Micron Surges 9% After Guiding $6.4 Billion Above Consensus

2 hrs ago

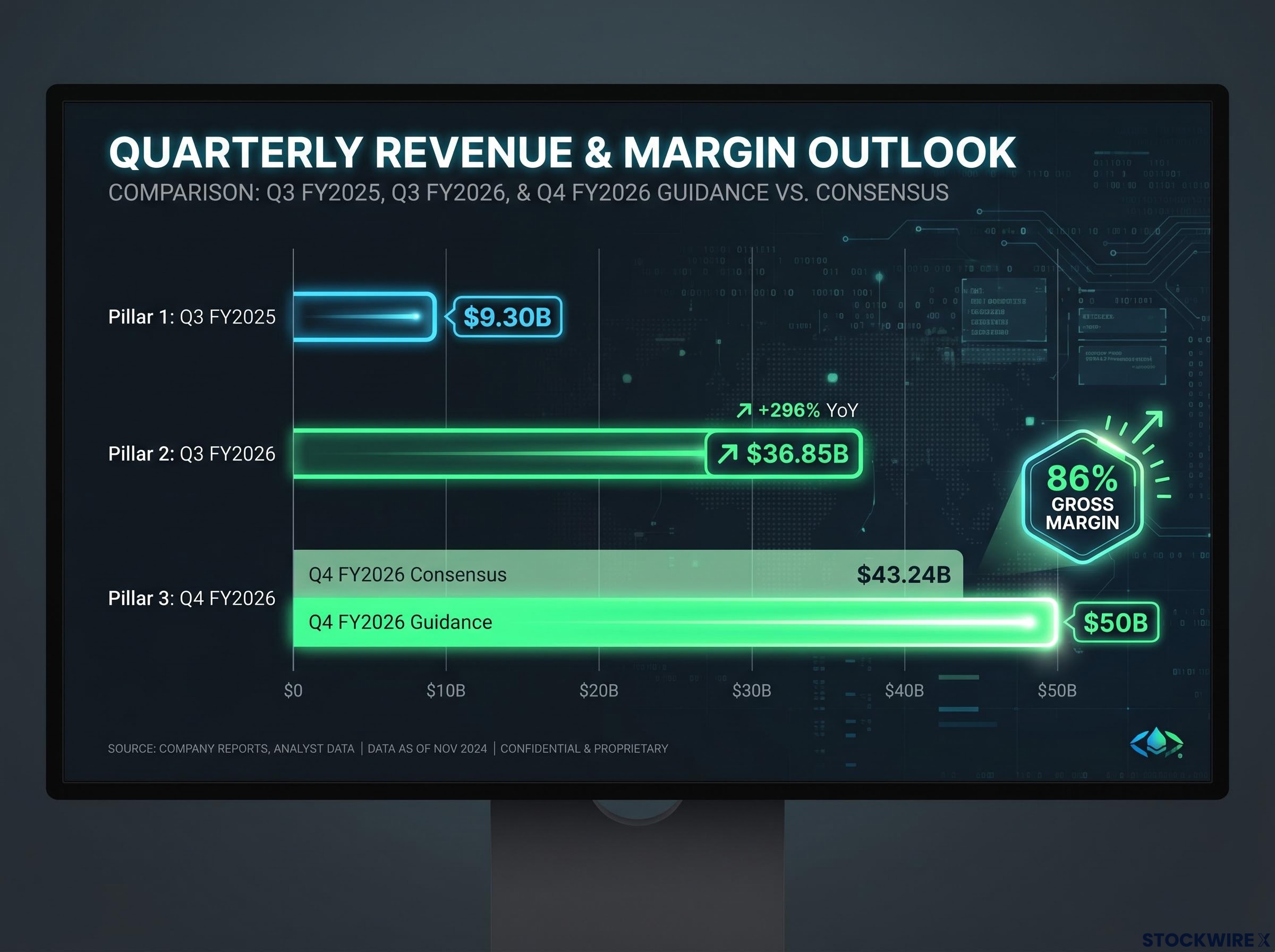

Micron Technology just posted quarterly revenue of $36.85 billion, guided to approximately $50 billion next quarter, and watched its stock surge more than 12% after hours. Those numbers do not belong to a memory chip company. Or rather, they did not until now.

The results reflect a fundamental repricing of what the memory semiconductor business can produce when AI infrastructure spending reaches escape velocity. Micron beat consensus estimates on every key metric for Q3 FY2026 and then issued guidance so far above Wall Street projections that the standard analyst-versus-actual framing barely captures the distance between expectation and reality.

Here is what Micron reported, what is driving it, and what guidance at this scale tells you about where AI memory demand is heading. The question worth holding as you read is whether this is a cycle peak or something the industry has not seen before: a structural reset of the memory business model itself.

Start with the year-over-year comparison, because it is the single most striking number in the release. Micron reported $9.30 billion in revenue in Q3 FY2025. One year later, the same quarter produced $36.85 billion. That is roughly a fourfold increase in twelve months, a trajectory that does not describe a cyclical uptick. It describes a business that has been structurally transformed by the scale of demand it is serving.

The Q3 FY2026 figure came in above analyst consensus of $35.69 billion, but the beat on revenue was almost secondary to the beat on profitability. The adjusted EPS figure of $25.11 cleared the consensus forecast of $20.49 by a margin that points to sell-side models having substantially misjudged how much pricing power Micron carried into the quarter.

The quarter saw $7.1 billion deployed in capital expenditure, while adjusted free cash flow came in at $18.3 billion. Shareholders will receive a quarterly dividend of $0.15 per share, with payment scheduled for 21 July. The cash generation at this scale, alongside sustained investment, tells you this is a company funding its own capacity expansion from operating cash flow rather than stretching its balance sheet to chase demand.

Micron’s official Q3 FY2026 earnings release confirms the non-GAAP diluted EPS of $25.11 and the Q4 FY2026 revenue guidance midpoint of $50 billion, providing the primary source documentation for the figures discussed across this report.

| Metric | Q3 FY2026 Reported | Analyst Consensus | Q3 FY2025 Comparable |

|---|---|---|---|

| Revenue | $36.85B | $35.69B | $9.30B |

| Adjusted EPS | $25.11 | $20.49 | — |

| Capital Expenditure | $7.1B | — | — |

| Adjusted Free Cash Flow | $18.3B | — | — |

| Quarterly Dividend | $0.15/share | — | — |

$50 billion. That is Micron’s revenue guidance for Q4 FY2026, with a range of $49 billion to $51 billion. Absorb the number on its own before the comparison, because the comparison makes it even harder to process.

Wall Street’s consensus estimate for Q4 was $43.24 billion. Management guided nearly $7 billion above that midpoint. For Q4 earnings, Micron set a diluted EPS range of $30.00 to $32.00, with the GAAP figure at $30.73 and the non-GAAP figure at $31.00, well ahead of the Street’s $25.31 expectation.

Then there is the gross margin figure: approximately 86%. That number has no precedent in DRAM and NAND manufacturing. Even during the strongest pricing environments in memory history, margins fell well short of this level. An 86% gross margin guided for a memory manufacturer signals something beyond cyclical pricing power; it tells you Micron’s AI-oriented products have moved into a pricing regime that resembles supply-constrained scarcity more than a commodity memory market.

The memory chip price trajectory through 2028, confirmed by S&P Global Ratings, shows that Samsung, SK Hynix, and Micron have collectively redirected capacity toward high-margin HBM for AI customers, structurally tightening commodity DRAM availability and contributing to memory now accounting for approximately 35% of laptop bill-of-materials costs, up from 15-18% previously.

Q4 FY2026 revenue guidance: approximately $50 billion (consensus: $43.24 billion). The gap between management’s outlook and Wall Street’s estimate is the single largest guidance surprise in Micron’s recent history.

CEO Sanjay Mehrotra highlighted multi-year Strategic Customer Agreements as a framework intended to strengthen the durability and predictability of Micron’s financial performance, addressing the cyclical swings that have long characterised the memory industry. If those agreements are locking in demand at these margin levels, the pricing environment may prove more durable than a single quarter suggests.

Key Q4 guidance metrics at a glance:

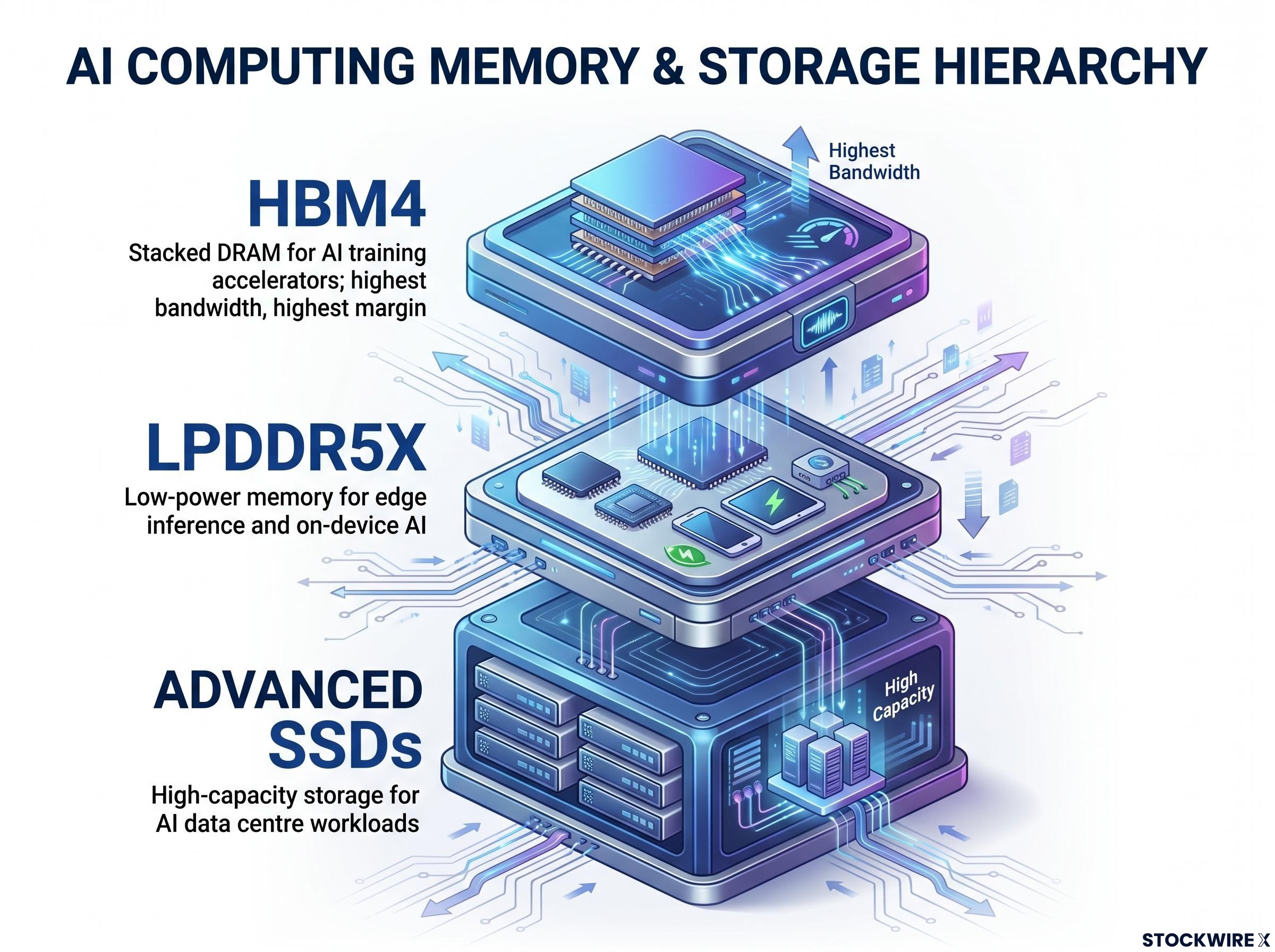

To understand why Micron can guide 86% gross margins, you need to understand what it is actually selling. The product at the centre of the story is HBM4, or High Bandwidth Memory, generation four. HBM is a type of DRAM (dynamic random-access memory, the fast memory chips used in computing) that is physically stacked in layers and placed as close as possible to the AI accelerator chips inside data centre servers. That physical proximity, combined with bandwidth characteristics that standard DRAM cannot match at scale, is what makes HBM indispensable for training and running large AI models.

During Q3 FY2026, Micron achieved high-volume production and delivery of HBM4 into a lead customer platform, while work on the subsequent generation, HBM4E, continued to track on schedule. The generational cadence matters: each new HBM version offers higher bandwidth and capacity, which keeps pricing power intact as customers commit to next-generation AI accelerator platforms that require the latest memory specification.

HBM4 supplier qualifications for Nvidia’s Vera Rubin platform confirmed that all three manufacturers cleared certification simultaneously for the first time, with SK Hynix estimated to hold 60-70% of initial volume allocations, Samsung at 25-30%, and Micron securing the smallest share but establishing a strategic foothold in the platform cycle that positions it to compete for larger allocations in subsequent generations.

The supply side is equally important. HBM manufacturing requires advanced packaging technology, specifically chip-on-wafer-on-substrate processes, that only a small number of companies can execute at scale. The effective global supply pool is three manufacturers: Micron, Samsung, and SK Hynix. For you as an investor, that supply concentration against a demand environment measured in hundreds of billions of dollars annually is the structural explanation for why Micron can guide these margins without the market expecting immediate competitive erosion.

HBM is the headline product, but Micron’s AI memory portfolio extends further. LPDDR5X (low-power double data rate memory, generation 5X) is being deployed in inference-optimised hardware and on-device AI applications, where power efficiency matters as much as raw bandwidth. Advanced SSD (solid-state drive) solutions serve the data centre storage layer, a segment distinct from compute-adjacent HBM but growing alongside the same AI infrastructure buildout.

Shares in Micron finished the regular session on 24 June 2026 at $1,047.20, a decline of 0.44% from the prior close. Once the earnings figures were published, after-hours trading pushed the stock to $1,175.53, representing an advance of $127.02, or roughly 12.11% from the closing price.

After-hours: $1,175.53 (+12.11%) versus a regular session close of $1,047.20. The after-hours move alone added more than $127 per share.

A 12% move on a stock priced above $1,000 is not just a percentage. For institutional holders with position-sizing constraints, it represents a capital event of considerable magnitude in a single session. The scale of the reaction tells you the market was not positioned for guidance of this size. Sell-side models for AI memory demand heading into Q4 were too conservative, and the repricing happened in minutes rather than over a gradual re-rating cycle.

The guidance gap, not the Q3 beat, was the primary catalyst. Micron beat Q3 estimates, but the $50 billion Q4 outlook against a $43.24 billion consensus is what forced the after-hours repricing. That distinction matters: it tells you the market is still catching up to the demand trajectory, not just to a single quarter’s results.

Micron’s numbers are extraordinary by historical standards for a memory company. The question is whether the forces producing them are temporary or structural. Three factors distinguish this environment from prior DRAM cycles:

If these three factors hold, the traditional memory cycle framework, where capacity eventually catches demand, prices fall, and margins compress, is the wrong tool for evaluating Micron’s current business. Investors applying historical price-to-earnings and margin benchmarks from prior memory cycles may be systematically undervaluing the stock in an environment where the rules have changed.

Mehrotra characterised memory as holding strategic importance within the AI technology landscape, with the company committing to record-level investment across technology development and supply expansion. That language signals management expects the demand environment to persist, not peak.

Micron’s Q3 results and Q4 guidance function as a confirmation signal for the broader AI infrastructure investment thesis. If the memory layer of the AI stack is generating returns at this scale, the demand at the compute, networking, and interconnect layers is proportionally intense. Memory sits downstream from the capital allocation decisions that hyperscalers have already made; Micron’s revenue is, in effect, a receipt for AI spending that has already been committed.

Hyperscaler AI capital expenditure from the four largest US cloud operators reached $130 billion in Q1 2026 alone, with full-year 2026 combined guidance approaching $725 billion, a demand signal that flows directly into the order books of the memory supply chain and explains why Micron’s visibility on multi-year procurement agreements has strengthened considerably.

The Q4 guidance of approximately $50 billion implies a single quarter of revenue higher than Micron’s entire annual revenue in any fiscal year prior to the AI memory acceleration. That is the scale of the transformation underway.

For investors trying to determine whether Micron is at a cycle peak or a structural inflection, three forward variables deserve active tracking across the next two quarters:

The cycle peak versus structural shift question for Micron carries real analytical weight because a stock trading at 14 times current earnings may simultaneously trade at 50 times normalised earnings if the cycle reverts, a valuation framework that becomes essential context for any investor trying to determine whether the Q4 guidance scale represents a new earnings baseline or an extraordinary peak.

This is not a call on what Micron stock does next. It is a framework for reading the next two quarters of results and competitive announcements with the right questions in mind. The Q3 report gave you the data. The forward variables give you the lens.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Micron reported Q3 FY2026 revenue of $36.85 billion, adjusted EPS of $25.11, adjusted free cash flow of $18.3 billion, and capital expenditure of $7.1 billion, beating analyst consensus on every key metric.

HBM4 (High Bandwidth Memory generation four) is a type of stacked DRAM placed directly alongside AI accelerator chips in data centre servers to deliver the bandwidth that large AI models require; because only three manufacturers globally can produce it at scale, supply constraints against massive AI infrastructure demand have pushed gross margins to approximately 86%.

The primary catalyst was Q4 FY2026 revenue guidance of approximately $50 billion, nearly $7 billion above the $43.24 billion analyst consensus, forcing an immediate repricing as sell-side models had substantially underestimated the scale of AI memory demand Micron was serving.

Micron guided Q4 FY2026 revenue of $49 billion to $51 billion (midpoint approximately $50 billion), diluted EPS of $30.00 to $32.00, and gross margin of approximately 86%, all materially above prior Wall Street expectations.

The three variables that will determine whether Micron's current earnings profile is durable are the HBM4E commercialisation timeline into 2027, the gross margin trajectory as supply eventually scales, and the renewal terms on the multi-year Strategic Customer Agreements that underpin revenue visibility.