now

The Q1 data points to a clear positioning framework: overweight AI infrastructure names, and treat handset and consumer semiconductors as a structurally separate, less attractive cycle.

Within the AI infrastructure bucket, the three primary access points are complementary, not redundant:

- Nvidia: Merchant GPU dominance; the largest single-name beneficiary of hyperscaler AI capex

- AMD: Dual exposure through both MI-series GPU accelerators and EPYC server CPUs (where it continues to gain share from Intel), providing two separate product-line routes into AI infrastructure spending

- Broadcom: Custom ASIC and XPU model plus AI networking silicon; bespoke solutions for hyperscaler workloads that differ from the merchant GPU approach

Combining exposure across these three reduces single-name concentration risk while preserving full participation in the underlying capex cycle. That is diversification within a theme, not redundancy.

Semiconductor cycle positioning across the current acceleration phase requires monitoring not just demand signals but also the locked-in supply wave arriving in 2027-2029, when TSMC’s $52-56 billion 2026 capital budget and Samsung’s estimated $70-80 billion annual outlay translate into wafer capacity that could outpace even AI-driven demand growth.

The two forward variables to watch:

- Q3 2026 earnings guidance from AI-exposed names. Any sign of guidance deceleration would be the earliest signal that the acceleration phase is maturing.

- A structural AI catalyst for Qualcomm. If on-device AI or another revenue stream gives Qualcomm meaningful participation in AI infrastructure spending, its relative positioning changes materially.

Until one of those variables shifts, the Q1 earnings split provides the clearest segmentation framework investors have had for navigating the semiconductor sector this cycle.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.