Technology has declared financial exchanges obsolete at least four times in the last thirty years. Ticker tape gave way to electronic trading, electronic trading gave way to ECNs, ECNs gave way to dark pools, and each time the incumbents absorbed the challenger, grew larger, and emerged with wider moats. The pattern is so consistent it has become its own signal.

The current moment is the most intense version of this recurring narrative. Prediction markets, AI-native data tools, and crypto perpetual futures are all being cited simultaneously as exchange-killers, and the convergence is prompting investors to reassess whether exchange stocks deserve their infrastructure-grade multiples. It is a fair question, and it deserves a structured answer rather than a reflexive one.

Here is what the structural logic and the data actually tell you about exchange durability, why the disruption categories are not interchangeable, and why MIAX specifically warrants examination at its current valuation discount. The framework that follows separates durable moats from genuine pressure points, and gives you a clear lens for evaluating where to apply conviction and where to stay cautious.

How exchanges have absorbed every disruption thrown at them

The pattern compresses neatly. Ticker tape was supposed to democratise information away from floor traders; exchanges adopted it and expanded access. Electronic trading was supposed to disintermediate the venue itself; exchanges went electronic and cut costs. ECNs were supposed to fragment liquidity permanently; the major exchanges acquired or replicated the best ECN features. Dark pools were supposed to siphon institutional volume; exchanges launched their own dark pool alternatives and retained the regulatory and clearing infrastructure that institutions require.

- Ticker tape: Adopted as a distribution tool; expanded exchange reach rather than undermining it

- Electronic trading: Absorbed into exchange infrastructure, reducing costs and increasing throughput

- ECNs: Best features acquired or replicated; exchanges retained the liquidity core

- Dark pools: Exchanges launched competing offerings while retaining clearing and regulatory advantages

The most telling illustration is not hypothetical. CME ran a direct campaign to incentivise traders to migrate away from the Minneapolis spring wheat contract, the predecessor to MIAX Futures, yet walked away with less than 1% of market share despite its considerable capital and distribution advantages. This is not a trivial footnote. It demonstrates that liquidity positions, once established, are sufficiently durable that even a well-resourced incumbent offering financial inducements could not break them loose, which is arguably the most instructive data point available when assessing disruption risk to exchange stocks.

Exchanges have already begun acquiring and replicating prediction market and crypto-adjacent products. Tokenisation and DeFi, according to institutional commentary, are more likely to reconfigure plumbing than destroy incumbents. The absorption pattern is structural behaviour, not luck.

When big ASX news breaks, our subscribers know first

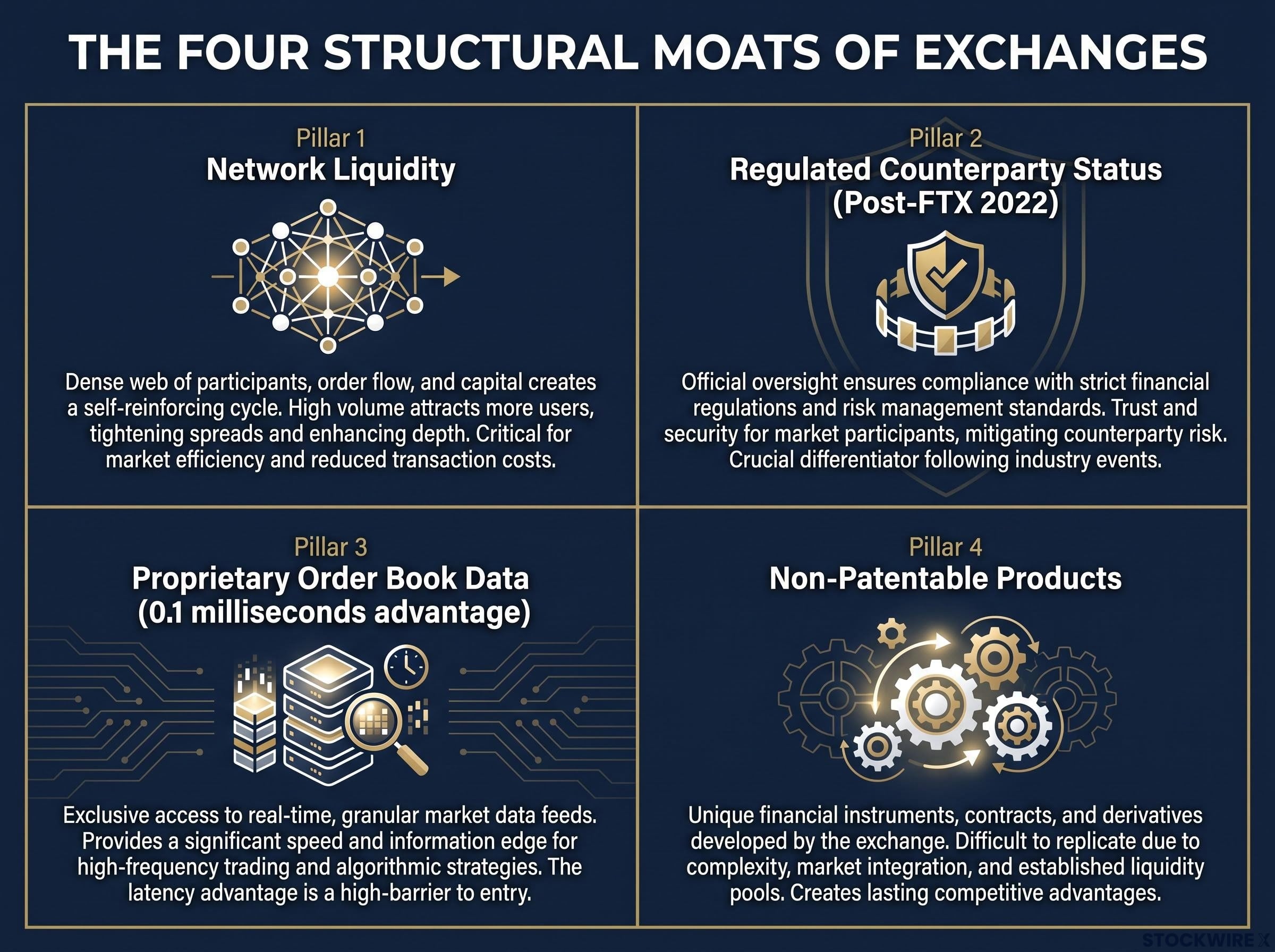

The four structural moats that make exchanges difficult to kill

Exchange durability rests on four interlocking barriers. Each one is individually difficult to replicate. Combined, they form a competitive position that no challenger has managed to overcome simultaneously.

The five competitive moat sources formalised by Morningstar, intangible assets, switching costs, network effects, cost advantage, and efficient scale, map directly onto exchange infrastructure, with exchanges typically exhibiting multiple reinforcing sources simultaneously rather than relying on any single driver.

Network liquidity is the most visible moat. Accumulated liquidity attracts more liquidity; new entrants face a cold-start problem that capital alone cannot solve, as the CME spring wheat example demonstrates. Regulated counterparty requirements form the second layer: institutional investors and sovereign wealth funds require regulated, audited counterparties for settling large trades, which structurally excludes unregulated platforms from this market segment.

Proprietary order book data represents the third moat. Exchanges sit at the centre of trillions of dollars in buy and sell side flow, accumulating data that no public source can replicate. The dynamic is illustrated by a well-known episode in which a Wall Street firm built a fibre optic cable running 0.1 milliseconds faster than existing infrastructure and found that every major player subscribed, not because the advantage was large in absolute terms, but because no firm could afford to let a competitor hold it instead. That logic governs institutional data subscription decisions across the board.

The fourth moat is counterintuitive. Non-patentable products mean that any trading product an upstart launches can be replicated immediately by an exchange with superior liquidity and distribution. This sounds like it weakens incumbents, but it does the opposite: it removes the moat-building potential from challengers while preserving the liquidity and infrastructure advantages of established players.

| Moat type | What it protects | Why it is hard to replicate |

|---|---|---|

| Network liquidity | Volume concentration and pricing efficiency | Cold-start problem; liquidity attracts liquidity |

| Regulated counterparty status | Institutional and sovereign fund access | Post-FTX regulatory requirements have raised the bar further |

| Proprietary order book data | Data revenue and speed-dependent subscriptions | Trillions in flow data; no public substitute exists |

| Non-patentable products | Product replication advantage for incumbents | Challengers cannot build durable product moats; incumbents clone freely |

The post-FTX regulatory reinforcement

The collapse of FTX in 2022 did not merely damage crypto confidence. It reinforced institutional demand for regulated, audited venues at a structural level. Governance and compliance requirements that were already present became non-negotiable. For an investor evaluating exchange stocks, the relevant question is not whether a competitor can launch a similar product, but whether it can replicate the liquidity, regulatory standing, and data infrastructure simultaneously. The historical record says no entrant has managed all four.

The CFTC Designated Contract Market requirements establish the registration, compliance, and operational standards that any new entrant must satisfy before accessing institutional flow, a regulatory bar that the post-FTX environment has raised rather than lowered.

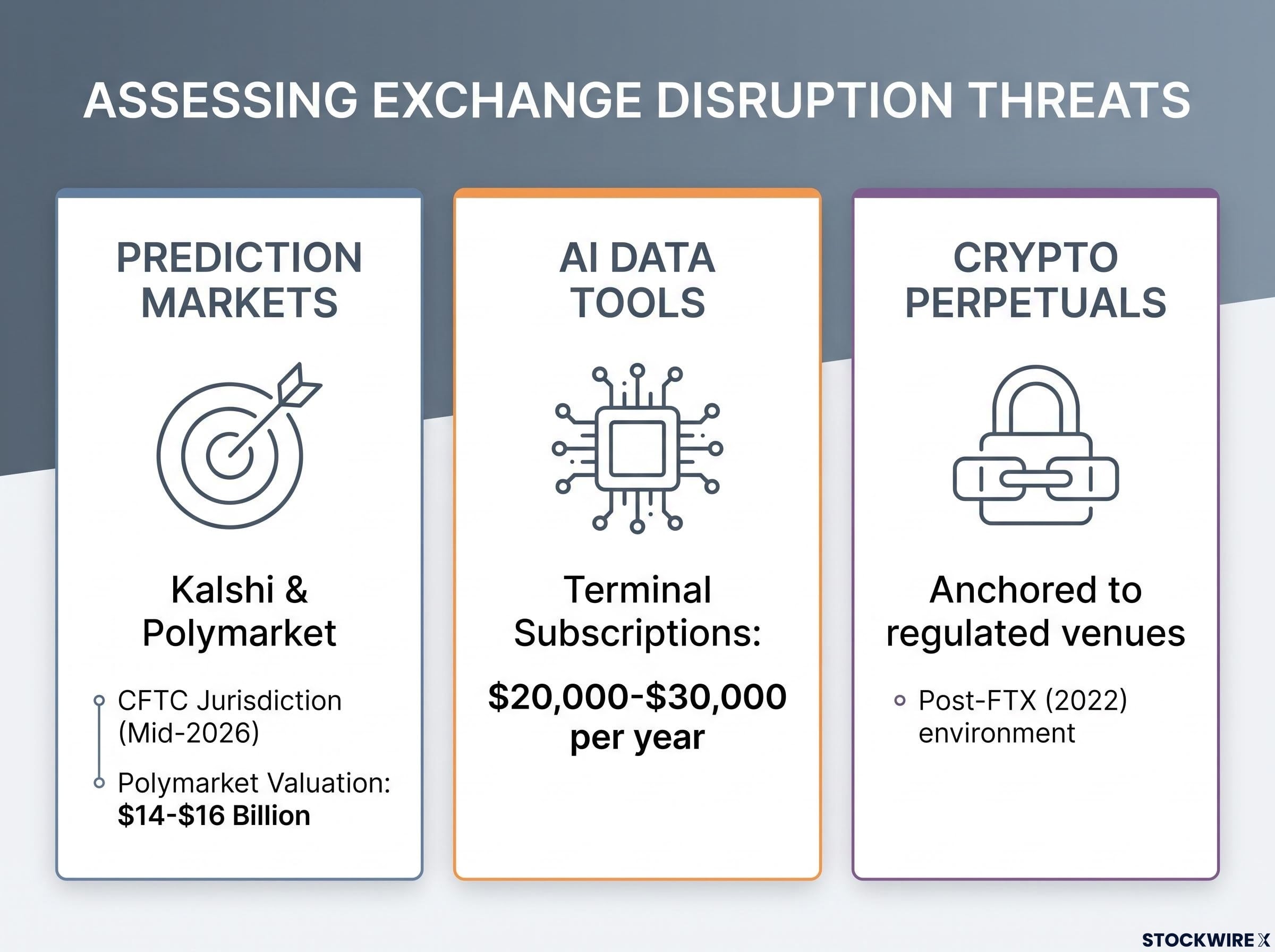

Where the disruption narrative has real teeth, and where it does not

Granting that exchange moats are durable does not mean every disruption vector is toothless. The analytical task is distinguishing where pressure is real from where it is misapplied.

Prediction markets are attracting genuine institutional experimentation. Kalshi and Polymarket both operate under CFTC jurisdiction as of mid-2026, and institutions are exploring event contracts for macro and policy hedging. That is real. But volumes remain negligible compared to NYSE or CME, the outsized presence of well-informed participants means retail traders are systematically on the wrong side of these markets, and Polymarket’s private valuation of approximately $14-$16 billion would represent a manageable acquisition cost for a major exchange. The institutional track is developing; the existential threat is not.

AI-native data tools present a more specific distinction that investors routinely conflate. Exchange data businesses sit on irreplaceable proprietary order flow. Third-party terminal vendors, whose aggregation and analytics layers face real margin compression from AI-native platforms, are a different business. Terminal subscriptions run $20,000-$30,000 per year for institutional users, a cost that is economically immaterial relative to the capital being deployed, which removes the switching incentive. If you own exchange stocks, AI disruption to terminal economics is not the same as AI disruption to the exchange’s underlying data revenue, and conflating the two is a mispricing opportunity.

Crypto perpetual futures have credible advocates arguing that equity perpetuals represent a structural shift. The counter-argument deserves acknowledgment. But institutional capital continues to be directed toward regulated venues, anchored there by governance frameworks, risk management protocols, and regulatory alignment obligations that the post-FTX environment has tightened rather than loosened.

Crypto regulatory enforcement trends matter to exchange investors precisely because tighter compliance regimes across major markets have redirected institutional flow toward regulated venues, reinforcing the post-FTX dynamic that has structurally benefited exchange incumbents at the expense of unregulated platforms.

- Prediction markets: Real institutional experimentation under CFTC jurisdiction, but negligible volumes versus incumbent exchanges and acquisition-sized valuations

- AI data tools: Genuine margin pressure on third-party terminal vendors, but exchange proprietary data businesses are structurally distinct and protected

- Crypto perpetuals: Credible structural shift argument, but institutional flow remains anchored to regulated venues by governance requirements

Exchange venues accumulate order book data across trillions of dollars of buy and sell side transactions, a body of information that publicly available sources cannot come close to replicating.

MIAX valuation, catalysts, and what the discount actually reflects

MIAX trades at approximately 13x forward EBITDA against mid-teens multiples for NASDAQ and CME. The discount exists. The question is whether it reflects genuine weakness or a combination of transient and addressable factors.

Three sources explain the gap. The litigation overhang from an ongoing NASDAQ lawsuit, paired with a large cash reserve that some analysts interpret as settlement preparation, suppresses the multiple. Size and float constraints limit buyback activity. Business mix differs from larger peers. The first factor is potentially resolution-driven. The second is structural but not value-destructive. The third is a composition question, not a quality question.

The mechanics driving valuation multiples, particularly the sensitivity of forward earnings-based multiples to discount rate assumptions and the distinction between current profitability and priced-in growth, are what make the MIAX discount versus peers analytically interpretable rather than a simple buy or sell signal.

Year-to-date performance adds context. CBOE is down approximately 1%, CME down roughly 4%, NASDAQ down approximately 13%, and ICE down nearly 20%. MIAX is positive on the year, with particular strength in energy volatility trading. That performance differential is not noise; it reflects a business mix well-positioned for the current volatility and energy environment, and investors evaluating the discount should weigh that context before concluding the gap is permanent.

| Exchange | Forward EBITDA multiple | YTD performance (approx.) | Distinguishing characteristic |

|---|---|---|---|

| MIAX | ~13x | Positive | Energy volatility strength; Onyx technology platform |

| CBOE | Mid-teens | Down ~1% | VIX franchise and options dominance |

| CME | Mid-teens | Down ~4% | Broadest derivatives product suite globally |

| NASDAQ | Mid-teens | Down ~13% | Market technology and index licensing revenue |

| ICE | Mid-teens | Down ~20% | Energy and fixed income data dominance |

Onyx and Bloomberg 500 as re-rating catalysts

Onyx, MIAX’s proprietary options trading platform, processes trades several milliseconds faster than competing systems and is already licensed to exchanges globally. This is infrastructure-toll revenue: recurring, sticky, with margin characteristics more typical of software than transactional exchange revenue. If Onyx licensing scales, it supports a re-rating of the earnings mix, though execution risk around that scaling remains genuine and requires a five-year horizon to assess.

The Bloomberg 500 index partnership captures a different kind of value. Unlike the S&P 500, which requires a minimum one-year seasoning period for inclusion, the Bloomberg 500 incorporates newly public companies more rapidly. For MIAX as the host exchange, this means commission revenue on all related trading volume, including mechanically forced quarterly rebalancing flows, without directional exposure to the underlying securities. NASDAQ is pursuing a similar faster-inclusion index product, which serves as competitive validation of the approach.

Under moderately conservative growth assumptions, the price target range sits at approximately $80-$100 per share by end of the decade. Under a 40% revenue growth scenario, upside would be materially above that base case.

The next major ASX story will hit our subscribers first

Primary risks to the exchange investment thesis

The bull case requires the same rigour applied to risk.

- Litigation overhang: The ongoing NASDAQ lawsuit and the large cash reserve interpreted as potential settlement preparation create binary outcome risk. This is the most legible risk because it is resolution-driven. What to watch: any settlement announcement, cash reserve changes, or legal filing developments.

- Non-patentability as a two-edged sword: The same dynamic that lets MIAX replicate competitors also lets CME and NASDAQ replicate MIAX products. Larger balance sheets and regulatory relationships amplify this risk asymmetrically. What to watch: larger peers launching competing products in MIAX’s strongest verticals.

- Acquisition risk: A premium takeover removes the opportunity to compound at projected rates, which is a nuanced concern rather than a traditional downside event. What to watch: unusual options activity, proxy filing changes, or strategic review announcements.

- Prediction market maturation: If platforms like Kalshi and Polymarket scale into institutional-grade venues under improving CFTC regulatory clarity, the threat assessment changes materially. What to watch: institutional AUM reported in prediction market products and any expansion of CFTC-approved event contract categories.

The litigation overhang is binary and trackable. The non-patentability risk is more structurally interesting because it sets a ceiling on how deep any single exchange’s moat can ultimately become. Understanding which risks you are being compensated for (the valuation discount covers litigation) versus which require conviction (the five-year horizon, catalyst execution) is how you size a position.

What the exchange investment case actually requires you to believe

The arguments have been laid out. Here is what conviction actually looks like in practice, framed as four explicit beliefs with the evidence that supports or complicates each one.

- Absorption continues: You need to believe that the historical pattern of exchanges absorbing challengers persists through the current cycle. The moat structure and the CME spring wheat example support this. The complication is that three disruption vectors arriving simultaneously is unprecedented, even if each individual vector has historical precedent.

- The MIAX discount resolves: You need to believe that the valuation gap versus peers narrows as litigation concludes and Onyx and Bloomberg 500 contribute meaningfully to revenue. The litigation is binary; the catalyst execution is not guaranteed.

- The five-year horizon holds: You need to believe you can hold through volatility while Onyx licensing revenue and Bloomberg 500 trading volume scale. The price target range of approximately $80-$100 per share by end of the decade requires patience and tolerance for interim drawdowns.

- Disruption threats remain marginal to institutional flow: You need to believe that CFTC regulation and institutional governance requirements continue to anchor large-scale flow to regulated venues. The post-FTX environment currently supports this, but regulatory frameworks evolve.

Investors wanting to stress-test the disruption narrative against peer-level operational data will find our deep-dive into exchange sector mispricing useful, which examines how CME and ICE have absorbed prior disruption cycles while compounding at 15-18% annualised across multiple rate environments.

What to monitor as new information arrives: Onyx licensing revenue trajectory, Bloomberg 500 trading volume, NASDAQ litigation developments, and any material change in institutional adoption of prediction market products.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Price targets and growth projections are speculative and subject to change based on market developments and company performance.