CBA Share Price Crashes 10% on Budget and Provision Shock

1 hr ago

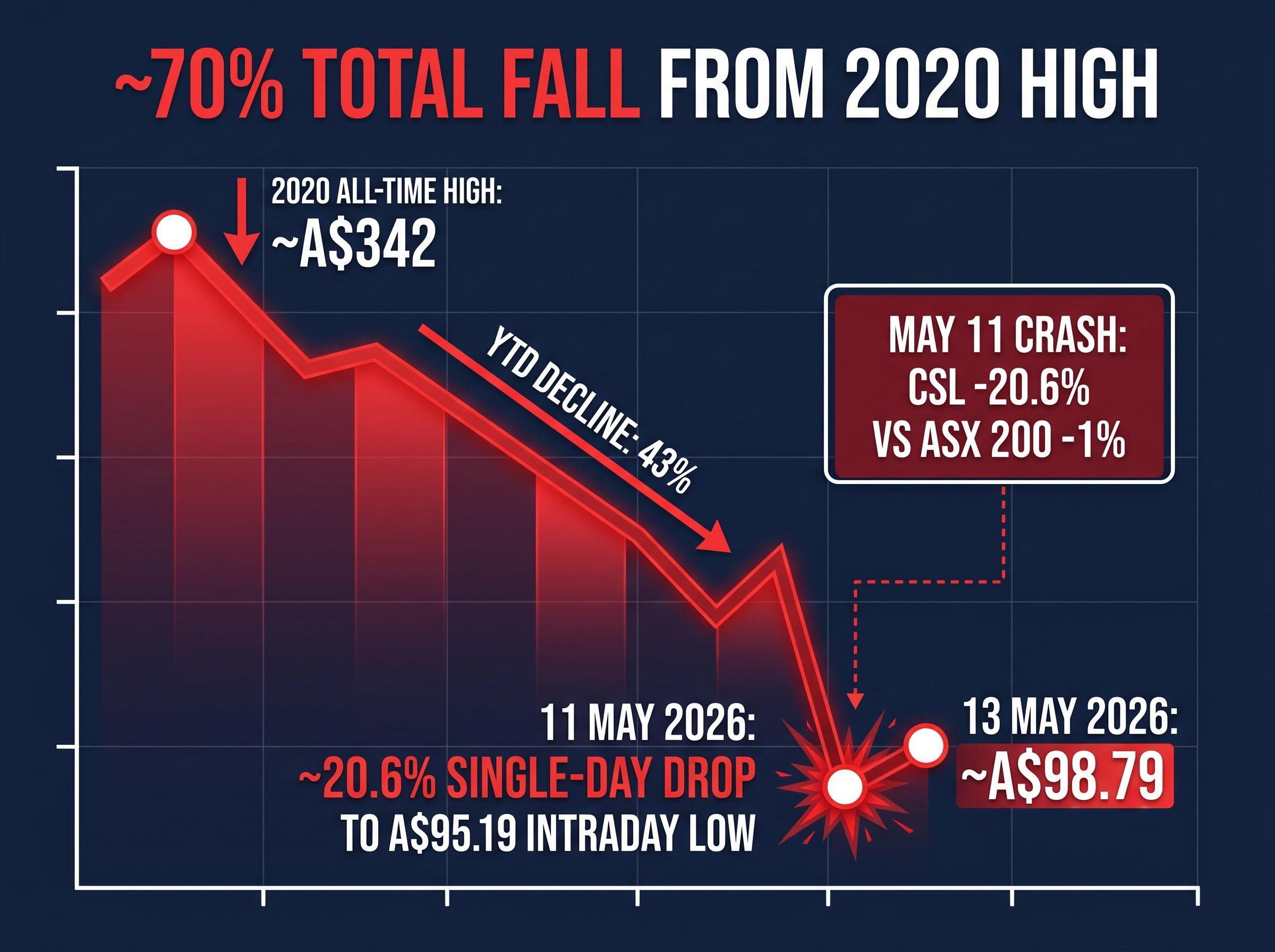

On 11 May 2026, CSL Limited shed more than 20% of its value in a single trading session, dragging the ASX 200 lower and marking what some market commentators are already calling the worst chapter in the company’s listed history. CSL has long been considered one of the ASX’s premier blue-chip growth stocks, so a 43% year-to-date decline to a near 9.5-year low demands explanation. The selloff was triggered by a company-specific guidance cut, not a sector-wide shock, which means the question investors now face is whether the underlying business remains structurally sound or whether something more fundamental has broken.

This analysis unpacks the specific catalysts behind the crash, walks through CSL’s three operating divisions, examines the income statement and balance sheet metrics that matter, and frames what the numbers actually tell a finance-educated Australian investor weighing whether this is a value opportunity or a value trap.

The scale of the event sets the context. On 11 May 2026, CSL fell approximately 20.6% to an intraday low of A$95.19, a record single-session decline described as the second worst trading day in the company’s history. The ASX 200 fell only about 1% on the same day, with CSL as the dominant drag, confirming that this was a business-specific event rather than a market-wide shock.

CSL’s single-day decline of approximately 20.6% on 11 May 2026 was the largest in the company’s listed history, wiping billions from its market capitalisation in a matter of hours.

The proximate trigger was a guidance update delivered as part of interim CEO Gordon Naylor’s 90-day strategic review. FY26 revenue guidance was set at approximately US$15.2B, a year-on-year decline from FY25’s US$15.6B, the first such decline in recent memory. FY26 NPATA guidance came in at approximately US$3.1B, down from the FY25 actual of US$3.3B.

Two specific revenue headwinds were cited:

As of 13 May 2026, the CSL share price sat at approximately A$98.79, a near 9.5-year low last seen around 2016.

Alongside the earnings downgrade, CSL flagged an impairment charge of approximately US$5B (more than A$7.5B) on its CSL Vifor assets. Vifor was acquired in 2021 for approximately US$14.5B, and the division has become a material drag on group performance. The impairment is excluded from NPATA but flows directly through the reported balance sheet.

Competitive pressures in nephrology and broader softness in the iron deficiency treatment market provide the operational context for the write-down. Market commentary has widely characterised the acquisition as overpaying for an asset that has failed to deliver expected returns.

The CSL Vifor impairment announced on 11 May 2026 encompasses not only the charges flagged in the strategic review but also additional write-downs flagged across FY26 and FY27, with the full scope of asset deterioration extending beyond what a single guidance update can fully capture.

Investors who treat CSL as a single “biotech bet” miss the structural reality that its three divisions carry entirely different risk profiles, growth dynamics, and margin characteristics. Understanding the business from the ground up is necessary before assessing the financial headwinds.

| Division | Core Focus | Key Revenue Driver |

|---|---|---|

| CSL Behring | Blood plasma-derived products | Immunoglobulin and albumin sales globally |

| CSL Seqirus | Influenza vaccines and pandemic preparedness | Government contracts and seasonal vaccine programmes |

| CSL Vifor | Iron deficiency and nephrology treatments | Specialty pharmaceutical sales (acquired 2021) |

CSL Behring, incorporated in 2004, is the largest and most revenue-critical division. It manufactures and distributes plasma-derived therapies, and its immunoglobulin and albumin revenue lines were the specific products cited in the May 11 guidance cut. Management confirmed that underlying US immunoglobulin demand growth remains in the mid-to-high single digits, but channel inventory normalisation is masking that strength in reported figures.

CSL Seqirus operates the influenza vaccine and pandemic preparedness arm, with government contract exposure creating a revenue profile that behaves differently from plasma economics.

CSL Vifor, acquired for approximately US$14.5B in 2021, was intended to diversify CSL into nephrology and iron deficiency treatments. The US$5B impairment announced on 11 May 2026 reflects how far the reality has drifted from that strategic rationale.

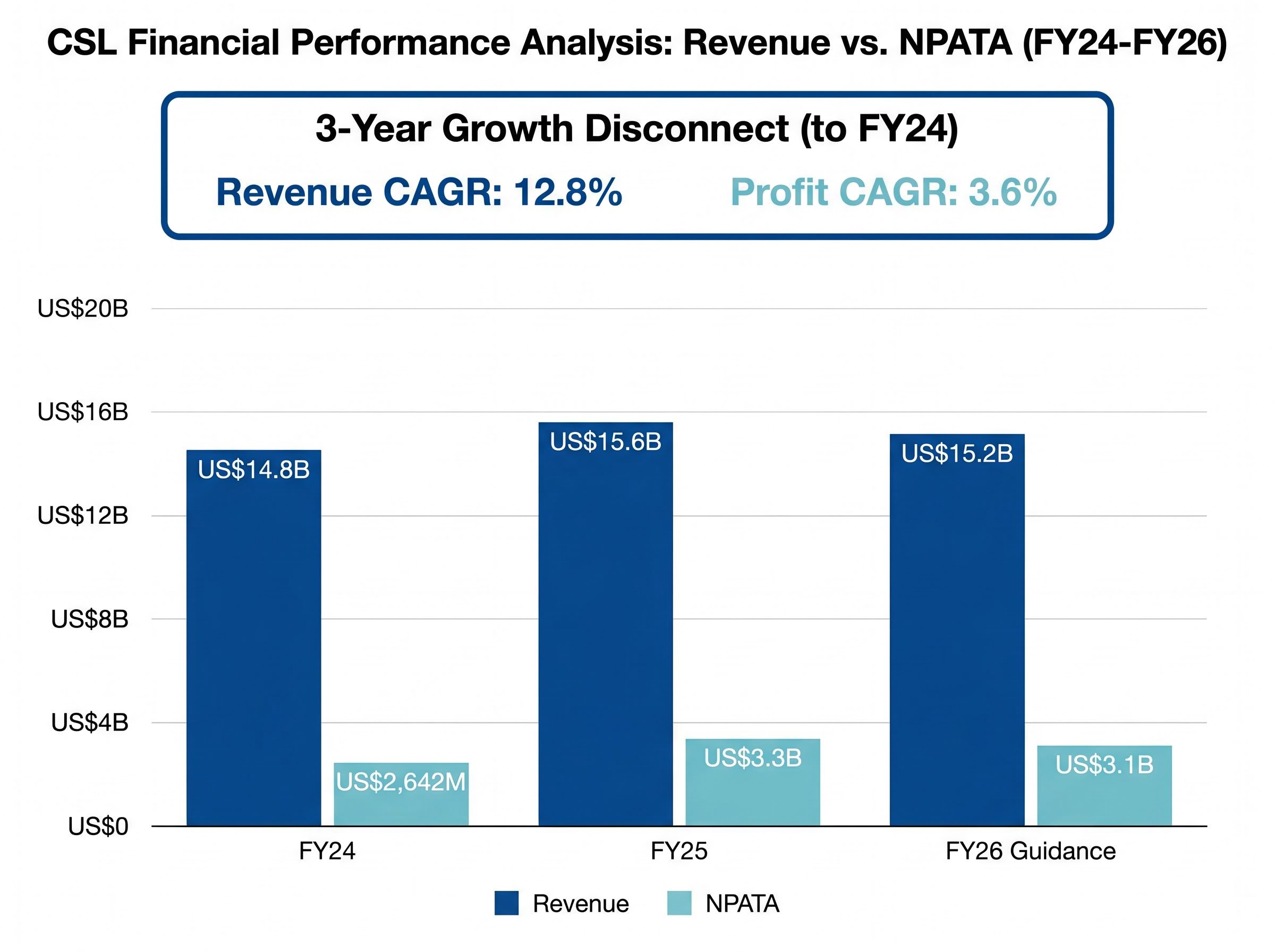

The tension in CSL’s income statement is visible before any analyst commentary frames it. The numbers speak clearly when placed side by side.

| Metric | FY24 | FY25 | FY26 Guidance |

|---|---|---|---|

| Revenue | ~US$14.8B | US$15.6B | ~US$15.2B |

| NPATA | ~US$2,642M | US$3.3B | ~US$3.1B |

| Gross Margin | 52.1% | Not disclosed | Not disclosed |

Over the three years to FY24, CSL delivered a revenue compound annual growth rate (CAGR) of 12.8% per annum. In the same period, net profit grew at just 3.6% per annum.

A revenue CAGR of 12.8% alongside a profit CAGR of only 3.6% is the financial signature of a business where costs have been growing faster than revenues, a pattern the FY26 guidance extends rather than reverses.

Gross margin, which measures profitability before overhead deductions, stood at 52.1% in FY24. While no updated figure has been disclosed, the combination of US immunoglobulin channel disruption and China albumin value decline suggests further compression is likely.

FY26 guidance implies both revenue decline (from US$15.6B to US$15.2B) and profit decline (from US$3.3B to US$3.1B in NPATA). Margin recovery is now the central question any investor must answer before forming a view on CSL.

The income statement tells what CSL earns. The balance sheet reveals the obligations sitting underneath those earnings, and it is here that the Vifor acquisition exerts its most direct pressure.

Three metrics frame the balance sheet picture:

A US$5B goodwill or asset impairment flows through to a reduction in total assets and retained earnings, compressing reported equity. This means debt-to-equity ratios will be more elevated on a post-impairment basis than the 62.8% pre-impairment figure implies.

Investors should treat the 62.8% figure with caution until post-impairment balance sheet figures are disclosed. The interaction between US$10.5B in net debt, a US$5B equity reduction, and declining earnings creates a structural risk that determines whether any earnings recovery, if it materialises, can actually translate into shareholder value.

The May 2026 guidance cut did not arrive in isolation. It is the latest in a sequence of earnings misses and expectation resets that has defined CSL’s trajectory since mid-2024.

The cumulative market verdict on this sequence is severe. CSL has fallen approximately 70% from its 2020 all-time high of approximately A$342 to its current level near A$98.79.

Serial guidance resets across August 2025, October 2025, and February 2026 preceded the May announcement, meaning the credibility deficit the market is now pricing was already building across multiple earnings cycles before the record single-day decline occurred.

Market Index has described the decline as potentially “the ASX’s biggest ever blue chip disaster,” a framing that reflects the magnitude of the re-rating rather than a forward-looking assessment.

Intelligent Investor (reporting on 13 May 2026) noted the extreme discount implied by current pricing versus historical peaks but stopped short of issuing a buy recommendation. The pattern of management asserting that growth initiatives are delivering, only for reported results to fall short, is the structural credibility problem that has driven each successive leg lower.

For Australian retail investors, the question is not whether CSL was once a great business. It almost certainly was. The question is whether a 43% price decline reflects a valuation reset of a fundamentally intact operation, or whether repeated guidance misses signal a more structural deterioration in the earnings model that lower prices alone cannot fix.

At A$98.79, CSL is priced at levels last seen in 2016, but the business in 2026 carries far more debt, a troubled acquisition on the books, and a management team with a credibility deficit to rebuild.

Analyst price targets for CSL range from approximately A$109 (UBS, Sell) to A$141 (Morgan Stanley, Equal Weight) as of mid-May 2026, a spread that reflects genuine uncertainty about whether the plasma franchise re-rating is complete or whether further earnings resets remain ahead.

Structural positives to monitor:

Unresolved risks to track:

The gap between what is known and what remains uncertain is wide enough to warrant specific monitoring before forming an investment view.

First, the permanent CEO appointment and accompanying strategic plan release will be the first meaningful credibility signal. Second, the post-impairment balance sheet disclosure (expected with FY26 full-year results) will be the moment to reassess leverage ratios with accurate figures. Third, the US immunoglobulin channel inventory clearance timeline, which management has flagged as temporary but has not quantified in terms of resolution period, will determine whether the largest revenue headwind is genuinely transient.

Investors exploring whether the current price level represents a genuine entry point will find our dedicated guide to falling knife entry signals examines six specific technical conditions, including 200-day moving average position, lower-low lower-high structure, and volume capitulation, and documents why none of those conditions were met as of 14 May 2026.

The financial metrics show a business with real scale and historical revenue growth. They also show margin compression, elevated debt, a costly acquisition write-down, and a sequence of credibility-damaging guidance misses that make near-term re-rating uncertain.

This analysis provides a structured starting point, not a complete investment thesis. Valuation analysis, including price relative to earnings, peer benchmarking against plasma and biotech companies such as Grifols and Takeda, and comparison to historical multiples, is the necessary next layer of work for investors considering whether current pricing represents opportunity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

CSL shares fell approximately 20.6% on 11 May 2026 after interim CEO Gordon Naylor's 90-day strategic review produced a FY26 guidance cut, a US$5B impairment on the Vifor acquisition, and flagged a combined US$500M revenue headwind from US immunoglobulin channel inventory normalisation and China albumin market value decline.

CSL Vifor is a nephrology and iron deficiency treatment division acquired by CSL in 2021 for approximately US$14.5B. The US$5B impairment reflects competitive pressures in nephrology and broader softness in the iron deficiency treatment market, with market commentary widely characterising the acquisition as overpaying for an asset that failed to deliver expected returns.

NPATA stands for net profit after tax and amortisation, a measure that excludes large non-cash amortisation charges typically associated with acquired intangible assets, making it a cleaner comparison of underlying operating earnings. For CSL, FY26 NPATA guidance is approximately US$3.1B, down from the FY25 actual of US$3.3B, while the US$5B Vifor impairment flows through the reported balance sheet rather than NPATA.

CSL has fallen approximately 70% from its all-time high of approximately A$342 reached in 2020 to its current level near A$98.79 as of mid-May 2026, representing a 43% year-to-date decline in 2026 alone and a price level last seen around 2016.

Three key signals to monitor are the permanent CEO appointment and accompanying strategic plan, the post-impairment balance sheet disclosure expected with FY26 full-year results, and the timeline for US immunoglobulin channel inventory clearance, which management has described as temporary but has not quantified in terms of resolution period.