UBS Maps 3 Market Paths From $200 Oil to S&P 500 at 8,200

38 mins ago

The memory market has not repriced. It has restructured. Micron just posted quarterly revenue of $41.46 billion, clearing the Street’s $35.91 billion estimate by a wide margin, with gross margins of 84.9% and next-quarter guidance of $50 billion. Those numbers are not a cyclical blowout. They are the first legible signal of a permanent shift in who captures value from the AI infrastructure buildout.

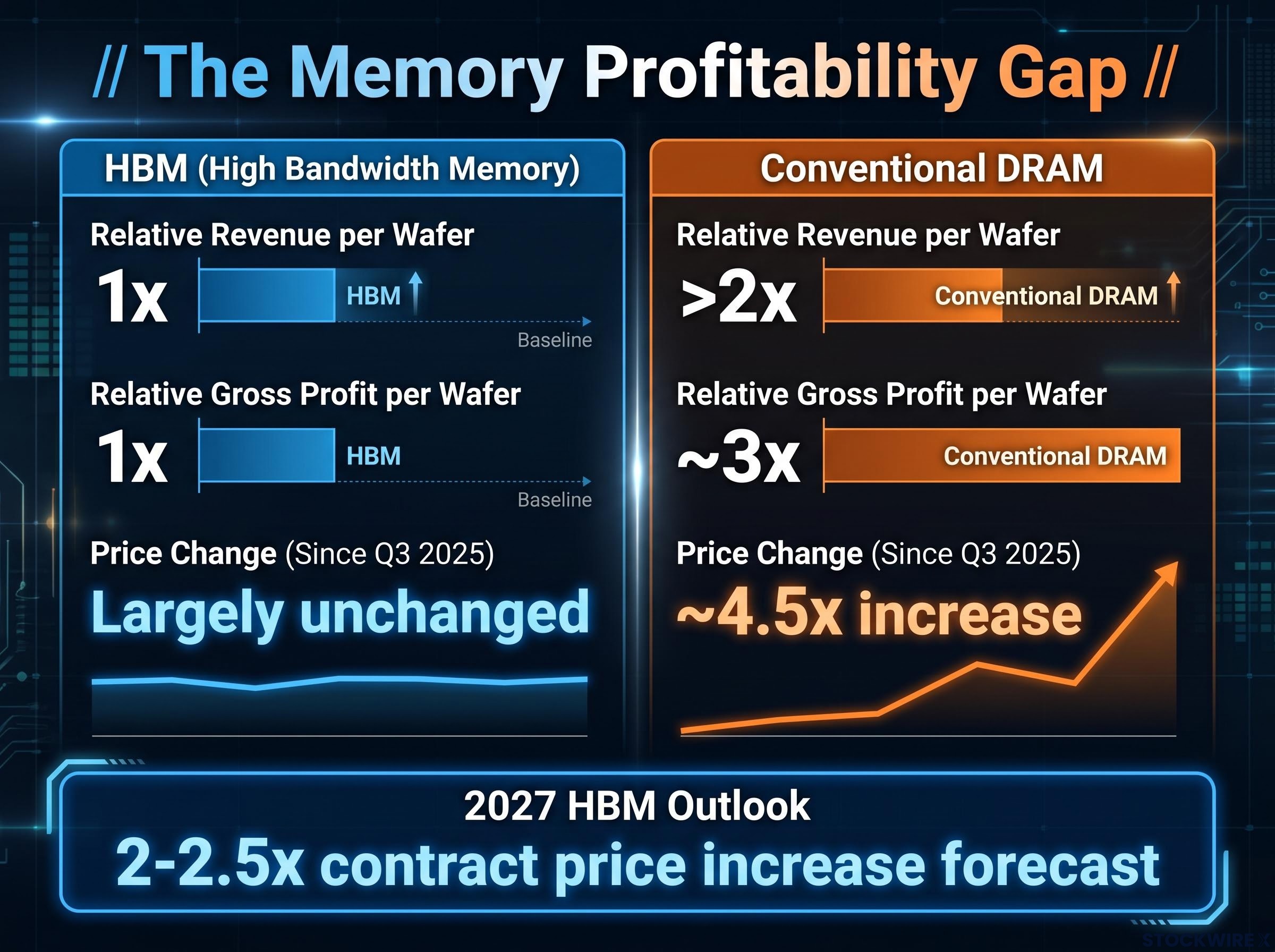

Behind the headline beat sits a pricing dynamic that has not yet fully registered in markets or in hyperscaler capital allocation plans. High Bandwidth Memory (HBM), the specialised memory architecture at the core of every high-performance AI accelerator, faces contract price increases of 2 to 2.5 times for 2027 procurement cycles. That adjustment is not supplier aggression. It is the structural floor required to keep wafer capacity oriented toward HBM rather than drifting back to conventional DRAM, which currently delivers roughly two times the revenue and close to three times the gross profit per wafer. The entire AI accelerator roadmap depends on resolving this economic irrationality.

Here is the framework for assessing where earnings power accrues, where cost pressure builds, and what to watch before committing capital: from Micron’s wafer economics to GPU bill-of-materials, from hyperscaler capex budgets to the equity revaluation already underway among analysts who have run the numbers.

The core paradox is straightforward. HBM is the most strategically important memory architecture in AI, yet it is the least profitable way to use a wafer. Bernstein finds that directing wafer capacity toward conventional DRAM yields revenue exceeding two times that of HBM and gross profit of roughly three times per wafer, a gap that has grown increasingly difficult for suppliers to ignore.

That gap has widened sharply. Spot prices for conventional DRAM have climbed roughly 4.5 times since Q3 2025, while HBM rates, fixed under annual supply agreements, have moved little across the same stretch.

Conventional DRAM prices have climbed roughly 4.5 times since Q3 2025. HBM contract pricing has held largely flat over that same period. That divergence is the single clearest signal that HBM is mispriced relative to the capacity it consumes.

The substitution threat is real. If the gap is not closed, rational capacity allocation moves away from HBM and toward commodity DRAM, choking the AI accelerator supply chain at its most critical input. Bernstein analyst Mark Li projects a 2 to 2.5 times HBM average selling price (ASP) increase for 2027, pitched at a level that narrows the profitability gap without fully closing it, so that HBM remains economically viable for the broader AI ecosystem.

What this tells you is that the repricing is not supplier aggression. It is a structural correction the supply chain has no credible mechanism to avoid.

The DRAM supply constraint underpinning that divergence is not a temporary inventory correction; SK Hynix projects tightness through 2030, HBM inventory industry-wide sits at just 3-4 weeks, and all three major producers are fully sold out through 2026, conditions that give suppliers the structural leverage to push through the repricing mechanics described above.

| Metric | HBM | Conventional DRAM |

|---|---|---|

| Relative revenue per wafer | 1× (baseline) | >2× |

| Relative gross profit per wafer | 1× (baseline) | ~3× |

| Price change since Q3 2025 | Largely unchanged | ~4.5× increase |

| 2027 pricing direction | 2-2.5× increase forecast | Elevated, stabilising |

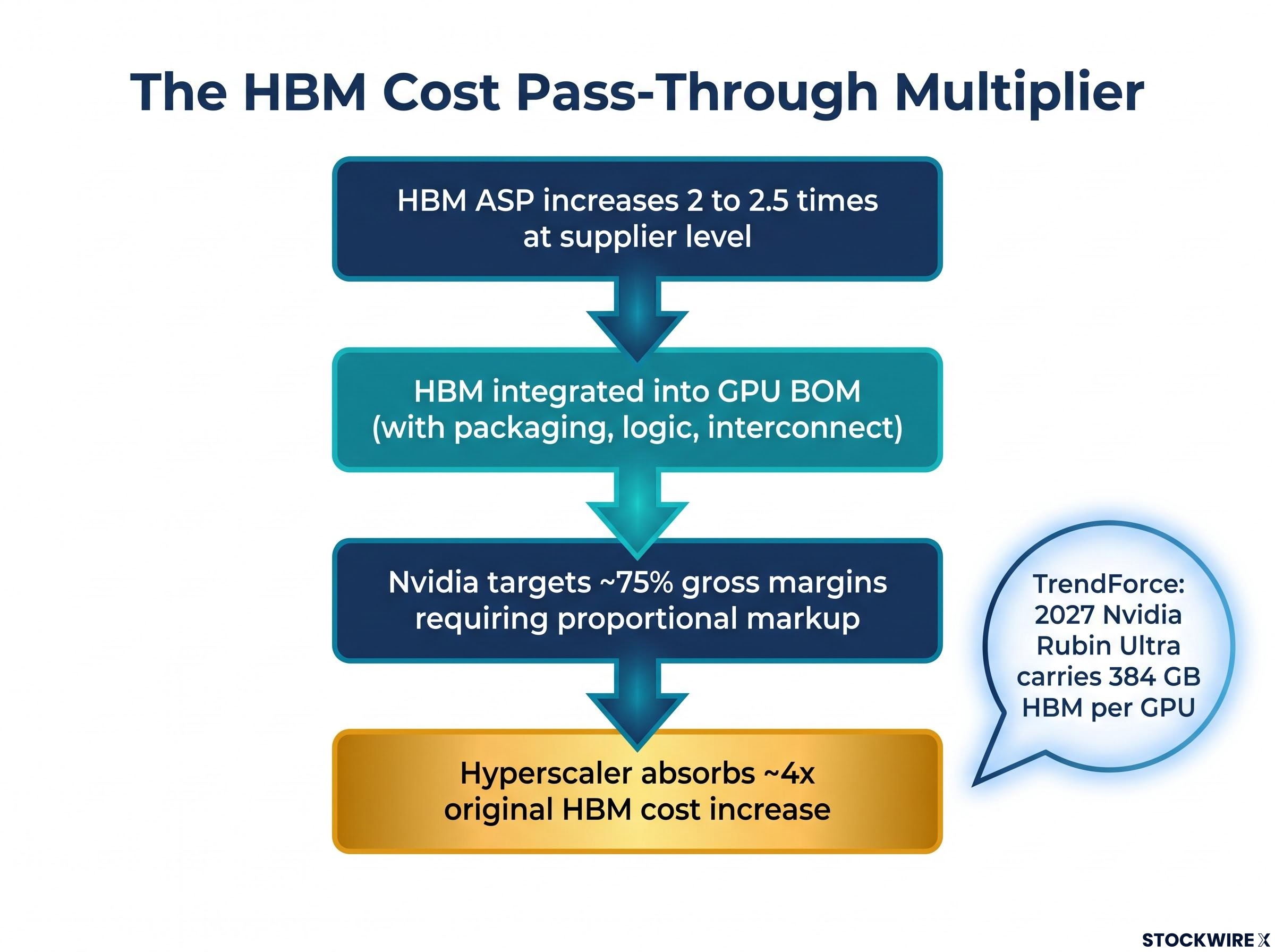

HBM is not purchased as a standalone component. It is integrated directly into GPUs and AI accelerators, meaning its cost feeds straight into the bill of materials (BOM), the full list of components and costs that make up a finished product. That structural position means HBM price changes are not absorbed; they are multiplied through the margin expectations of GPU vendors.

Bernstein maps the pass-through mechanism in four steps:

That fourfold multiplication is not aggressive pricing. It is the mathematical consequence of maintaining margin structure across a bill of materials where memory is now the fastest-moving cost input.

Price alone does not capture the full impact. Next-generation accelerators carry substantially more HBM per device. According to TrendForce, Nvidia’s Rubin Ultra platform in 2027 will carry 384 GB of HBM per GPU, a significant increase from the current generation.

TrendForce HBM capacity forecasts indicate that HBM wafer input will account for approximately 30% of total DRAM wafer input by end of 2027, a capacity concentration that makes the per-wafer profitability gap between HBM and conventional DRAM increasingly difficult for suppliers to sustain without a significant pricing correction.

According to Micron, HBM4 uptake is accelerating at twice the rate seen with the previous generation, and customers have locked in supply commitments running through 2028 and further out. Higher density and higher per-unit prices are arriving simultaneously, not sequentially.

What this means for anyone modelling GPU economics is that the memory line item inside every next-generation AI accelerator stops being secondary cost context. It becomes the primary pricing variable that finance teams and procurement officers need to model.

The most consequential shift in Micron’s business model is not the HBM pricing tailwind. It is the contract architecture sitting underneath it.

Micron has put 16 strategic customer agreements (SCAs) in place, each structured as a binding, take-or-pay obligation that cannot be cancelled. Unlike standard purchase orders, these arrangements require customers to pay regardless of whether they accept delivery, with terms that typically span five years and include pricing floor provisions that protect gross margins above any prior cycle peak.

Q3 results at Micron came in at $41.46 billion in revenue versus the $35.91 billion consensus, with adjusted EPS of $25.11 against $20.86 expected, and gross margins of 84.9%. The magnitude of the beat is the headline. The contract structure beneath it is the story.

Micron’s Q4 guidance of approximately $50 billion in revenue, paired with an approximately 86% gross margin target that has no precedent in DRAM and NAND manufacturing history, reflects the moment when HBM4 pricing crossed from supply-constrained cyclical into a scarcity-pricing regime that the contract structure is now designed to sustain.

| SCA metric | Current coverage | Projected (full implementation) |

|---|---|---|

| Contract type | Non-cancellable, take-or-pay | |

| DRAM bit volume covered | ~20% | Expanding |

| NAND bit volume covered | ~33% | Expanding |

| Total revenue under SCA | Partial | >50% |

| Key structural terms | Price floors locking gross margins above any prior cycle peak | |

For a finance-focused reader evaluating Micron equity, the SCA structure is the mechanism that converts an HBM pricing event into a durable, multi-year earnings uplift rather than a single-quarter beat. When contracted revenue meets HBM repricing, memory begins to behave more like an infrastructure utility than a commodity, with an earnings profile that is both more predictable and structurally higher-margin than in any prior cycle. That is the argument for shifting Micron’s valuation framework away from trough-to-peak cyclical multiples toward long-duration cash flow analysis.

The repricing does not stop at the memory supplier. It propagates into the capital budgets of every company building AI infrastructure at scale.

According to Bernstein, the inflation in memory costs alone has the potential to push hyperscaler data centre capital expenditure up by around 30%. Applied to capex envelopes already measured in the hundreds of billions, the absolute dollar impact is substantial even if unit demand remains intact.

Hyperscaler capex budgets reaching approximately $725 billion in 2026 provide the demand floor that makes the HBM repricing economically viable without triggering demand destruction, since the AI infrastructure deployment targets underlying those budgets cannot be achieved without continued HBM allocation regardless of per-unit cost increases.

Hyperscalers face three strategic responses:

Bernstein analyst Mark Li expects AI spending to press forward, but argues that some form of recalibration is unavoidable, with cost pressures likely spreading across the supply chain and less resilient participants seeing their margins squeezed.

The 30% capex inflation figure is abstract until you recognise that it will function as a sorting mechanism. Well-capitalised hyperscalers expand and maintain strategic AI advantage. Undercapitalised cloud players face genuine deployment slowdowns that show up in competitive positioning over the next 18 months.

Downstream, higher AI service pricing and tougher internal hurdle rates will create a two-speed AI deployment environment. Strategically essential workloads proceed at scale. Speculative or lower-priority AI projects face deferral or repricing, particularly for smaller cloud operators and AI startups that cannot pass cost increases through as effectively.

The equity revaluation underway is not a collection of isolated upgrades. It is a coherent rerating thesis centred on 2027 EPS revisions driven by the HBM repricing mechanics already described.

Bernstein has raised price targets across all three major HBM-exposed memory suppliers, with 2027 EPS forecasts running approximately 25 to 38% above prior consensus:

| Company | Prior target | New target | Rating | Key forward metric |

|---|---|---|---|---|

| Samsung | KRW 225,000 | KRW 440,000 | Outperform | 2027 EPS 25-38% above consensus |

| SK Hynix | KRW 1,150,000 | KRW 3,300,000 | Outperform | 2027 EPS 25-38% above consensus |

| Micron | $510 | $1,300 | Outperform | 2027 EPS 25-38% above consensus |

| KIOXIA | N/A | Underperform | No material HBM exposure | |

Susquehanna separately moved its Micron price target to $2,000 from a prior $1,750, with revised estimates now pointing to annualised EPS in the region of $200 as the company exits fiscal year 2027.

Susquehanna’s updated model has Micron generating more than $110 billion in free cash flow across FY2027, with shareholders expected to receive the bulk of those proceeds.

The divergence between KIOXIA’s maintained Underperform and the dramatic target increases for Samsung, SK Hynix, and Micron tells you that HBM exposure is not a modifier within the memory trade. It is the binary variable determining whether the structural repricing thesis applies to a given position at all.

The structural bull case is analytically sound. Whether it delivers depends on a specific set of conditions that investors can monitor in real time.

Micron has revised its forecast for the HBM total addressable market, now expecting it to cross $100 billion in 2027, pulling that milestone forward by roughly twelve months relative to earlier projections. That demand anchor is what makes the pricing correction viable without destroying demand.

Bernstein’s 2 to 2.5 times range is deliberately set below the level that would fully close the profitability gap with conventional DRAM, reflecting an awareness that eliminating the gap entirely would put downstream ecosystem participants under excessive strain. That built-in conservatism is itself a risk buffer: even at the low end, the earnings uplift for HBM-exposed suppliers is substantial. The Rubin Ultra 384 GB HBM density specification provides the near-term demand anchor.

The read you should take from this is that one data point, the HBM contract price published for 2027 GPU procurement cycles, will confirm or challenge the entire thesis. That makes contract price announcements the highest-priority monitoring trigger for anyone positioned in memory stocks.

The analytical thread runs in one direction. The HBM repricing is structural, driven by wafer economics that the supply chain cannot override. The contracted revenue model at Micron converts that pricing event into multi-year earnings visibility. And the equity revaluation among analysts, with 2027 EPS forecasts 25 to 38% above prior consensus for HBM-exposed names, is directionally consistent with the underlying economics.

The asymmetry in where cost pressure lands is the critical framing for portfolio positioning:

Memory suppliers with HBM capacity and contracted revenue structures currently offer the most analytically grounded upside case relative to prior consensus. GPU and hyperscaler exposure requires separate analysis of margin compression and capex absorption capacity. The HBM contract price for 2027 remains the single variable that will either validate or challenge this framework.

For investors wanting to stress-test the structural shift thesis against the cyclical peak scenario, our dedicated guide to Micron’s valuation framework examines the 14 times earnings multiple in detail, including what that multiple implies about normalised earnings if the cycle partially reverts and how Samsung’s 2026 capacity expansion changes the downside calculus.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

High Bandwidth Memory (HBM) is the specialised memory architecture at the core of every high-performance AI accelerator, making it a critical input cost for GPU vendors like Nvidia. Because HBM is integrated directly into the GPU bill of materials, price changes at the memory supplier level amplify approximately fourfold by the time they reach hyperscaler purchase prices.

Conventional DRAM currently delivers more than twice the revenue and roughly three times the gross profit per wafer compared to HBM, creating a structural incentive for suppliers to redirect capacity away from HBM. Bernstein projects a 2 to 2.5 times HBM average selling price increase for 2027 procurement cycles as the minimum correction needed to keep wafer capacity oriented toward HBM and prevent a supply chain bottleneck.

According to Bernstein, memory cost inflation alone could push hyperscaler data centre capital expenditure up by around 30%, applied against capex envelopes already running into the hundreds of billions of dollars. Hyperscalers face a choice between expanding total budgets, accepting fewer deployed accelerators per dollar, or rebalancing toward HBM-lighter accelerator configurations.

Micron has put 16 non-cancellable, take-or-pay strategic customer agreements in place, typically spanning five years with pricing floors that lock gross margins above any prior cycle peak. These contracts convert the HBM pricing tailwind into multi-year earnings visibility rather than a single-quarter beat, supporting the case for valuing Micron on long-duration cash flow analysis rather than traditional cyclical multiples.

Bernstein has raised price targets for Samsung (to KRW 440,000), SK Hynix (to KRW 3,300,000), and Micron (to $1,300), with 2027 EPS forecasts running 25 to 38% above prior consensus for all three. KIOXIA, which has no material HBM exposure, carries a maintained Underperform rating, illustrating that HBM capacity is the binary variable separating beneficiaries from bystanders in this repricing cycle.