Why Seeing Machines Trades Below 5p Despite EU Mandate Wins

7 hrs ago

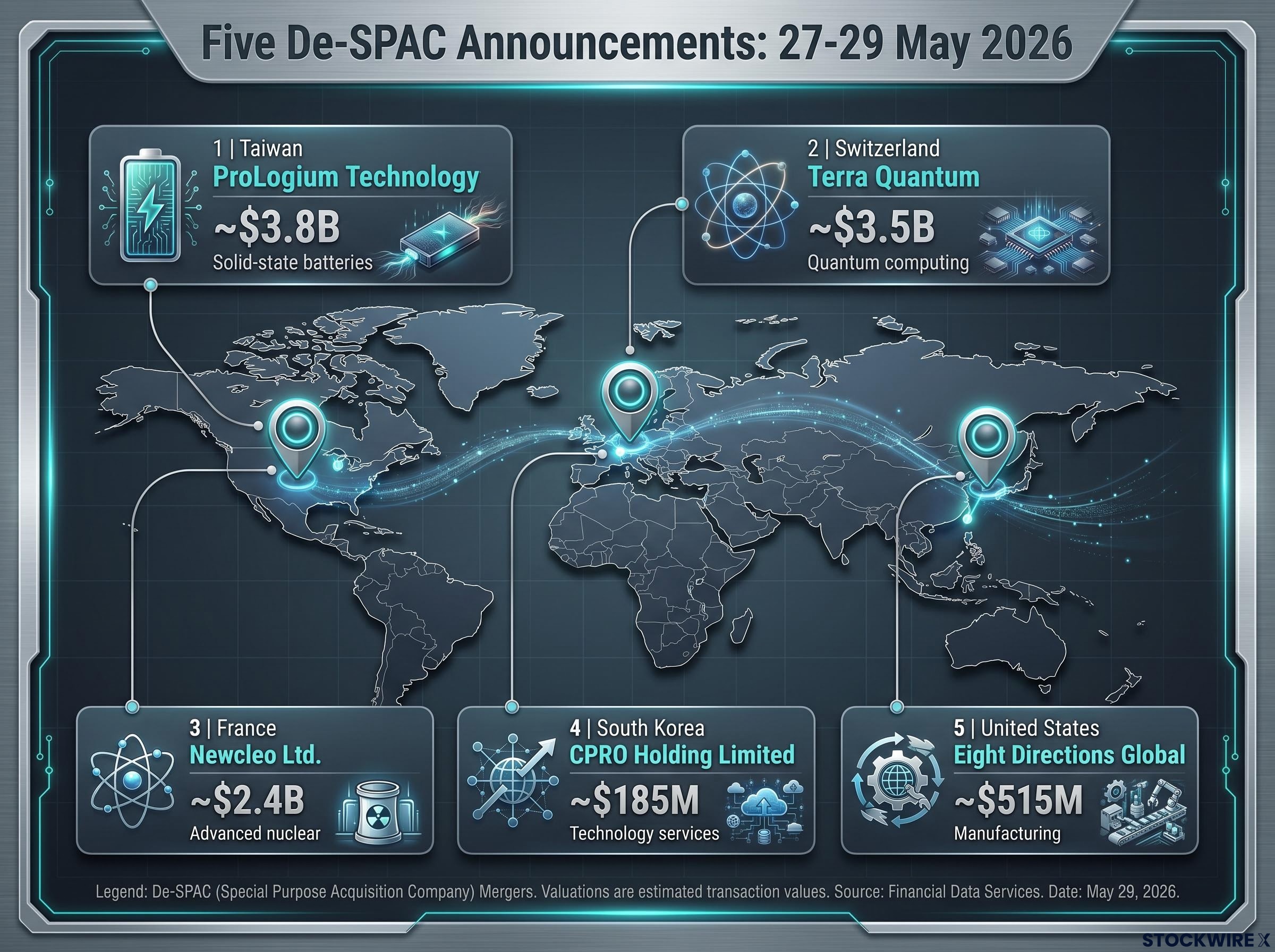

In the first two months of 2026, SPACs raised approximately $10 billion across 50 vehicles, outpacing 24 traditional IPOs that raised $7 billion combined. By late May, five more de-SPAC deals had been announced in a single week, spanning quantum computing in Switzerland, advanced nuclear energy in France, solid-state batteries in Taiwan, manufacturing in the United States, and technology services in South Korea. The announcements are not isolated outliers. More than 100 business combinations were announced in 2025 alone, and the year-to-date 2026 SPAC IPO count had reached 98 by end of May. The five transactions offer a concrete, data-grounded lens into who is using the de-SPAC route in 2026, why these companies are choosing the structure over a traditional IPO, and what investors should evaluate before drawing conclusions from headline equity values. What follows is an examination of the five transactions as a dataset, the patterns they reveal, the mechanics underlying every de-SPAC, and a practical framework for evaluating any deal announcement that arrives next.

Between 27 May and 29 May 2026, five de-SPAC transactions were announced on Nasdaq. The targets range from a $185 million technology services company headquartered in South Korea to a $3.8 billion solid-state battery manufacturer based in Taiwan. Three of the five sit in capital-intensive deeptech sectors; one operates in conventional manufacturing; one provides technology services.

The table below presents all five transactions side by side, drawn from a single week of public announcements rather than a curated sample selected to illustrate a thesis.

| Target Company | SPAC Ticker | Headquarters | Sector | Announced Equity Value |

|---|---|---|---|---|

| ProLogium Technology | TDAC | Taiwan | Solid-state batteries | ~$3.8 billion |

| Terra Quantum | AXINU | Switzerland | Quantum computing | ~$3.5 billion |

| Newcleo Ltd. | NHIC | France | Advanced nuclear | ~$2.4 billion |

| Eight Directions Global | QSEAU | United States | Manufacturing | ~$515 million |

| CPRO Holding Limited | LCCCU | South Korea | Technology services | ~$185 million |

Data sourced from FactSet as of 27-29 May 2026. Of the five, only Newcleo disclosed a PIPE commitment ($220 million). The remaining four either structured without a PIPE or had not yet disclosed terms publicly at the time of announcement. That distinction, and what it signals, warrants closer examination later in this analysis.

A traditional IPO prices shares based on a roadshow and book-building process managed by underwriters. A de-SPAC works in two stages. First, a blank-cheque company (the SPAC) raises capital through its own IPO, with proceeds held in a trust account. Second, the SPAC identifies a private operating company and merges with it, converting the target into a publicly listed entity. The merger is the de-SPAC.

The de-SPAC pathway is structurally distinct from traditional IPO mechanics in ways that directly affect how retail investors access shares, at what price, and against what information backdrop; in a conventional offering, institutional book-building sets price discovery before any public shares trade, a process that consistently advantages insiders over later entrants.

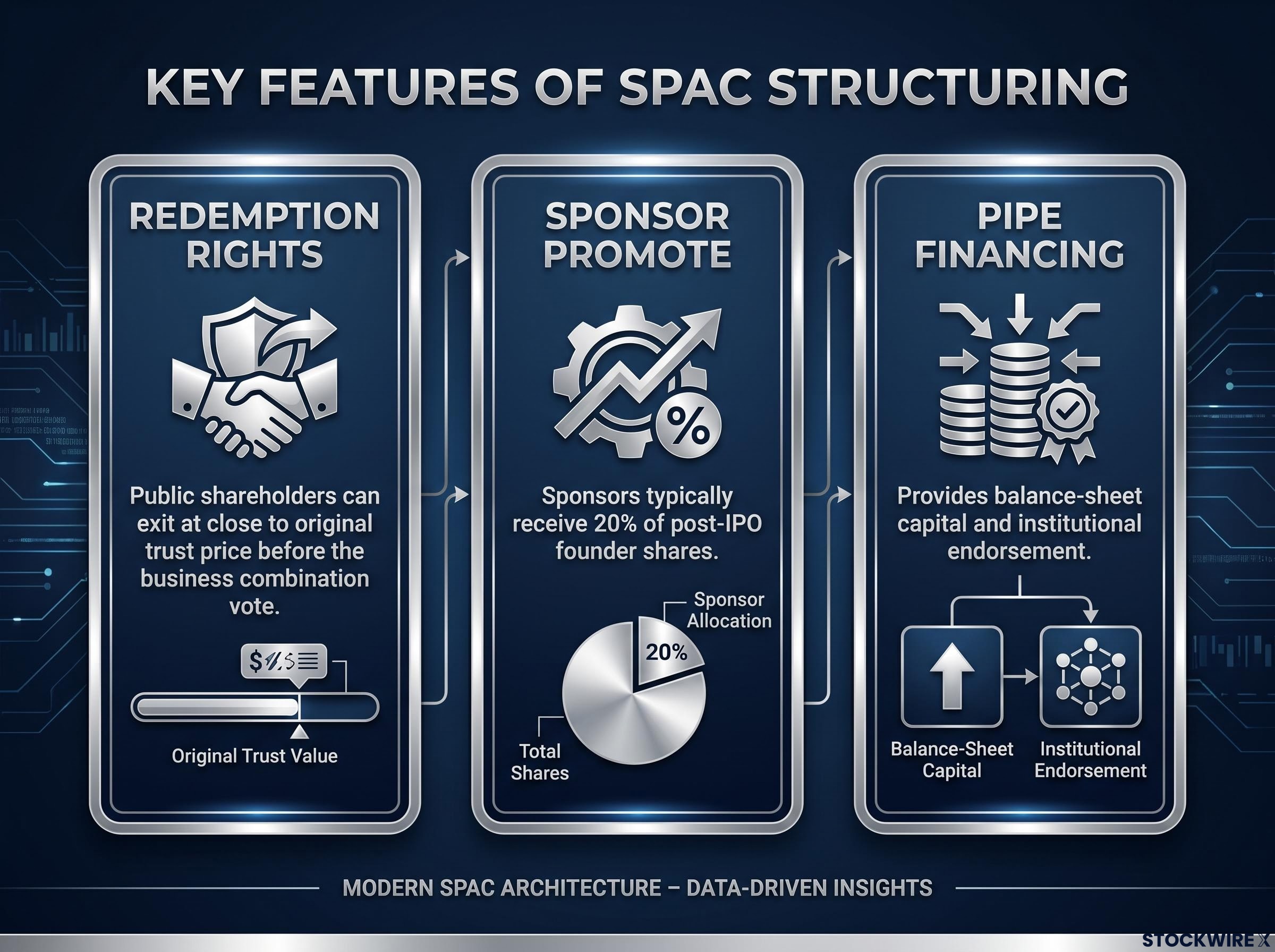

Three structural features distinguish this pathway from a conventional listing, and each carries direct implications for investors:

Harvard Law School research on SPAC dilution found that sponsor promote structures result in extraordinarily high sponsor returns while leaving post-merger shareholders holding materially diluted positions, a dynamic that makes sponsor track record and promote terms among the highest-priority due diligence items in any de-SPAC evaluation.

Regulatory note: De-SPAC filings routinely include multi-year financial projections from the target company. Before 2022, the safe harbour provisions of the Private Securities Litigation Reform Act afforded broader liability protection for such projections than was available in traditional IPOs. Post-2022 SEC rule changes narrowed that shield, aligning de-SPAC projection liability more closely with traditional IPO standards. Projections in de-SPAC filings remain more detailed than those in typical IPO prospectuses, but the legal protection around them is now materially thinner.

Understanding these three features, and the revised projection liability framework, equips investors to interpret any de-SPAC announcement with appropriate scrutiny regardless of sector or headline valuation.

The five transactions share a single announcement window. They share little else. That contrast is where the patterns emerge.

Four of the five targets are headquartered outside the United States:

Only Eight Directions Global is U.S.-based. The SPAC route is functioning as a cross-border listing mechanism, giving international companies access to U.S. capital markets through a merger pathway that bypasses some of the structural difficulties smaller or pre-revenue foreign issuers face in a traditional IPO roadshow. This aligns with broader 2026 data: as of 22 May 2026, China’s CSRC had publicly disclosed 50 filing applications relating to U.S. listings, according to ARC Group citing CSRC data, with the actual number potentially higher due to confidential filings. The appetite for U.S. market access extends well beyond Chinese issuers.

Three of the five targets operate in sectors that market commentary has identified as dominant themes in 2026 SPAC dealmaking: advanced nuclear, quantum computing, and solid-state batteries. These are capital-intensive businesses with long development timelines, precisely the profile that benefits from the de-SPAC structure’s ability to present detailed forward projections and secure committed institutional capital at the point of listing. The remaining two targets (manufacturing and technology services) demonstrate that the mechanism serves conventional sectors as well, but the centre of gravity in late-May announcements sits firmly in deeptech.

The equity value range across the five transactions, from approximately $185 million to approximately $3.8 billion, demonstrates that the SPAC mechanism is not confined to a single size tier. CPRO Holding Limited, at the smaller end, represents a growth-stage international company that would likely face structural difficulty accessing a traditional U.S. IPO. ProLogium Technology, at the larger end, chose the SPAC route despite a valuation that could have supported a conventional public offering. The structure scales in both directions.

Not every de-SPAC reaches completion: SPAC deal termination and renegotiation are routine features of the pipeline, and when a target exits one sponsor relationship to pursue better-aligned terms with another, the episode reveals how companies weigh SPAC structure against valuation ambition and timing constraints.

Among the five transactions, only Newcleo disclosed a PIPE: $220 million in committed institutional capital, representing roughly 9% of the company’s approximately $2.4 billion announced equity value.

A PIPE in a de-SPAC context serves a dual function. It provides balance-sheet capital that supplements the SPAC trust proceeds, and it acts as an observable signal of institutional conviction. When named institutional investors commit capital at deal announcement, they are effectively telling the public market that they have conducted their own due diligence and are willing to hold equity at or near the announced valuation. For retail investors who cannot access pre-merger diligence materials, the presence, size, and identity of PIPE investors is one of the most informative publicly available data points.

The absence of disclosed PIPEs in the other four transactions is analytically noteworthy but not necessarily a negative signal. Some de-SPACs are structured without PIPE financing. In other cases, PIPE terms may not yet be publicly disclosed at the announcement stage. The distinction matters: no PIPE and undisclosed PIPE are different conditions, and investors should track subsequent filings for clarification.

FTI Consulting has observed that 2026 SPAC transactions attracting committed institutional capital tend to be those where sponsor incentives, target fundamentals, and long-term investors are aligned. The PIPE is one observable expression of that alignment.

The patterns and mechanics described above converge into a repeatable analytical framework. The following eight questions, drawn from the structural and thematic observations in this analysis, apply to any de-SPAC announcement.

Assessing sponsor track record in de-SPAC transactions draws on the same per-share return analysis and red-flag frameworks that professional investors apply to small-cap management teams more broadly, including scrutiny of how capital has been allocated in prior vehicles, whether raises were signalled in advance, and whether promote structures incentivise deal completion over shareholder value.

The table below maps each company stage to the analytical lens most appropriate for evaluation.

| Target Company Stage | Primary Analytical Lens |

|---|---|

| Pre-revenue deeptech | Burn rate, licensing timeline, technology validation milestones |

| Early-revenue | Revenue trajectory, customer concentration, path to unit economics |

| Established operating business | Earnings quality, margin profile, competitive positioning |

The five transactions announced in late May 2026 are not a prediction of de-SPAC market performance. They are a credible snapshot of who is accessing the structure, in which sectors, and at what scale in the current market cycle. The geographic breadth, the sector concentration in capital-intensive deeptech, and the structural scalability from $185 million to $3.8 billion all point to a SPAC market that has moved past the speculative dynamics of 2020-2021 into a more selectively constructive phase.

A note on verification: the five specific transactions could not be independently confirmed in public SPAC deal databases at the time of research. Transaction details are carried as reported by FactSet, and readers should conduct independent verification before making investment decisions.

The practical next step is straightforward. When the next de-SPAC announcement arrives, start with the stage-of-development categorisation before engaging with projected financials or headline equity values. The SEC’s EDGAR database, specifically Form S-4 and Form DEFM14A filings, remains the primary source for transaction projections, PIPE terms, and sponsor promote structure.

For investors wanting to build the document-reading skills that apply directly to de-SPAC filings, our dedicated guide to reading IPO prospectus filings walks through how to navigate SEC EDGAR, locate the specific sections that contain revenue assumptions, governance terms, and risk disclosures, and apply a consistent analytical framework to any new listing, whether a traditional S-1 or a de-SPAC Form S-4.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Financial projections referenced in de-SPAC filings are subject to market conditions and various risk factors. Past performance does not guarantee future results.

A de-SPAC deal is the merger between a blank-cheque SPAC company (which has already raised capital through its own IPO) and a private operating company, converting that private company into a publicly listed entity. Unlike a traditional IPO, where underwriters run a roadshow and institutional book-building sets the price before public shares trade, a de-SPAC allows the target company to present detailed multi-year financial projections and negotiate deal terms directly with the SPAC sponsor.

A PIPE (private investment in public equity) is a commitment of capital from institutional investors placed at or near the time of a de-SPAC announcement, and it serves two purposes: it supplements the SPAC trust proceeds on the target's balance sheet, and it signals that professional investors have conducted their own due diligence and are willing to hold equity at the announced valuation. Among the five late-May 2026 de-SPAC deals, only Newcleo disclosed a PIPE commitment of $220 million, making it one of the most informative publicly available data points for retail investors evaluating any deal.

SPAC sponsors typically receive 20% of post-IPO founder shares as compensation for sourcing and executing a deal, which dilutes other shareholders, making sponsor track record and promote terms among the highest-priority due diligence items. Investors should review whether lockup and incentive terms align the sponsor with long-term shareholder value rather than simply incentivising deal completion.

The SPAC route is functioning as a cross-border listing mechanism, giving international companies access to U.S. capital markets through a merger pathway that bypasses some of the structural difficulties smaller or pre-revenue foreign issuers face in a traditional IPO roadshow. Four of the five de-SPAC deals announced in late May 2026 involved targets headquartered in Taiwan, France, Switzerland, and South Korea.

The most important starting point is categorising the target's stage of development (pre-revenue deeptech, early-revenue, or established operating business), as this determines the appropriate valuation methodology and risk framework before any other analysis begins. From there, investors should examine burn rate and capital adequacy, sponsor track record and promote structure, PIPE quality and terms, geographic and regulatory risks for non-U.S. targets, and the key assumptions underlying multi-year financial projections.