Google’s CEO Sundar Pichai told Stripe founder John Collison that even with roughly $180 billion in annual capital expenditure on the table, it is memory, not money, that prevents him from building bigger. That single admission reframes the entire AI infrastructure narrative. The public discussion of AI’s physical limits has centred on compute power, GPU clusters, and data centre electricity. Memory has occupied a quieter corner. Yet SK Hynix projects a worldwide memory shortage persisting through 2030, every major DRAM producer is fully sold out through 2026, and industry HBM inventory sits at approximately 3-4 weeks, below normal operating levels. What follows traces the structural forces making memory the binding constraint on AI growth, explains why the DRAM industry’s concentrated architecture amplifies rather than absorbs demand shocks, and closes with an honest historical caveat: the most confident shortage forecasts have, in previous cycles, preceded the most violent oversupply corrections.

Memory is not the only physical ceiling slowing AI buildout: AI infrastructure constraints around power have reached their own structural limit, with the IEA projecting data centre and AI electricity consumption exceeding 1,000 TWh by 2026 and Goldman Sachs estimating AI-specific incremental demand could add 800-1,000 TWh versus a no-AI baseline by 2030.

The signal hiding in plain sight: why Pichai’s memory comment matters more than any capex figure

Pichai’s admission arrived almost as an aside. In a podcast conversation with John Collison, the Google CEO described a company prepared to spend approximately $180 billion in a single year on infrastructure, yet constrained not by capital but by the physical availability of memory chips.

Sundar Pichai, CEO of Google (podcast with John Collison, Stripe): Memory availability is among the most critical constraints currently limiting AI infrastructure expansion, even with approximately $180 billion in planned capital expenditure.

The distinction matters. Capital constraints are solvable by spending more. Physical supply constraints are not solvable on any short timeline by any amount of money. Clean rooms cannot be willed into existence; fabrication equipment cannot be fast-tracked past multi-year lead times.

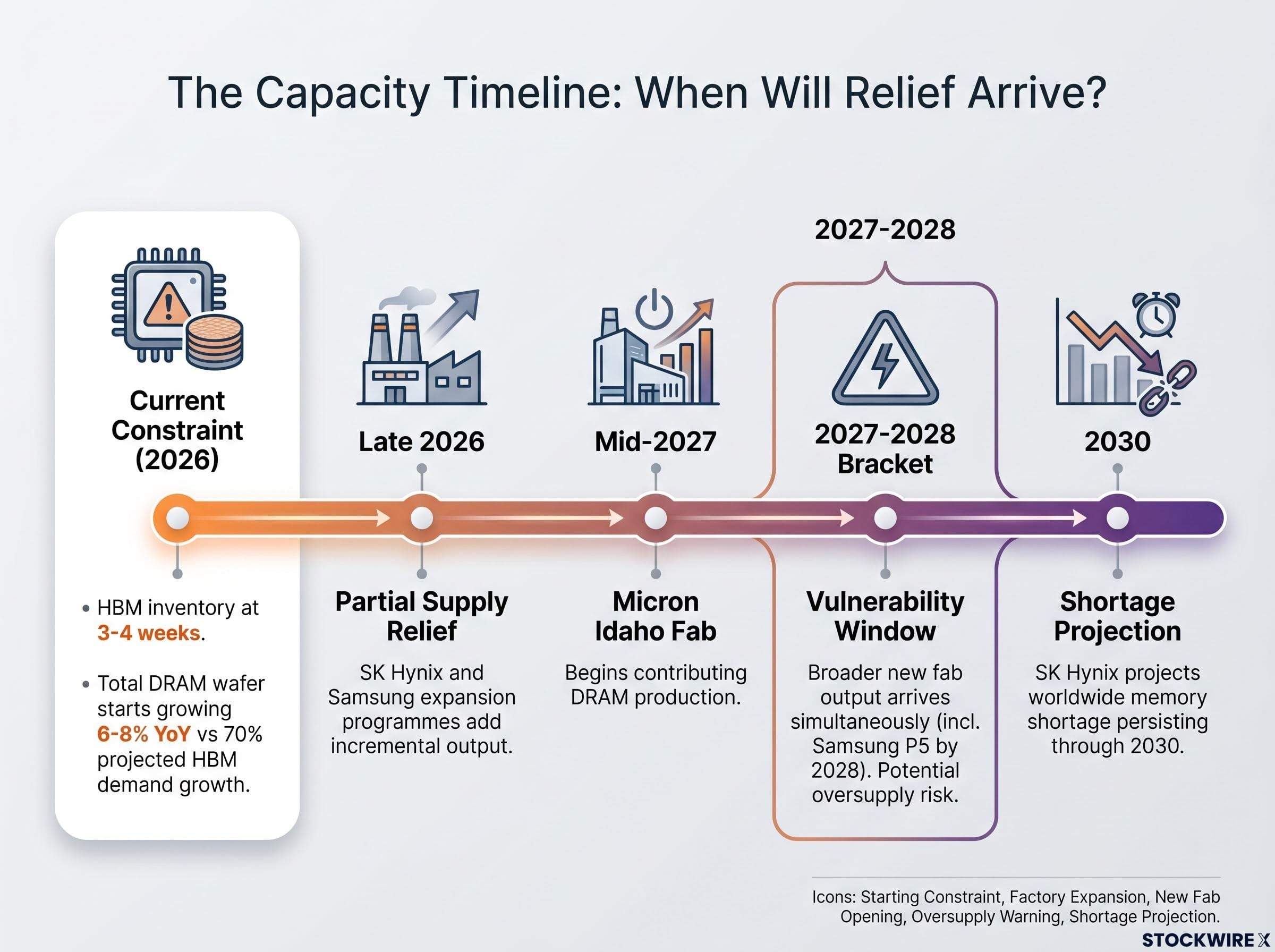

When the most capital-abundant technology company on earth identifies a specific category of silicon as its binding limit, it signals a structural, multi-year supply condition rather than a temporary procurement problem. According to The Diligence Stack (February 2026), HBM inventory levels industry-wide sit at roughly 3-4 weeks, below normal operating thresholds. SK Hynix’s public projection of a global memory shortage lasting through 2030 is not a promotional claim. It is, at minimum, consistent with what Pichai’s statement reveals about the demand side.

When big ASX news breaks, our subscribers know first

What makes AI workloads so memory-hungry: the mechanics of the demand surge

Three compounding forces are driving memory demand beyond anything the industry has previously absorbed:

- Simultaneous model training at scale: Multiple large AI models are being trained concurrently, each requiring enormous quantities of working memory across distributed hardware.

- Growing inference query volumes: End-user inference, where individuals query deployed models, is rising substantially, and each query consumes memory capacity in real time.

- Expanding context windows: Larger context windows and longer token sequences require more working memory per session, multiplying the per-query memory footprint.

These three drivers do not merely add. They compound. A model that is larger, queried more frequently, and processing longer inputs multiplies its memory requirements across all three dimensions simultaneously.

The squeeze extends beyond DRAM into the broader data storage market, where enterprise hardware prices for high-capacity models surged up to 60% as major suppliers sold out production capacity through 2026, confirming that AI-driven supply exhaustion is not a single-product phenomenon but a systemic condition running across the physical infrastructure layer.

Not all memory is interchangeable. DRAM is the broad category of dynamic random-access memory used across computing. HBM, or high bandwidth memory, is a specialised architecture in which memory chips are stacked vertically and connected through silicon interposers to deliver the bandwidth AI accelerators require. HBM is a subset of DRAM, but it is the fastest-growing and most supply-constrained subset by a wide margin.

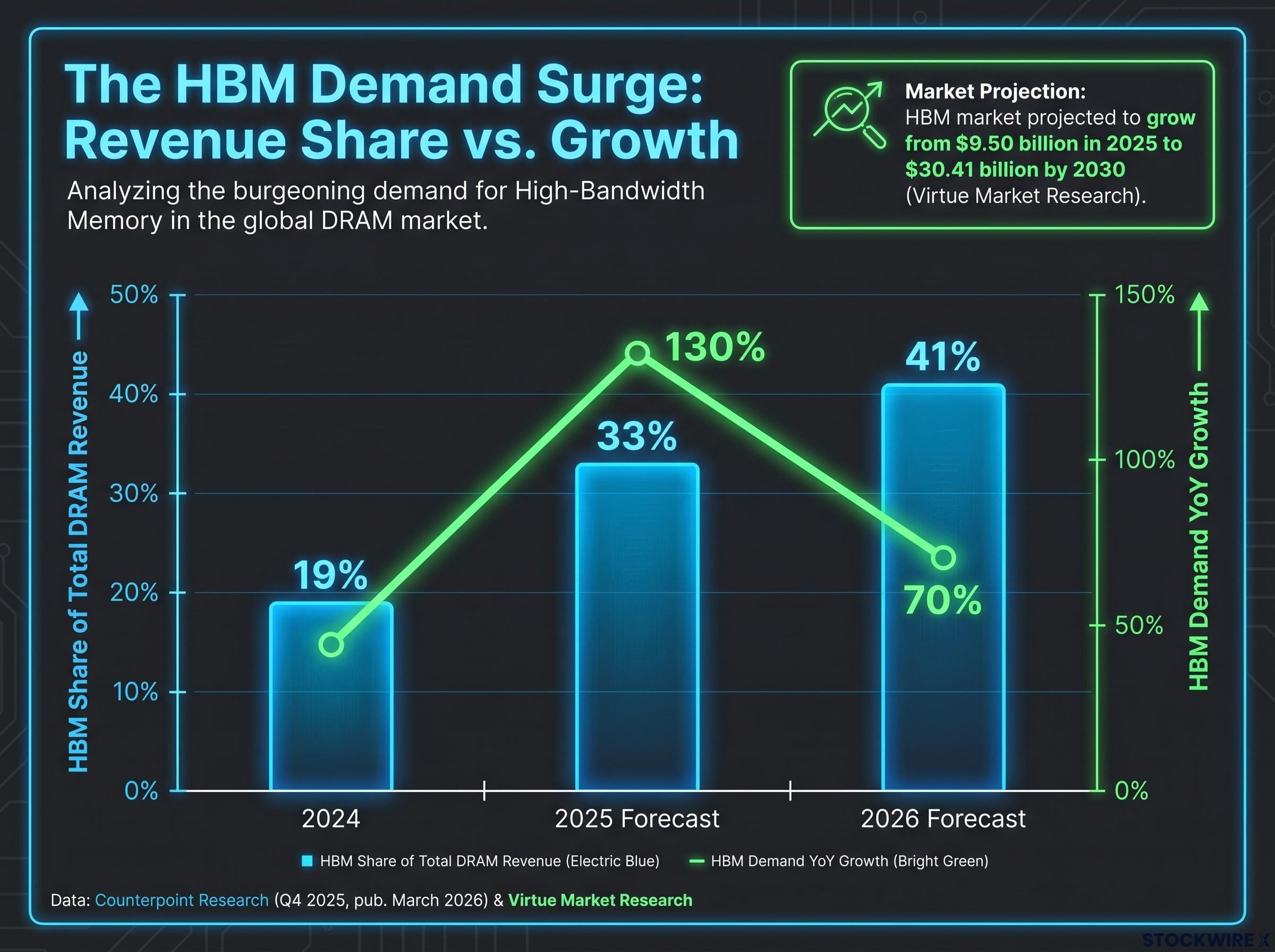

According to Counterpoint Research’s Memory Market Tracker (Q4 2025, published March 2026), HBM demand grew 130% year-on-year in 2025 and is projected to grow 70% year-on-year in 2026. The revenue share trajectory tells the story of where the industry’s centre of gravity is shifting.

TrendForce global memory market projections, updated in May 2026, estimate the total market reaching over $1.28 trillion by 2027, driven by agentic AI workloads that consume HBM at a rate that directly displaces conventional DRAM wafer capacity and tightens pricing across the entire stack.

| Metric | 2024 | 2025 (Forecast) | 2026 (Forecast) |

|---|---|---|---|

| HBM share of total DRAM revenue | 19% | 33% | 41% |

| HBM demand YoY growth | — | 130% | 70% |

Virtue Market Research projects the HBM market will grow from $9.50 billion in 2025 to $30.41 billion by 2030. The trajectory is not linear. It is exponential, driven by inference scaling that shows no sign of plateauing.

A concentrated industry’s structural inability to respond: how the DRAM oligopoly handles a demand shock

The DRAM industry is not structured for rapid supply response. Samsung, SK Hynix, and Micron collectively control over 90% of global DRAM supply. That concentration makes these producers durable businesses in normal cycles; it also makes them structurally incapable of flooding the market with new capacity when demand surges unexpectedly.

The constraint is physical, not financial. Clean room construction, where semiconductor fabrication occurs in precisely controlled environments, is measured in years. No amount of capital committed today produces wafers tomorrow. According to IDC and The Diligence Stack (February 2026), total DRAM wafer starts are growing only 6-8% year-on-year exiting 2026, well below the triple-digit demand growth rates for HBM.

A compounding effect tightens supply further: every wafer directed toward HBM production displaces multiple conventional DRAM wafers. The supply squeeze is not confined to one product category. It runs across the entire stack simultaneously.

All three suppliers are fully sold out through 2026:

- SK Hynix: Entire 2026 HBM production sold out. Holds approximately 62% HBM market share as of Q2 2025 (Patsnap, March 2026). No major yield issues reported.

- Samsung: Plans to increase HBM production capacity by approximately 50% in 2026. HBM4 mass production began February 2026. Entire 2026 HBM4 capacity sold out. However, Samsung has faced yield and qualification challenges for 12-layer HBM3E against NVIDIA‘s standards, adding a technology-risk layer.

- Micron: All 2026 HBM production committed. New Idaho fab does not contribute DRAM production until mid-2027.

When new fabs will actually add supply, and what that timeline means

Partial supply relief may emerge in late 2026 as SK Hynix and Samsung expansion programmes add incremental output. Micron’s Idaho fab begins contributing from mid-2027. Broader new fab output across all three suppliers is not expected to reach meaningful volumes until 2027-2028.

Samsung’s planned P5 fabrication facility is expected to begin operations by 2028. The gap between the 6-8% wafer start growth rate and HBM’s 70% projected demand growth for 2026 alone is the single clearest quantitative expression of why these shortage conditions are structural rather than cyclical.

The $200 billion signal: what massive domestic investment plans reveal about the decade ahead

The scale of investment commitments now underway offers its own form of analysis. Micron has committed to a $200 billion long-term U.S. investment plan spanning Idaho, New York, and Virginia. New York fabs broke ground in January 2026. The Idaho facility begins DRAM production in mid-2027.

SK Hynix has committed approximately $14.6-$15 billion for new HBM packaging plants and fabrication facilities in the United States and South Korea, with total investment commitments exceeding $30 billion. The company plans to double wafer production capacity over the next five years.

SK Hynix’s total investment commitments exceed $30 billion, yet the first meaningful new output from these facilities is not expected until 2027-2028. The lag between capital deployment and supply contribution is measured in years, not quarters.

These are not speculative announcements. Companies with disciplined capital allocation histories do not commit hundreds of billions of dollars unless they expect the supply gap to persist long enough to justify decade-scale construction programmes. The CHIPS Act-era push for domestic semiconductor manufacturing in the United States adds a geopolitical demand layer on top of commercial demand, creating a second structural investment pressure independent of AI growth alone.

Memory chip stocks have already begun repricing these structural conditions, with Micron, Sandisk, and SK Hynix posting combined gains exceeding 250% over 30 days ending May 2026, a market re-rating driven by sold-out HBM capacity, a looming Samsung labour action, and US-China trade policy shifts rather than any single earnings surprise.

The CHIPS and Science Act investment framework administered by the NIST CHIPS Program Office allocated $50 billion to incentivise domestic semiconductor fabrication, creating a geopolitical demand layer for U.S.-based memory production that operates independently of AI growth and adds a second structural pressure sustaining long-horizon capital commitments from all three major DRAM suppliers.

Fortune Business Insights projects the global DRAM market reaching $223.7 billion by 2034, up from approximately $121.83-$126 billion in 2025. The investment commitments from all three suppliers are forward-looking votes on the duration of the shortage; they corroborate SK Hynix’s 2030 projection through capital action rather than analyst forecast.

Why boom-bust history demands proportionate humility in any shortage forecast

DRAM has been a cyclical commodity business for decades. Capacity additions arrive in large, lumpy increments; when they overshoot demand, the resulting oversupply has historically been severe. The current AI-driven shortage does not structurally eliminate that risk.

An analytical humility signal: Li Lu, founder of Himalaya Capital and the money manager entrusted by Charlie Munger with a substantial portion of his personal wealth, previously held approximately 11 million shares of Micron before exiting the position in 2023, prior to the AI-driven rally. Estimated foregone gains exceed $11 billion. Even investors with exceptional track records and intimate knowledge of the industry’s dynamics have been wrong about DRAM timing at enormous cost.

The specific window of vulnerability is 2027-2028, when new fab output from all three suppliers arrives simultaneously. If AI inference demand continues compounding at current rates, that new capacity is absorbed. If demand cools, deployment timelines slip, or enterprise AI adoption plateaus, the same capacity additions that are too slow to solve the shortage by 2027 could produce the oversupply that has terminated every previous DRAM shortage cycle.

No current analyst commentary is prominently flagging oversupply risk for 2027-2028. That absence itself warrants attention. The conditions under which previous DRAM corrections have occurred, consensus confidence in sustained demand growth during a period of aggressive capacity addition, are present now.

Investors wanting to pressure-test these structural arguments against actual analyst models will find our deep-dive into the AI memory investment thesis, which walks through KB Securities’ SK Hynix and Samsung price targets, the three compounding HBM supply constraints, and the valuation starting-point risk that makes timing this trade as important as the thesis itself.

Memory is the AI story: what the shortage means for the semiconductor decade ahead

The DRAM shortage is not a sidebar to the AI infrastructure story. It is the structural foundation. The capital expenditure narratives around compute and data centres are downstream of the memory constraint; without sufficient memory supply, no amount of GPU procurement or power generation solves the bottleneck.

SK Hynix’s public statements project the total addressable market for HBM tied to AI applications expanding from approximately $35 billion to roughly $100 billion. The global DRAM market is forecast to grow from approximately $121.83-$126 billion in 2025 toward $223.7 billion by 2034 (Fortune Business Insights). SK Hynix’s 2030 shortage projection is anchored by the 6-8% wafer start growth rate against 70% projected HBM demand growth for 2026 alone.

The conditions under which that projection holds, or does not:

- Bull case, condition one: AI inference demand continues compounding at rates consistent with 2025-2026 trajectories, absorbing new capacity as it comes online.

- Bull case, condition two: New fab output ramps gradually enough that supply additions are absorbed by demand rather than overshooting it.

- Bear case: The 2027-2028 capacity additions from all three suppliers arrive into a demand plateau, tipping the market from shortage to oversupply as previous cycles have done.

The structural case for memory demand is supported by the evidence available in mid-2026. The historical record of the DRAM industry demands that case be held with proportionate epistemic humility. Both observations are true simultaneously, and any analysis that presents only one is incomplete.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this article are subject to market conditions and various risk factors.