Why Goldman Sees AI Infrastructure Leading a 21x Market

50 mins ago

When AI data centre operators face power constraints so severe that they cannot wait for grid connections, they turn to a company that spent 25 years being largely overlooked by Wall Street. When they need to store the vast outputs of inference workloads without a continuous power draw, they turn to NAND flash memory from a firm that only recently regained its independence. Neither Bloom Energy nor Sandisk fits the conventional image of an AI stock, yet both have more than doubled in 2026 year-to-date and are reporting triple-digit revenue growth in a sector the market was slow to recognise.

The AI investment narrative has concentrated heavily on chip designers, hyperscaler cloud platforms, and frontier model developers. That concentration has left a meaningful gap in public understanding of where AI capital expenditure physically lands, specifically in the unglamorous categories of energy delivery and non-volatile storage that make large-scale inference and training possible. This analysis examines the structural reasons why power and storage have become breakout investment categories in 2026, uses Bloom Energy and Sandisk as detailed case studies, and explains what the pattern signals about how infrastructure-cycle investing works during a technology buildout.

AI training and inference workloads require continuous, high-density power and large-scale non-volatile storage at a level that existing data centre infrastructure was never designed to provide. Grid connection timelines are measured in years; NAND capacity requirements are measured in exabytes. These are physical constraints that software solutions cannot substitute away.

The scale of AI infrastructure investment now underway represents a capital reallocation unlike anything in the technology sector’s recent history, with Wall Street projecting $530 billion to $700 billion in global IT data centre spending for 2026 alone, the majority of which is landing in physical assets rather than software licences.

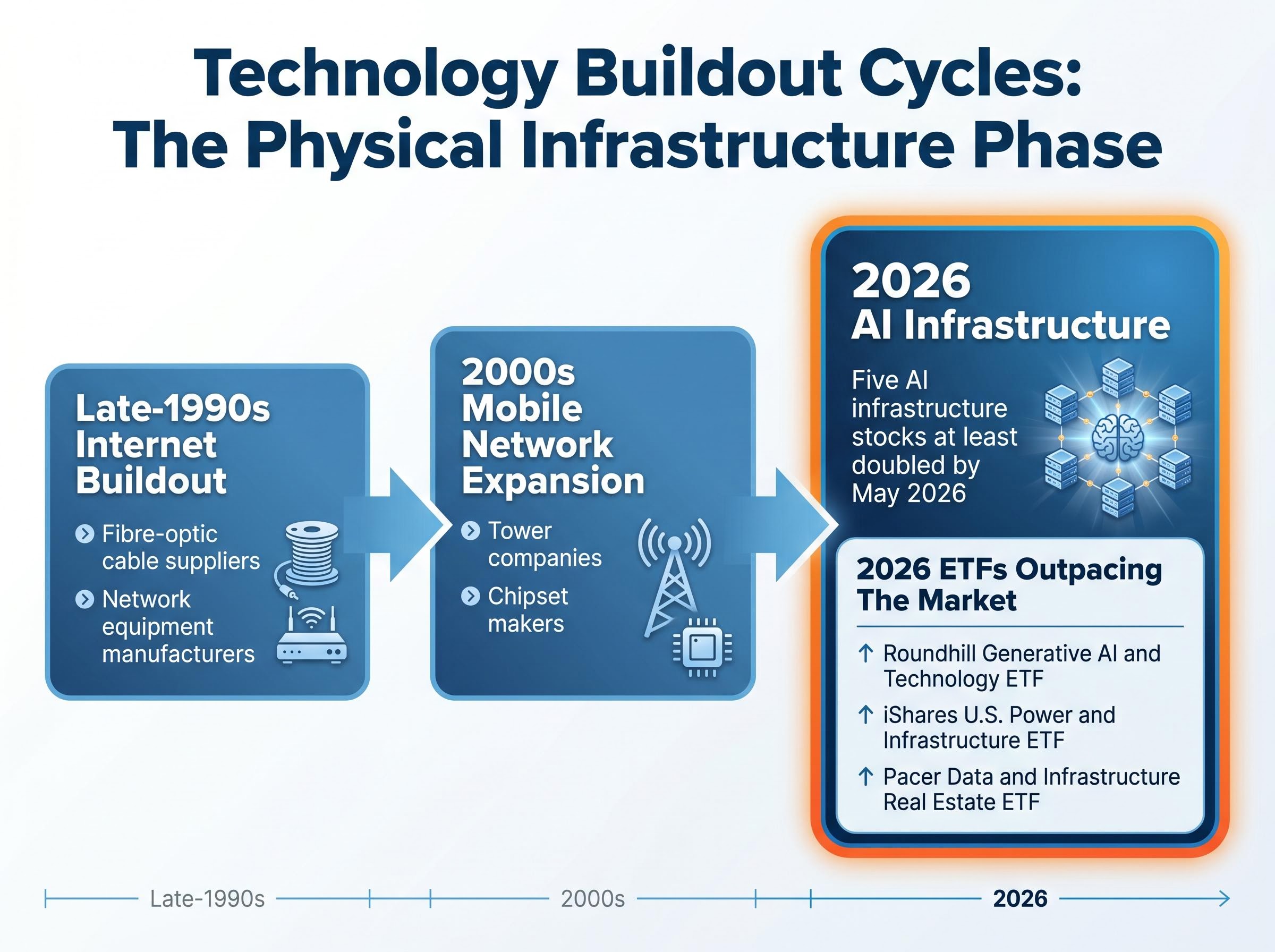

The pattern is not new. The late-1990s internet buildout rewarded fibre-optic cable suppliers and network equipment manufacturers before it rewarded the portals that ran on their infrastructure. The 2000s mobile network expansion delivered outsized returns to tower companies and chipset makers before the app economy matured. In each case, picks-and-shovels suppliers captured disproportionate value during the buildout phase precisely because their scarcity was physical.

The market is recognising the pattern in real time. Several AI-focused ETFs are outpacing even the Nasdaq-100 year-to-date in 2026, itself already ahead of the S&P 500:

Five AI infrastructure stocks had each at least doubled by May 2026, within the first five months of the year, according to analysis by Jennifer Saibil, The Motley Fool (17 May 2026).

The outperformance is concentrated, and it is landing in the companies that supply the physical inputs AI cannot function without.

The business logic comes first: a hyperscaler planning a new AI training cluster needs megawatts of continuous power, and it needs that power operational within months, not the three-to-five-year timeline a new utility grid connection typically requires. Bloom Energy’s standalone energy servers, powered by its proprietary fuel cell technology, operate independently of the traditional electrical grid. That independence compresses deployment timelines from years to months.

For most of its 25-year history, Bloom served a broad customer base across retail, aerospace, and general enterprise. The AI buildout has reoriented the business decisively. The financial results reflect that reorientation not merely as revenue acceleration, but as a qualitative shift from chronic losses to genuine profitability.

Research aggregating data from the IEA, BloombergNEF, and PJM Interconnection on AI data centre grid connection timelines finds that only 20% of projects in the US interconnection queue ever reach operation, with a five-year median wait, a constraint that makes off-grid fuel cell deployment commercially compelling for any operator that cannot defer capacity by half a decade.

| Metric | Prior Period | Q1 2026 | Change |

|---|---|---|---|

| Revenue growth (YoY) | Baseline | 130% | N/A |

| Net income | Loss-making | $70 million | First-time profitability |

| Operating cash flow | Negative | $73.6 million | +$184.3 million swing |

| FY2026 revenue guidance | +60% (prior) | +80% (revised) | Upward revision |

The operating cash flow swing of $184.3 million, moving from negative to $73.6 million positive in a single quarter, signals that Bloom has crossed from growth-stage speculation into a business generating real returns.

The company’s market capitalisation stands at approximately $86 billion, with a 52-week trading range of $18.12 to $322.83 (note: readers should verify this figure against current filings, as it originates from a single source). Full-year 2026 revenue guidance was revised upward from a projected 60% increase to an anticipated 80% increase. For commercially oriented investors, the profitability inflection carries more weight than the revenue growth rate alone; it indicates that the AI demand surge is converting into durable unit economics, not simply higher-cost scaling.

The physical property that makes NAND flash valuable for AI workloads is straightforward: it retains stored data without requiring a continuous power supply. This is what “non-volatile” means in storage terminology: data persists even when the device is powered off.

Three properties make NAND flash structurally suited to large-scale AI storage:

Sandisk operates as a focused NAND flash company following its re-establishment as an independent entity, concentrating capital and engineering on the single storage category experiencing the most acute demand from AI data centre operators.

Traditional enterprise storage is designed for transactional read/write patterns with moderate volume: a database handling customer records, for instance, with bursty activity during business hours. AI inference operates on a fundamentally different model. Serving model outputs to users continuously requires low-latency retrieval of model weights and intermediate outputs at far greater density, around the clock, with no quiet periods.

This structural difference means that the current surge in NAND demand is not purely cyclical. It is tied to the long-term growth of AI deployment at the application layer. As more AI-powered services enter production, each one generates persistent, high-throughput storage requirements that compound rather than replace the prior quarter’s demand.

The memory chip supercycle now unfolding differs from prior DRAM upcycles in one critical respect: agentic AI, AI-capable smartphones, and automotive ADAS are broadening demand well beyond the hyperscaler tier, which means the storage intensity compounding described above is occurring simultaneously across every layer of the hardware stack rather than in a single demand category.

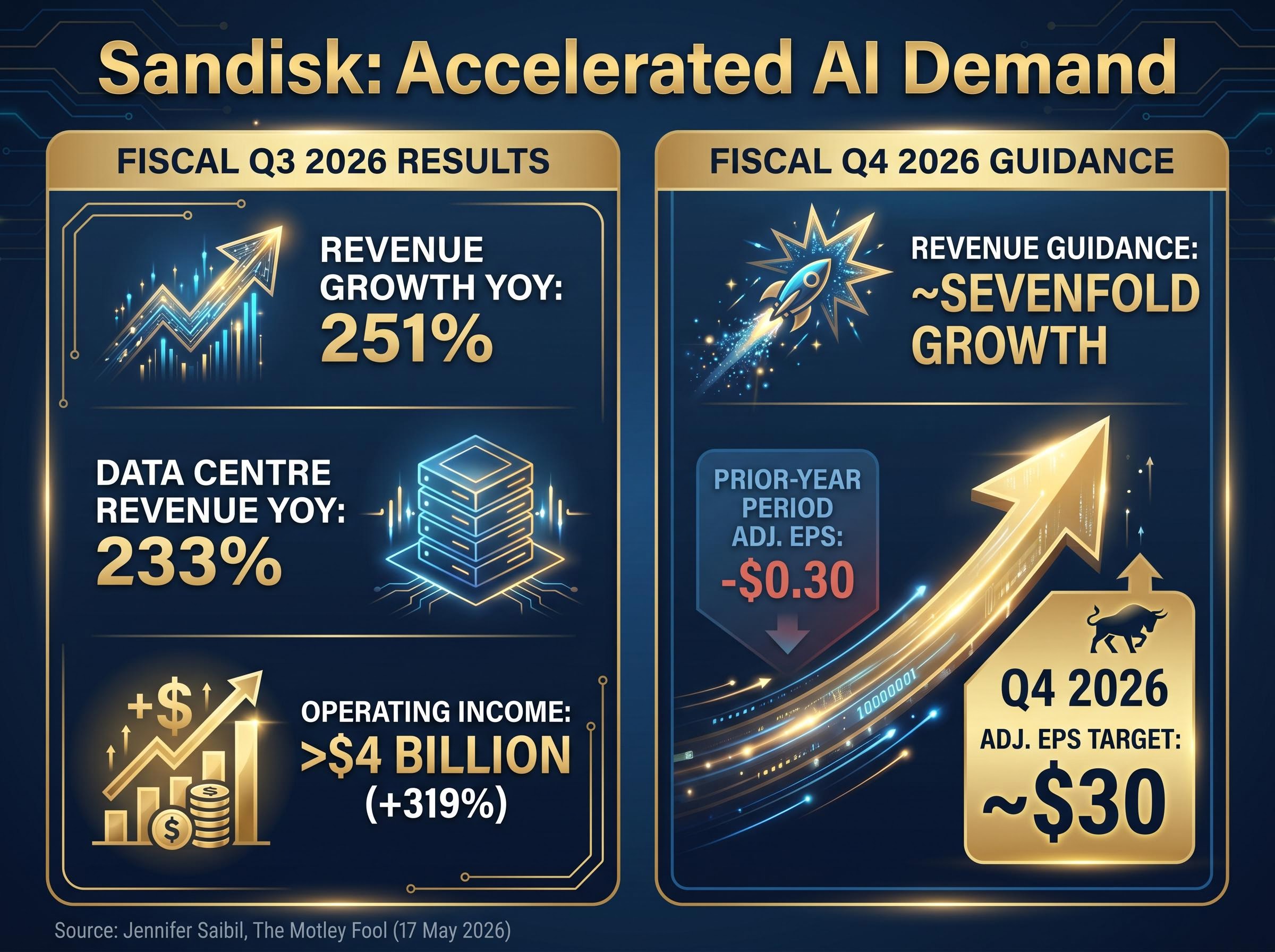

Sandisk’s fiscal Q3 2026 results (quarter ended 3 April 2026) reflect this dynamic: revenue grew 251% year over year, with data centre revenue specifically rising 233%. Management guided for approximately sevenfold revenue growth in fiscal Q4 2026.

The revenue figures are striking, but the operating leverage story is where the analytical weight falls. Sandisk’s fiscal Q3 2026 operating income expanded 319% to exceed $4 billion. That margin expansion indicates a business that has moved past the investment phase and is converting demand into profits at an accelerating rate.

The memory sector repricing now underway reflects something more durable than a standard inventory recovery: hyperscalers are locking in multi-year NAND supply contracts rather than purchasing on spot markets, a structural procurement shift that reduces the boom-bust volatility that characterised prior cycles and supports the operating leverage visible in Sandisk’s margin expansion.

| Metric | Fiscal Q3 2025 | Fiscal Q3 2026 | Change |

|---|---|---|---|

| Revenue growth (YoY) | Baseline | 251% | N/A |

| Data centre revenue (YoY) | Baseline | 233% | N/A |

| Operating income | Prior-year level | >$4 billion | +319% |

| Adj. EPS (FQ4 guidance) | -$0.30 | ~$30 | Qualitative shift |

Adjusted EPS guidance of approximately $30 for fiscal Q4 2026, compared to a loss of $0.30 per share in the prior-year period. That is not a marginal improvement; it is a qualitative shift in business economics.

Management guided for approximately sevenfold revenue growth in fiscal Q4 2026, suggesting the demand trajectory is steepening rather than plateauing. All figures are sourced from Sandisk management guidance as reported by Jennifer Saibil, The Motley Fool (17 May 2026). Readers should note that no independently verified stock price or year-to-date return figure for Sandisk was confirmed in the available research base; current share price data should be sourced directly at time of reading.

For commercially oriented investors, the EPS swing from negative to $30 is the single most significant data point in this analysis. It indicates that Sandisk has passed through the capital-intensive phase of its business cycle and entered a period of genuine earnings power.

Bloom Energy and Sandisk operate in different categories and serve different functions, yet they share three structural characteristics that define infrastructure-cycle winners:

Five AI infrastructure stocks had each at least doubled by May 2026, and ETF-level data (including the iShares U.S. Power and Infrastructure ETF and the Pacer Data and Infrastructure Real Estate ETF) confirms that passive allocation vehicles are also recognising the theme. This is a sector-level phenomenon, not individual stock-selection success.

Niche suppliers in infrastructure cycles often outperform platform companies during the buildout phase for a specific reason: platform companies compete on software ecosystems and scale; niche infrastructure suppliers compete on physical scarcity. When the constraint is physical, pricing power accrues to the supplier with capacity, not the one with the best algorithm.

No competitive landscape data for either Bloom Energy or Sandisk was available from named sources as of May 2026. This represents a material gap: investors cannot assess the durability of either company’s market position without understanding who the emerging challengers are in fuel cell power and NAND flash.

Investors wanting to assess the durability of Sandisk’s market position will find our full explainer on memory chip competitive dynamics covers the Samsung labour strike risk, HBM supply sold-out conditions, and US-China trade policy variables that shape the near-term pricing environment across the NAND and DRAM sectors.

No independent risk, regulatory, or analyst downgrade data was available for either company. The financial figures cited in this analysis originate from a single source (Jennifer Saibil, The Motley Fool, 17 May 2026). Readers should verify current stock prices, market capitalisation figures, and year-to-date returns independently before drawing investment conclusions.

The structural demand thesis for both companies is well-supported by the available data. Grid connection constraints will persist for years. AI inference storage requirements will compound as more applications enter production. These are durable demand drivers, not one-quarter anomalies.

The valuation question is harder to resolve. Stocks that have already doubled or more in five months are pricing in significant future growth. Bloom Energy’s 52-week trading range of $18.12 to $322.83 (to be verified independently) illustrates the volatility this category carries. Five AI infrastructure names had already doubled by May 2026, suggesting that much of the initial recognition move may be complete.

The infrastructure thesis is structurally sound. The question is whether current prices already reflect it, and this analysis, limited by the absence of competitive, regulatory, and risk-adjusted data, cannot fully answer that.

Both companies’ management guidance figures are forward-looking and subject to revision based on market conditions and execution. Past performance does not guarantee future results.

AI infrastructure spending is not abstract. It lands in kilowatts of off-grid power and exabytes of non-volatile storage, and the companies supplying those inputs are generating some of 2026’s most extraordinary revenue growth. Bloom Energy and Sandisk illustrate how a technology buildout rewards the suppliers of physically scarce inputs before it rewards the platforms that consume them.

The due diligence that follows logically from this analysis involves three steps: verify current valuations against independent financial data providers, research the competitive dynamics this article could not cover, and assess management guidance credibility across multiple reporting cycles before forming a position. The categories that appear unglamorous at the start of a technology buildout are often the ones that generate the most durable returns, because their scarcity is physical rather than replicable.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Readers interested in the broader AI data centre investment theme may find value in exploring related analysis on infrastructure ETF performance and hyperscaler capital expenditure trends, and in verifying the specific financial figures cited here against current company filings.

AI infrastructure stocks are companies supplying the physical inputs that AI data centres require, such as off-grid power and non-volatile storage. They are outperforming in 2026 because AI training and inference workloads have created acute demand for these physically scarce resources that cannot be substituted by software.

Grid connections for new data centres typically take three to five years to complete, and only 20% of projects in the US interconnection queue ever reach operation. Bloom Energy's standalone fuel cell servers operate independently of the grid, compressing deployment timelines from years to months for operators that cannot defer capacity.

NAND flash is a type of non-volatile storage that retains data without a continuous power supply, making it energy-efficient at scale. AI inference workloads require low-latency retrieval of model weights and outputs around the clock, creating persistent, high-throughput storage demand that compounds as more AI-powered services enter production.

Sandisk reported fiscal Q3 2026 revenue growth of 251% year over year, with data centre revenue specifically rising 233%, and operating income expanding 319% to exceed $4 billion. Management also guided for approximately sevenfold revenue growth in fiscal Q4 2026.

Stocks in this category that have already doubled or more within five months may already be pricing in significant future growth, leaving limited upside at current valuations. Investors should also note the absence of publicly available competitive landscape data for companies like Bloom Energy and Sandisk, and verify all financial figures independently before forming a position.