Samsung Posts Record AI Chip Profit, Then Its Stock Falls 6%

7 mins ago

The S&P/ASX 200 Health Care Index has collapsed 39% over the past year, reaching a six-year low of 25,193 points in late April 2026 while the broader ASX 200 edged modestly higher. That divergence is not an accident.

Australian healthcare stocks were once considered defensive, steady earners. The past 12 months have exposed how vulnerable the ASX healthcare sector becomes when multiple headwinds arrive simultaneously: a surging Australian dollar, back-to-back RBA rate hikes, a collapse in consumer confidence, corporate governance shocks, and geopolitical disruption compressing margins from the cost side. No single force explains a 39% decline. The compounding of all five does.

What follows unpacks each of these forces, examines what individual stock performance reveals about which companies are most exposed to each driver, and explains why Ramsay Health Care has managed to post an 18% gain while every other top-ten name has bled.

The XHJ stood at approximately 26,154 as of 5 May 2026, down 39% over 12 months. Over the same period, the ASX 200 sat at 8,697.10, up modestly. No other sector on the ASX 200 comes close to that degree of underperformance; the technology sector, the next worst performer, declined approximately 26%.

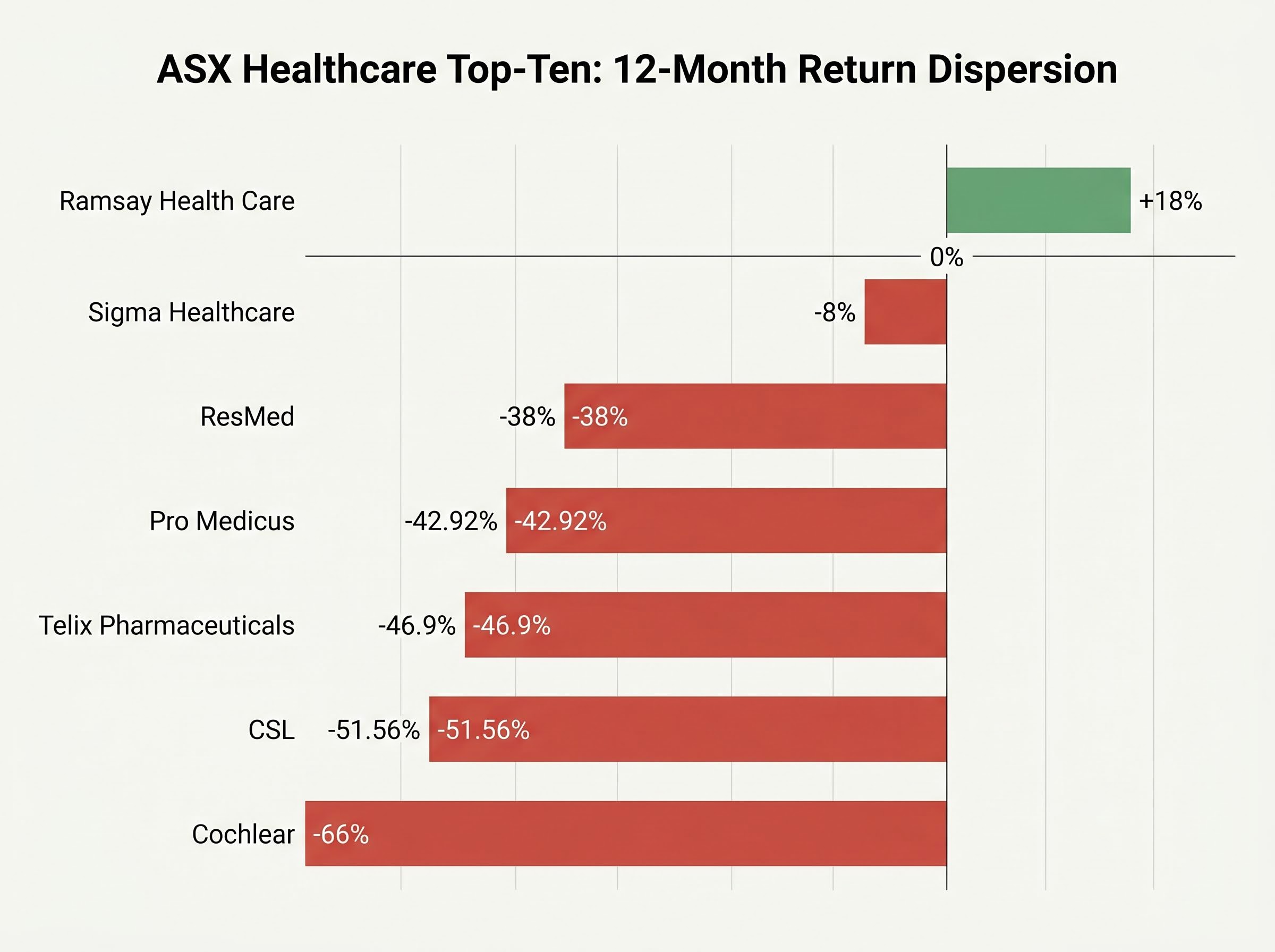

But the headline number obscures a structural reality. CSL constitutes approximately 45% of the XHJ’s weighting. Its 51.56% 12-month decline, the steepest of any top-ten constituent, functions as an index-level wrecking ball.

CSL constitutes approximately 45% of the ASX 200 Health Care Index, making its 51.56% decline the single largest mechanical drag on the XHJ.

Strip CSL out, and the decline is still severe. But it is no longer a uniform 39% story. The dispersion across the top ten reveals which companies are caught in specific headwinds and which are weathering them.

| Company | 12-month return (approx.) |

|---|---|

| CSL | -51.56% |

| Cochlear | -66% |

| Telix Pharmaceuticals | -46.9% |

| Pro Medicus | -42.92% |

| Sonic Healthcare (SHL) | Negative |

| ResMed | -38% |

| Ansell | Negative |

| Sigma Healthcare | -8% |

| Fisher & Paykel Healthcare | Negative |

| Ramsay Health Care | +18% |

One company posted a positive return. The rest are spread across a range from -8% to -66%. That spread is the signal: the sector’s pain is not uniform, and understanding why requires examining each driver individually.

The rate environment and the currency move are not parallel problems. They compound each other, and the companies sitting at the intersection of both have suffered the steepest declines.

The RBA raised the cash rate to 4.35% on 5 May 2026, implementing its second hike of the year. Market pricing implies a 76% probability of a further increase at the next meeting. The mechanism connecting rate hikes to healthcare stock declines is straightforward:

This sequence hits high-multiple names hardest. Pro Medicus, down 42.92%, and Telix Pharmaceuticals, down 46.9%, both traded on elevated earnings multiples heading into the rate cycle. Sigma Healthcare, a lower-multiple name, declined only 8% over the same period, illustrating how rate sensitivity tracks directly with valuation premium.

The Australian inflation data underpinning the RBA’s May decision showed headline CPI at 4.6% in March 2026, nearly double the top of the 2-3% target band, with Deputy Governor Hauser flagging a potential stagflation scenario if elevated inflation persists alongside slowing growth, a combination that would extend the rate plateau beyond current market pricing.

CSL, ResMed, and Cochlear generate substantial revenue in US dollars. When those US-dollar earnings are translated back into Australian dollars, a stronger AUD shrinks the reported figure.

The AUD/USD rate reached approximately 0.7169 as of 5 May 2026, a four-year high of 71.3 US cents over the 12-month period. That represents an appreciation of approximately 12%, directly eroding the Australian-dollar value of offshore revenue streams. For a company like CSL, where the majority of earnings originate overseas, a 12% currency headwind arrives on top of the rate-driven multiple compression, not instead of it.

Until either the RBA pivots or the AUD retreats, these twin forces will continue to cap recoveries in high-multiple and offshore-earning healthcare names.

Healthcare spending has long been considered non-discretionary. Cochlear’s February 2026 guidance downgrade tested that assumption directly.

Management revised FY26 underlying net profit guidance downward, from a prior range of $435-$460 million to $290-$300 million, citing deteriorating consumer confidence and historically low US consumer sentiment.

Cochlear FY26 guidance revision: Underlying net profit cut from $435-$460 million to $290-$300 million.

Shares fell approximately 35% following the announcement. Over 12 months, Cochlear is down approximately 66%, the worst performer among the top ten.

Australian consumer sentiment recorded its steepest monthly decline in five years in April 2026, compounding the pressure for companies with dual-market exposure.

Cochlear’s revenue depends on patients choosing to proceed with implant surgery. That decision requires both clinical availability and patient willingness to engage with an elective procedure carrying significant out-of-pocket costs. When household budgets tighten, hearing implants can wait.

The same demand sensitivity applies to other procedure-dependent medtech companies across the sector. The assumption that healthcare is immune to consumer belt-tightening holds for emergency care and essential medications. It does not hold for elective procedures priced at a premium.

CSL shares stood at approximately $124.83 as of 5 May 2026, an eight-year low and a 51.56% decline over 12 months. The damage traces back to a concentrated sequence of shocks from the February 2026 half-year results:

Shares fell approximately 12% in a single session. The cumulative impact, layered on top of the rate and currency headwinds already pressuring the stock, produced the steepest decline of any top-ten constituent.

CSL’s interim CEO appointment of Gordon Naylor, an internal candidate with 33 years of company experience, was structured explicitly to provide continuity during a permanent search rather than signal a strategic pivot, though the board’s choice of a Seqirus turnaround specialist carries its own implications for how management intends to address the division’s underperformance.

12 of 18 analysts rate CSL buy or strong buy, with an average price target of approximately $209.44 versus a current price of approximately $124.83.

CSL’s tariff exemption for plasma-derived therapies under the US Section 232 proclamation removed one potential earnings shock, but the protection does not extend uniformly across all product lines: CSL Seqirus’ Fluad vaccine faces a 10% levy tied to its UK manufacturing base, adding a further layer of complexity to an already-disrupted US business outlook.

Morgans noted CSL was trading at its cheapest valuation in 14 years. The gap between analyst targets and current price is either a measure of significant upside or a signal that consensus has not yet fully adjusted to a structurally different earnings outlook.

Because CSL constitutes nearly half the XHJ, its re-rating alone accounts for a substantial portion of the sector’s headline 39% decline. The sector-level number is, in part, a CSL story wearing a sector costume.

Two background risk factors are harder to quantify than rates or earnings, but they are creating a ceiling on any potential recovery.

Middle East geopolitical instability has elevated freight and logistics costs for healthcare operators, compounding already-strained margins alongside rising wages and constrained insurance reimbursement rates. The International Monetary Fund (IMF) has warned that a prolonged fuel crisis stemming from Middle East conflict could trigger a global recession.

Cochlear specifically flagged order cancellation risks and delivery disruptions to Middle Eastern markets for H2 FY26. The company also noted that reduced patient reimbursement rates in China are expected to weigh on premium product sales in the same period, a separate geographic headwind layered onto the freight-cost pressure.

Hospital operators like Ramsay face a margin squeeze from three simultaneous directions: higher freight costs, rising wages, and constrained reimbursement rates.

The US Food and Drug Administration (FDA) regulatory environment under the Trump administration has introduced a layer of pipeline risk for ASX-listed companies with significant US exposure. The specific concerns include:

FDA leadership instability in 2025-2026 has been characterised by an historic leadership exodus and a seesaw dynamic of deregulation across therapeutic categories, creating approval unpredictability that compounds the pipeline risk facing ASX-listed companies with significant US exposure.

Former CSL CEO Dr Paul McKenzie stated at the October 2025 Annual General Meeting (AGM) that the decline in US influenza vaccination rates exceeded the company’s expectations. A rare diseases advocacy group has reported that a large proportion of biotech companies faced capital-raising difficulties in the current environment.

These risks matter because they sit largely outside management control. Operational improvements alone cannot resolve them, which means a fundamental earnings turnaround may not be sufficient to re-rate the sector while macro and regulatory headwinds persist.

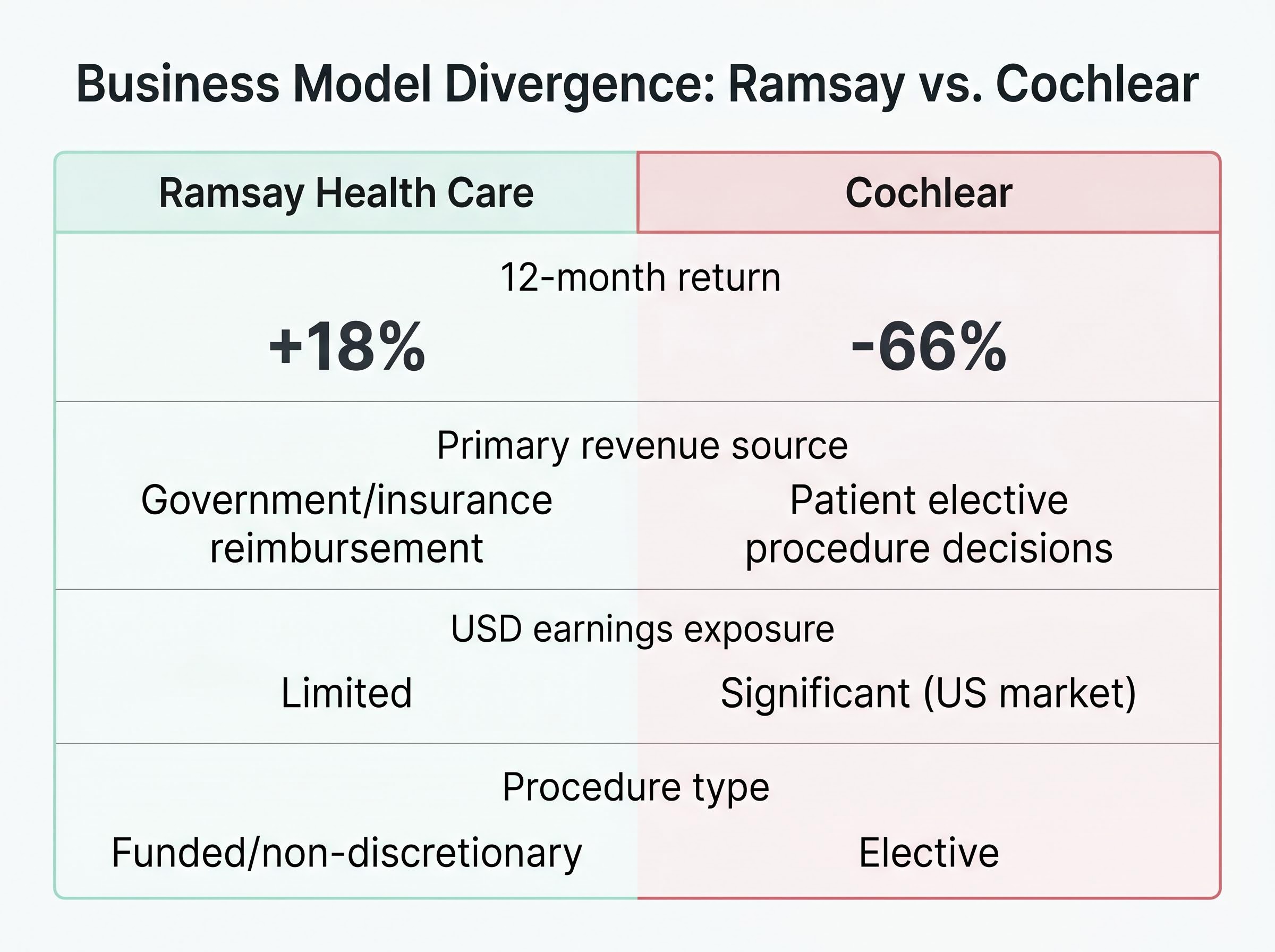

Ramsay Health Care stood at approximately $38.31 as of 5 May 2026, up approximately 18% over 12 months and approximately 21% over six months. It reached an 18-month high of $44.73 in March 2026. It is the sole top-ten healthcare company to post a positive annual return.

While Cochlear fell 66% and CSL fell 51.56% over 12 months, Ramsay Health Care rose 18%, reaching an 18-month high in March 2026.

The structural reasons for Ramsay’s resilience map directly onto the forces destroying value elsewhere. As a hospital operator primarily focused on Australian and European markets, its USD earnings exposure is limited relative to CSL or ResMed, reducing the currency drag. Its revenue model, funded substantially by government and private health insurance reimbursements rather than discretionary patient decisions, provides more stable demand than elective procedure-dependent companies like Cochlear.

| Dimension | Ramsay Health Care | Cochlear |

|---|---|---|

| 12-month return | +18% | -66% |

| Primary revenue source | Government/insurance reimbursement | Patient elective procedure decisions |

| USD earnings exposure | Limited | Significant (US market) |

| Procedure type | Funded/non-discretionary | Elective |

Ramsay’s outperformance is a useful analytical filter: it confirms that the sector’s pain is not uniformly distributed and that business model characteristics (revenue source, currency exposure, procedure type) matter far more than the sector label when assessing individual stock risk during a multi-factor downturn.

Ramsay’s margin expansion in Australian hospital operations, with 40 basis points of improvement reported in the February 2026 half-year results alongside a 6.3% dividend increase, provides the earnings foundation that supports its valuation resilience relative to peers absorbing currency and rate headwinds simultaneously.

The rate environment remains the single largest variable. With the RBA cash rate at 4.35% and a 76% probability of a further hike priced into the next meeting, growth stock valuations face a structural ceiling regardless of company-specific improvements.

If the RBA signals rate cuts or the AUD retreats from its four-year high, the headwinds that mechanically compressed growth stock multiples would ease. That scenario would provide the strongest tailwind for the most beaten-down names, particularly high-multiple stocks like Pro Medicus and Telix. This remains a macro-dependent scenario rather than a company-specific catalyst, and no indication of a near-term pivot is visible in current market pricing.

ResMed’s Q3 FY26 results, released 30 April 2026, beat analyst estimates and demonstrated that fundamental earnings performance can still generate outperformance within a broadly weak sector. Morgans maintains a buy rating with a $47.73 price target (from February 2026) against a current price of approximately $29.78.

The analyst consensus on CSL (12 of 18 analysts buy or strong buy; average target approximately $209.44 versus current $124.83) represents either significant upside or a sign that analyst targets have not yet fully adjusted to the new environment. That gap will narrow from one direction or the other.

The companies hardest hit over the past 12 months share three characteristics:

Ramsay’s resilience reflects the inverse of all three. For investors assessing whether the sector’s pain presents an opportunity or a trap, that divergence, and the gap between analyst targets and current prices, provides a more useful analytical lens than the 39% aggregate decline alone.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The S&P/ASX 200 Health Care Index has declined 39% over the past 12 months due to five compounding forces: RBA rate hikes compressing growth stock valuations, a surging Australian dollar eroding offshore earnings, collapsing consumer confidence reducing demand for elective procedures, corporate governance shocks at CSL, and geopolitical disruption raising costs. No single factor alone explains the magnitude of the decline.

The XHJ is the S&P/ASX 200 Health Care Index, which tracks the performance of ASX-listed healthcare companies. CSL constitutes approximately 45% of the index's weighting, meaning its 51.56% decline over 12 months is the single largest mechanical drag on the headline index figure.

Ramsay's revenue is funded primarily by government and private health insurance reimbursements rather than discretionary patient decisions, making demand more stable. It also has limited USD earnings exposure compared to peers like CSL and ResMed, reducing the currency drag from the surging Australian dollar.

Higher interest rates increase the discount rate applied to future earnings, which reduces the present value of long-dated growth, causing multiple contraction. High-multiple healthcare names like Pro Medicus (down 42.92%) and Telix Pharmaceuticals (down 46.9%) are hit hardest, while lower-multiple names like Sigma Healthcare (down only 8%) show far less sensitivity.

A recovery is most likely if the RBA signals rate cuts or the Australian dollar retreats from its four-year high, which would ease the valuation compression on high-multiple growth stocks. However, with a 76% probability of a further RBA hike priced into the next meeting, no near-term pivot is visible in current market conditions.