Generac Earnings Beat Estimates as Enterprise Sales Jump 28%

9 mins ago

The pre-market trading session delivered a dramatic 8.61% equity surge for Generac Holdings Inc. investors early Wednesday morning, pushing shares to $236.01. On 29 April 2026, the power equipment manufacturer released its first-quarter financial results, comprehensively shattering Wall Street consensus estimates after a notably disappointing previous quarter. This immediate market validation of the latest Generac earnings release reveals a significant corporate transformation unfolding beneath the headline figures.

While traditional consumer markets stalled, executive leadership successfully executed a massive commercial pivot into cloud computing data centres and enterprise infrastructure. Combined with an aggressive acquisition strategy, this industrial focus has structurally altered the company’s profit profile. What follows is a detailed examination of the specific financial metrics driving today’s valuation spike. Retail and institutional investors now face a fundamentally different business model than the one they evaluated just three months ago.

The contrast between the final months of last year and today’s financial revelation is stark. During the prior quarter, the power generation specialist reported a discouraging earnings miss of $1.61 per share alongside declining revenues. Today’s first-quarter metrics completely reversed that momentum, delivering adjusted per-share profits of $1.80.

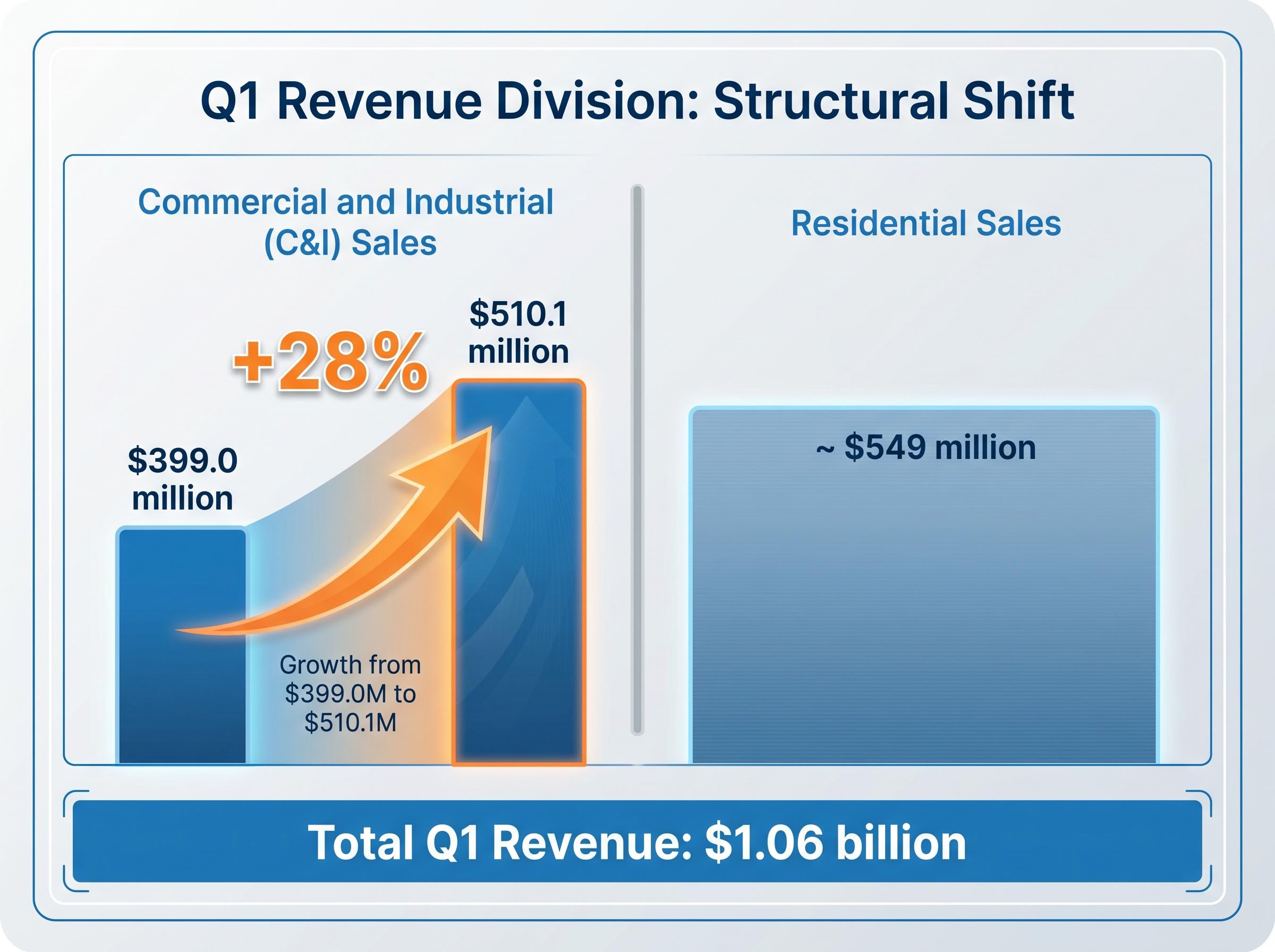

This decisive result easily cleared the $1.33 consensus estimate by 47 cents. Total net sales for the first three months of the year reached $1.06 billion, representing a 12% year-over-year increase. Profitability metrics proved equally compelling, with adjusted EBITDA hitting $193 million to secure a highly efficient 18.3% margin.

The market reaction was instantaneous and aggressive, driving the 8.61% pre-market valuation jump as traders priced in the operational improvements. Retail and institutional investors now have clear quantitative evidence that executive leadership has successfully recalibrated the underlying business.

This recalibration is heavily supported by the broader shift toward capital-intensive AI infrastructure, where major technology firms are directing hundreds of billions into new computing facilities.

| Metric | Wall Street Consensus | Reported Q1 2026 |

|---|---|---|

| Adjusted EPS | $1.33 | $1.80 |

| Total Revenue | $1.05B – $1.07B | $1.06 billion |

| Revenue Growth (YoY) | +12% |

The true engine driving this morning’s outperformance lies in a decisive shift away from consumer dependency. While the traditional residential segment was historically the primary revenue driver, recent quarters have seen consumer demand plateau. The first quarter confirmed this stagnation, but the newly expanded enterprise division entirely absorbed the consumer weakness.

Executive leadership has aggressively pushed into supplying continuous power solutions for the rapidly expanding data centre sector.

The division of revenue highlights this structural shift:

Commercial and Industrial (C&I) sales boomed by 28%, climbing rapidly from $399.0 million to $510.1 million. Residential sales were approximately $549 million. * Enterprise infrastructure projects now represent a significantly larger share of the total $1.06 billion quarterly intake.

The scale of data center construction continues to accelerate globally, with hyperscalers projected to allocate the vast majority of their expansion budgets toward physical hardware and facility development.

This divergence reveals a company successfully transitioning from a consumer-focused brand to a vital technology infrastructure provider. Internally, the business already leverages Amazon Web Services (AWS) to power its proprietary Grid Services platform. This establishes deep operational familiarity with cloud infrastructure requirements.

Securing direct contracts with massive cloud computing buyers remains the most significant forward-looking catalyst for the stock. Company leadership has highlighted ongoing progress in entering the massive hyperscaler sector. These technology giants require rigorous certification processes before integrating third-party backup generation into their critical infrastructure.

Successfully navigating these technical approvals remains highly significant. Securing certified supplier status with major technology buyers would guarantee a pipeline of institutional capital for years to come.

To understand why Wall Street is assigning such a high premium to this commercial pivot, investors must examine the mechanics of enterprise power generation. The fundamental difference between consumer residential backup power and enterprise-grade continuous power solutions comes down to scale and redundancy. A standard home unit is designed to keep household appliances running during temporary suburban grid failures.

In contrast, modern industrial systems are custom multi-megawatt installations engineered to maintain uninterrupted operations for entire technological ecosystems.

The rise of artificial intelligence workloads has dramatically escalated the energy demands of modern data centres. These facilities require unprecedented levels of backup generation redundancy to prevent catastrophic data loss and service interruptions during grid instability. When a cloud computing facility loses power, the financial cost is measured in millions of dollars per minute, making backup infrastructure a non-negotiable capital expense.

Recent IEA data centre electricity tracking highlights severe bottlenecks in global power grids, making localized continuous generation essential for facility operators looking to mitigate utility shortfalls.

Securing contracts in this highly specialised sector provides long-term recurring revenue predictability that consumer retail markets simply cannot match. Home generator sales rely on unpredictable weather events and consumer confidence, whereas enterprise data centre contracts are locked into multi-year development cycles. This structural shift effectively builds a massive economic moat, insulating the balance sheet from the volatility of household spending.

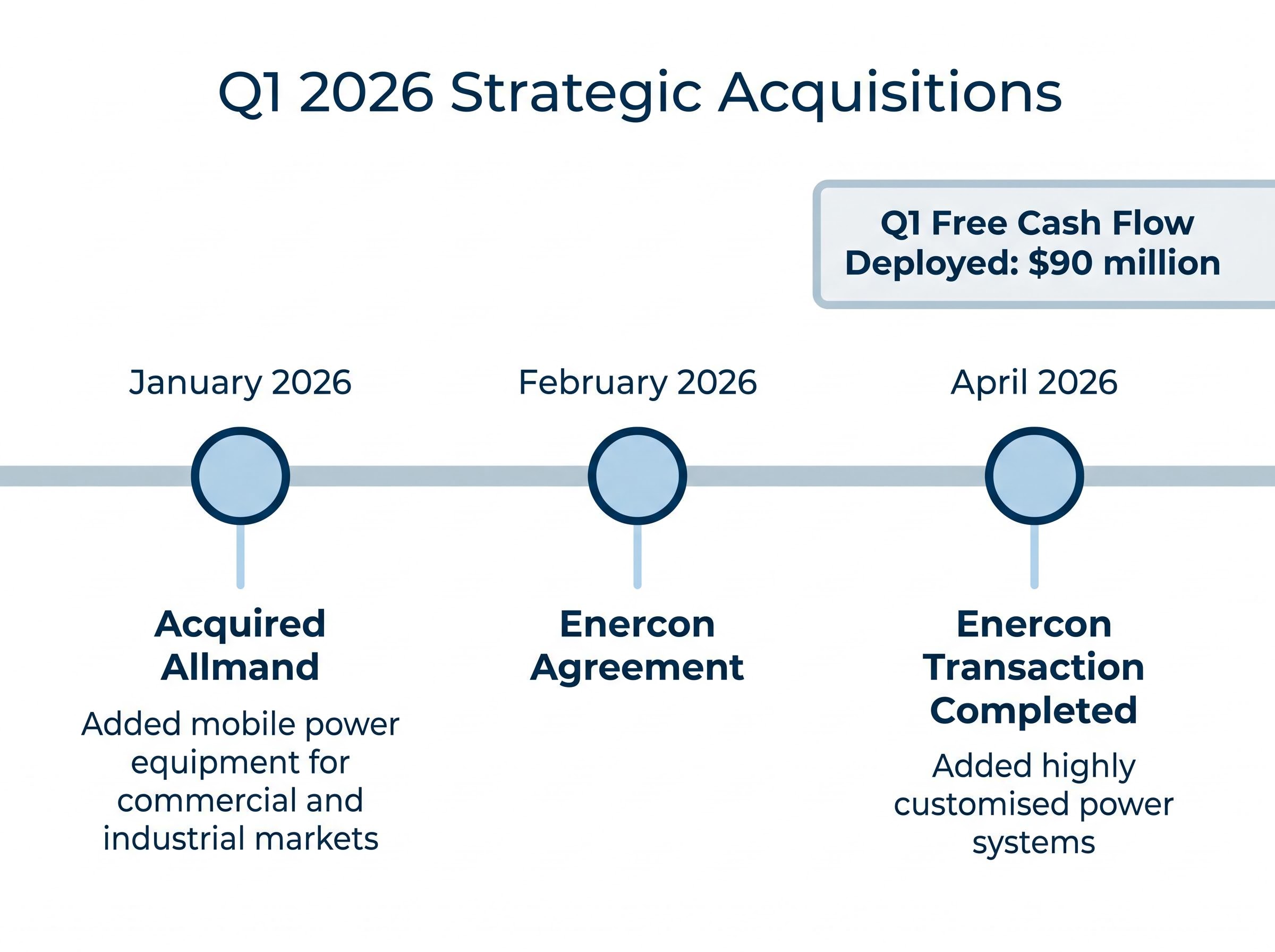

This quarter’s success is not accidental, but rather the result of a deliberate capital allocation strategy executing exactly as planned. Management has methodically bought its way to higher profitability by targeting specialised industrial manufacturers. The company generated $90 million in free cash flow during the quarter, deploying this capital to absorb entities that directly support the commercial and industrial growth strategy.

The timeline of recent corporate buyouts demonstrates a clear push toward vertical integration. In January 2026, the company completed the acquisition of Allmand, immediately adding mobile power equipment targeted specifically at commercial and industrial markets. This was quickly followed by an agreement to buy Enercon in February, a transaction fully completed by April that added highly customised power systems to the corporate portfolio.

Independent financial coverage of these strategic acquisitions confirms the Allmand and Enercon buyouts directly accelerated commercial sales growth by bringing high-margin fabrication capabilities under internal control.

These cash outlays directly feed the expanded profit margins by bringing previously outsourced manufacturing capabilities in-house.

Management Strategy “These strategic acquisitions enhance our product portfolio and increase our vertical integration capabilities, providing the distinct size advantages necessary to service massive infrastructure projects.”

By absorbing these specific entities, leadership has constructed a more evenly distributed business framework. Retail investors are witnessing the mathematical outcome of this strategy. The newly integrated industrial capabilities allow the company to capture larger margins on complex data centre contracts.

The strong initial quarter and integrated acquisition strategy have prompted a significant upward revision in the company’s full-year projections. This upgraded guidance serves as a clear signal of management confidence in their newly established commercial identity. Executives will step into their 10:00 a.m. EDT conference call with a distinctly stronger narrative than analysts anticipated.

The specific changes to the full-year 2026 guidance metrics include:

These forward-looking metrics provide the framework Wall Street will use to track performance for the remainder of the fiscal year. By resetting expectations higher, the business has confirmed that the enterprise infrastructure boom is a permanent recalibration of its earning potential.

Investors exploring the global scale of these multi-year development cycles will find our detailed coverage of data centre capacity expansion, which examines how major international operators are funding and delivering new megawatt capacity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

Generac's Q1 earnings significantly beat Wall Street estimates with adjusted EPS of $1.80, exceeding the $1.33 consensus. This was primarily driven by strong commercial and industrial sales growth and strategic acquisitions.

Generac is strategically pivoting from a consumer-dependent business to a technology infrastructure provider, focusing on supplying continuous power solutions for rapidly expanding data centers and enterprise projects. This move reduces reliance on volatile residential markets.

Data center contracts offer long-term, predictable recurring revenue that consumer markets cannot match. These multi-year development cycles provide a structural economic moat, insulating Generac's balance sheet from household spending volatility.

In Q1 2026, Generac acquired Allmand, adding mobile power equipment for commercial and industrial markets. It also completed the acquisition of Enercon, which brought highly customized power systems into its corporate portfolio.

Generac has raised its full-year 2026 sales growth projections to mid-to-high teen percentages, up from initial mid-teen estimates. Adjusted EBITDA profitability margin targets were also bumped to a band between 18.5% and 19.5%.