Big Tech Earnings Face $600B AI Reality Check Today

1 min ago

Generac shares jumped in early morning trading on 29 April 2026, capturing the attention of markets just hours before the opening bell. The sudden pre-market surge followed a first-quarter Generac earnings release that completely dismantled Wall Street consensus expectations. Financial analysts had significantly underestimated the company’s profitability and industrial momentum heading into the new year, leaving models unprepared for the reported figures.

This price action reflects a fundamental reassessment of the power infrastructure manufacturer’s baseline valuation. Investors who previously viewed the company through a purely consumer lens are now rapidly calculating the impact of a massive profit beat. What follows is a detailed breakdown of the catalysts behind this morning’s financial surprise, focusing specifically on how aggressive enterprise sales and targeted corporate acquisitions engineered the quarter. Grasping these structural shifts reveals why standard forecasting models missed the mark so widely, and what it means for the stock moving forward.

The sheer magnitude of the financial outperformance forced an immediate recalibration of baseline expectations across the market. Management reported an adjusted earnings per share of $1.80, comprehensively beating the $1.35 Wall Street consensus prediction. This $0.45 profit beat represents a significant operational victory, not merely a minor accounting adjustment or a one-time tax benefit.

The company generated $73.25 million in net income and a reported GAAP EPS of $1.24. These figures confirm a steady year-over-year growth trajectory that cleanly distances the current quarter from the $43.84 million net income recorded during the exact same period last year.

The Q1 2026 official earnings release breaks down these profitability metrics across both GAAP and adjusted categories, confirming the fundamental operational improvements that fueled the pre-market rally.

Top-line metrics similarly overpowered analyst projections during the reporting period. First-quarter revenue reached $1.06 billion, beating the $1.05 billion forecast and demonstrating clear expansion from the baseline established in the first quarter of 2025. Investors require these raw numbers to understand exactly why the stock is jumping today. Grasping the size of the beat validates the bullish pre-market reaction and establishes a much higher financial floor for the remainder of the year.

| Metric | Wall Street Consensus | Reported Q1 2026 Results |

|---|---|---|

| Adjusted EPS | $1.35 | $1.80 |

| Total Revenue | $1.05 billion | $1.06 billion |

| Net Income | Not Specified | $73.25 million |

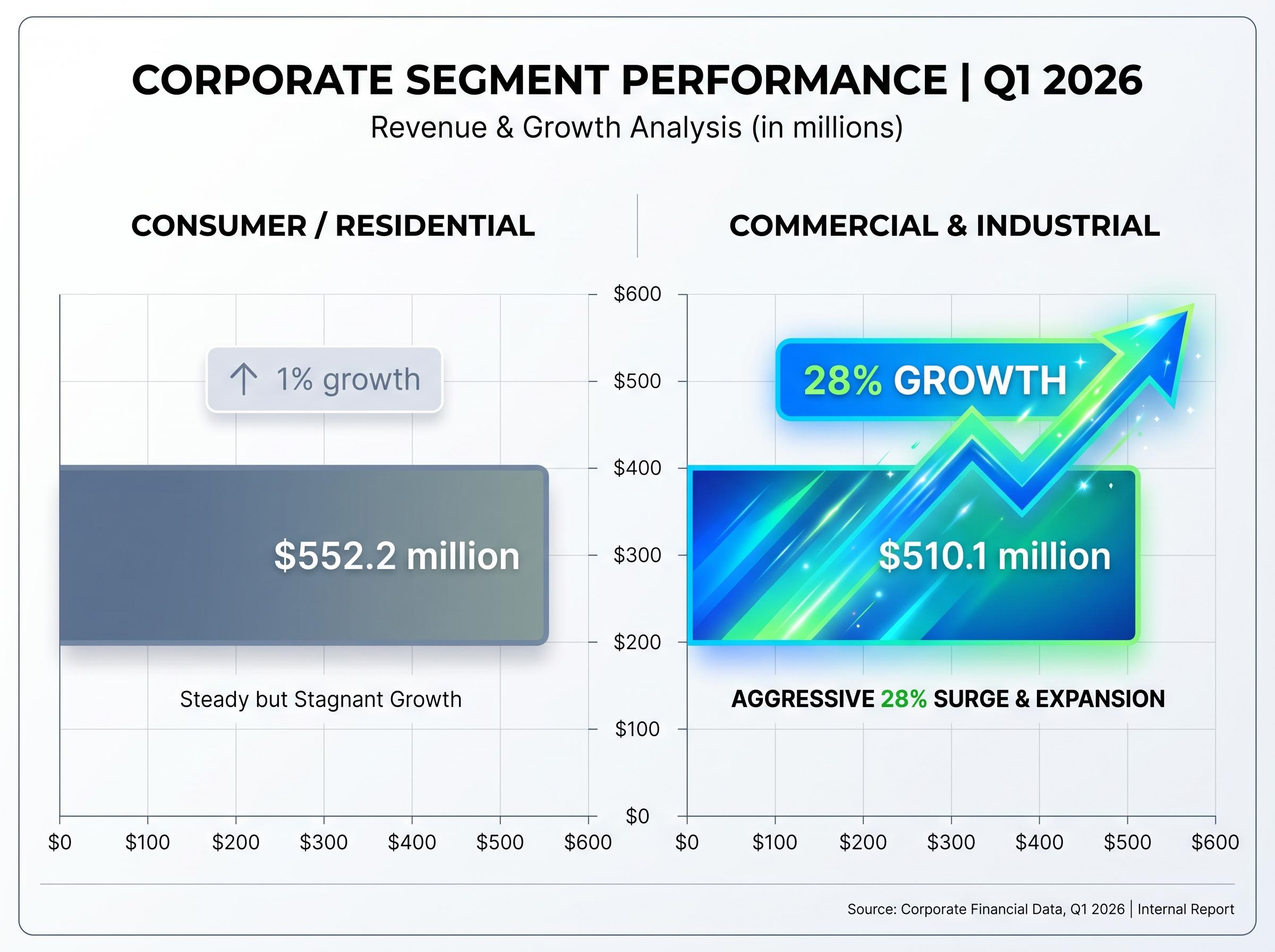

Beneath the headline numbers, the company’s historical reliance on home backup generators is actively giving way to enterprise market dominance. The business model splits broadly into two primary categories: a consumer residential unit that sells backup power to individual homeowners, and a commercial and industrial segment that builds large-scale power infrastructure for corporate clients.

In a traditional reporting period, a flat consumer segment would drag down overall corporate performance and spook retail shareholders. However, the enterprise segment completely absorbed the slack this quarter, insulating the broader earnings report. According to segment reports, consumer home unit revenue grew by approximately 1% to reach $552.2 million, a figure that would ordinarily prompt analyst concern.

According to company reports, the commercial and industrial division delivered the momentum that analysts missed, surging by 28% to hit $510.1 million. This stark percentage difference in growth between the two divisions illustrates an ongoing structural shift in the core business model. The contrast in dollar value highlights how corporate spending is actively overtaking residential purchasing patterns.

To understand the velocity of this shift, investors can reference the fourth quarter of 2025 baseline. During that previous period, the commercial division grew 10% to reach $400 million. The rapid acceleration from 10% to 28% in a single quarter shows how the revenue mix protects the company from misinterpreting flat residential sales as a sign of overall weakness. This educational breakdown proves to retail investors that the immediate growth story now lives entirely within the enterprise sector.

The commercial segment’s success connects directly to the explosion of artificial intelligence and cloud computing infrastructure across the United States. This quarter’s beat forms part of a larger macroeconomic trend rather than a one-off anomaly.

United States-based data centres are driving an unprecedented demand for continuous power infrastructure, and the company is actively securing lucrative contracts with these massive cloud buyers. Management anticipates a 30% or greater increase in commercial sales throughout 2026. This aggressive forward-looking forecast relies heavily on ongoing certification processes that are nearing completion with major cloud computing operators.

Upgraded BloombergNEF data center power forecasts project national capacity requirements reaching 106 gigawatts by 2035, illustrating the massive scale of the structural tailwind lifting commercial generation suppliers.

Connecting the stock to the highly lucrative artificial intelligence narrative reveals a multi-year growth runway. This technological tailwind fundamentally changes the total addressable market, shifting the firm from standard backup generation into critical technology infrastructure. Understanding the data centre connection shows why institutional capital is rotating into the stock this morning.

These expanding data centre contracts ensure that the company maintains a steady pipeline of enterprise demand. Investors can view these certifications as long-term revenue anchors that stabilise the broader financial outlook.

While macroeconomic tailwinds provided the opportunity, leadership deliberately engineered the current revenue upgrade through targeted corporate purchases. The company is actively deploying capital to capture market share, proving they are playing offence rather than just passively benefiting from industry trends.

Absorbing new entities creates immediate size advantages and establishes a more evenly distributed business framework. These non-organic additions are currently compounding the organic growth generated by the data centre division. Management cited these specific strategic buyouts as primary drivers behind the increasingly optimistic annual outlook.

Similar targeted industrial manufacturing acquisitions are increasingly being used by sector leaders to secure proprietary engineering capabilities and immediately unlock new commercial revenue streams.

The execution timeline highlights this aggressive expansion strategy:

5 January 2026: According to company statements, the company completed the acquisition of Allmand, targeting immediate scale and expanded capabilities in industrial worksite infrastructure. 1 April 2026: According to company statements, the purchase of Enercon was finalised, specifically designed to expand custom power engineering capabilities for large corporate clients.

By integrating these two companies within a four-month window, leadership secured the manufacturing capacity required to meet their upgraded commercial sales targets. Readers must understand that these buyouts directly accelerate market share capture. This deliberate capital deployment proves the executive team is actively building a moat around their enterprise power segment.

The first quarter’s momentum has forced an upward revision to the company’s full-year fiscal predictions. Annual revenue expansion targets have been upgraded from mid-teen growth to the middle-to-upper teen percentage brackets.

Profitability margins are also expanding alongside top-line revenue targets. According to company guidance, management bumped the adjusted EBITDA profitability margins to a band between 18.5% and 19.5%, establishing a new median EBITDA target of 19.0%. This upgraded guidance provides concrete proof that leadership believes the current enterprise momentum is entirely sustainable.

Maintaining these elevated industrial subsidiary profit margins has become a critical indicator of operational efficiency, especially as specialised manufacturers work to offset higher supply chain and production costs.

As the market digests these upgraded figures, standard trading hours and impending analyst upgrades will likely dictate the next major price action for the stock. These forward-looking projections are subject to market conditions and various execution risk factors. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Generac's Q1 2026 earnings beat was primarily driven by exceptional growth in its commercial and industrial segment, strategic acquisitions, and increasing demand for power infrastructure from data centers.

Generac is strategically shifting its business focus towards the commercial and industrial sector, which showed significantly higher growth at 28% compared to the residential segment's 1% growth in the first quarter of 2026.

Data centers are a major catalyst for Generac's commercial segment growth, as the explosion of AI and cloud computing infrastructure creates unprecedented demand for continuous power, leading to lucrative contracts and certifications with major cloud operators.

Yes, Generac upgraded its full-year fiscal predictions following the strong Q1 2026 results, revising annual revenue expansion targets upwards and boosting adjusted EBITDA profitability margins to a median of 19.0%.