Finfluencer Rules Won’t Work Until the Penalty Beats the Profit

2 hrs ago

CSL shares closed at A$119.88 on 8 May 2026, a price last seen in 2016. A stock that once commanded a price-to-earnings ratio above 40x now trades at roughly 14.7x trailing earnings. The question facing Australian investors is no longer whether the damage has been done, but whether the valuation has finally caught up with the reality of a business in the middle of an earnings reset, a leadership transition, and approximately A$5 billion in impairment charges. CSL’s decline, now exceeding 60% from its all-time high and approximately 50% over the past 12 months, is not a quiet re-rating. For the many ASX investors who hold this stock in a portfolio or superannuation fund, this article examines the specific factors compounding the decline, builds a framework for thinking about where valuation floors form in falling quality growth stocks, and presents the bear and bull cases so that investors can assess whether the current price represents distress or opportunity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

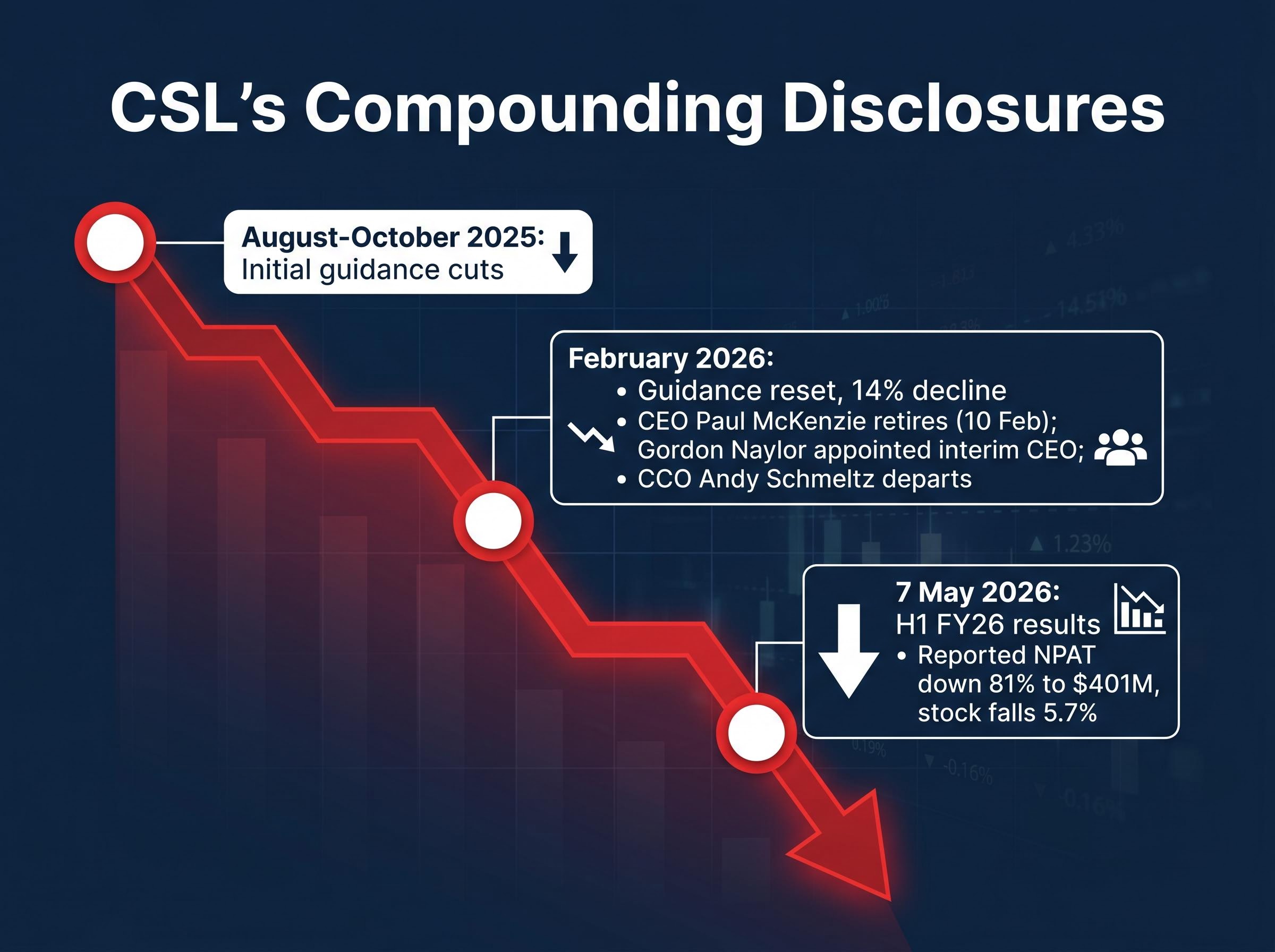

CSL’s sell-off did not arrive in a single shock. It accumulated through a sequence of negative disclosures, each one eroding the credibility buffer the next announcement needed to hold the share price.

The pattern ran as follows:

Reported NPAT fell 81% to $401 million for H1 FY26, against underlying NPATA of approximately $1.9 billion (underlying down 7%). The gap between reported and underlying figures reflects the scale of non-cash impairments now running through the income statement.

Multiple guidance resets within a short timeframe represent a qualitatively different category of risk than a single miss. A single miss can be attributed to an external shock. Serial resets signal systematic forecasting failure, and that distinction matters. The year-to-date decline of approximately 25% from a year-start price of roughly A$160 sits on top of the prior 12-month erosion, producing cumulative losses that have reshaped how brokers and institutions assess management credibility.

Serial guidance resets damage a stock more severely than a single miss because each reset recalibrates market expectations downward while simultaneously eroding the credibility of the next forecast, creating a compounding dynamic where even an in-line result can be interpreted as insufficient evidence that the forecasting failure pattern has broken.

The ASX continuous disclosure obligations require listed entities to immediately notify the exchange of any information that a reasonable person would expect to have a material effect on the price or value of securities, a standard that frames how each of CSL’s sequential guidance resets should be read as a formal acknowledgement of material change rather than routine investor communication.

The headline number is approximately A$5 billion in pre-tax impairments spanning FY26 and FY27. The majority is tied to Vifor intangibles and underutilised physical assets, not operational deterioration in the plasma business itself.

That distinction matters for different investor cohorts. The reported NPAT figure ($401 million for H1 FY26) captures impairments and restructuring costs. The underlying NPATA figure (approximately $1.9 billion) strips them out. Income-focused investors and superannuation funds often screen on reported figures. Growth investors tend to anchor to underlying metrics. Both numbers tell part of the story; neither tells all of it.

Impairments are non-cash, but they carry a specific meaning: management is formally acknowledging that prior acquisition price assumptions were too optimistic. When those write-downs reach A$5 billion, the acknowledgement is substantial.

The three revenue headwinds quantified in CSL’s FY26 guidance revision — US immunoglobulin channel inventory normalisation at approximately $300 million, China albumin price compression at approximately $200 million, and other items including HEMGENIX and Vifor iron competition at approximately $150 million — are characterised by management as timing and structural issues rather than demand deterioration, a framing that underpins the bull case but remains unverified by results.

Beyond the impairments, several revenue headwinds are compressing the earnings base:

| Revenue headwind | Estimated impact | Primary driver |

|---|---|---|

| US immunoglobulin channel inventory | ~$300M | Channel inventory normalisation reducing near-term demand |

| Chinese albumin pricing | ~$200M | Market price deterioration in Chinese albumin segment |

| Middle East, HEMGENIX, iron therapy | ~$150M | Regional exposure, revised gene therapy expectations, competitive pressure |

Vifor was acquired in 2022 to diversify CSL beyond plasma into renal and iron therapy. The rationale has not materialised in returns. Integration challenges in the renal segment have been compounded by rising competition in iron therapy, and HEMGENIX, CSL’s gene therapy asset, now carries revised commercial expectations. The multi-asset impairment picture raises a capital allocation question that extends beyond a single write-down cycle: whether remaining asset valuations on the balance sheet are credible.

Quality growth stocks tend to de-rate in stages. First, the growth premium compresses: the price-to-earnings ratio falls from 40x to 25x as the market prices out above-trend earnings expansion. Then the quality premium compresses: 25x becomes 18x as questions emerge about whether the business model itself has changed. At that point, the floor question shifts from growth expectations to normalised earnings power.

CSL is now in the third stage. At 14.7x trailing earnings, the stock sits near a 10-year low, trading below the multiples that even cyclical healthcare names typically command.

Three valuation frameworks are being applied:

| Methodology | Implied price range | Key assumption |

|---|---|---|

| DCF (reset discount rate) | A$193-A$240 | Discount rate of 8-9% (vs prior 7%), long-term growth of 2-4% (vs prior 8-10%) |

| Sum-of-parts | Plasma core at 12-15x (~70% of value) | Seqirus and Vifor assets discounted 20-30% for impairment and execution risk |

| Peer anchoring | Floor at ~15x forward earnings | Sonic Healthcare and Cochlear historically trade at 20-25x; CSL’s plasma risk justifies a discount |

Simply Wall St revised its fair value estimate to AU$195.41, down from prior estimates around A$237-A$246. Consensus forward P/E sits at 15-18x FY27 NPATA. Historical precedent offers some reference: CSL’s 2018 earnings miss saw the stock trade near A$150 before recovering, and analysts have flagged technical support around A$120.

RSI sat at 27.98 as of early May 2026, deeply oversold territory. Yet selling pressure has continued. Oversold signals that fail to halt a decline are associated with fundamental reassessment rather than short-term panic, a pattern that typically resolves only when a credible earnings recovery narrative is established.

The distinction between a technical floor and a fundamental floor is the difference between averaging down productively and catching a falling knife. Technical indicators have not arrested this decline. A fundamental floor requires a new earnings story, and that story has not yet arrived.

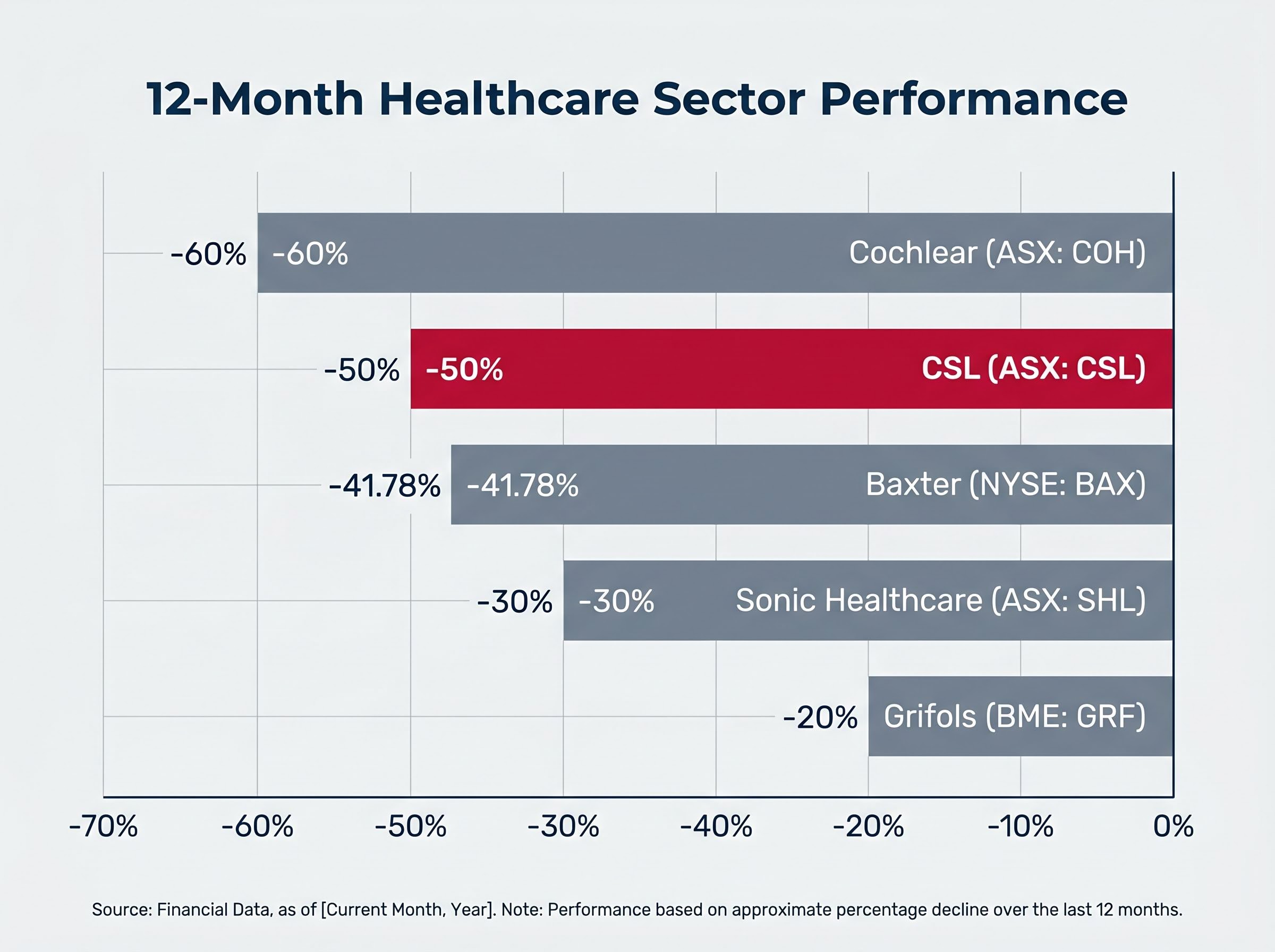

CSL’s decline does not exist in isolation. A broad re-rating across Australian healthcare and global biologics names has been significant over the past 12 months.

| Company | 12-month performance | Primary driver |

|---|---|---|

| CSL (ASX: CSL) | ~-50% | Impairments, guidance resets, leadership transition |

| Cochlear (ASX: COH) | ~-60% | Premium valuation unwinding |

| Sonic Healthcare (ASX: SHL) | ~-30% | Earnings normalisation post-pandemic |

| Baxter (NYSE: BAX) | ~-41.78% | Margin pressure, renal/iron therapy competition |

| Grifols (BME: GRF) | ~-20% | Plasma collection headwinds, US pricing pressure |

The sector headwind is real. Cochlear’s 60% decline and Sonic Healthcare’s 30% fall confirm that the re-rating extends well beyond CSL. Attributing the entire decline to company-specific factors would be an error.

The five compounding forces driving the broader ASX healthcare selloff — covering RBA rate policy, Australian dollar appreciation, consumer confidence deterioration, corporate governance failures, and geopolitical disruption — create a sector-level backdrop against which company-specific damage becomes harder to isolate, and the Cochlear and Sonic Healthcare declines in the peer table reflect this macro overlay as much as any business-specific deterioration.

Grifols, however, provides the most instructive comparison. As the closest plasma sector peer, its 20% decline over the same period shares the industry-level pressure on collection costs and immunoglobulin pricing. The 30-percentage-point gap between Grifols and CSL represents the idiosyncratic premium the market is attaching to CSL’s specific combination of impairments, serial guidance resets, leadership instability, and demerger uncertainty. That gap is the market pricing company-specific risk, and investors attributing all of the decline to macro conditions may be underestimating it.

The sell-side is split: approximately 60% Buy (with conditions attached) and 40% Hold or Sell. That split itself signals genuine uncertainty, not a green light.

Analyst consensus targets range from approximately A$193 to A$241, with RBC Capital Markets at A$274 (Outperform) and Bell Potter at A$240 (Hold). Against a current price of A$119.88, even the most conservative target implies significant upside, illustrating the scale of scepticism the market is expressing relative to broker frameworks.

For the recovery thesis to hold, several conditions would need to materialise:

RBC Capital Markets targets A$274. Motley Fool Australia has flagged the possibility of shares surpassing A$265 if near-term headwinds ease. At 14.7x trailing earnings, the bull case rests on the proposition that this is a once-in-a-decade entry for a structurally sound business.

The lower re-rating floor holds if the following conditions persist:

Bear case floor targets sit around A$150 with a 20% impairment buffer applied. CSL’s dividend yield below 1.5% offers limited income support during the wait, a material consideration for retail and self-managed superannuation fund (SMSF) investors whose holding cost is real.

Investors wanting to stress-test the recovery timeline against specific pipeline and divisional data will find our deep-dive into CSL’s pipeline assets and FY27 targets, which examines Andembry’s peak sales forecast of approximately A$1.5 billion by FY30, the 15% year-on-year increase in Seqirus pre-orders for the 2026-2027 flu season, and the 12-15% FY27 NPATA growth target that underpins the consensus price range.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The next 6-12 months of disclosures will be more decisive than any current point estimate of fair value. Four specific catalysts will most clearly resolve the bull-bear ambiguity:

CSL’s ASX announcements page remains the recommended source for the latest disclosures.

CSL at 14.7x trailing earnings looks statistically cheap against its own history of 30-40x. Statistical cheapness and fundamental cheapness, however, are different things when the earnings base itself is under active revision.

The consensus average analyst target of approximately A$193-A$241 implies significant upside from A$119.88. Even Bell Potter’s Hold-rated target of A$240 implies more than 100% upside, a figure that speaks less to analyst conviction and more to the scale of the market’s scepticism about whether those frameworks still hold.

Some analysts have expressed a preference for other ASX growth names with clearer paths to earnings expansion, a legitimate framing for investors who are not compelled to hold a name simply because it has fallen far.

The relevant question is not whether CSL is cheap relative to last year. It is whether the structural quality of the business that justified a decade of premium valuation is still intact. There is no mechanical floor in a stock where impairments are ongoing, leadership is transitional, and guidance credibility has been damaged. The floor forms when a credible new earnings narrative is established, and that narrative has not yet arrived.

These statements are speculative and subject to change based on market developments and company performance.

A guidance reset occurs when a company formally revises its earnings or revenue forecasts downward, signalling that prior expectations were too optimistic. For CSL, multiple resets within a short timeframe have compounded credibility concerns, because each reset makes the next forecast harder for the market to trust.

CSL shares have declined approximately 50% over the past 12 months due to a combination of roughly A$5 billion in pre-tax impairments tied to the Vifor acquisition, serial guidance resets, a reported NPAT decline of 81% to $401 million for H1 FY26, and a leadership transition following the retirement of CEO Paul McKenzie.

The approximately A$5 billion in pre-tax impairments primarily relates to Vifor intangibles and underutilised physical assets, representing a formal management acknowledgement that the acquisition price assumptions made in 2022 were too optimistic. This raises ongoing questions about whether remaining asset valuations on the balance sheet are credible.

Key catalysts include the appointment of a permanent CEO to replace interim Gordon Naylor, whether FY26 full-year results meet or again reset guidance, concrete progress on the Seqirus demerger, and whether any further impairment disclosures emerge beyond the current A$5 billion cycle.

CSL now trades at approximately 14.7x trailing earnings, near a 10-year low, compared to a historical price-to-earnings ratio that once exceeded 40x. Analyst consensus forward price-to-earnings sits at roughly 15-18x FY27 NPATA, reflecting the market's reassessment of the company's growth and earnings quality.