10 Approved Rivals, Yet S&P Global’s Moat Keeps Compounding

59 mins ago

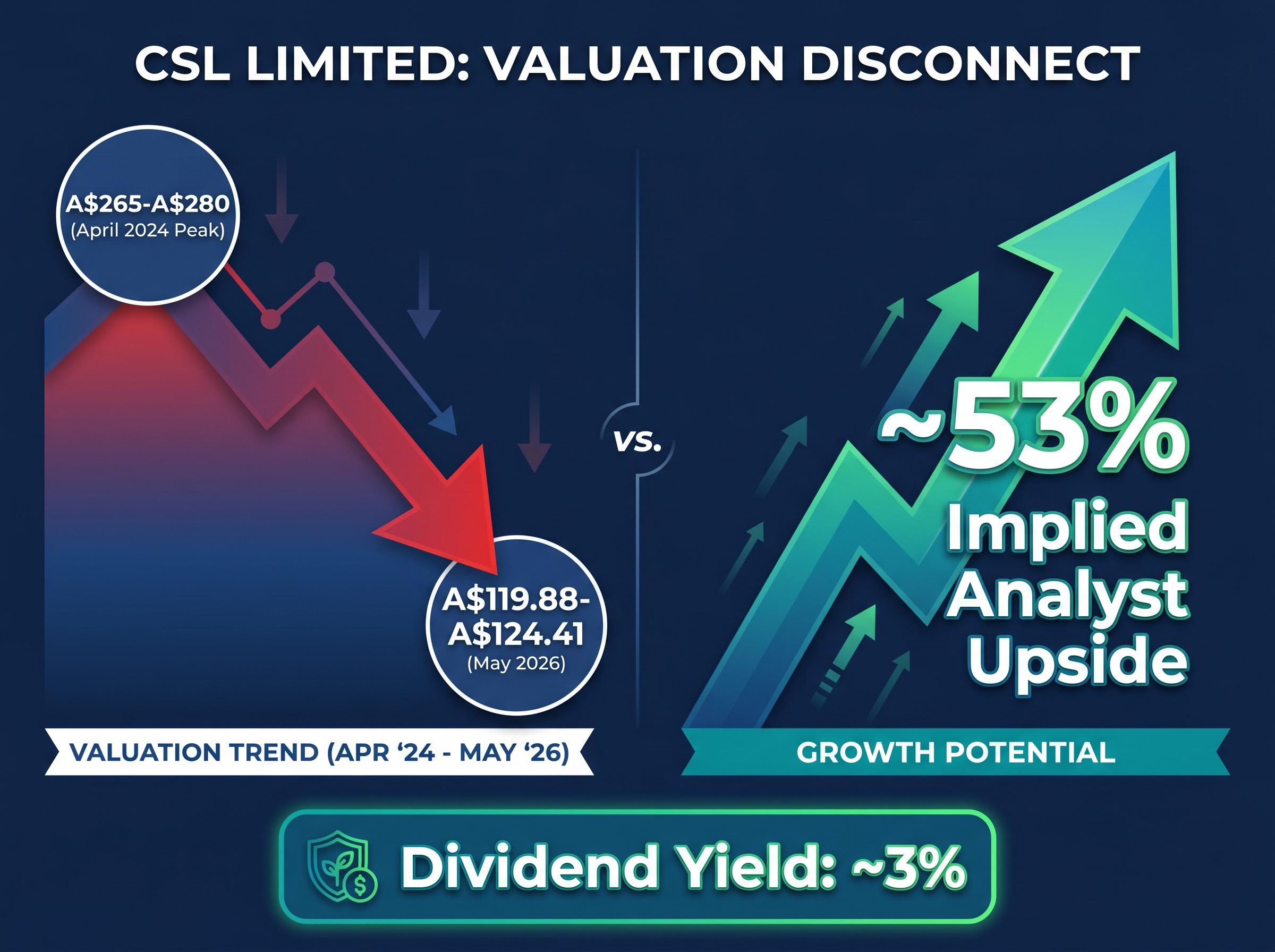

CSL Limited has shed roughly half its value from its April 2024 peak and now trades near decade lows around A$120. Yet more than half the analysts covering the stock carry their strongest positive rating, with the consensus implying approximately 53% upside from current levels. That gap, between where the market prices CSL and where professional coverage says it should trade, is the tension at the centre of any investment decision on the stock in 2026.

The disconnect reflects genuine disagreement about whether CSL’s problems are cyclical and fixable or structural and persistent. On one side: an FY26 earnings guidance downgrade, a mid-cycle CEO departure, and a vaccines division under pressure from a weak flu season. On the other: an FDA-approved rare disease therapy, a US$1.5 billion plasma capacity expansion, and durable immunoglobulin demand underpinned by patient populations with no therapeutic alternatives. What follows is a structured analytical framework for evaluating the CSL recovery thesis, identifying where the legitimate execution risks sit, and specifying the concrete developments that would confirm or invalidate the bull case.

A 50% drawdown from a household name does not, by itself, constitute a thesis. The analytical question is whether the decline reflects a temporary compression of the multiple investors are willing to pay, a deterioration in the underlying earnings trajectory, or some combination of both. In CSL’s case, the answer is both, and untangling them is where position-sizing discipline begins.

The current valuation snapshot:

Analyst consensus implies approximately 53% upside from current levels. That figure is a useful data point, not a buy signal. Consensus targets embed assumptions about cost programme execution, Seqirus recovery, and leadership continuity that remain untested against incoming results.

A P/E of 33-35x is not cheap by broad market standards. It has re-rated significantly from the 40x-plus multiples CSL commanded at its peak, but it still carries a premium that requires a credible earnings recovery to justify. Investors drawn to the stock by name recognition and a halved price need to ask a harder question: does the earnings trajectory support the remaining premium, or is further compression possible?

Scenario-based valuation frameworks that assign explicit probability weights to bull, base, and bear cases are particularly useful when analyst consensus implies large upside but near-term earnings guidance sits well below the level required to justify the existing multiple, because the blended value calculation forces an investor to be explicit about which future they are actually paying for.

The bullish case for CSL starts with CSL Behring, and it starts there for a reason that goes beyond revenue contribution. Plasma-derived therapies treat patients with chronic rare disease conditions, primarily immunodeficiencies, who have no therapeutic substitutes. These are not elective treatments. Demand is insulated from discretionary spending cycles in a way that few pharmaceutical categories can match.

Behring reported H1 FY26 revenue of approximately A$5.2 billion, representing approximately 9% year-on-year growth. That growth came despite broader earnings pressure across the group, underscoring the division’s role as the structural floor beneath CSL’s investment case.

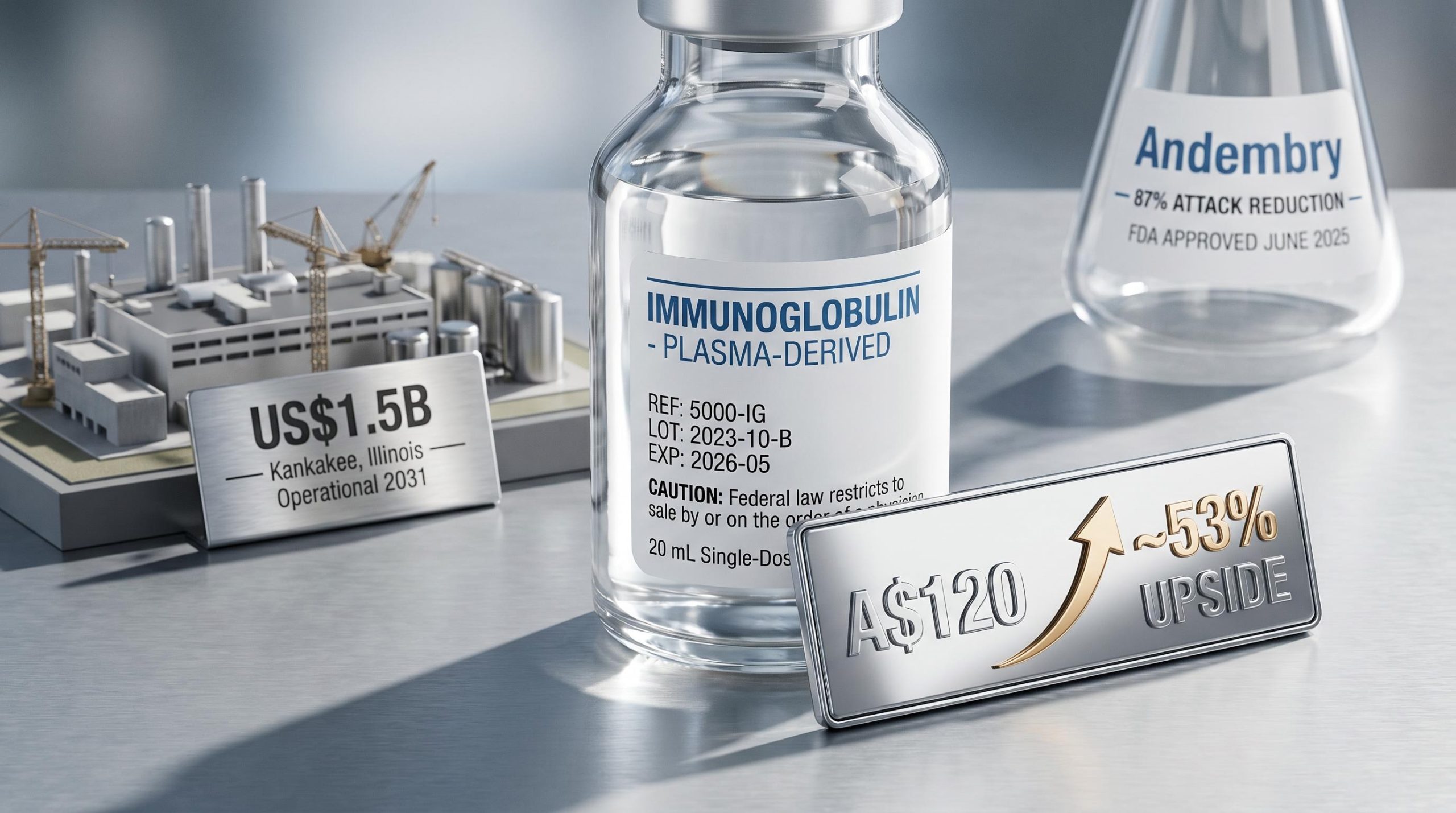

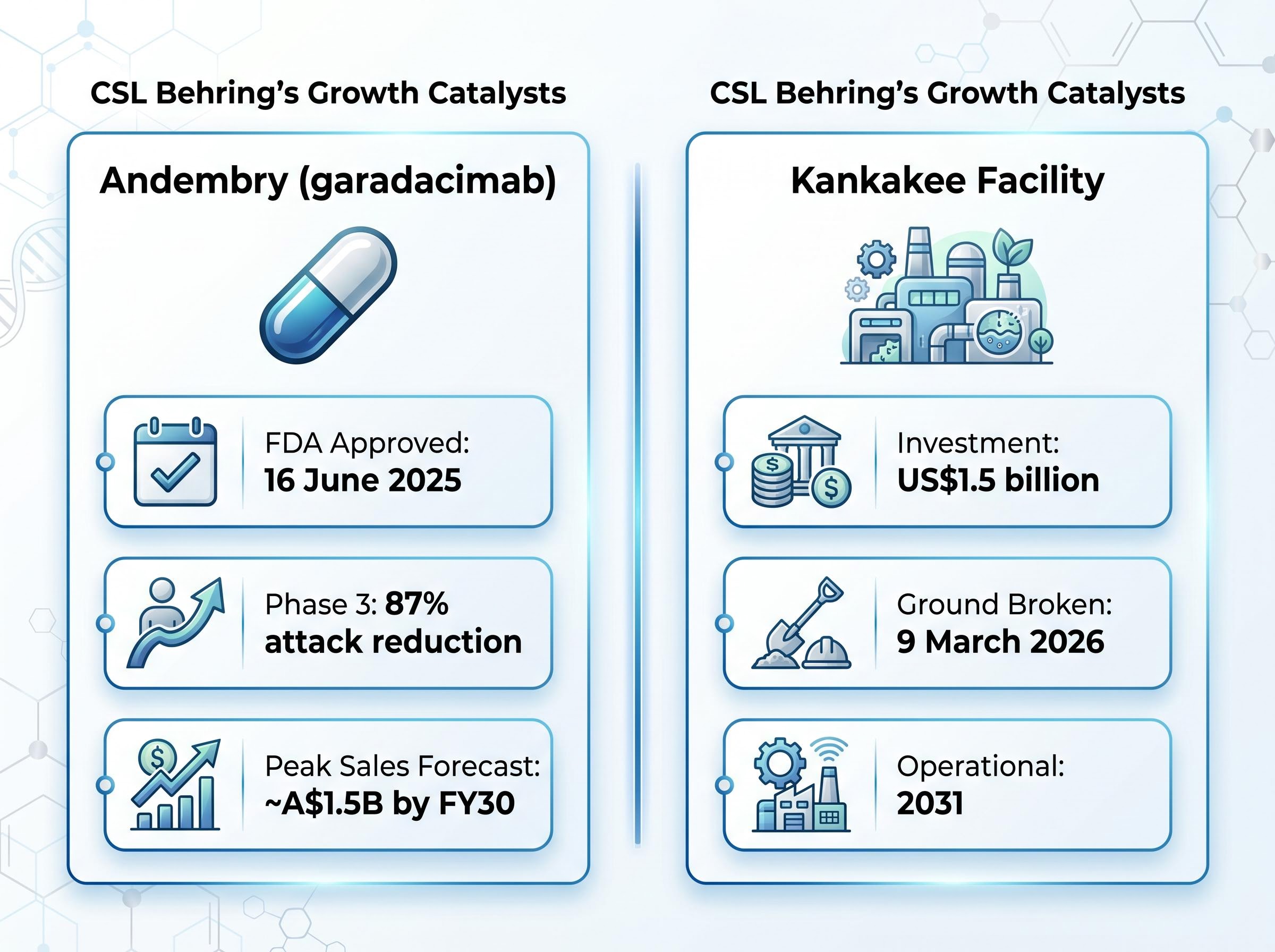

Two specific catalysts reinforce the forward view. Garadacimab, marketed as Andembry, received FDA approval on 16 June 2025 for prophylactic treatment of hereditary angioedema (HAE). It is the only prophylactic HAE treatment targeting Factor XIIa with once-monthly dosing from initiation, and Phase 3 data demonstrated an 87% attack reduction. Peak sales are forecast at approximately A$1.5 billion by FY30.

The second is a capacity commitment. CSL broke ground on 9 March 2026 on a US$1.5 billion expansion of its Kankakee, Illinois manufacturing facility. The facility is expected to be operational by 2031, meaning it contributes nothing to near-term earnings but signals long-run confidence in plasma demand growth.

| Asset | Indication | Status | Key data point | Milestone |

|---|---|---|---|---|

| Andembry (garadacimab) | Hereditary angioedema | FDA approved (June 2025) | 87% attack reduction (Phase 3) | Peak sales ~A$1.5B by FY30 |

| Kankakee facility | Plasma capacity expansion | Under construction | US$1.5B investment | Operational 2031 |

| Privigen (IVIG) | CIDP, motor neuropathy | Label expansions pending | ~42% global Ig market share | Verification required |

CSL Behring holds approximately 42% of the global immunoglobulin market, a position aided by a competitor shortage affecting Octagam. That concentration provides pricing power, but it also means the division is the primary target for competitive entry.

A separate regulatory development has removed one near-term risk from the picture: CSL secured a tariff exemption for plasma-derived therapies under the U.S. Section 232 pharmaceutical import proclamation, protecting the highest-value portion of its U.S. Behring revenue from import duties effective September 2026, though Seqirus’ Fluad vaccine faces a residual 10% tariff due to its UK manufacturing origin.

Grifols launched a biosimilar IVIG product in the U.S. in February 2026, creating an estimated approximately 5% pricing headwind for the IVIG segment. This is a legitimate but bounded risk. At 42% global share, CSL Behring retains sufficient scale to absorb moderate pricing pressure without a structural margin collapse. The headwind is worth monitoring across reporting periods, not worth treating as an existential threat to the division’s economics.

Seqirus is the division that explains most of the gap between CSL’s structural quality and its current market price. It is also the division most sensitive to factors the company does not control, which makes it simultaneously the most visible source of near-term pain and the most difficult to forecast with confidence.

Headwinds:

Tailwinds:

Seqirus pre-orders for 2026/27 are up approximately 15% year-on-year. This is the most concrete forward-looking signal that the demand trough may be passing, though it remains subject to actual flu season severity.

The company has guided for 5-10% revenue growth in FY27 for the division, with breakeven as the stated target. Whether that target is achievable depends heavily on whether vaccination rates normalise and whether CSL can hold share against Sanofi and GSK in a competitive market. Investors should calibrate how much of the stock’s depression is Seqirus-specific pain versus how much would persist even under a divisional recovery scenario.

Paul McKenzie retired as CEO on 10 February 2026. Gordon Naylor was appointed interim CEO the following day. The speed of the transition was notable; the absence of a permanent successor is more so.

Strategic direction under an interim CEO is inherently less certain than under a permanent appointment. Naylor has not publicly reaffirmed the financial targets McKenzie laid out before his departure, which included NPATA growth of 12-15% in FY27, accelerating to 15%+ in FY28, and a margin rebuild to 32% by FY28 from approximately 28% in FY26. Those targets should be treated as analyst reference points, not as commitments, until explicitly reaffirmed by confirmed permanent leadership.

The restructuring programme adds a further layer of uncertainty. CSL has confirmed restructuring activity including Seqirus facility closures and headcount reductions. However, the specific US$550 million cost reduction programme figure cited in some analyst commentary could not be verified against primary ASX filings. Investors should treat that figure with caution until confirmed through official disclosures.

FY26 NPATA growth guidance has been downgraded to 4-7%, the earnings-level evidence of near-term pressure.

Before committing to the recovery thesis, an investor should verify three things:

FY27 NPATA guidance, when issued under confirmed permanent leadership, will be the single most important data point for validating or invalidating the recovery thesis. If the guidance lands materially below the 12-15% range McKenzie targeted, the bull case loses its earnings anchor. If it confirms or exceeds that range, the market will need to re-price the stock’s recovery timeline.

Large-cap healthcare recovery situations tend to share three characteristics: structural demand durability (which supports the floor), near-term divisional drag (which creates the discount), and execution uncertainty (which determines the timeline). CSL exhibits all three, and recognising the pattern helps an investor separate what is knowable from what requires patience.

The distinction that matters most is between what the company controls and what it does not.

| Category | Inside company control | Outside company control |

|---|---|---|

| Earnings trajectory | Cost programme, margin rebuild | Flu season severity, vaccination rates |

| Revenue growth | Capacity investment, portfolio mix | Biosimilar pricing pressure |

| Leadership | Permanent CEO appointment | Market confidence, board dynamics |

| Competitive position | Andembry commercialisation | Regulatory timelines, competitor launches |

The metrics to track across reporting periods:

The Kankakee expansion reaching operational status in 2031 and Andembry peak sales arriving around FY30 are reminders that the capacity-driven upside is a five-year story. The dividend yield of approximately 3% at A$120, with no suspension confirmed, provides a partial return floor for patient capital while longer-horizon catalysts develop.

The bull case is specific: Behring growing at approximately 9% with a new FDA-approved rare disease asset approaching commercialisation, Seqirus showing forward order recovery, and a stock priced at roughly half its peak level. The analyst consensus, with more than 50% on their strongest positive rating and approximately 53% implied upside, reflects the view that CSL’s structural assets are being materially underpriced.

CSL’s FDA approval announcement for Andembry confirms the therapy covers patients aged 12 years and older, with pivotal Phase 3 VANGUARD trial data showing a median HAE attack reduction exceeding 99% and 62% of patients remaining entirely attack-free across the study period — clinical differentiation that supports the peak sales forecast underpinning the bull case.

The bear case is equally specific: interim leadership with no confirmed successor, a restructuring programme whose scope cannot be verified against primary filings, a downgraded FY26 earnings year (4-7% NPATA growth), biosimilar pricing pressure in a core product category, and capacity upside that does not materialise until 2031.

| Dimension | Bull case | Bear case |

|---|---|---|

| Earnings trajectory | FY27 NPATA growth 12-15% | FY26 guidance at 4-7%; FY27 unconfirmed |

| Leadership | Naylor stabilises; permanent CEO appointed | Interim uncertainty persists; targets unaffirmed |

| Divisional outlook | Behring 9%+ growth; Seqirus pre-orders recovering | Seqirus breakeven delayed; biosimilar headwinds |

| Valuation | ~53% analyst upside; 3% yield floor | 33-35x P/E still requires recovery to justify |

The core tension: analyst consensus implies approximately 53% upside, yet FY26 earnings growth guidance sits at just 4-7%. The gap between those two numbers is the recovery thesis itself, and it remains unproven.

Three developments would meaningfully shift the probability distribution: a permanent CEO appointment with explicit reaffirmation of forward targets, FY27 NPATA guidance landing within or above the 12-15% range, and a Seqirus H2 FY26 result showing divisional losses narrowing. Balance sheet, leverage, and peer comparison data require primary source verification before a full position assessment can be completed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The structural demand case for plasma therapies is durable. Patients with chronic immunodeficiencies require ongoing treatment, and CSL Behring’s market position, pipeline, and capacity investment all point in the same direction. The directional case for recovery is credible.

The timing case is less clear. The confirming catalysts, a permanent CEO, FY27 guidance under settled leadership, and demonstrable Seqirus improvement, may be one to three reporting periods away. Andembry peak sales are an FY30 horizon. The Kankakee facility reaches operation in 2031. A 3% dividend yield provides some income while capital appreciation remains unrealised.

The investor’s practical task is not to decide whether CSL recovers. It is to decide how much timing risk is acceptable given that the confirming signals have not yet arrived.

Near-term catalysts to monitor before reassessing position sizing:

The next major data event will be the full-year FY26 result and any leadership update from the board. At that point, the thesis either gains concrete grounding or requires reassessment.

CSL has shed roughly half its value from its April 2024 peak due to a combination of factors including a downgraded FY26 earnings guidance (4-7% NPATA growth), a mid-cycle CEO departure, and pressure on its Seqirus vaccines division from a weak flu season and falling U.S. vaccination rates.

Andembry (garadacimab) is CSL's FDA-approved therapy for hereditary angioedema, approved in June 2025, and is the only prophylactic treatment targeting Factor XIIa with once-monthly dosing. Phase 3 trial data showed a median HAE attack reduction exceeding 99%, with peak sales forecast at approximately A$1.5 billion by FY30.

More than 50% of analysts covering CSL carry their strongest positive rating, and the consensus price target implies approximately 53% upside from current levels around A$120; however, that target depends on assumptions about cost programme execution, Seqirus recovery, and permanent leadership confirmation that remain unproven.

Paul McKenzie retired as CEO in February 2026 and was replaced by interim CEO Gordon Naylor, who has not publicly reaffirmed forward targets including 12-15% NPATA growth in FY27 and a margin rebuild to 32% by FY28, meaning investors should treat those figures as analyst reference points rather than confirmed commitments until permanent leadership is in place.

Investors should watch for three key developments: a permanent CEO appointment with explicit reaffirmation of FY27-FY28 financial targets, FY27 NPATA guidance landing within or above the 12-15% range, and a Seqirus H2 FY26 divisional result showing losses narrowing toward the stated FY27 breakeven target.