Why Goldman Sees AI Infrastructure Leading a 21x Market

2 hrs ago

Barclays strategist Emmanuel Cau published a cross-asset scenario analysis on 27 May 2026 identifying a potential Iran peace agreement as a catalyst capable of triggering a broad market rally, even as equity valuations look stretched by conventional measures. The research note arrives at a moment of tension between caution and opportunity: investor sentiment is guarded, short positioning remains thin, and long-only fund inflows have slowed to their weakest since January 2026. European equities, battered by an energy price shock, have underperformed sharply. The combination means a single geopolitical catalyst could release substantial repositioning energy across equities, bonds, and currencies simultaneously. What follows is a breakdown of the specific market mechanics behind the Barclays thesis, which asset classes and regions stand to benefit most, what the current state of investor positioning means for the magnitude of any move, and what conditions would need to materialise for the scenario to play out.

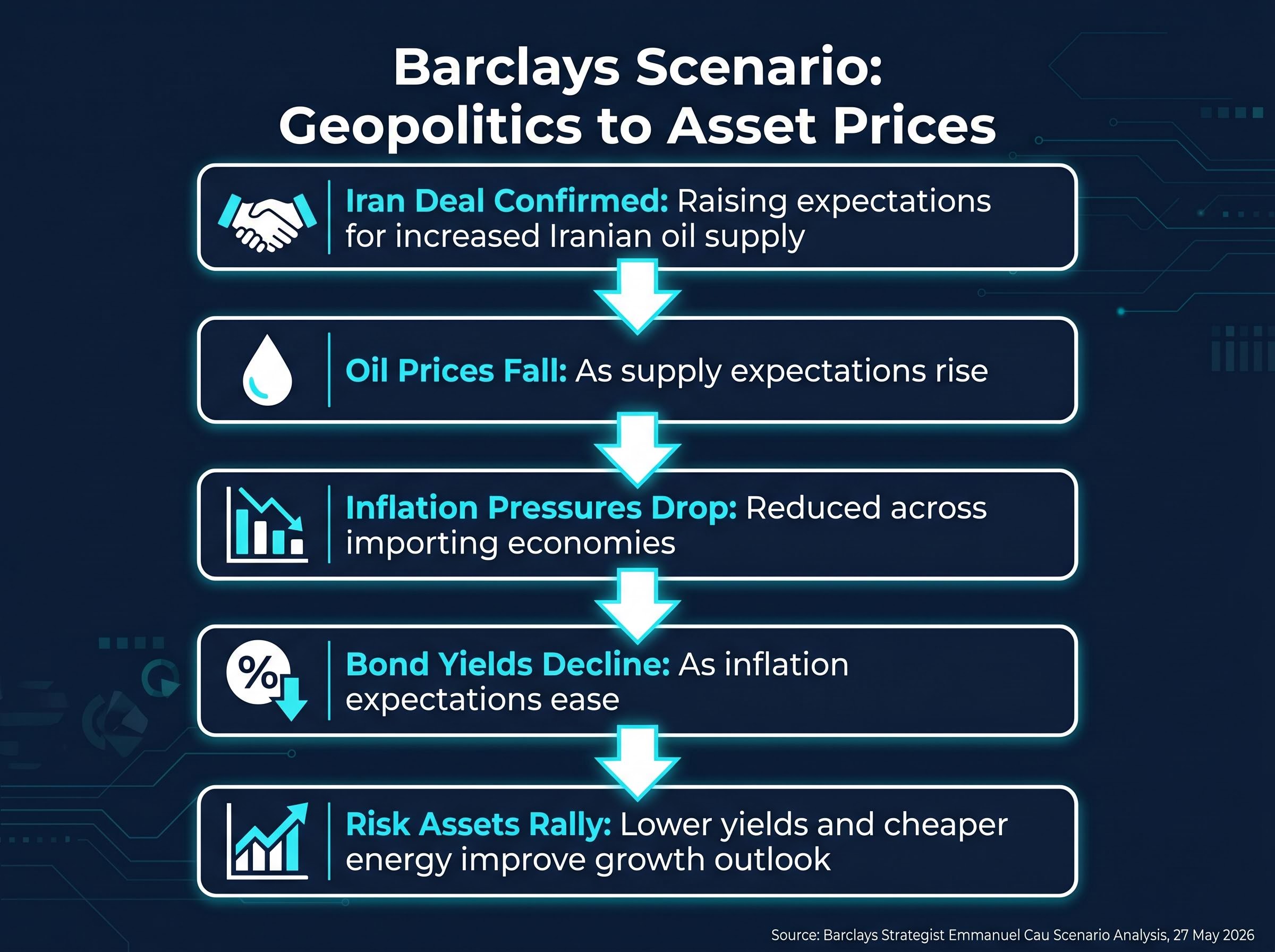

A diplomatic negotiation might seem like political news. Barclays is treating it as a market event because of a direct transmission mechanism that connects geopolitics to asset prices.

The relationship between geopolitical risk and stock market behaviour is more nuanced than headline-driven intuition suggests: markets process diplomatic events as probability-adjusted inputs to future earnings, which is why the same shock can produce a sharp sell-off in one context and near-total indifference in another.

The logic runs in a clear sequence:

This is not theoretical framing. Bloomberg market data from late May 2026 shows that easing geopolitical tensions coincided with lower oil prices and rising global equities, a pattern directionally consistent with the Barclays thesis.

Cau’s analysis is explicitly conditional. No Iran deal has been confirmed as of 27 May 2026, and the Barclays note reads as scenario planning around a prospective event rather than a forecast of an imminent agreement. The value of the research lies in mapping what would happen across asset classes if such a catalyst were to arrive, and why the current market setup makes the potential impact larger than investors might assume.

European equities have not underperformed by accident. The energy price shock has transmitted directly into weaker economic activity across the region, driving accelerating capital outflows and widening the performance gap relative to US markets.

European equity valuations have compressed from approximately 18x to 14.4x forward earnings since January 2026, a repricing Goldman Sachs attributes primarily to multiple compression driven by the oil shock rather than broad earnings deterioration, which leaves the valuation floor exposed to the same energy cost mechanism that drove it lower.

According to Barclays, investor allocations remain heavily tilted toward US equities, with the US-versus-Europe positioning trade significantly skewed in favour of American assets. Capital outflows from European markets have been picking up pace as the energy shock feeds through into softer growth data.

The result is a region where positioning has been, in Barclays’ characterisation, largely cleared out.

Barclays views European positioning as having been largely cleared out, a setup the bank identified as capable of producing a meaningful reversal if energy prices decline.

That cleared positioning is precisely what makes Europe the highest-beta beneficiary of any oil-price reversal. A deal that pushes oil lower would directly address the primary headwind driving outflows, while the absence of crowded long positions means even modest good news could trigger disproportionate repositioning flows.

The dynamic is asymmetric. Sentiment among investors is cautious, yet few are willing to establish outright short positions against European equities. The market is not positioned for a sharp downside move, but neither is it positioned for upside.

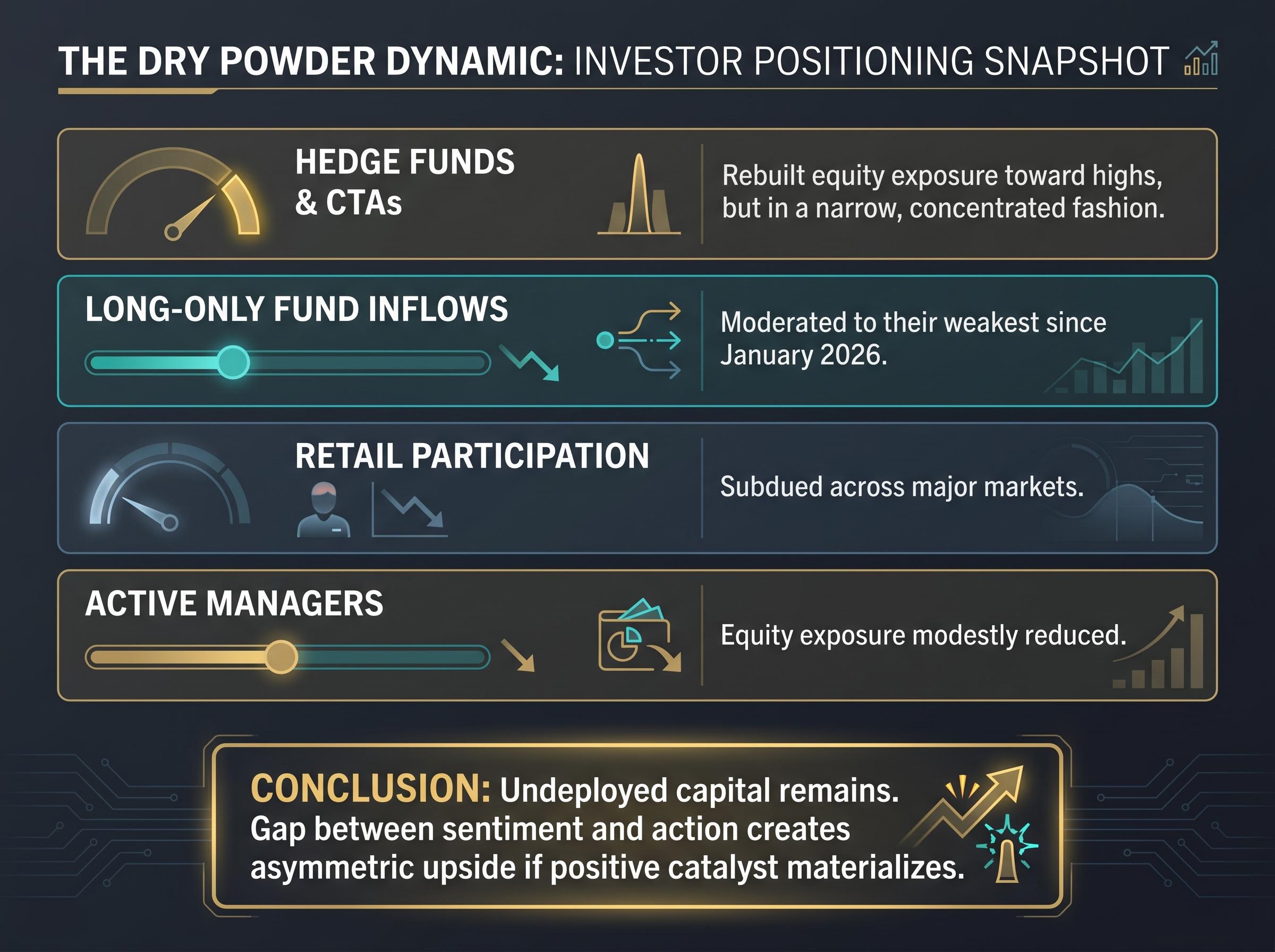

Long-only fund inflows moderated to their weakest since January 2026, per Barclays, indicating capital sitting on the sidelines rather than actively deployed against Europe. That sidelined capital represents latent buying power. If a positive catalyst materialises, the lack of existing long exposure means the repositioning flow into European equities could be larger and faster than the prevailing sentiment would suggest.

The Barclays scenario extends well beyond European equities. Cau identified emerging market equities and bonds, Japanese equities, and bond markets broadly as beneficiaries of a lower-oil environment, each connected to the same transmission mechanism.

For emerging markets, lower oil prices would reduce import costs for energy-dependent economies while easing inflationary pressure, creating room for central banks to hold or cut rates. That combination supports both equity valuations and bond prices. For Japan, the logic is similar: as a major oil importer, cheaper energy improves the corporate cost structure and supports consumer spending.

Bond markets broadly would benefit from reduced inflation expectations feeding into lower yields.

The cross-asset repricing mechanics at work in 2026 are unusually direct: the ECB’s chief economist explicitly linked the oil shock to potential rate hikes in May, Asian equity markets registered broad synchronised declines as energy costs escalated, and China’s April retail sales data of just 0.2% year-on-year introduced a stagflationary undercurrent that complicates the clean bond rally Barclays projects in a resolution scenario.

Bloomberg’s observed market behaviour in late May 2026, where easing geopolitical tensions coincided with lower oil prices and rising global equities, is directionally consistent with these mechanics. Specific yield movement or price-level estimates for emerging markets and Japan are not available from current named-source reporting, though the general direction is well supported.

| Asset Class / Region | Direction of Impact | Primary Driver | Sourcing Confidence |

|---|---|---|---|

| European equities | Positive | Energy cost relief, repositioning flows | Named Barclays sourcing |

| Emerging market equities and bonds | Positive | Lower oil import costs, reduced inflation | Barclays direction; no quantified estimates |

| Japanese equities | Positive | Cheaper energy input costs, yield support | Barclays direction; no quantified estimates |

| Bond markets broadly | Positive | Lower inflation expectations, falling yields | Barclays direction; general market logic |

The question most scenario analyses leave unanswered is not which direction markets would move, but how far. Barclays’ positioning data offers an answer.

Cau found that cross-asset positioning has not reverted to pre-conflict levels despite stretched equity valuations. That gap between price and positioning means residual dry powder remains available to amplify any rally triggered by a geopolitical catalyst.

The positioning snapshot is specific:

Barclays identified a divergence between sentiment and action: investors are worried, but few have positioned defensively. That gap creates asymmetric upside if a positive catalyst materialises.

This divergence is what transforms the Iran deal scenario from a directional hypothesis into a potentially outsized market event. When capital is sidelined rather than short, a positive shock does not need to overcome bearish positioning; it simply needs to give cautious capital a reason to re-enter. The concentrated nature of existing hedge fund exposure adds further amplification risk, as broadening participation could drive a move beyond what narrow positioning would ordinarily produce.

The Barclays analysis is scenario planning, not a forecast. As of 27 May 2026, no named-source reporting confirms that Iran negotiations are active, approaching conclusion, or have produced an agreement.

For the thesis to play out, three conditions would need to materialise in sequence:

The diplomatic backdrop includes active discussion of US sanctions relief proposals to Iran, with reported offers covering oil waivers as part of a broader framework aimed at extending a ceasefire and opening wider negotiations, the specific terms of which would determine how quickly Iranian supply could reach global markets.

Each step carries its own risk. A deal that fails to materialise or stalls in negotiation would leave the energy shock in place, continuing to weigh on European growth. If positioning gradually normalises over time without a catalyst, the dry powder argument weakens as sidelined capital finds other destinations.

There is also the question of how much has already been priced. Bloomberg’s observation that markets responded positively to easing geopolitical tensions in late May 2026 raises the possibility that some portion of the scenario is already reflected in current prices.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements are speculative and subject to change based on market developments and geopolitical conditions.

Cau’s analysis demonstrates that a single geopolitical catalyst, operating through the oil-price mechanism, could unlock coordinated repositioning across equities, bonds, and currencies. The potency of the scenario rests on three conditions converging: the direct oil transmission channel that links an Iran deal to risk asset relief, European positioning that has been cleaned out to the point where modest good news could trigger disproportionate flows, and undeployed dry powder across asset classes that has not reverted to pre-conflict levels.

For investors, the monitoring implication is straightforward. Credible signals from any Iran-related diplomatic process would serve as a leading indicator for the cross-asset moves Barclays has mapped. The scenario remains prospective rather than confirmed, but the positioning setup means the gap between “nothing happens” and “something happens” could be wider than conventional analysis suggests.

Investors wanting to translate the Barclays scenario into a concrete positioning framework will find our dedicated guide to the barbell strategy for an oil-down rotation, which walks through Alpine Macro’s equal-weighted approach pairing long AI and technology with long Old Economy cyclicals, the historical precedents from the 2014-2015 and 2020 oil declines, and the specific sectors that have outperformed when crude prices fall sustainably.

Barclays strategist Emmanuel Cau published a cross-asset scenario analysis on 27 May 2026 arguing that a confirmed Iran peace agreement could trigger a broad market rally by pushing oil prices lower, easing inflation, reducing bond yields, and releasing sidelined capital into risk assets.

A confirmed Iran agreement would raise expectations of increased Iranian oil supply reaching global markets, pushing oil prices lower, which reduces inflationary pressure across importing economies, supports lower bond yields, and improves the growth outlook for equities.

Barclays identified European equities as the highest-beta beneficiary due to cleaned-out positioning and energy-cost sensitivity, with emerging market equities and bonds, Japanese equities, and bond markets broadly also expected to benefit through lower oil import costs and reduced inflation.

Barclays found that hedge fund and CTA equity exposure is concentrated rather than broad, long-only fund inflows moderated to their weakest since January 2026, retail participation is subdued, and residual undeployed dry powder remains available to amplify any rally triggered by a positive geopolitical catalyst.

Three sequential conditions are required: a credible de-escalation signal or confirmed Iran agreement, an actual oil price decline large enough to relieve inflationary pressure, and repositioning flows moving into European equities and other beneficiary asset classes.